- Beauty & Personal Care

- Natural Organic Personal Care Product Market

Natural Organic Personal Care Product Market Size, Share, and Growth Forecast 2026 - 2033

Natural Organic Personal Care Product Market by Product Type (Skin Care, Body Care, Hair Care, Oral Care, Cosmetics, Fragrance & Deodorants), Packaging (Pumps & Dispensers, Compact Cases, Jars, Pencils & Sticks, Tubes, Sachets, Other), Consumer Orientation (Men, Women, Kids), Sales Channel, and Regional Analysis 2026-2033

Natural Organic Personal Care Product Market Size and Trend Analysis

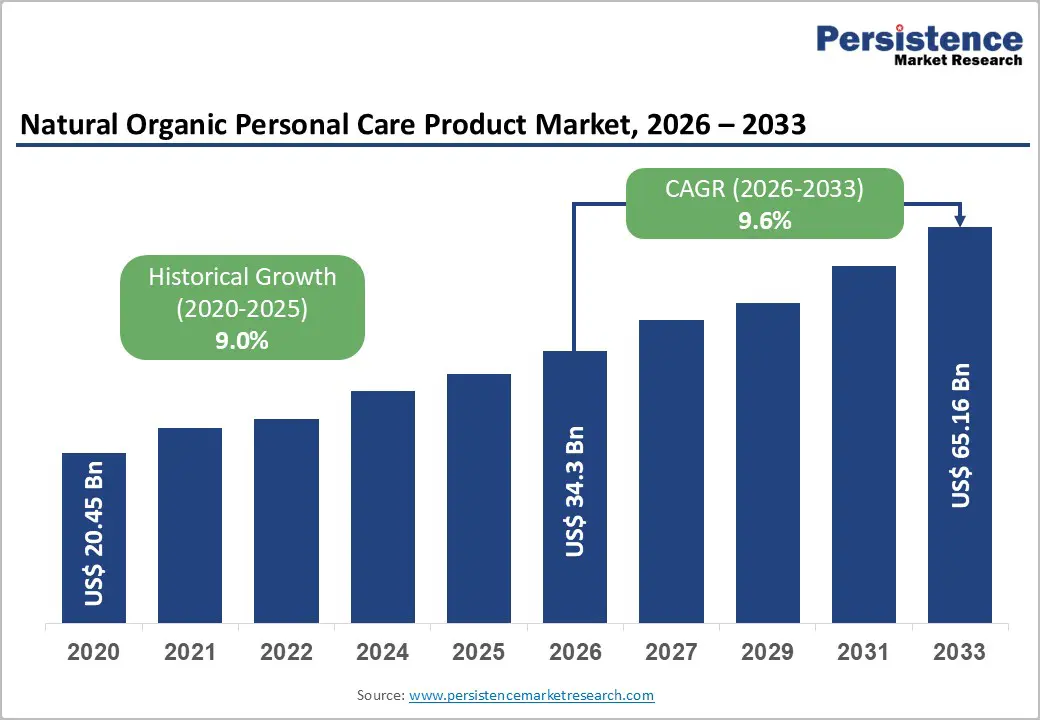

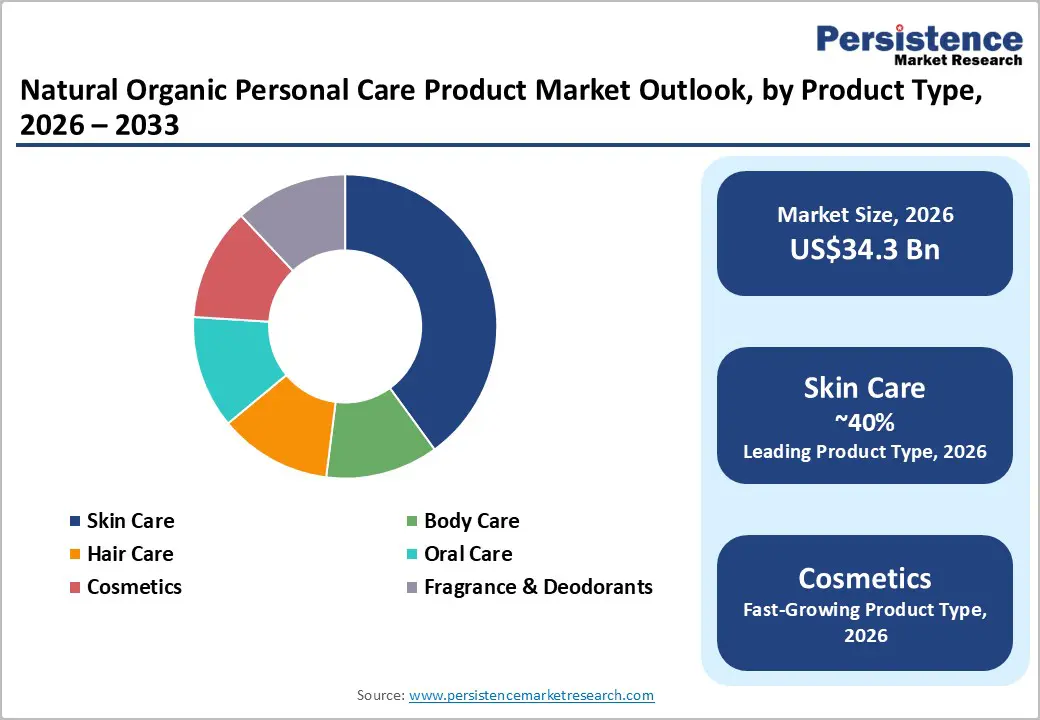

The global natural organic personal care product market size is supposed to be valued at US$ 34.3 Bn in 2026 and is projected to reach US$ 65.2 Bn by 2033, growing at a CAGR of 9.6% between 2026 and 2033.

The market expansion is primarily driven by escalating consumer awareness regarding harmful synthetic chemicals in conventional personal care products, prompting a decisive shift toward organic and natural alternatives. According to NSF International, certified organic personal care products must contain at least 70% organic ingredients by weight, excluding water and minerals, ensuring authenticity and quality assurance for health-conscious consumers. The proliferation of e-commerce channels has revolutionized product accessibility, with online sales of organic personal care products surging by 48% in 2024, now accounting for 62% of total category revenue. Additionally, the clean beauty movement, emphasizing transparency in ingredient sourcing and production processes, continues to gain momentum globally, particularly among millennials and Generation Z consumers who prioritize sustainability, ethical sourcing, and cruelty-free formulations.

Key Market Highlights

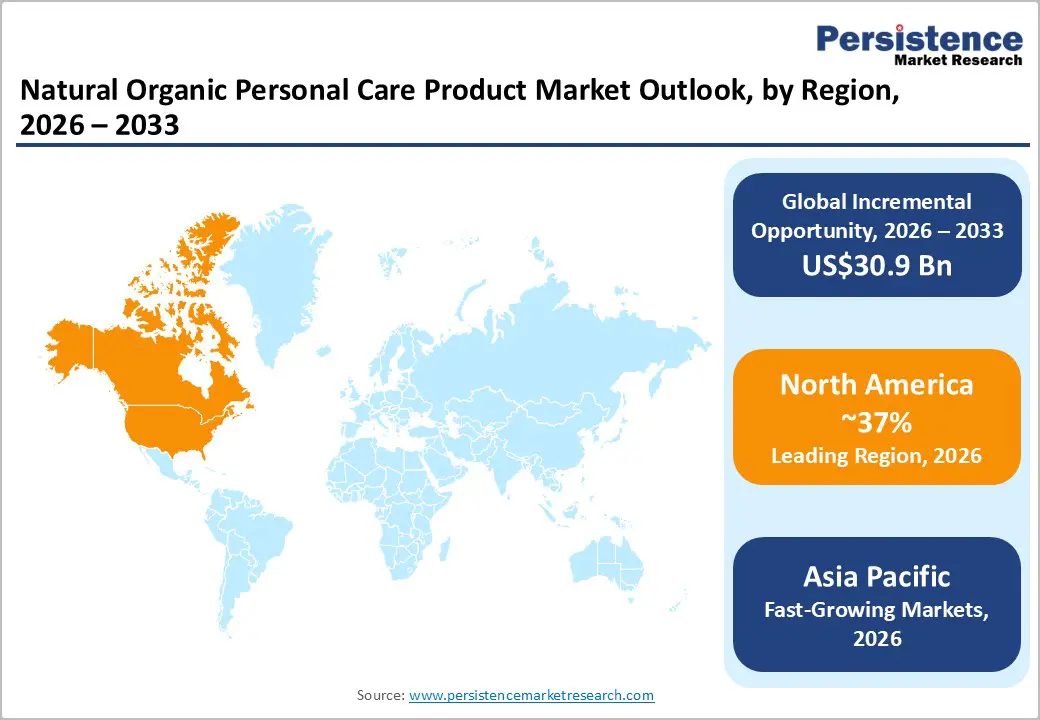

- Leading Region: North America maintains market leadership, with 37% market share, driven by sophisticated consumer awareness, stringent regulatory frameworks including USDA Organic, NSF/ANSI 305, and EWG certifications, and robust innovation ecosystems supported by leading manufacturers including L'Oréal, Estée Lauder, and Johnson & Johnson.

- Fastest Growing Region: Asia-Pacific region demonstrates the highest growth trajectory at 9.0% CAGR, driven by demographic composition emphasizing younger population segments, accelerating disposable income expansion, rapid e-commerce infrastructure development, and cultural receptivity toward natural and traditional botanical formulations, particularly within China, India, Japan, and Southeast Asian markets where population exceeds 2.3 billion consumers.

- Dominant Segment: Skin care products maintain category dominance with approximately 40% market share, reflecting consumer prioritization of comprehensive facial care routines, preventive anti-aging protocols, and specialized formulations addressing distinct skin concerns, including acne, sensitivity, hyperpigmentation, and environmental protection through natural botanical actives.

- Fastest Growing Segment: Online retail channels represent fastest-expanding distribution mechanism with 14.76% CAGR through 2028, driven by digital commerce platform proliferation, social media integration, augmented reality product visualization capabilities, personalized recommendation algorithms, and consumer preference normalization regarding beauty product online purchase methodologies.

- Key Market Opportunity: Waterless and solid cosmetics formulations representing concentrated, sustainable, zero-waste product architectures address escalating consumer environmental consciousness and water conservation priorities, with potential accessible to innovators capable of translating sustainability values into compelling consumer products.

| Report Attribute | Details |

|---|---|

|

Natural Organic Personal Care Product Size (2026E) |

US$ 34.3 Bn |

|

Market Value Forecast (2033F) |

US$ 65.2 Bn |

|

Projected Growth CAGR (2026-2033) |

9.6% |

|

Historical Market Growth (2020-2025) |

9.0% |

Market Dynamics

Market Growth Drivers

Rising Consumer Awareness and Health Consciousness

Heightened consumer awareness of the adverse health implications associated with synthetic chemicals, such as parabens, phthalates, sulfates, and formaldehyde, has driven a significant shift toward natural and organic personal care alternatives. A survey conducted by Prodge Marketing Company in July 2021 revealed that over 34% of U.S. consumers prefer organic beauty products to synthetic variants. Concerns regarding skin irritation, dryness, allergic reactions, and long-term health risks have prompted more rigorous scrutiny of ingredient labels.

Natural components, including pomegranate oil, camellia extract, jojoba oil, argan oil, grape seed extract, vitamin C, hyaluronic acid, and green tea extract, deliver multiple benefits such as hydration, collagen support, skin renewal, and anti-aging properties without synthetic fillers or preservatives. This trend reinforces consumer confidence and strengthens brand loyalty within the organic personal care segment.

Stringent Regulatory Frameworks and Third-Party Certification Standards

The implementation of rigorous organic certification standards has substantially strengthened market credibility and enhanced consumer trust in natural personal care products. The COSMOS (COSMetic Organic Standard), established by leading European certification bodies such as ECOCERT, Soil Association, BDIH, Cosmebio, and ICEA, requires products labeled as COSMOS Organic to contain a minimum of 95% organic materials while prohibiting petrochemicals, genetically modified organisms (GMOs), and synthetic colorants.

In the United States, the NSF/ANSI 305 standard and USDA Organic certification provide comprehensive frameworks governing ingredient sourcing, production processes, and labeling practices. These certifications play a critical role in mitigating greenwashing, promoting environmental sustainability, advancing green chemistry principles, and ensuring responsible resource utilization and biodiversity protection, thereby encouraging manufacturers to invest in organic product development and compliance initiatives.

Market Restraints

Premium Pricing and Cost Constraints

High manufacturing costs remain a significant barrier to the growth of natural and organic personal care products, particularly in price-sensitive markets. The sourcing of certified organic ingredients requires adherence to strict farming practices, sustainable extraction methods, and rigorous quality control, all of which substantially increase production expenses compared to synthetic alternatives.

Additional cost drivers include the extraction of natural oils and botanicals, shorter shelf life, and specialized storage requirements. Compliance with international certification standards such as COSMOS, ECOCERT, NSF/ANSI 305, and EWG Verified further necessitates considerable investment in documentation, auditing, and ongoing monitoring. Consequently, these factors result in premium pricing, limiting accessibility among middle- and low-income consumer segments despite rising awareness of the benefits of organic formulations.

Limited Shelf Life and Distribution Challenges

Natural and organic personal care products generally exhibit a shorter shelf life than synthetic alternatives due to the absence of chemical preservatives and stabilizers. The prohibition of synthetic agents such as parabens, phenoxyethanol, and formaldehyde-releasing compounds in certified organic formulations necessitates reliance on natural preservation systems, such as essential oils, tocopherols, and rosemary extract, which provide limited antimicrobial protection. This limitation increases the need for specialized cold-chain logistics, temperature-controlled storage, and faster inventory turnover, thereby elevating distribution costs and operational complexity.

Retailers face heightened risks of product deterioration and wastage, particularly in regions with inadequate infrastructure or high ambient temperatures. Additionally, maintaining product integrity requires innovative packaging solutions, including airless dispensers, UV-protective containers, and vacuum-sealed formats, which add to manufacturing costs and may restrict design flexibility and brand differentiation.

Market Opportunities

Exponential Growth in E-Commerce and Digital Marketing Platforms

The rapid digital transformation of retail channels has created significant growth opportunities for organic personal care brands. E-commerce has emerged as the fastest-growing distribution segment, with online sales of organic personal care products increasing by 48% in 2024 and accounting for 62% of total category revenue. Platforms such as Amazon, Sephora, and direct-to-consumer websites offer extensive product assortments, transparent ingredient information, customer reviews, and competitive pricing.

Influencer marketing, social media campaigns, subscription models, and AI-driven recommendations enable brands to engage millennials and Generation Z consumers who value authenticity, sustainability, and convenience. The shift toward online shopping, accelerated by the COVID-19 pandemic, has permanently changed purchasing behavior, driving demand for seamless digital experiences. To capitalize, brands must invest in robust digital marketing, influencer partnerships, and omnichannel strategies.

Male Grooming Segment Expansion with Natural and Organic Formulations

The male personal care market is emerging as a significant growth opportunity, driven by the increasing adoption of natural and organic formulations. Factors such as the normalization of male skincare routines, influencer and celebrity advocacy, and heightened awareness of anti-aging benefits are fueling demand within this previously underserved demographic. Research indicates that Generation Z and millennial men strongly favor clean-labeled, vegan, and cruelty-free products, creating distinct value propositions compared to conventional alternatives.

Premium men’s grooming products featuring natural ingredients, such as sandalwood, aloe vera, essential oils, and botanical extracts, command higher price points and foster strong brand loyalty. This growth is further supported by expanding e-commerce channels, targeted digital marketing, and specialized retail formats, with emerging brands like BCOS exemplifying successful strategies through sustainable packaging and male-focused innovation.

Category-wise Insights

Product Type Analysis

The skin care segment holds a dominant position in the natural and organic personal care market, accounting for approximately 40% of the overall share. This leadership reflects strong consumer prioritization of facial and body care solutions addressing concerns such as acne, aging, sensitivity, and environmental protection. Growing emphasis on comprehensive routines, preventive care, and evidence-based formulations drives demand for personalized solutions, as surveys indicate nearly 80% of U.S. skincare users rely on trial-and-error to find suitable products.

Innovation in natural skin care focuses on clinically validated botanical actives, including vitamin C, niacinamide, retinol alternatives, peptides, and hyaluronic acid, supporting barrier repair and collagen synthesis. Market growth is further reinforced by consumer preference for transparent ingredient sourcing, dermatological validation, and sustainable packaging, with a willingness to pay premium prices for efficacy and environmental responsibility.

Packaging Analysis

Pumps and dispensers dominate the packaging segment in the natural and organic personal care market, accounting for approximately 35% of market share. Their popularity stems from superior product preservation, precise portion control, and enhanced consumer convenience. Dispenser-based designs minimize exposure to air and contaminants, extending shelf life for formulations with minimal synthetic preservatives. This preference reflects consumer demand for hygienic application, reduced waste, and premium aesthetics.

Furthermore, sustainable innovations, such as recycled materials, refillable systems, and minimalist designs, address growing environmental concerns while maintaining functionality. Alternative formats, including glass jars, tubes, sachets, and pencil sticks, serve specialized needs such as jars for creams, sachets for travel and sampling, and sticks for precise cosmetic application. The evolving packaging landscape increasingly prioritizes multi-material sustainability solutions that balance product protection with eco-friendly objectives.

Consumer Orientation Analysis

Women constitute the dominant consumer demographic in the natural and organic personal care market, representing approximately 52% of overall participation. This leadership is driven by heightened awareness of ingredient safety, environmental sustainability, and willingness to invest in premium skincare and cosmetic products. Female consumers exhibit a sophisticated understanding of ingredient functionality, regulatory compliance, and brand positioning, with strong emphasis on transparency, ethical sourcing, and alignment with wellness values. This trend reflects cultural shifts toward female empowerment, informed decision-making, and social media-driven beauty education, supported by increased disposable income.

In contrast, the male segment is the fastest-growing demographic, projected to achieve an 11.9% CAGR through 2033, as skincare routines become normalized and grooming categories gain traction. Children’s personal care is also expanding, with specialized, hypoallergenic formulations meeting parental demand for safe, chemical-free products.

Sales Channel Analysis

Online retailers have emerged as the fastest-growing distribution channel for natural and organic personal care products, accounting for approximately 41% of market sales in developed economies, with continued acceleration expected throughout the forecast period. Digital commerce platforms, including direct-to-consumer websites, major e-commerce marketplaces such as Amazon, Sephora, and Nykaa, and social commerce platforms like TikTok Shop and Instagram Shopping, offer extensive product variety, transparent ingredient information, personalized recommendations, and competitive pricing.

This growth reflects sustained digital transformation, widespread consumer acceptance of online beauty purchases, and improved logistics enabling rapid fulfillment. Specialty stores remain significant, capturing 35–40% of market share through curated selections and professional consultations, while hypermarkets and supermarkets hold 30–35% due to accessibility and competitive pricing. Pharmacy and departmental stores maintain stable performance, particularly in premium and dermatology-focused categories.

Regional Insights

North America Natural Organic Personal Care Trends

The North American market, led by the United States, reflects a mature landscape characterized by advanced consumer preferences, stringent regulatory standards, and a dynamic innovation ecosystem. The U.S. holds approximately 68.5% of the regional share, driven by heightened awareness of harmful chemicals in conventional products, high disposable income, and robust retail infrastructure supporting natural and organic categories.

Regulatory measures, including the FDA’s Modernization of Cosmetics Regulation Act (MoCRA) introduced in 2022, have strengthened compliance, transparency, and safety requirements, while USDA Organic certification provides standards for agricultural ingredients despite the absence of FDA regulation for the term “organic.” Consumers increasingly favor clean beauty formulations emphasizing transparency, clinical validation, and sustainable packaging. E-commerce penetration has reached 41% of beauty sales, projected to rise to 50% by 2030, supported by biotech-driven innovations and convergence between mass-market and prestige segments.

Europe Natural Organic Personal Care Trends

Europe stands as the global hub for natural and organic cosmetics adoption, driven by stringent regulatory harmonization, strong environmental consciousness, and a well-established certification framework. The European natural cosmetics market was reflecting sustained demand for chemical-free, sustainably sourced formulations. Germany leads the region, with 52% of consumers using natural beauty products and sustainability influencing over 70% of purchasing decisions. The country also dominates certification, with 2,596 COSMOS-certified and 3,932 NATRUE-certified products, the highest global concentration.

France follows with 17,054 COSMOS-certified products, representing 48% of global certifications, while the U.K. shows strong growth potential at 7.4% CAGR through 2035. Regulation (EC) No. 1223/2009 enforces ingredient transparency, bans animal testing, and drives innovation in botanical extraction, fermentation biotechnology, and preservative systems, positioning Europe as a leader in sustainable beauty innovation.

Asia Pacific Natural Organic Personal Care Trends

Asia-Pacific is the fastest-growing regional market for natural and organic personal care products, driven by its large, youthful demographic base and rapid e-commerce adoption. The region accounts for approximately 39.5% of the global beauty and personal care market and is projected to expand at a 9.0% CAGR, significantly outpacing mature markets. China leads with 32.3% share, supported by over 700 million internet users, advanced digital commerce platforms such as Taobao Live, Xiaohongshu, and WeChat, and government initiatives promoting domestic cosmetics innovation.

Indian growth is fueled by a young population, cultural preference for Ayurvedic and herbal formulations, and increasing online accessibility through platforms like Amazon, Flipkart, and Nykaa. Japan demonstrates market maturity with strong demand for premium natural formulations aligned with K-beauty and J-beauty trends. Southeast Asian markets, including Thailand, Vietnam, Indonesia, and the Philippines, show accelerated adoption of multi-step skincare routines and premium organic products, amplified by social media influence and rising disposable incomes.

Competitive Landscape

Market Structure Analysis

The natural and organic personal care market is characterized by a fragmented competitive structure comprising multinational corporations, specialized natural beauty brands, and emerging digital-native companies with distinct positioning strategies. Leading conglomerates such as L’Oréal, Estée Lauder, Unilever, Shiseido, Beiersdorf, LVMH, Procter & Gamble, Coty Inc., Kao Corporation, and Johnson & Johnson maintain strong market presence through diversified portfolios spanning mass-market, prestige, and luxury segments. Meanwhile, indie and digital-native brands focused on sustainability, transparency, and social commerce exhibit disruptive potential. Consolidation is accelerating via mergers and acquisitions, with major players prioritizing proprietary biotechnology, patented ingredients, and clinically validated efficacy to secure competitive advantages and counter commoditization pressures.

Key Market Developments

- January 2025: L'Oréal Groupe introduced revolutionary skin analysis technology at CES 2025 in Las Vegas, featuring a portable device providing personalized skin assessment in five minutes through advanced proteomics analysis.

- September 2023: Shiseido Company, Limited commenced full-scale operations of an innovative inner beauty business segment through brand launch SHISEIDO BEAUTY WELLNESS, representing corporate expansion into wellness market integration, combining beauty with nutritional supplementation.

- February 2024: Kao Corporation introduced The Answer, premium hair care brand demonstrating corporate commitment to premium market segment penetration and advanced scientific formulation positioning.

Top Companies in Natural Organic Personal Care Market

L'Oréal S.A. (Paris, France) maintains a global leadership position within the natural organic personal care market through a diversified brand portfolio including luxury, prestige, and mass-market segments. The corporation demonstrates substantial commitment to natural and organic formulation innovation through acquisitions of specialty brands, including Youth to the People and proprietary biotech partnerships with innovation suppliers, including Geno, Evola, and NanoEnTek. L'Oréal's research and development capabilities, encompassing advanced formulation science, ingredient sourcing innovation, and sustainability implementation, position the company as an industry innovation leader within natural cosmetics advancement.

Estée Lauder Companies Inc. (New York, U.S.) maintains substantial market presence through diversified luxury, prestige, and specialized brand portfolios emphasizing premium positioning and clinical efficacy validation. The company's acquisition of Deciem for substantial capital investment demonstrates a strategic commitment to science-backed natural formulation innovation and digital-direct-to-consumer channel development. Estée Lauder's portfolio diversification across luxury prestige and emerging digital-native brands enables comprehensive market coverage, addressing demographic and price-point segmentation across consumer populations.

Kao Corporation (Tokyo, Japan) demonstrates particular strength within Asian personal care markets through established brand recognition, advanced research and development capabilities, and consumer trust accumulation spanning decades. The company's innovation focus emphasizing natural ingredients, skin science advancement, and cultural alignment with Japanese beauty principles positions Kao as dominant regional competitor. Kao's portfolio including premium brands such as Kanebo, Suqqu, and mass-market offerings demonstrates segmented market coverage strategies addressing diverse consumer preferences and purchasing power demographics throughout Asia-Pacific and emerging international markets.

Companies Covered in Natural Organic Personal Care Product Market

- L'Oréal S.A.

- Amway Corporation

- Beiersdorf

- Benefit Cosmetics LLC

- Chanel S.A.

- Clarins Group

- Coty Inc.

- Estee Lauder Companies Inc.

- Johnson & Johnson

- Kao Corporation

- Laverana GmbH & Co. KG

- LVMH (Möet Hennessy Louis Vuitton)

- MAC Cosmetics

- Mary Kay Cosmetics

- Shiseido Co., Ltd.

Frequently Asked Questions

The global natural organic personal care product market is projected to reach US$ 65.2 Bn by 2033, expanding from US$ 34.3 Bn in 2026, representing a 90.1% absolute value expansion and 9.6% CAGR growth trajectory driven by sustained consumer demand for chemical-free, sustainably-sourced personal care formulations.

Market growth is predominantly catalyzed by escalating consumer health consciousness regarding synthetic chemical exposure risks, expanding environmental sustainability values, digital commerce proliferation enabling product accessibility, social media-driven beauty education dissemination, regulatory harmonization emphasizing transparency and safety, and emerging market penetration with younger demographic cohorts prioritizing natural formulations and ethical sourcing practices.

Skin care products dominate the natural organic personal care market with approximately 40% market share, driven by consumer prioritization of comprehensive facial care routines, preventive anti-aging protocols, and scientifically-validated formulations incorporating natural botanical actives addressing diverse skin concerns, including acne, aging, sensitivity, and environmental protection.