- Biotechnology

- Europe Personalized Medicine Biomarkers Market

Europe Personalized Medicine Biomarkers Market Size, Share, and Growth Forecast, 2026 - 2033

Europe Personalized Medicine Biomarkers Market by Indication (Medium Commercial Vehicle, Heavy Duty Commercial Vehicle, and Buses & Coaches) Application (Diesel, Petrol, Electrically-Chargeable (ECV), Others) for 2026 - 2033

Europe Personalized Medicine Biomarkers Market Size and Trends Analysis

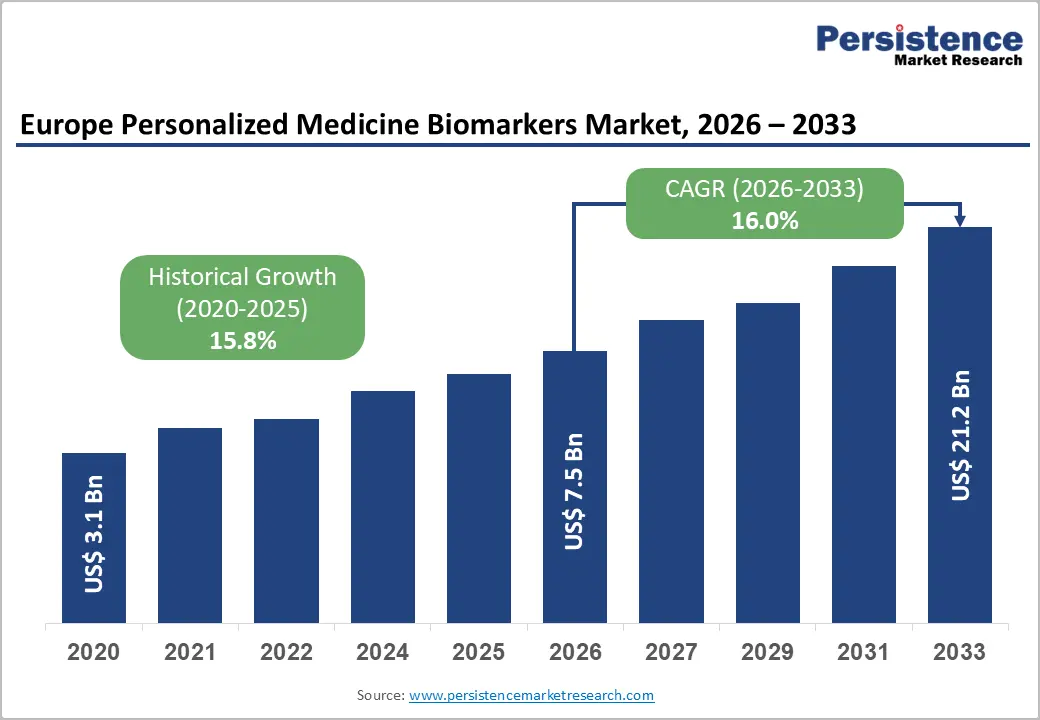

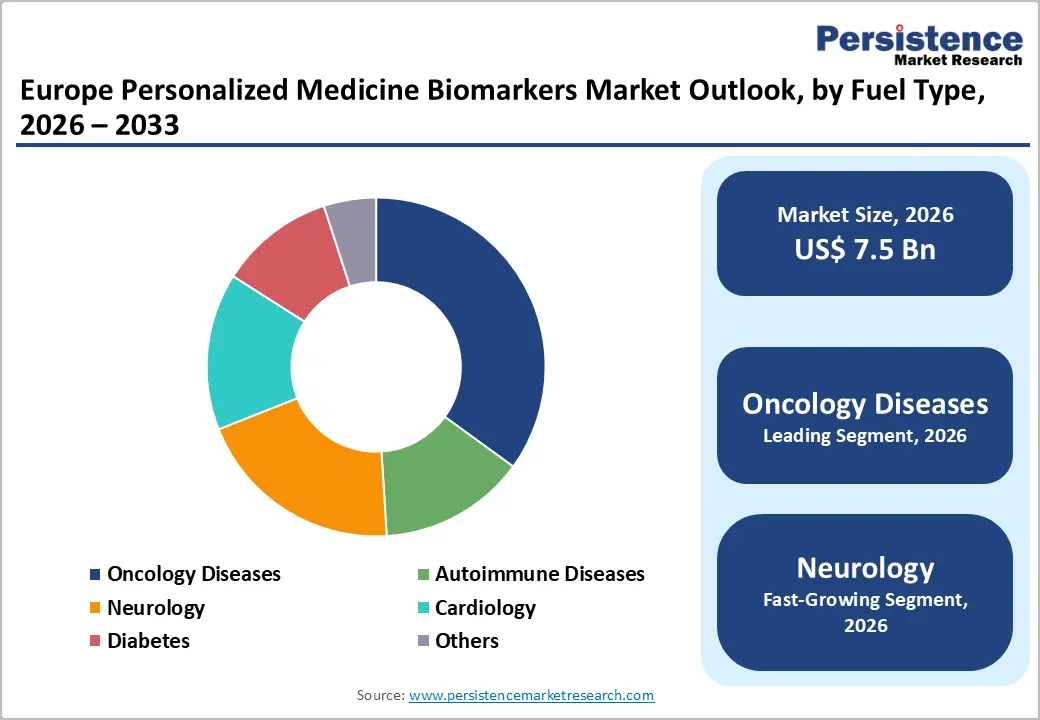

The Europe personalized medicine biomarkers market size is likely to be valued at US$7.5 billion in 2026 and is expected to reach US$21.2 billion by 2033, growing at a CAGR of 16.0% during the forecast period from 2026 to 2033, driven by rising adoption of precision oncology, liquid biopsy technologies, and next-generation sequencing across major healthcare systems.

According to the European Medicines Agency, pharmacogenomics and multi-omics integration are increasingly supporting personalized treatment approaches across Europe. Rising adoption of targeted therapies, companion diagnostics, liquid biopsy technologies, and AI-driven biomarker analysis, along with growing investments in biotechnology research and supportive regulatory initiatives, is accelerating innovation and strengthening biomarker-based precision medicine.

Key Industry Highlights:

- Leading Product Type: Oncology diseases are projected to represent the leading product type in 2026, accounting for 38% of the revenue share, driven by the extensive use of companion diagnostics and precision oncology therapies.

- Leading Indication: Diagnosis is anticipated to be the leading indication type, accounting for over 45% of the revenue share in 2026, supported by growing integration of biomarker-guided clinical decision-making.

- Key Opportunity: A key opportunity in the Europe personalized medicine biomarkers market is the rapid expansion of AI-enabled multi-omics integration and liquid biopsy, based precision diagnostics, enabling earlier disease detection, highly personalized treatment strategies, and large-scale adoption of predictive healthcare across oncology and chronic diseases.

DRO Analysis

Driver - Increasing Demand for Targeted Therapies and Companion Diagnostics

The increasing demand for targeted therapies and companion diagnostics across oncology, cardiology, and autoimmune disease treatment. Healthcare providers are increasingly adopting biomarker-guided therapies to improve treatment precision, reduce adverse drug reactions, and enhance patient outcomes. Companion diagnostics play a critical role in identifying patient populations most likely to respond to specific therapies, particularly in cancer care. The growing prevalence of chronic diseases and rising investments in genomic research are accelerating biomarker utilization.

Pharmaceutical companies are also collaborating with diagnostic developers to support precision medicine initiatives and strengthen personalized treatment strategies throughout European healthcare systems. Advancements in molecular diagnostics, next-generation sequencing, and liquid biopsy technologies are supporting the adoption of personalized medicine biomarkers in Europe. Hospitals and research institutions are integrating biomarker testing into routine clinical workflows to support individualized treatment decisions and disease monitoring.

Regulatory support from European healthcare authorities for precision medicine programs is encouraging broader use of companion diagnostics in clinical practice. Increasing awareness among healthcare professionals regarding the benefits of biomarker-based therapies is driving market expansion. The growing number of targeted drug approvals and clinical trials involving biomarker-guided therapies continues to reinforce the importance of personalized medicine across Europe’s healthcare and biotechnology sectors.

Restraint - Reimbursement and Accessibility Disparities

Several European countries continue to face challenges related to inconsistent reimbursement policies for biomarker testing and companion diagnostics. Limited insurance coverage and high costs associated with advanced genomic testing restrict patient access to personalized treatment approaches, particularly in developing healthcare systems within Eastern and Southern Europe. Variations in healthcare infrastructure and diagnostic capabilities also contribute to unequal adoption of precision medicine technologies across the region.

Differences in regulatory frameworks, laboratory standardization, and healthcare funding mechanisms across European nations complicate market expansion. Many healthcare providers face difficulties in implementing large-scale biomarker testing due to budget constraints and limited availability of specialized diagnostic facilities. The lack of harmonized reimbursement pathways for innovative molecular diagnostics reduces investment incentives for biotechnology companies and diagnostic manufacturers. Rural and underserved populations often experience reduced access to advanced personalized medicine services, creating healthcare inequalities.

Opportunity - Expansion of AI/ML and Multi-Omics Integration

The expansion of artificial intelligence (AI), machine learning (ML), and multi-omics integration presents significant growth opportunities for the Europe personalized medicine biomarkers market. AI-powered analytics are increasingly being used to process complex genomic, proteomic, and metabolomic datasets, enabling faster and more accurate biomarker discovery. Multi-omics approaches improve disease understanding by combining data from multiple biological pathways, supporting highly personalized treatment strategies. These technologies are enhancing diagnostic precision, accelerating drug development, and improving predictive disease modeling across oncology, neurology, and autoimmune disorders.

Research institutions and biotechnology companies are heavily investing in AI-driven biomarker platforms to strengthen precision medicine capabilities throughout the European healthcare ecosystem. Growing collaborations between pharmaceutical companies, bioinformatics firms, and academic research organizations are accelerating innovation in AI-enabled biomarker development. Machine learning algorithms are improving patient stratification, treatment response prediction, and clinical trial optimization, helping healthcare providers deliver more individualized therapies.

The increasing use of cloud computing and digital health infrastructure is supporting real-time biomarker analysis and large-scale genomic data management. European government initiatives promoting digital healthcare transformation and precision medicine research are encouraging the adoption of advanced analytical technologies. The increasing adoption of digital pathology and real-world evidence platforms is creating new opportunities for AI-driven biomarker validation and clinical decision support. Expansion of biobank networks and genomic databases across Europe is improving access to large-scale patient datasets for biomarker research.

Category-wise Analysis

Indication Insights

Oncology diseases are expected to lead the Europe personalized medicine biomarkers market, accounting for approximately 38% of revenue in 2026, driven by the increasing adoption of targeted cancer therapies, companion diagnostics, and precision oncology programs across major European healthcare systems.

The high prevalence of breast cancer, lung cancer, and colorectal cancer has significantly increased demand for biomarker-based diagnostics and treatment selection tools. A notable example includes Roche Diagnostics, which continues to expand its oncology biomarker portfolio and companion diagnostic solutions across Europe to support personalized cancer treatment strategies. Biomarkers such as HER2, EGFR, and PD-L1 are widely used to support personalized therapy decisions and improve clinical outcomes in oncology care.

Neurology is likely to represent the fastest-growing segment, supported by the rising prevalence of neurodegenerative disorders, increasing biomarker research activities, and growing demand for personalized neurological treatments. Conditions such as Alzheimer’s disease, Parkinson’s disease, and multiple sclerosis are driving the need for advanced biomarker-based diagnostics capable of enabling early disease detection and monitoring.

Advancements in neurogenomics, proteomics, and cerebrospinal fluid biomarker analysis are improving understanding of disease progression and treatment response. For example, Illumina, which supports neurological biomarker research through advanced sequencing technologies used in precision medicine and neurogenomic studies across European healthcare and research institutions.

Application Insights

Diagnosis is projected to lead the market, capturing around 45% of the revenue share in 2026, supported by the growing integration of biomarker-based testing into routine clinical practice. Biomarkers are increasingly used for disease identification, patient stratification, and therapy planning across oncology, cardiology, neurology, and autoimmune disorders. The rising adoption of molecular diagnostics and next-generation sequencing technologies has improved diagnostic accuracy and enabled more personalized treatment approaches.

Healthcare providers are emphasizing early and precise diagnosis to improve patient outcomes while reducing unnecessary treatments and healthcare costs. Increasing support from European healthcare authorities for precision diagnostics is accelerating adoption across hospitals and diagnostic laboratories. For instance, Qiagen, which provides advanced molecular diagnostic and companion diagnostic solutions widely used in Europe for biomarker-driven disease diagnosis and precision treatment decision-making.

The early detection and screening segment is likely to be the fastest-growing application, driven by increasing focus on preventive healthcare and rising adoption of liquid biopsy technologies. Biomarker-based screening tools are gaining strong demand for identifying diseases at earlier stages, particularly in oncology and neurological disorders, where early intervention significantly improves treatment outcomes.

Technological advancements in non-invasive diagnostics, genomic testing, and AI-driven biomarker analysis are enhancing the effectiveness of early disease detection programs across Europe. Increasing awareness regarding preventive medicine and personalized healthcare is encouraging broader adoption of biomarker-based screening approaches in clinical settings. For example, Guardant Health which has expanded its liquid biopsy-based cancer screening and early detection solutions to support precision oncology and non-invasive diagnostic applications across European markets.

Competitive Landscape

The Europe personalized medicine biomarkers market exhibits a moderately fragmented structure, driven by rapid advancements in genomics, molecular diagnostics, liquid biopsy technologies, and precision medicine research across the region. The competitive environment is shaped by increasing collaborations between biotechnology companies, pharmaceutical manufacturers, diagnostic laboratories, and research institutions to strengthen biomarker discovery and companion diagnostic development.

Rising demand for targeted therapies and personalized treatment approaches in oncology, neurology, and autoimmune diseases is encouraging companies to expand their biomarker portfolios and invest in next-generation sequencing and AI-driven diagnostic platforms.

With key leaders, including Roche Diagnostics, Illumina, Inc., Guardant Health, Qiagen, Agilent Technologies, Bio-Rad Laboratories, Foundation Medicine, NeoGenomics Laboratories, and Quest Diagnostics Incorporated, the market continues to witness strong technological and strategic developments. These players compete through advanced genomic sequencing technologies, companion diagnostic innovations, strategic partnerships, research collaborations, and expansion of precision oncology testing capabilities across European healthcare systems.

Companies are increasingly focusing on AI-powered biomarker analysis, multi-omics integration, and non-invasive diagnostic solutions to improve clinical efficiency and patient outcomes.

Key Industry Developments:

- In May 2026, InsideTracker announced the launch of its new AI-powered health platform designed to deliver hyper-personalized wellness guidance at scale for consumers and enterprise partners. The platform integrates biomarker data, wearable inputs, genetic information, and lifestyle metrics to generate individualized health insights and actionable recommendations.

- In September 2025, Quest Diagnostics announced the expansion of its Alzheimer’s disease diagnostics portfolio through its AD-Detect™ blood testing program, aimed at improving clinical confirmation of Alzheimer’s disease in patients with cognitive impairment. The new blood-based test utilizes multiple biomarkers, including amyloid beta and phosphorylated tau proteins, to assess Alzheimer’s-related brain pathology with high diagnostic accuracy.

Companies Covered in Europe Personalized Medicine Biomarkers Market

- Laboratory Corporation of America Holding

- Quest Diagnostics Incorporated

- Agilent Technologies, Inc.

- Genome Medical, Inc.

- Coriell Life Sciences.

- Roche Diagnostics

- NeoGenomics Laboratories

- FOUNDATION MEDICINE, INC.

- Illumina, Inc.

- Guardant Health

- PerkinElmer

- Bio-Rad Laboratories

- GE Healthcare

- Qiagen

Frequently Asked Questions

The Europe personalized medicine biomarkers market is projected to reach US$7.5 billion in 2026.

The Europe personalized medicine biomarkers market is driven by the rising adoption of precision medicine, increasing demand for targeted therapies, and expanding use of biomarker-based diagnostics in oncology and chronic disease management.

The Europe personalized medicine biomarkers market is expected to grow at a CAGR of 16.0% from 2026 to 2033.

Key market opportunities in the Europe personalized medicine biomarkers market lie in the expansion of AI-driven biomarker analysis, multi-omics research, liquid biopsy technologies, and growing adoption of personalized healthcare across oncology, neurology, and preventive medicine applications.

Laboratory Corporation of America Holding, Quest Diagnostics Incorporated, and Agilent Technologies, Inc. are the leading players.