- Healthcare Services

- Personalized Medicine Biomarkers Market

Personalized Medicine Biomarkers Market Size, Share, and Growth Forecast, 2026 - 2033

Personalized Medicine Biomarkers Market by Biomarker Type (Genomic, Proteomics, Metabolic, Others), Application (Disease Diagnosis, Drug Discovery & Development, Others), Disease Indication (Oncology, Neurology, Diabetes, Autoimmune diseases, Cardiology, Others), and Regional Analysis for 2026 - 2033

Personalized Medicine Biomarkers Market Size and Trends Analysis

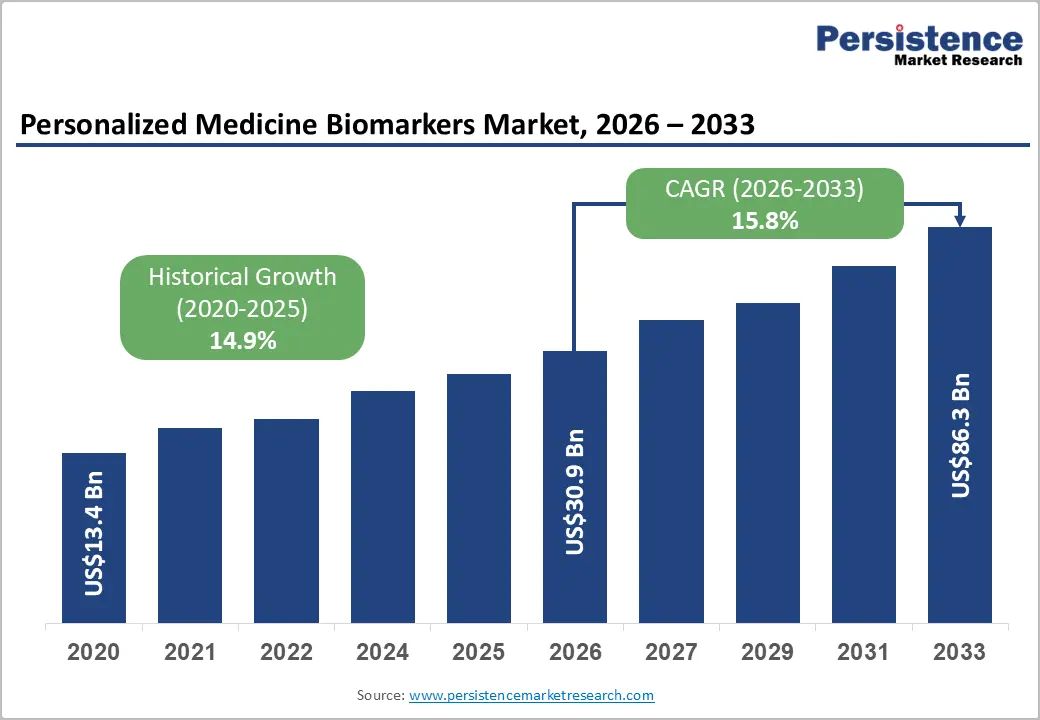

The global personalized medicine biomarkers market size is likely to be valued at US$30.9 billion in 2026 and is expected to reach US$86.3 billion by 2033, growing at a CAGR of 15.8% during the forecast period from 2026 to 2033, driven by precision-driven clinical decision frameworks across chronic and complex diseases.

Demographic shifts toward aging populations increase the demand for early detection tools. Regulatory alignment across major healthcare systems strengthens clinical adoption pathways. Technology adoption in next-generation sequencing and multiplex assay platforms improves diagnostic accuracy.

Key Industry Highlights:

- Leading Biomarker Type: Genomic biomarkers are set to hold approximately 38% revenue share in 2026, driven by companion diagnostic integration in oncology drug approvals.

- Fastest-growing Biomarker Type: Metabolic biomarkers are projected to be the fastest-growing segment, supported by rising diabetes prevalence and wearable metabolite monitoring adoption.

- Leading Disease Indication: Oncology is estimated to hold approximately 42% revenue share in 2026, driven by deep integration of validated biomarker panels in targeted therapy and immunotherapy protocols.

- Fastest-Growing Indication: Neurology is forecast to record the fastest growth, driven by blood-based Alzheimer's biomarker approvals opening population-scale screening markets.

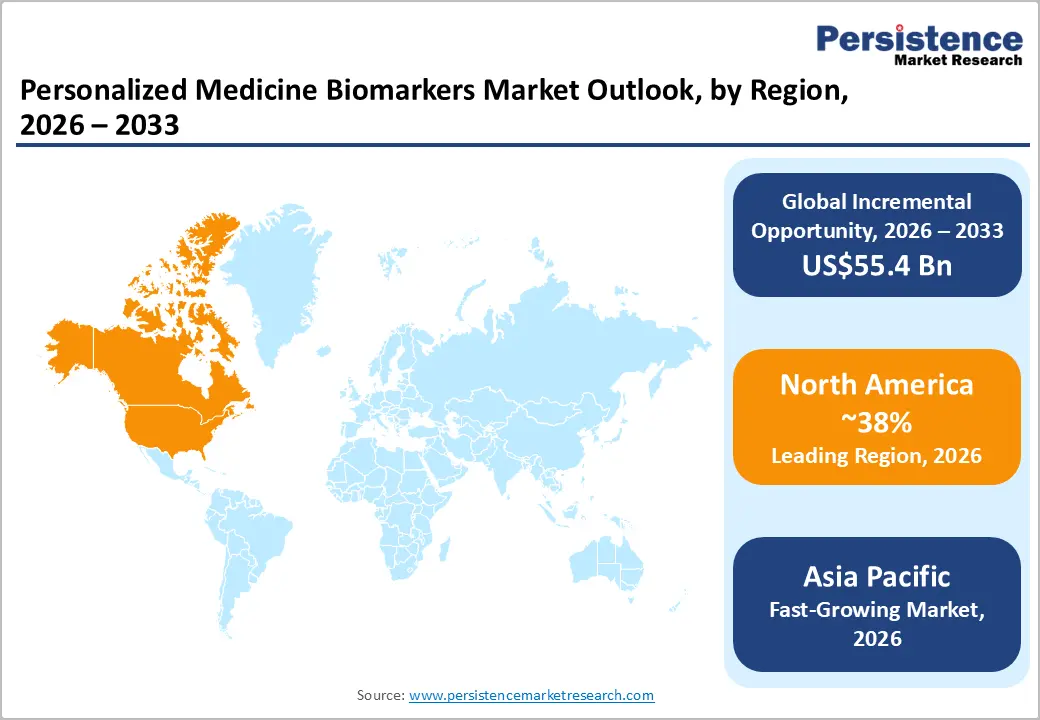

- Regional Leadership: North America is projected to capture roughly 38% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth due to rapid clinical laboratory infrastructure expansions.

DRO Analysis

Driver - Expansion of Precision Oncology Programs

Rising integration of precision oncology into clinical workflows increases reliance on biomarker-based diagnostics for therapy selection and patient stratification. Oncology care shifts toward genomic and proteomic profiling to match targeted treatments with molecular tumor profiles. Hospital systems expand molecular testing capacity to support decision-driven treatment pathways. Pharmaceutical alignment with companion diagnostics strengthens demand for validated biomarker panels across clinical applications and therapeutic development programs.

Clinical decision frameworks increasingly depend on molecular-level insights for oncology management. Diagnostic laboratories scale sequencing infrastructure to support rising test volumes linked to targeted therapy eligibility. Regulatory pathways support broader adoption of companion diagnostics in treatment protocols. This structural shift strengthens demand for validated biomarkers across clinical trials and routine patient care.

Restraint - Fragmented Institutional Reimbursement Frameworks

The absence of standardized, cross-border reimbursement coverage creates structural friction that limits the adoption of newly approved diagnostic assays. Health insurance providers and national health systems utilize varying evaluation criteria to determine the clinical-economic value of multi-gene panels. Because payers often demand long-term survival data before granting positive coverage determinations, standard clearance frequently lags behind regulatory approval by several years. This systemic delay forces healthcare providers to choose between out-of-pocket patient billing and absorbing testing costs internally.

This financial disconnect directly reduces the addressable commercial space for cutting-edge companion testing options. Diagnostic manufacturers cannot scale production volumes effectively when product utilization remains restricted by localized, piecemeal coverage policies. The resulting cash-flow constraints suppress long-term research and development budgets, delaying the commercialization of secondary pipelines. Without predictable, widespread insurance coverage, institutional purchasing departments decline to invest in the specialized training and instrumentation required for workflow implementation.

Opportunity - Liquid Biopsy and Non-Invasive Longitudinal Monitoring

The transition from invasive tissue extraction to blood-based circulating biomarker isolation provides a clear avenue for sustained market expansion. Liquid biopsy techniques enable the capture of circulating tumor DNA, exosomes, and cell-free RNA from standard peripheral blood draws. This non-invasive methodology permits clinicians to perform serial sampling throughout the treatment continuum without subjecting patients to repetitive, painful surgical procedures. Healthcare organizations can monitor real-time clonal evolution, therapeutic response, and minimal residual disease with minimal clinical risk.

The capability to detect early molecular resistance before structural disease progression appears on conventional imaging scans creates a substantial commercial opening. Pharmaceutical developers can leverage longitudinal cell-free monitoring to adjust targeted therapy dosages or switch to secondary therapeutic options during clinical testing phases. Diagnostic companies that establish proprietary, highly sensitive liquid biopsy assays stand to capture significant recurring revenue streams through continuous surveillance pricing models. This technology shift redefines the clinical workflow from a single diagnostic event into an ongoing management protocol.

Category-wise Analysis

Biomarker Type Insights

Genomic biomarkers are expected to lead the personalized medicine biomarkers market, accounting for approximately 38% of the revenue share in 2026. The FDA's approval of Foundation Medicine's FoundationOne CDx as a pan-tumor companion diagnostic demonstrates clinical acceptance. Genomic panels deliver actionable mutation data that directly governs chemotherapy and targeted therapy selection, cementing dominance.

Metabolic biomarkers are likely to represent the fastest-growing segment, propelled by rising diabetes and metabolic syndrome prevalence. Platforms such as Metabolon's HD4 metabolomics panel are enabling clinicians to stratify therapeutic response in type 2 diabetes patients. Wearable metabolite monitoring integration is further accelerating adoption in ambulatory care settings.

Application Insights

Disease diagnosis is projected to lead the market, capturing around 32% of the revenue share in 2026. Roche's cobas EGFR Mutation Test exemplifies validated diagnostic biomarker deployment in clinical pathology. The volume of biomarker-guided diagnostic decisions in oncology and cardiology sustains dominant revenue concentration within this application.

Treatment selection is likely to be the fastest-growing segment, fueled by expansion in immuno-oncology. Keytruda's PD-L1 companion diagnostic requirement has established precedent for mandatory biomarker testing prior to therapy initiation. Regulatory agencies in the U.S. and EU are reinforcing this model across an expanding roster of therapeutic approvals.

Disease Indication Insights

Oncology is likely to be the leading segment with a projected 42% of the personalized medicine biomarkers market share in 2026 due to the deep integration of companion diagnostics into cancer therapy approval pathways. Illumina's TruSight Oncology 500 panel illustrates the commercial scale of genomic biomarker deployment across solid tumor indications globally.

Neurology is anticipated to be the fastest-growing segment, fueled by the clinical validation of cerebrospinal fluid and blood-based biomarkers for Alzheimer's disease. The FDA's clearance of Lumipulse for plasma phospho-tau quantification has created a new blood-based Alzheimer's diagnostic category, expanding addressable volumes in symptomatic clinical contexts, though it remains restricted from general asymptomatic screening.

Regional Insights

North America Personalized Medicine Biomarkers Market Trends

North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by high concentrations of pioneering biotechnology firms and robust corporate venture capital inflows. The systematic integration of multi-omic profiling platforms within major clinical networks accelerates local growth.

U.S. Personalized Medicine Biomarkers Market Insights

The U.S. is projected to command an 85% share of the regional revenue in 2026 due to continuous federal research funding injections. Government initiatives expanding precision oncology reference databases accelerate the validation of rare genetic variant indicators. Prominent domestic players focus on establishing strategic collaborations with contract research organizations to shorten companion assay development cycles.

Canada Personalized Medicine Biomarkers Market Insights

Canada is forecast to capture a 15% share of the regional market in 2026, driven by public healthcare infrastructure modernization programs. National provincial health authorities are increasingly incorporating liquid biopsy testing options into standard oncology management pathways to reduce surgical hospital burdens. This public procurement strategy encourages local diagnostic developers to scale up assay manufacturing operations.

Europe Personalized Medicine Biomarkers Market Trends

Europe is expected to secure a 29% share of the global market in 2026, supported by centralized regulatory framework updates that streamline cross-border diagnostic validations. European research institutions are increasingly participating in international consortia aimed at mapping proteomic signatures for rare pathologies.

Germany Personalized Medicine Biomarkers Market Insights

Germany is likely to lead the European sector with an expected regional market share of 24% in 2026 due to an advanced laboratory automation manufacturing landscape. Domestic industrial groups are actively launching high-capacity fluidic systems that reduce manual handling errors during delicate genetic assay preparation steps. This technical capability attracts international biopharmaceutical firms seeking reliable clinical trial testing sites.

U.K. Personalized Medicine Biomarkers Market Insights

The U.K. is expected to reach a 19% share of the European market in 2026, following massive national genomic sequencing database updates. Public health initiatives utilize these large-scale population data arrays to discover novel predictive factors for complex cardiovascular and metabolic conditions. This rich data environment facilitates immediate assay validation partnerships with private biotechnology enterprises.

Asia Pacific Personalized Medicine Biomarkers Market Trends

Asia Pacific is forecast to be the fastest-growing market for personalized medicine biomarkers, stimulated by rapid healthcare infrastructure build-outs and expanding middle-class access to advanced clinical testing options. Regional regulatory bodies are updating approval pathways to fast-track precision therapeutics and matching companion tools.

China Personalized Medicine Biomarkers Market Insights

China is projected to secure a 31% share of the regional revenue in 2026 as domestic firms aggressively scale up local manufacturing of sequencing reagents. Strategic public-private partnerships focus on developing affordable multiplex cancer screening kits tailored to local demographic profiles. This domestic supply expansion drives down testing costs, allowing widespread institutional integration.

Japan Personalized Medicine Biomarkers Market Insights

Japan is expected to account for a 26% share of the Asia Pacific revenue in 2026 due to a rapidly aging demographic profile demanding cost-efficient chronic disease management models. Regulatory agencies are accelerating the co-approval of novel targeted immunotherapies and corresponding molecular diagnostic assays. This policy environment ensures immediate clinical uptake across major university hospital networks.

Competitive Landscape

The global personalized medicine biomarkers market is moderately fragmented, with a small number of large multinational diagnostics and life sciences companies commanding significant revenue concentration alongside a substantial cohort of specialized mid-tier and emerging players. Leading incumbents, including Roche Diagnostics, Thermo Fisher Scientific, Illumina, QIAGEN, and Abbott Laboratories, derive competitive advantage from integrated assay-to-instrument ecosystems, regulatory track records, and global commercial distribution networks.

Competitive differentiation is shifting from single-analyte assay performance toward comprehensive multi-omic platform capability, data analytics integration, and regulatory approval portfolio breadth. Strategic acquisitions of bioinformatics and artificial intelligence firms by large diagnostics players are reshaping the competitive boundary between instrument manufacturers and software-defined diagnostics companies, elevating barriers to meaningful competitive entry.

Key Industry Developments:

- In May 2026, Leica Biosystems expanded its collaboration to advance precision medicine through AI-powered diagnostics and biomarker-driven pathology solutions in oncology.

Companies Covered in Personalized Medicine Biomarkers Market

- Roche Diagnostics

- Thermo Fisher Scientific

- Illumina, Inc.

- QIAGEN N.V.

- Abbott Laboratories

- Siemens Healthineers

- bioMérieux SA

- Myriad Genetics

- Foundation Medicine

- Guardant Health

- Exact Sciences

- Becton, Dickinson

- Agilent Technologies

- Bio-Techne Corporation

- Sysmex Corporation

Frequently Asked Questions

The global personalized medicine biomarkers market is projected to reach US$30.9 billion in 2026.

The personalized medicine biomarkers market is driven by increasing adoption of precision oncology, expansion of genomic sequencing technologies, and rising demand for targeted and patient-specific therapeutic decision-making across chronic and complex diseases.

The personalized medicine biomarkers market is poised to witness a CAGR of 15.8% from 2026 to 2033.

Key market opportunities include expansion of liquid biopsy applications, integration of artificial intelligence in biomarker discovery, and growing adoption of multi-omics platforms for early disease detection and personalized therapy selection.

Some of the key market players include Roche Diagnostics, Thermo Fisher Scientific, Illumina, QIAGEN, and Abbott Laboratories.