- Baby Care & Accessories

- Baby Personal Care Market

Baby Personal Care Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Baby Personal Care Market By Product Type (Skin Care, Hair Care, Toiletries), Nature (Organic/Natural, Synthetic), Age Group (0 to 6 Months, 6 to 12 Months, 12 to 24 Months, 25 Months and Above), by Distribution Channel, and Regional Analysis for 2025 - 2032

Baby Personal Care Market Size and Trends

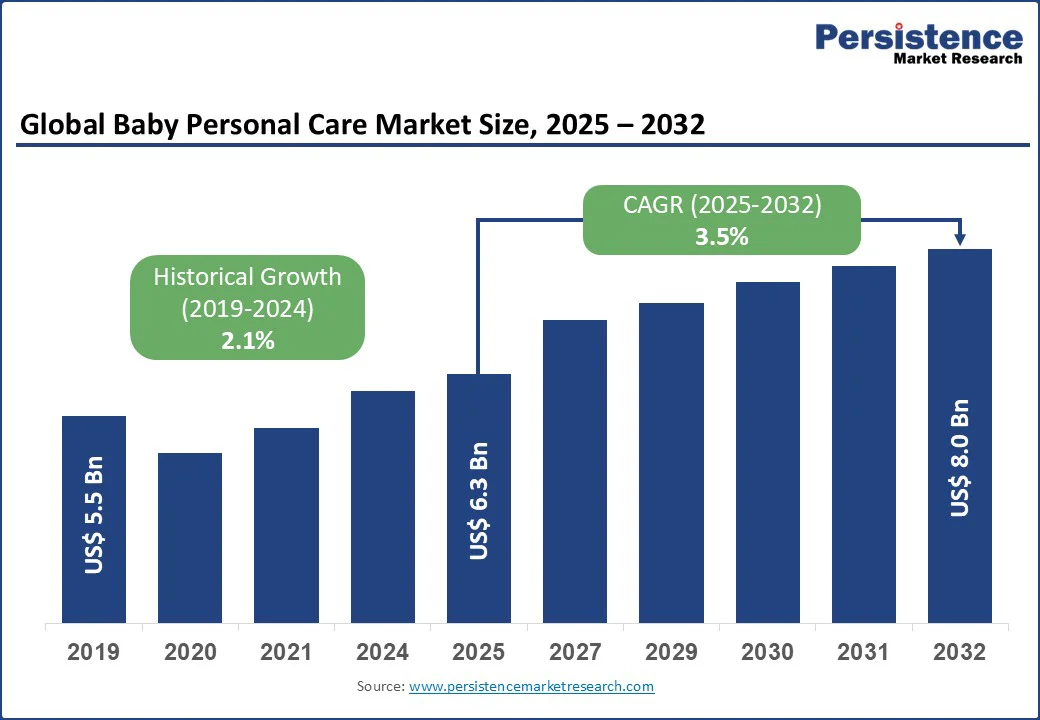

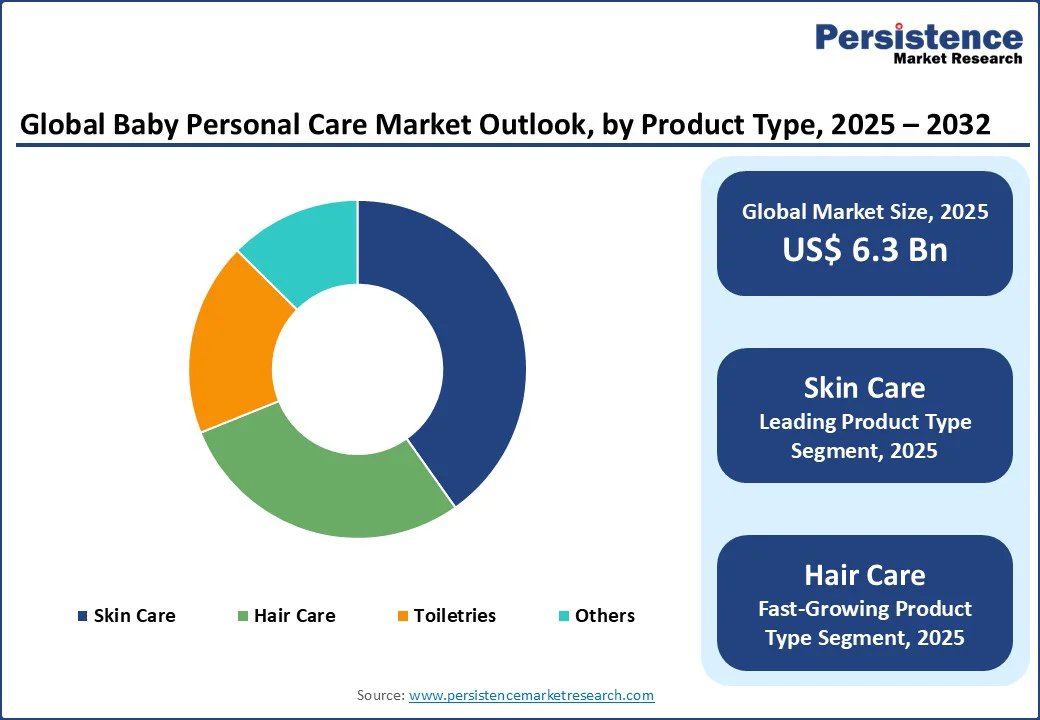

The baby personal care market size is likely to be valued at US$ 6.3 Bn in 2025 and is estimated to reach US$ 8.0 Bn in 2032, growing at a CAGR of 3.5% during the forecast period 2025 - 2032, majorly driven by rising parental awareness, demand for organic formulations, and the proliferation of digital retail channels.

Key Industry Highlights:

- Marketing Campaign: Sebamed launched a new campaign for Baby Sebamed, its specialized baby care line. Created by Leo India, the campaign highlights a baby’s journey from inside the womb to their very first breath in the outside world.

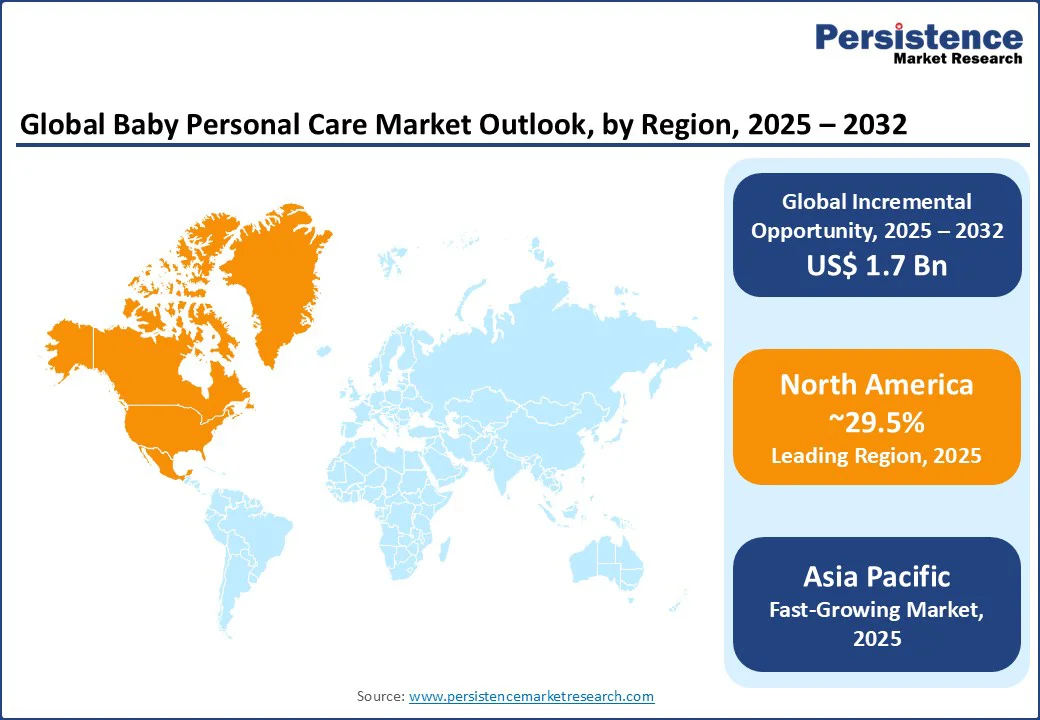

- Leading Region: North America with about 29.5% share in 2025, as regulatory standards encourage trust in product quality and safety.

- Fastest-growing Region: Asia Pacific, due to rising birth rates and expanding middle-class population in countries such as India and China.

- Leading Product Type: Skin care holds nearly 40.2% share in 2025, because infant skin sensitivity creates a rising demand for protective and moisturizing products.

- Dominant Nature: Organic, approximately 57.4% of the baby personal care market share in 2025, owing to surging parental concerns about chemical exposure.

- Key Distribution Channel: Hypermarkets/supermarkets recorded about 30.9% share in 2025, spurred by wide product assortments that enable parents to compare brands easily in one place.

| Key Insights | Details |

|---|---|

| Baby Personal Care Market Size (2025E) | US$ 6.3 Bn |

| Market Value Forecast (2032F) | US$ 8.0 Bn |

| Projected Growth (CAGR 2025 to 2032) | 3.5% |

| Historical Market Growth (CAGR 2019 to 2024) | 2.1% |

Market Factors - Growth, Barriers, Opportunity Analysis

Rising Parental Awareness and Health Concerns

With over 75% of global parents prioritizing natural and chemical-free baby products, the segment benefits from rising concern regarding allergies, eczema, and sensitive skin in infants. Increasing preference for products certified 'hypoallergenic' or 'dermatologist-tested' stimulates demand, notably in mature markets such as North America and Europe.

Parents actively shun parabens and synthetic fragrances, prompting leading businesses to reformulate and innovate for safety and effectiveness.

The steady expansion of the global middle-class population in emerging markets is directly boosting demand for premium baby care products. Parents are increasingly willing to allocate high budgets toward infant-specific toiletries, skincare, and hair care solutions, perceiving them as essential to child wellbeing.

According to the World Bank, the global middle class is projected to represent more than 50% of the population by 2030. This shift is predicted to drastically influence consumer expenditure on childcare essentials.

Shift toward Organic and Sustainable Products

The share of organic/natural products is expected to dominate in 2025, registering the fastest segmental growth rate. With environmental consciousness rising, sustainable packaging solutions and plant-based ingredients propel product launches and portfolio revamps.

Notably, premium pricing structures leverage parents’ readiness to invest in product safety, pushing brands such as Mustela, Honest Co., and Johnson & Johnson to introduce new organic sub-lines priced 20 to 30% above basics.

This momentum is further reinforced by regulatory encouragement and third-party certifications that validate product authenticity. Labels such as USDA Organic, COSMOS, and ECOCERT have become powerful decision-making factors for parents, who often rely on certifications to distinguish genuine organic products from greenwashed alternatives.

Digital Retail Expansion and E-commerce Penetration

The proliferation of e-commerce channels has materially broadened market access, with 65% of buyers in key economies shopping online. Subscription models and influencer-led marketing on Amazon, Shopee, and Tmall bring recurring revenues and fuel consumer loyalty. Digital retail formats enable customized product recommendations utilizing AI and advanced analytics for hyper-personalized solutions, supporting market expansion.

The ongoing digital transformation is complemented by improved mobile penetration and the rising use of social media platforms. These act as both marketing and sales channels for baby care brands. Parents now rely on online reviews, video tutorials, and parenting communities to evaluate products before purchase, giving brands an opportunity to build credibility and engagement digitally.

Restraint- High Regulatory and Compliance Costs

Stringent safety regulations placed on ingredient transparency, claims substantiation, and mandatory product testing lead to increased compliance costs. Firms are required to substantiate claims such as organic or hypoallergenic, specifically in response to incidents, including Johnson & Johnson’s talc powder litigation, which increase both operating costs and reputational risk for manufacturers.

Competitive Saturation and Price Pressure

The market’s fragmented landscape, with multiple brands delivering similar product lines, poses barriers to differentiation. Price competition, especially in emerging markets, leads to the standardization of product lines and restricted innovation investments, making brand loyalty difficult to sustain.

Opportunities

Technological Developments in Product and Packaging

Breakthroughs such as microbiome-friendly and biotechnology-driven products, DNA and skin-type-based customization, and sustainable, refillable packaging provide actionable avenues for new entrants and established players alike. Integration of IoT for monitoring, AI-powered skin analysis apps, and smart packaging solutions deliver convenience and improved efficacy in baby care routines.

Rising Demand for Subscription-based and Direct-to-consumer Models

The market for baby personal care products is witnessing a surge in subscription services for essentials such as diapers and wipes, catering to recurring consumer demands. These formats lead to increased lifetime customer value, predictable revenue streams, and greater opportunities for personalization and upselling.

Emerging Markets and Middle-class Expansion

Asia Pacific, mainly China and India, presents high growth, propelled by surging birth rates and rising disposable income. These markets are forecasted to achieve CAGRs of 6.7% and 7.1% respectively between 2025 and 2032, contributing substantially to incremental revenue. Local packaging trends and affordable plant-based products enable brands to penetrate new consumer bases.

Category-wise Analysis

Product Type Insights

Skin care products will likely account for around 40.2% of the global market share in 2025, owing to rising awareness of infant skin concerns such as dryness, rashes, and eczema as well as the preference for gentle creams, lotions, and oils. The segment’s growth correlates strongly with scientific recommendations for dermatologically-approved and mild formulations targeting infants aged 0 to 6 and 6 to 12 months.

Haircare and toiletries, though trailing skin care, are projected to outpace other segments due to developments in hypoallergenic and plant-based ingredients, targeting conditions such as cradle cap and scalp sensitivities. Parents’ increasing focus on comprehensive hygiene and dedicated product ranges for each life stage propel growth rates in these categories.

Nature Insights

Organic segment dominance at around 57.4% of share in 2025 is propelled by rising consumer demand for chemical-free and plant-based formulations. Brands are proactively reformulating legacy products, switching to sustainable packaging, and engaging with eco-conscious parents through influencer endorsements and certifications.

While synthetic products appeal in price-sensitive markets, the increasing preference for natural replacements remains evident. Yet, affordable synthetic product lines continue to support adoption in developing regions where price remains a primary purchase driver.

Distribution Channel Insights

Hypermarkets and supermarkets constitute nearly 30.9% of the global market share in 2025, providing convenience, product variety, and competitive pricing. Brick-and-mortar locations still dominate in countries such as Japan and South Korea, where in-person testing is valued.

E-commerce channels show the fastest expansion, capturing over 65% of online sales in China, the U.S., and Southeast Asia. Specialty stores yield higher margins through customized services and dedicated product education, further utilizing influencer engagement.

Regional Insights

North America Baby Personal Care Market Trends

North America leads with a significant market share of approximately 29.5% in 2025. This is due to high per-capita spending, novel regulatory oversight, and superior digital infrastructure. The U.S. will likely command a 5.6% CAGR through 2032, with parents highly valuing dermatologist approvals and subscription-based purchases via mass merchants and online platforms.

Regulatory frameworks such as the Food and Drug Administration (FDA) oversight, coupled with innovations, including AI-based apps and sustainable products, set standards for product safety and efficacy. Investments are increasingly directed toward biotechnology, green formulations, and consumer education programs to uphold competitiveness.

Asia Pacific Baby Personal Care Market Trends

Asia Pacific emerges as the fastest-growing region, spurred by demographic expansion, urbanization, and digital retail penetration. China and India display the most prominent growth, while Japan and ASEAN economies bolster development through manufacturing efficiency and local ingredient integration.

Asia Pacific is characterized by increasing disposable income, regulatory support for child health, and the ascendancy of local brands embracing price sensitivity and cultural preferences. Investments target new production facilities, local distribution networks, and AI-backed retail analytics.

Europe Baby Personal Care Market Trends

Europe follows with strong performance in Germany, the U.K., and France, reflected a positive CAGR in the forecast period. Key growth drivers include the prioritization of eco-friendly packaging, regulatory harmonization under EU guidelines, and a strong innovation ecosystem propelling product developments in vegan, cruelty-free, and specialty skincare segments.

Competitive intensity is surged by both multinational and local brands, utilizing ethical sourcing and recyclable packaging. Key regulations such as the ban on specified chemicals boost industry-wide reformulations, augmenting trust and market integrity.

Competitive Landscape

The baby personal care market is moderately concentrated, with Johnson & Johnson, Procter & Gamble, Unilever, Kimberly-Clark, and Beiersdorf collectively holding over 50 to 60% market share, complemented by various regional and niche brands. Despite their dominance, frequent innovation and merger and acquisition activity sustain a dynamic landscape, supporting both consolidation and the rise of specialty players.

Business Strategies

Dominant strategic elements include AI-powered customization, cost leadership, and market expansion via digital and specialty retail channels. Key differentiators rest on exclusive ingredient sourcing, product safety certifications, and direct-to-consumer engagement. Subscription and bundled-portfolio business models support sustained recurring revenues and customer loyalty.

Key Industry Developments

- In September 2025, Coterie launched a new baby skincare line to meet the rising demand for products that are safe, effective, and gentle enough for even the most sensitive or eczema-prone skin. The new products are free from petrolatum, fragrance, and other common irritants.

- In September 2025, CuteStory, a new-age baby care brand built on the values of safety, sustainability, and emotional warmth, announced its official launch. It provides dermatologically tested, paraben-free, sulfate-free, pH-balanced, and non-irritant formulations.

Companies Covered in Baby Personal Care Market

- Johnson & Johnson

- Procter & Gamble

- Unilever

- Kimberly-Clark Corporation

- Beiersdorf AG (NIVEA Baby)

- Burt's Bees

- Marks & Spencer

- Sebamed

- Himalaya Drug Company

- Pigeon

- Danone S.A.

- Farlin Infant Products Corp.

- Asda Group

- Mead Johnson Nutrition

- Bonpoint

- Oral B Laboratories

- Galderma

- Others

Frequently Asked Questions

The baby personal care market is projected to reach US$ 6.3 Bn in 2025.

Growing awareness of infant hygiene and high demand for natural formulations are the key market drivers.

The baby personal care market is poised to witness a CAGR of 3.5% from 2025 to 2032.

Innovation in dermatologically tested products and collaborations with pediatricians are the key market opportunities.

Johnson & Johnson, Procter & Gamble, and Unilever are a few key market players.