- Hardware & Software IT Services

- Virtual Networking Market

Virtual Networking Market Size, Share, and Growth Forecast, 2026 - 2033

Virtual Networking Market by Component Type (Software, Services, Hardware ), Deployment Mode (On-Premise, Cloud-Based, Hybrid ), Application (Data Center Virtualization, Enterprise Networking, Cloud Service Provider Networks, Telecom & Service Provider Networks, Security & Network Segmentation, Misc. , End Use Industry (IT & Telecom, BFSI (Banking, Financial Services & Insurance), Healthcare & Life Sciences, Government & Public Sector, Retail & eCommerce, Manufacturing, Misc.) and Regional Analysis for 2026 - 2033

Virtual Networking Market Size and Trends Analysis

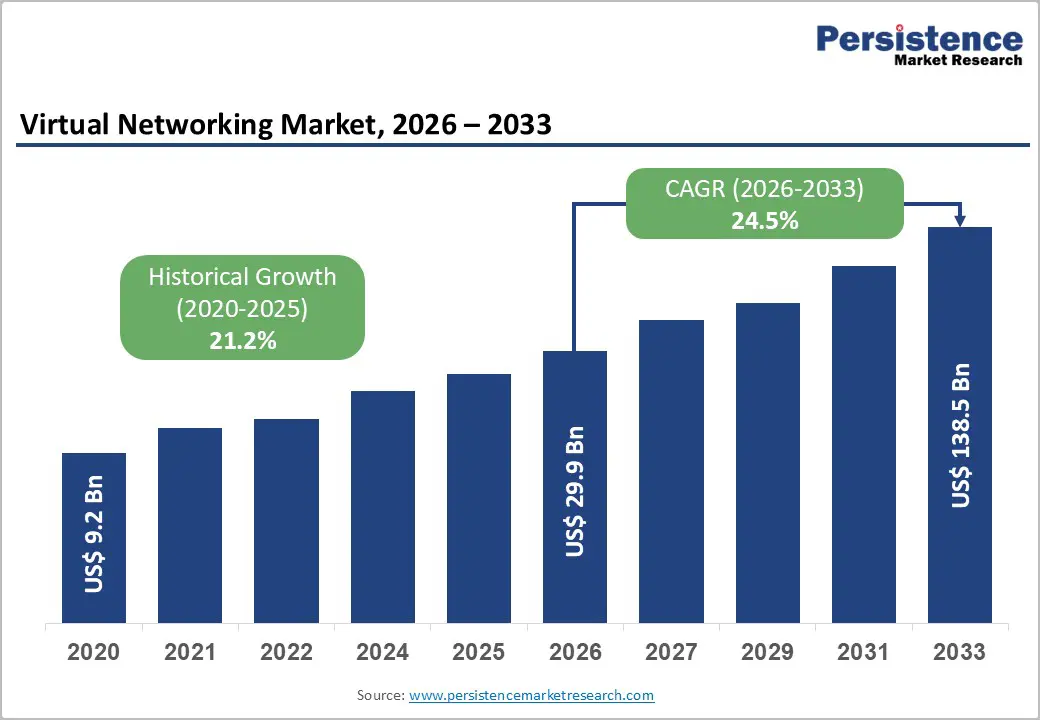

The global virtual networking market size was valued at US$ 29.9 billion in 2026 and is projected to reach US$ 138.5 billion by 2033, growing at a CAGR of 24.5% between 2026 and 2033. This exceptional expansion is driven by accelerated cloud migration initiatives that require software-defined network infrastructure, the widespread adoption of 5G networks that necessitate virtualized core functions, and enterprises' transition from hardware-dependent architectures to programmable, scalable virtual networking solutions.

The market's momentum reflects the fundamental shift from physical network appliances to software-based networking, enabling centralized management, automated provisioning, and cost-optimized infrastructure operations. With telecommunications operators virtualizing network functions, financial institutions migrating to hybrid cloud environments, and healthcare organizations implementing telemedicine platforms, virtual networking technologies have become essential for supporting distributed workforces, multi-cloud strategies, and digital transformation initiatives across global enterprises.

Key Industry Highlights:

- Regional Leadership: East Asia leads the global virtual networking market with 28% share, driven by rapid 5G deployment, telecom infrastructure virtualization, industrial digitalization, and government-supported software-defined networking initiatives.

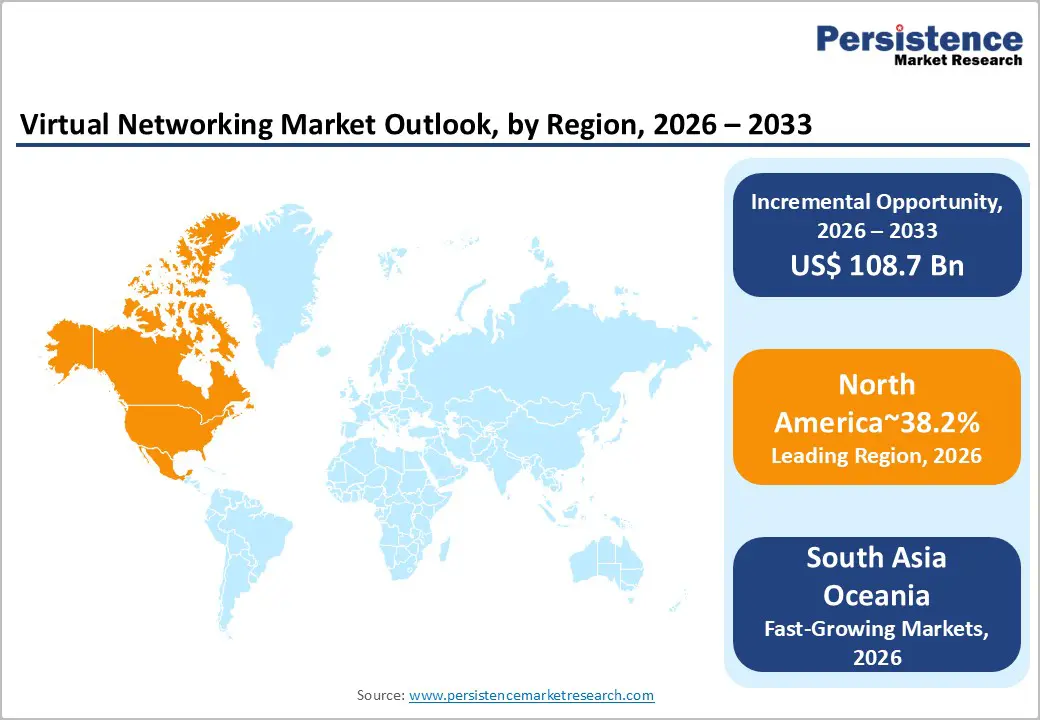

- Strong North American Presence: North America accounts for 38.2% of the market, driven by advanced cloud adoption, mature SD-WAN deployments, enterprise digital-transformation investments, and early adoption of AI-powered network management platforms.

- High-Growth European Market: Europe accounts for a 17% share, driven by GDPR-driven secure network segmentation, hybrid cloud adoption, and digital transformation initiatives across the finance and telecommunications sectors.

- Leading Component Segment: The Software segment dominates with 50.4% share, supported by the shift from hardware-based networking to programmable, centralized, and automated virtual network platforms.

- Fastest-Growing Component Segment: The Services segment is the fastest-growing, driven by consulting, implementation, network design, and managed virtual networking services supporting NFV/SDN integration and hybrid cloud environments.

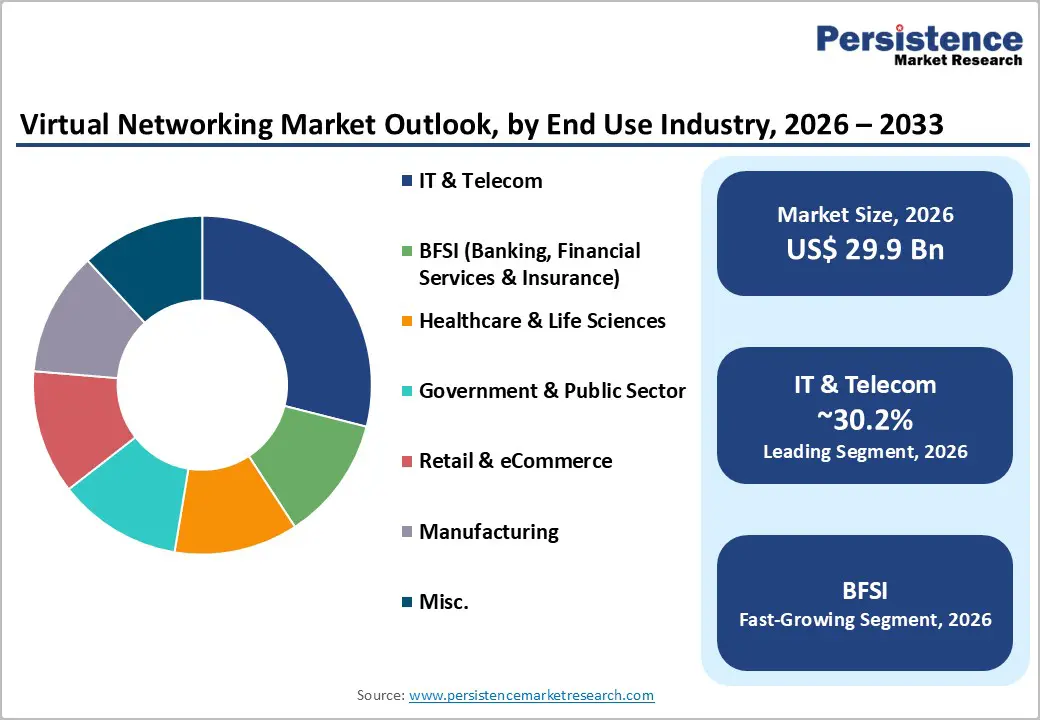

- Leading End-Use Segment: IT & Telecommunications commands the largest end-user share at 30.2%, reflecting the sector’s early adoption of NFV, SD-WAN, and virtualized core network functions for 5G infrastructure.

| Key Insights | Details |

|---|---|

| Virtual Networking Market Size (2026E) | US$ 29.9 Bn |

| Market Value Forecast (2033F) | US$ 138.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 24.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 21.2% |

Market Dynamics

Growth Drivers

Telecommunications Infrastructure Virtualization and 5G Network Function Deployment

The comprehensive virtualization of telecommunications infrastructure and the deployment of 5G network functions are fundamentally driving the global virtual networking market as operators transition from proprietary hardware to software-based, virtualized network architectures, enabling dynamic service provisioning and operational cost optimization. India's telecom sector demonstrates this transformation, with a subscriber base of 1.21 billion and a tele-density of 86.09 percent as of June 2025, while internet subscribers reached 979 million.

Broadband adoption accelerated from 149.75 million connections in 2016 to 979 million in 2025, driven by 4G and rapidly expanding 5G networks, with 5G accounting for nearly a quarter of total wireless data usage in FY25. Gross telecom revenue rose from US$ 39.22 billion in FY24 to US$ 43.42 billion in FY25, with cumulative FDI inflows reaching US$ 40.07 billion between April 2000 and March 2025.

According to ITU estimates, global internet usage expanded to around 6 billion users in 2025, up from 60 percent in 2020, with nearly 1.3 billion people coming online between 2020 and 2025. On April 3, 2025, 6WIND partnered with Dense Air to supply virtualized security gateway (vSecGW) and virtual cell site router (vCSR) solutions, enhancing secure routing and connectivity for Dense Air's Neutral Host infrastructure supporting scalable virtual networking for multi-operator 5G deployments. This massive telecommunications modernization requires virtual networking solutions that enable network function virtualization (NFV), software-defined networking (SDN), and cloud-native network operations, substantially benefiting the global virtual networking market.

Digital Transformation and Cloud Computing Infrastructure Adoption

The acceleration of digital transformation initiatives and migration to cloud computing infrastructures across enterprises globally creates substantial demand for virtual networking technologies, enabling secure, scalable connectivity across hybrid and multi-cloud environments within the global virtual networking market. The EU information and communication services sector encompassed around 1.4 million enterprises and employed nearly 7.2 million people in 2022, generating €667 billion in value added and accounting for 6.6% of total EU business economy value added. Computer programming, consultancy, and related activities dominated the sector, contributing around 60 percent of total employment and, with apparent labour productivity reaching €92,800 per person employed.

Germany accounted for around 23 percent of EU sectoral value added and 22.5 percent of employment, followed by France, demonstrating concentration in major European markets. On April 8, 2025, Hewlett Packard Enterprise (HPE) expanded its HPE Aruba Networking Central platform with new virtual private cloud (VPC) and on-premises deployment options, enhancing virtual network management flexibility through AI-powered optimization, security, and observability features that address enterprise data sovereignty and regulatory requirements.

The global B2B eCommerce market demonstrated sustained growth with GMV climbing from $9,837 billion in 2017 to $36,163 billion by 2026, representing a CAGR of 14.5 percent, driven by the integration of advanced digital procurement solutions, cloud-based platforms enabling real-time collaboration, and data analytics throughout supply chains. This comprehensive expansion of digital infrastructure necessitates virtual networking solutions that provide automated provisioning, centralized policy management, and seamless connectivity across distributed cloud environments, driving sustained demand in the global virtual networking market.

Market Restraining Factors

Network Performance and Latency Concerns in Virtualized Environments

Organizations face legitimate concerns about network performance degradation, increased latency, and throughput limitations when transitioning from dedicated hardware appliances to virtualized networking infrastructure, particularly for latency-sensitive applications such as high-frequency trading, real-time communications, and industrial automation. Virtualized network functions introduce additional processing overhead through hypervisor layers, shared computing resources, and software-based packet processing, which can impact performance compared to purpose-built hardware.

Financial services institutions managing high-volume transaction processing, telecommunications operators handling real-time voice and video traffic, and healthcare providers delivering telemedicine services require guaranteed performance levels that may be challenging to achieve consistently in virtualized environments. These performance concerns constrain adoption, particularly for mission-critical applications, where network latency directly affects business outcomes and user experience.

Key Market Opportunities

Immersive Virtual Collaboration and Spatial Networking Technologies

The emergence of immersive virtual collaboration platforms and spatial networking technologies creates transformative opportunities for the global virtual networking market by enhancing business networking experiences, expanding virtual event capabilities, and enabling remote collaboration, thereby transcending traditional video conferencing limitations. On January 15, 2026, Elev8ors launched immersive tribe meeting rooms leveraging SpatialChat technology to enhance virtual networking through proximity-based audio and avatar interaction, enabling more realistic, relationship-driven business networking experiences for entrepreneurs and small business owners.

These spatial networking platforms use advanced virtual networking technologies to enable proximity-based audio rendering, avatar positioning, spatial audio processing, and real-time interaction that mimic physical networking environments. The technologies address limitations of traditional video conferencing platforms, which confine participants to static grid views, enabling more natural conversations, spontaneous interactions, and relationship-building comparable to in-person events.

Applications span virtual trade shows that enable exhibitor-attendee interactions, remote team collaboration spaces that facilitate informal conversations, educational environments that support student engagement, and professional networking events that connect geographically dispersed participants. The substantial enterprise investments in remote work infrastructure, combined with persistent demand for authentic human connections in digital environments, position immersive spatial networking as a significant growth opportunity that requires advanced virtual networking infrastructure to support low-latency audio processing, scalable participant management, and seamless cross-platform connectivity within the global virtual networking market.

Financial Inclusion and Digital Banking Infrastructure in Emerging Markets

The substantial financial inclusion initiatives and digital banking infrastructure deployment across emerging markets presents significant opportunities for the global virtual networking market through secure, scalable connectivity supporting mobile banking, digital payment systems, and fintech platform operations. Latin America's banking sector demonstrates this opportunity, with over 50 percent of adults unbanked and banks facing urgent pressure to modernize legacy systems that cannot support real-time payments such as Brazil's PIX. This requires core modernization through incremental, API-first approaches that enable faster time-to-market, improved customer personalization, and cost reduction.

India's BFSI sector's transformation from US$ 20.28 billion in 2005 to Rs. US$1 trillion in 2025 underscores the scale of financial services digitalization, with NBFCs emerging as significant credit engines, posting a 15 percent CAGR in net worth and a 31.7 percent CAGR in PAT. Mobile banking proliferation, digital wallet adoption, and fintech platform expansion require virtual networking solutions enabling secure API connectivity, encrypted transaction processing, multi-factor authentication integration, and regulatory compliance across distributed financial ecosystems.

Emerging markets' unique challenges include limited physical banking infrastructure, high mobile penetration, regulatory requirements for local data residency, and cost-sensitive market dynamics, which create demand for cost-optimized virtual networking solutions supporting financial inclusion initiatives while maintaining security and compliance standards, positioning emerging market digital banking infrastructure as a critical growth opportunity within the global virtual networking market.

Category-wise Analysis

Component Type Insights

Software dominates the Global Virtual Networking Market with 50.4% market share in 2026, reflecting the fundamental architecture shift from hardware-based networking to programmable, software-defined networking platforms enabling centralized management, automated provisioning, and dynamic network configuration. This segment encompasses virtual switching software, software-defined WAN (SD-WAN) controllers, network virtualization platforms, virtual routing software, and orchestration systems enabling policy-based network management across distributed infrastructure.

On April 8, 2025, Hewlett Packard Enterprise (HPE) expanded its HPE Aruba Networking Central platform with new virtual private cloud (VPC) and on-premises deployment options, enhancing virtual network management flexibility with AI-powered optimization, security, and observability features addressing enterprise data sovereignty and regulatory requirements.

Software components enable organizations to reduce capital expenditures on proprietary hardware, implement network changes through policy updates rather than physical reconfigurations, and scale networking capacity dynamically respond to workload demands, establishing software as the dominant component driving market value creation and competitive differentiation.

Services represent the fastest-growing component within the Global Virtual Networking Market, encompassing professional consulting, implementation support, network design services, managed virtual networking operations, and continuous optimization services addressing the complexity of transitioning from traditional to virtual networking architectures. The services segment's rapid expansion reflects the specialized expertise required to design software-defined networking frameworks, integrate virtual networking platforms with existing infrastructure, and optimize network performance across hybrid environments.

End Use Industry Insights

IT & Telecommunications commands the largest end-user share of the Global Virtual Networking Market at 30.2% in 2026, reflecting the sector's pioneering role in virtual networking adoption, extensive infrastructure virtualization initiatives, and fundamental dependence on software-defined networking for service delivery and operational efficiency. Telecommunications operators lead virtual networking implementation through network function virtualization (NFV), enabling dynamic service provisioning, software-defined WAN deployment, optimizing bandwidth utilization, and virtualized core network functions supporting 5G infrastructure.

Banking, Financial Services, and Insurance (BFSI) is the fastest-growing end-user segment in the global virtual networking market, driven by accelerated digital transformation, regulatory compliance requirements necessitating secure network segmentation, hybrid cloud migration initiatives, and the proliferation of digital banking platforms that require scalable, resilient connectivity infrastructure. The sector's rapid adoption reflects critical needs for secure multi-site connectivity, disaster recovery capabilities, and low-latency networking supporting real-time transaction processing.

Regional Insights and Trends

North America Market Trend

North America represents 38.2% of the Global Virtual Networking Market, characterized by advanced cloud computing adoption, mature software-defined networking deployments, substantial enterprise digital transformation investments, and concentrated presence of leading virtual networking vendors and sophisticated early-adopter customers. The region benefits from established hybrid cloud architectures, widespread SD-WAN implementation, and proactive investment in network automation and artificial intelligence-powered network management platforms.

The region's competitive landscape features established virtual networking platforms, robust venture capital supporting network automation, collaborative partnerships between cloud providers and networking vendors, and sophisticated enterprise customers driving demand for AI-powered network optimization, security automation, and intent-based networking capabilities. North America's advantages include strong enterprise IT spending, high cloud adoption rates, advanced telecommunications infrastructure supporting 5G enterprise services, and regulatory environments supporting digital innovation, positioning the region for continued leadership in virtual networking technology development, enterprise adoption, and emerging use cases including edge computing, IoT connectivity, and immersive collaboration platforms through 2033.

East Asia Market Trend

East Asia dominates the Global Virtual Networking Market with 28.0% share, driven by massive telecommunications infrastructure investments, rapid 5G deployment, substantial manufacturing digitalization, and government-led initiatives promoting software-defined networking across industrial and enterprise sectors. The region's market leadership reflects a strategic emphasis on technology sovereignty, domestic platform development, and the adoption of comprehensive virtual networking, which support the transformation of the digital economy.

China's banking and insurance sectors demonstrated robust growth and stability as of Q2 2025, with total banking assets reaching RMB 467.3 trillion, up 7.9 percent year-on-year, and insurance assets growing 9.2 percent to RMB 39.2 trillion. Large commercial banks accounted for 43.7 percent of total banking assets, while inclusive loans to micro and small enterprises rose 12.3 percent to RMB 36 trillion. Commercial banks maintained strong asset quality with an NPL ratio of 1.49 percent, a capital adequacy ratio of 15.58 percent, and net profits of RMB 1.2 trillion, requiring sophisticated virtual networking frameworks protecting customer data, transaction systems, and regulatory compliance across increasingly virtualized banking infrastructure.

East Asia's competitive advantages include government support for software-defined networking platforms, substantial telecommunications infrastructure modernization with large-scale 5G rollouts, manufacturing sector digitalization requiring industrial IoT connectivity, and strategic initiatives promoting virtual networking across smart city projects and enterprise cloud adoption, positioning the region for sustained market leadership through comprehensive digital infrastructure development and technology localization strategies through 2033.

Europe Market Trend

Europe accounts for 17% of the Global Virtual Networking Market, supported by stringent data protection regulations that require virtual network segmentation, comprehensive digital transformation initiatives across the financial services and telecommunications sectors, and mature enterprise cloud adoption that necessitates advanced virtual networking capabilities. The region's market characteristics reflect strong regulatory enforcement, technology sovereignty priorities, and established partnerships between telecommunications operators, financial institutions, and virtual networking solution providers.

The EU information and communication services sector comprised around 1.4 million enterprises, employed nearly 7.2 million people, and generated approximately €667 billion in value added in 2022, accounting for 6.6 percent of total EU business economy value added. Computer programming, consultancy, and related activities accounted for 59.8 percent of total employment and 51.1 % of value added, with apparent labour productivity reaching €92,800 per person. Germany accounted for 22.8 percent of EU sectoral value added and 22.6 percent of employment, followed by France, demonstrating concentration in major European markets.

Europe's competitive advantages include harmonized cybersecurity frameworks facilitating cross-border virtual networking deployments, GDPR compliance driving secure network segmentation, substantial investments in 5G infrastructure, and collaborative public-private partnerships advancing software-defined networking adoption, positioning the region for sustained growth aligned with digital sovereignty objectives and enterprise cloud modernization imperatives through 2033.

Competitive Landscape

The global virtual networking market is moderately consolidated, with a mix of established networking vendors and cloud-native platform providers collectively shaping the ecosystem. Major players such as Cisco Systems, VMware (Broadcom), HPE Aruba, Huawei, Juniper Networks, and Microsoft Azure maintain strong competitive positions through extensive product portfolios spanning SD-WAN, SASE, NFV, virtual routers, and cloud networking services. These vendors leverage global enterprise relationships, telecom partnerships, and cloud integration capabilities to reinforce their market presence.

While dominant incumbents lead in scale and deployment breadth, the market also includes innovative challengers specializing in virtualized network functions, automation, and cloud orchestration, contributing to a competitive yet innovation-driven environment. As digital transformation accelerates, competition increasingly centers on AI-enabled network management, multi-cloud connectivity, and secure edge networking.

Key Industry Developments

- April 3, 2025 – 6WIND partnered with Dense Air to supply virtualized security gateway (vSecGW) and virtual cell site router (vCSR) solutions, enhancing secure routing and connectivity for Dense Air’s Neutral Host infrastructure and supporting scalable virtual networking for multi-operator 5G deployments.

- April 8, 2025 – Hewlett Packard Enterprise (HPE) expanded its HPE Aruba Networking Central platform with new virtual private cloud (VPC) and on-premises deployment options, enhancing virtual network management flexibility with AI-powered optimization, security, and observability features to address enterprise data sovereignty and regulatory requirements.

Companies Covered in Virtual Networking Market

- Huawei Technologies Co., Ltd.

- Hewlett Packard Enterprise Development LP

- VMware, Inc.

- Cisco Systems, Inc.

- Microsoft Corporation

- IBM Corporation

- Citrix Systems, Inc.

- Juniper Networks, Inc.

- Oracle

- Verizon Communications Inc.

Frequently Asked Questions

The global Virtual Networking Market is projected to be valued at US$ 29.9 Bn in 2026.

The IT & Telecom segment is expected to account for approximately 30.2% of the Global Virtual Networking Market by End Use Industry in 2026.

The market is expected to witness a CAGR of 24.5% from 2026 to 2033.

The Global Virtual Networking Market is driven by telecommunications infrastructure virtualization and 5G deployment, digital transformation and cloud adoption, expanding internet and broadband usage, enterprise demand for secure multi-cloud connectivity, and strategic partnerships enabling NFV, SDN, and cloud-native network operations.

Key opportunities in the Global Virtual Networking Market lie in immersive virtual collaboration and spatial networking technologies for realistic remote interactions, and in supporting digital banking and financial inclusion infrastructure in emerging markets through secure, scalable, and compliant virtual connectivity.

Key players in the Software-Defined Security Market include Cisco Systems, VMware (Broadcom), HPE Aruba, Huawei, Juniper Networks, and Microsoft Azure.