- Communication Infrastructure & Services

- Network Traffic Analyser Market

Network Traffic Analyser Market Size, Share, and Growth Forecast, 2026 - 2033

Network Traffic Analyzer market by Component (Solutions, Services), Organisation Size (Small & Medium Enterprises (SMEs), Large Enterprises), Deployment Mode (Cloud/SaaS, On-Premise, Hybrid), Industry (Telecommunications & Service Providers, IT & Cloud Providers/Data Centers, BFSI (Banking, Financial Services & Insurance), Government & Public Sector, Healthcare, Manufacturing/Industrial (including IIoT), Others), and Regional Analysis for 2026 - 2033

Network Traffic Analyzer Market Size and Trends Analysis

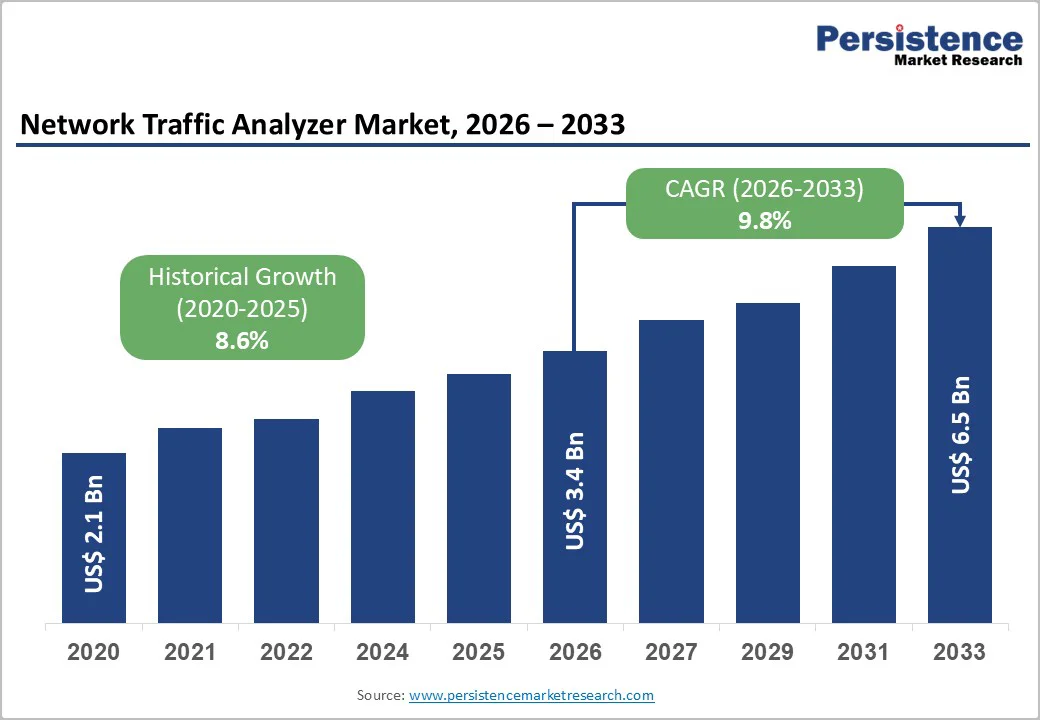

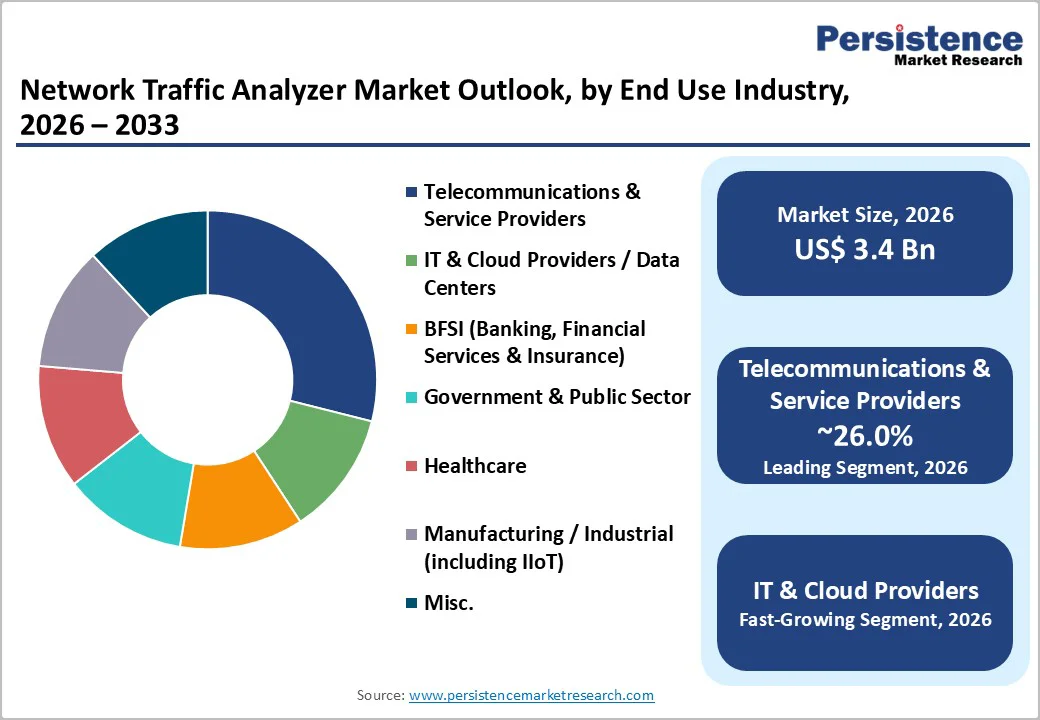

The global network traffic analyzer market size is likely to be valued at US$ 3.4 billion in 2026 and is projected to reach US$6.5 billion by 2033, growing at a CAGR of 9.8% between 2026 and 2033.

The market expansion is driven by three primary factors: escalating cyber threats necessitating real-time threat detection and anomaly identification, regulatory mandates requiring network security compliance and traffic monitoring documentation, and the widespread adoption of cloud infrastructure, generating complex hybrid environments that require comprehensive network visibility.

Key Industry Highlights:

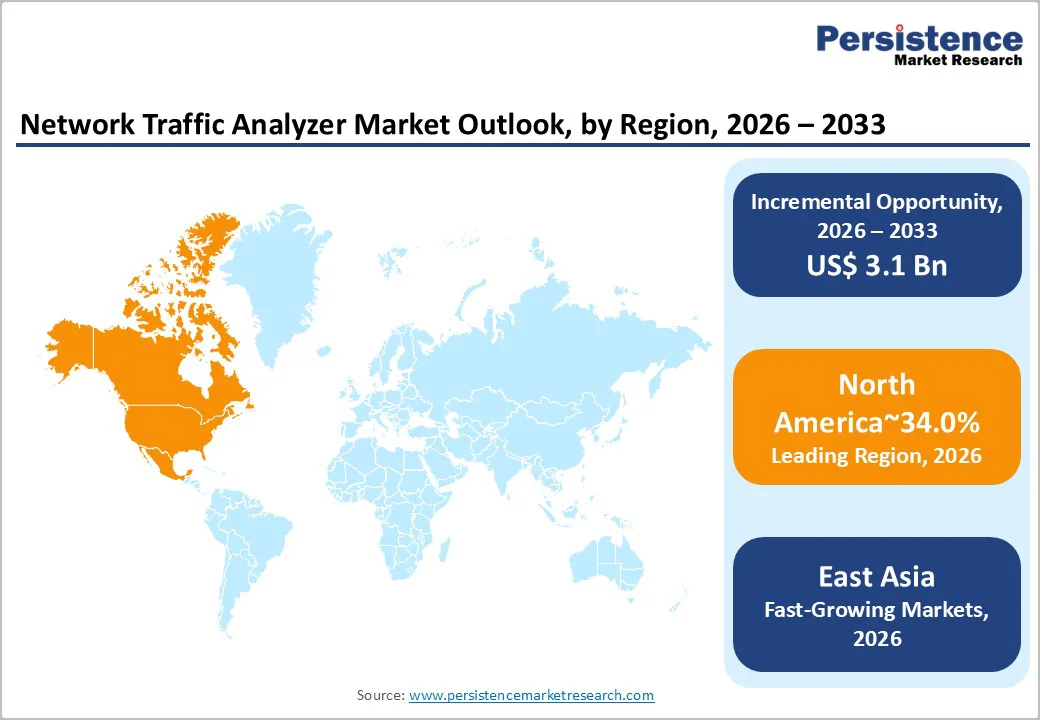

- Regional Leadership: North America commands 34% share of the global Network Traffic Analyzer Market, supported by strict regulatory mandates, advanced security frameworks, and strong enterprise adoption of unified network observability platforms.

- Component Dominance: The solutions segment leads with a 72% share in 2026, driven by enterprise demand for integrated packet capture, flow analytics, deep traffic inspection, and ML-powered monitoring architectures.

- Largest End-user Category: Telecommunications and service providers hold 26% market share, propelled by compliance obligations, large-scale traffic volumes, and rapid 5G network modernisation initiatives.

- Growth Indicator: Rising cyber threats, intensifying regulatory enforcement, and expanding hybrid cloud deployments fuel global demand for unified traffic visibility and real-time network intelligence.

- Emerging Opportunity: AI-driven predictive observability and autonomous anomaly detection present a significant growth opportunity as enterprises transition from reactive monitoring to proactive performance assurance.

- 5G & Edge Acceleration: 5G rollouts, network slicing adoption, and the expansion of edge computing infrastructure accelerate demand for advanced traffic analysis across telecom operators and hyperscalers.

- Technology: Recent advancements such as Cloudflare’s Radar intelligence upgrades and Arista’s AI job-centric observability capabilities strengthen industry movement toward granular, real-time, and contextual traffic insights.

| Key Insights | Details |

|---|---|

| Network Traffic Analyzer Market Size (2026E) | US$ 3.4 Bn |

| Market Value Forecast (2033F) | US$ 6.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.6% |

Market Dynamics

Drivers - Regulatory Compliance Mandates and Cybersecurity Risk Management Requirements

Government and regulatory bodies globally are establishing explicit requirements for telecommunications carriers and critical infrastructure operators to deploy network traffic analysis capabilities as fundamental security controls. The Federal Communications Commission (FCC) issued a Declaratory Ruling effective January 2025, clarifying that Section 105 of the Communications Assistance for Law Enforcement Act (CALEA) affirmatively requires telecommunications carriers to secure their networks from unauthorised access and communications interception, with enforcement authority to impose monetary penalties for non-compliance. This regulatory mandate directly compels telecom operators to implement network traffic analyzer solutions capable of detecting unauthorised access attempts, monitoring network anomalies, and maintaining comprehensive audit trails demonstrating security posture.

The accompanying Notice of Proposed Rulemaking establishes requirements for communications service providers to develop, implement, and annually certify cybersecurity and supply chain risk management plans, obligations that mandate network traffic analyzer deployment as documentary evidence of security control implementation. The European Union's NIS2 Directive, effective October 2024, extends similar network security monitoring obligations across telecommunications operators and critical infrastructure sectors, with penalties reaching €10 million or 2% of annual global turnover for non-compliance.

The market demand directly correlates with regulatory enforcement intensity: telecommunications providers across North America and Europe report that 71% of network security budget allocations address regulatory compliance requirements, with network traffic analyzers specified as mandatory controls. GDPR data breach notification requirements that include is72-hour reporting windows create operational demand for network traffic analyzers, enabling real-time threat detection and incident response documentation, supporting organisations' ability to comply with notification timelines and demonstrate "appropriate technical measures" under Article 32.

Digital Infrastructure Transformation and Cloud-Native Architectural Complexity

Organisations across all sectors are undertaking fundamental digital transformation initiatives involving cloud infrastructure adoption, distributed workload deployment, and hybrid IT architectures that generate unprecedented network complexity and data volumes requiring advanced traffic analysis capabilities.

International Data Corporation (IDC) forecasts that worldwide data creation will reach 175 zettabytes by 2025, a 61% increase from 2024, with the majority of new data generated at the edge through IoT sensors, autonomous systems, and distributed computing platforms. This exponential data growth translates directly into network traffic volumes exceeding traditional monitoring capabilities: telecommunications carriers report Internet traffic growth of 17% year-over-year , with data centre operators managing network throughputs exceeding 400 Gbps on individual spine-leaf network segments.

The Market addresses this complexity through solutions integrating NetFlow analysis, deep packet inspection, and machine learning-driven behavioural analytics, enabling real-time traffic classification and anomaly detection. Cloud infrastructure adoption by 94% of enterprises generates hybrid IT environments combining on-premises data centres, public cloud platforms (AWS, Azure, Google Cloud), and edge computing nodes that traditional network monitoring tools cannot adequately address.

Enterprise organisations specify network traffic analyzers capable of unified visibility across distributed infrastructure: Arista Networks' CloudVision Universal Network Observability (CV UNO) platform exemplifies this requirement through integration of network infrastructure performance with compute and server system data, delivering end-to-end visibility across data centre, campus, and wide area networks. The transition toward Software-Defined Networking (SDN), Network Function Virtualisation (NFV), and containerised infrastructure introduces programmatic network management requiring continuous traffic analysis to validate performance SLAs and security policies.

Advanced Threat Detection and Machine Learning-Driven Security Operations Evolution

Modern cybersecurity threat landscapes necessitate network traffic analyser solutions incorporating artificial intelligence and machine learning algorithms capable of identifying unknown attack vectors, advanced persistent threats, and zero-day exploits that signature-based detection systems cannot address. Organisations implementing traditional rule-based network security controls experience false-positive rates exceeding 45%, creating alert fatigue that undermines security operations effectiveness and increases mean-time-to-detection (MTTD) for actual threats.

The Market accelerates demand for AI/ML-based solutions, overcoming these limitations through behavioural analytics, unsupervised learning models, and anomaly detection algorithms that identify network traffic patterns deviating from established baselines. Broadcom's strategic launch of Trident 5-X12 network chip (November 2023) featuring an on-chip neural-network inference engine (NetGNT) demonstrates technological convergence toward hardware-accelerated network traffic analysis capable of detecting complex traffic patterns such as AI/ML workload "incast" congestion at line rate without performance degradation. Organisations implementing network traffic analysers report a 63% reduction in mean-time-to-response (MTTR) following AI/ML implementation compared to baseline rule-based systems.

Government agencies and critical infrastructure operators specify network traffic analysers with integrated threat intelligence feeds, enabling real-time correlation of observed network flows against known command-and-control infrastructure, malware signatures, and threat actor indicators. This intelligence-driven analytics capability addresses sophisticated state-sponsored attacks increasingly targeting telecommunications infrastructure and financial systems, driving network traffic analyser adoption within government and BFSI segments.

Restraint - Integration Complexity and Legacy Infrastructure Compatibility Challenges

Organisations deploying network traffic analysers face substantial implementation complexity arising from heterogeneous network infrastructure encompassing legacy switching platforms, proprietary network protocols, and decentralised monitoring architectures resistant to unified visibility integration.

Enterprises managing network infrastructure across multiple technology generations report that 38% of network traffic analyser implementations exceed projected deployment timelines by 6-12 months due to compatibility complications with existing management systems (NetFlow collectors, SIEM platforms, NPM tools). Network virtualisation technologies and container orchestration platforms (Kubernetes) introduce additional complexity: network traffic captured at the hypervisor, virtual switch, or container runtime requires architectural adjustments to existing packet capture strategies, preventing straightforward migration from physical network monitoring to cloud-native environments.

Organisations report total cost of ownership (TCO) challenges arising from ongoing integration expenses, specialised personnel requirements for network telemetry configuration, and continuous software updates necessitating operational disruption, collectively constraining budget allocation and limiting market penetration in cost-sensitive customer segments.

Opportunity - AI-Driven Network Observability and Predictive Anomaly Detection Integration

The emerging opportunity for Network Traffic Analyzer Market growth lies in evolving network traffic analyzer solutions from reactive threat detection platforms toward proactive, predictive observability systems leveraging artificial intelligence to anticipate network anomalies, optimise traffic flows, and enable automated remediation before performance degradation or security incidents manifest.

Traditional network traffic analyzers operate in detection and response mode, identifying anomalies after occurrence; next-generation solutions incorporating AI/ML algorithms enable forecasting of network congestion patterns, automatic baselining of acceptable traffic profiles, and behavioural learning systems that adapt continuously to organizational network evolution.

Arista Networks' March 2025 launch of advanced Cluster Load Balancing (CLB) with AI job-centric observability through CloudVision Universal Network Observability demonstrates this opportunity: CLB optimises Ethernet-based AI cluster workloads using RDMA-aware flow placement, delivering millisecond-precision visibility into microsecond-level traffic patterns within large-scale compute clusters. This capability addresses unmet enterprise demand for network observability in AI-intensive environments where traditional network monitoring proves inadequate.

Organisations implementing predictive network traffic analysers report 41% reduction in unplanned network downtime and a 34% improvement in application performance through proactive congestion avoidance. The opportunity encompasses integration of network traffic analysers with AIOps (Artificial Intelligence for IT Operations) platforms that correlate network telemetry with application performance data, system logs, and business transaction metrics, enabling holistic incident causation analysis and automated remediation orchestration. This convergence creates premium pricing opportunities for vendors delivering integrated visibility across infrastructure layers previously requiring separate point solutions.

Managed Services and Outsourced Network Operations Expansion

The global telecommunications infrastructure modernisation toward 5G networks generates substantial opportunity for Network Traffic Analyzer Market vendors providing specialised solutions addressing unique 5G architecture characteristics and performance monitoring requirements. 5G networks introduce network slicing, edge computing functions, and virtualised infrastructure fundamentally distinct from legacy 4G architectures, requiring network traffic analyzers capable of monitoring service function chains, network slice performance, and radio access network metrics.

Telecommunications operators deploying 5G infrastructure report that traditional network traffic analyzers prove inadequate for monitoring network slice traffic isolation, virtual RAN (vRAN) resource utilisation, and ultra-low-latency requirements. Organisations specify network traffic analyzers with 5G-optimised telemetry collection (O-RAN compliant metrics), enabling visibility into network slice performance, edge computing traffic flows, and application-induced network optimisation requirements.

Government-mandated 5G infrastructure buildout investments exceed US$100 billion cumulatively across developed markets (North America, Europe) and emerging Asia-Pacific economies, directly translating to network traffic analyzer procurement across telecommunications carriers.

India's 5G network deployment (commenced 2022, projected completion 2025) involves 800,000+ base stations requiring network traffic analyzer deployment for capacity planning, interference detection, and security monitoring. This telecommunications infrastructure modernisation represents multi-year procurement opportunity for network traffic analyzer vendors with specialised 5G network monitoring capabilities.

Category-wise Analysis

Solution Module Insights

Solutions segment commands 72.0% market share in the Network Traffic Analyzer Market in 2026, reflecting customer preference for packaged software platforms combining packet capture, flow analysis, metadata processing, and visualisation capabilities within integrated solutions. This segment encompasses software platforms deployable on physical appliances, virtual machines, containerised environments, and cloud infrastructure, enabling organizations to specify deployment modes matching infrastructure architecture preferences.

Solutions segment leadership reflects customer investment patterns: organizations prioritize solution functionality breadth (flow analysis capabilities, deep packet inspection, machine learning analytics, integration with SIEM/SOC platforms) as determinative purchasing criteria, with management services and professional implementation characterized as secondary value-add components supporting solution adoption.

GL Communications' April 2025 launch of FastRecorder™ and PacketExtractor™ high-speed Ethernet capture applications exemplifies solutions segment evolution toward specialised packet processing capabilities: these tools enable wirespeed packet filtering and recording at 320 Gbps across multiple Ethernet interfaces with millisecond precision, addressing specialised use cases in network troubleshooting and traffic extraction. The solutions segment encompasses diverse functionality tiers from basic NetFlow analysis platforms to comprehensive network observability suites integrating packet capture, flow analysis, behavioural analytics, and threat intelligence correlation within unified interfaces.

Industry Insights

The telecommunications and service providers segment commands 26.0% market share in the Network Traffic Analyzer Market in 2026, reflecting regulatory mandates requiring carrier-grade network monitoring infrastructure and competitive differentiation through superior network performance and reliability. Telecommunications operators deploy Network Traffic Analyzer solutions addressing multiple operational requirements: capacity planning (traffic forecasting enabling infrastructure investment optimisation), congestion management (identifying network bottlenecks enabling traffic engineering optimisation), and security monitoring, detecting unauthorised access, anomalous traffic patterns, and denial-of-service attacks.

The FCC's January 2025 Declaratory Ruling mandating telecommunications carriers to secure networks under CALEA Section 105 directly compels network traffic analyser deployment across the U.S. telecommunications infrastructure. Telecommunications operators report that network traffic analyser solutions generate operational efficiency improvements: AT&T's network analytics implementation enabled 12% improvement in network utilisation efficiency and 31% reduction in mean-time-to-resolution for network incidents.

International telecommunications operators, which include Deutsche Telekom, Vodafone, Orange, Singapore Telecommunications, similarly specify enterprise-grade network traffic analyser solutions supporting carrier-class reliability, scalability to exabyte-scale traffic volumes, and integration with operations support systems (OSS) and business support systems (BSS).

The IT and Cloud Providers / Data Centres segment represents the fastest-growing end-user industry within the Network Traffic Analyser Market, driven by explosive growth in cloud infrastructure adoption, hyperscaler expansion, and data center buildout requirements. Cloud infrastructure providers (AWS, Microsoft Azure, Google Cloud, Alibaba Cloud) operate massive distributed data centre networks processing exabyte-scale traffic volumes daily, necessitating sophisticated network traffic analyzer solutions enabling real-time visibility across distributed infrastructure spanning multiple regions and availability zones.

Regional Insights and Trends

North America Network Traffic Analyzer Market Trends

North America commands 34% of the global Network Traffic Analyzer Market share, representing the largest mature market for network infrastructure monitoring, driven by advanced technology adoption, substantial enterprise IT spending, and regulatory mandates compelling network security infrastructure investment. The region encompasses the United States, the primary market driver, Canada, and Mexico. North America's market dominance reflects technological infrastructure maturity, with enterprises operating hybrid cloud environments combining on-premises data centres with public cloud consumption, necessitating comprehensive network observability solutions spanning distributed systems.

The FCC's regulatory mandates, such as CALEA Section 105 Declaratory Ruling and proposed cybersecurity risk management plan requirements, drive telecommunications carrier network traffic analyser investment across North America. Critical infrastructure operators in energy, financial services, and defence across the United States prioritise network traffic analyser deployment as a foundational security control supporting federal cybersecurity directives, including the Executive Order on Cybersecurity and NIST Cybersecurity Framework requirements.

The North American regulatory environment creates sustained compliance-driven demand for network traffic analyser solutions independent of economic cycles. The Securities and Exchange Commission (SEC) Cybersecurity Disclosure Requirements, effective February 2023, mandate public companies disclose material cybersecurity incidents within four business days of occurrence, creating operational necessity for network traffic analysers enabling real-time threat detection and incident response documentation. Financial services organisations subject to SEC requirements, federal banking agency examinations, and FINRA rules specify network traffic analysers as mandatory infrastructure supporting regulatory compliance demonstrations. Government agencies across federal, state, and local levels implement zero-trust security architectures requiring continuous network monitoring directly supported by network traffic analyzer deployment.

East Asia Network Traffic Analyzer Market Trends

East Asia represents 17% of the global network traffic analyser market share with substantially accelerating growth rates compared to North American mature market dynamics. The region encompasses China, Japan, and South Korea, each with distinct regulatory frameworks and organisational technology adoption patterns. China's network traffic analyser market demonstrates exceptional growth, driven by rapid 5G infrastructure deployment (1.3 million base stations by 2024), extensive 5G service expansion across urban centres, and government initiatives supporting "smart cities" and industrial automation. China's digital economy represents 41.5% of national GDP (US$ 7.25 trillion in 2022), generating unprecedented data volumes requiring sophisticated network monitoring infrastructure.

Japan's Society 5.0 strategy and investment in AI-optimised data centers drive network traffic analyzer adoption within cloud providers and technology companies supporting advanced AI workload optimisation.

East Asian governments actively promote digital infrastructure modernisation through strategic investments and regulatory frameworks explicitly requiring network security monitoring. China's "New Infrastructure" initiative encompasses 5G network buildout, data centre expansion, and cloud computing infrastructure development, all requiring sophisticated network traffic analyser deployment for performance optimisation and security assurance. Singapore's Smart Nation initiative and government digital transformation programs create network monitoring requirements for public sector organisations. India's Digital India programme and emerging cybersecurity guidelines (Indian Computer Emergency Response Team (CERT-In) recommendations) establish baseline network security requirements, driving enterprise adoption of network traffic analyser solutions.

Europe Network Traffic Analyzer Market Trends

Europe commands 27% of the global Network Traffic Analyser Market share with distinctive characteristics reflecting stringent regulatory frameworks and emphasis on data privacy infrastructure. The European market encompasses European Union member states plus non-EU countries (Switzerland, Iceland, Norway) and the UK post-Brexit, collectively representing approximately 500 million population with an advanced telecommunications infrastructure and substantial enterprise technology spending.

The European Network Traffic Analyser Market demonstrates moderate growth compared to East Asian acceleration, reflecting market maturity and comprehensive regulatory compliance frameworks already embedded in enterprise purchasing decisions. European organisations maintain higher baseline network monitoring investments than global peers due to GDPR compliance requirements, NIS2 Directive mandates, and strict data protection frameworks.

Competitive Landscape

The global network traffic analyser market is consolidated in nature, dominated by a few major players that hold a significant share of the market, while several smaller vendors compete for niche opportunities. The market’s consolidation is driven by high technological barriers, extensive R&D requirements, and the need for integrated solutions that provide real-time visibility, analytics, and security across enterprise and service provider networks.

Arista Networks, Broadcom Inc., Cisco Systems, Inc., Juniper Networks, Inc., SolarWinds Corporation, and Riverbed Technology, Inc. are recognised as leading vendors, offering advanced network traffic monitoring, AI-driven analytics, and cloud-integrated observability solutions. These players leverage innovation in telemetry, packet capture, machine learning, and high-speed switching platforms to differentiate their offerings.

The competitive intensity is further amplified by continuous technology upgrades, the rising adoption of cloud networking, IoT devices, and increasing enterprise emphasis on network performance and cybersecurity. Companies compete based on product capabilities, scalability, deployment flexibility, and advanced analytics features.

Key Industry Developments:

- In September 2025 - Cloudflare expanded its Radar platform with regional Internet traffic insights and detailed Certificate Transparency (CT) data, enhancing granular visibility into network traffic trends and Internet health. The update enables localised monitoring of bytes and requests, device type breakdowns, and bot versus human traffic at sub-national levels, allowing enterprises and network operators to analyse network performance and security more precisely across regions and autonomous systems.

- In March 2025 - Arista Networks introduced advanced Cluster Load Balancing (CLB) in Arista EOS® and AI job-centric observability through CloudVision® Universal Network Observability™ (CV UNO™), enhancing network traffic analysis for large-scale AI clusters. CLB optimises Ethernet-based AI workloads using RDMA-aware flow placement, ensuring uniform traffic distribution, low latency, and consistent high performance across leaf-spine network topologies.

- CV UNO provides end-to-end AI job visibility by unifying network, system, and AI job telemetry in real time via NetDL Streamer, enabling precise anomaly detection, flow visualisation, and rapid troubleshooting. These innovations allow network operators to monitor microsecond-level traffic, optimise AI workloads, and proactively resolve network performance bottlenecks, strengthening observability and operational efficiency for AI-driven enterprise networks.

Companies Covered in Network Traffic Analyser Market

- Arista Networks, Inc.

- Broadcom

- Cloudflare, Inc.

- Fortra, LLC

- Kentik

- Zoho Corporation Pvt. Ltd.

- NEC Corporation

- NETSCOUT

- Netreo

- Progress Software Corporation

Frequently Asked Questions

The global Network Traffic Analyzer market is projected to be valued at US$ 3.4 Bn in 2026.

The Solution segment is expected to account for approximately 72.0% of the global Network Traffic Analyzer market in 2026.

The market is expected to witness a CAGR of 9.8% from 2026 to 2033.

Regulatory compliance mandates, digital infrastructure transformation with growing cloud-native complexity, and the rising need for AI/ML-driven advanced threat detection collectively drive the Network Traffic Analyzer market growth.

AI-driven predictive observability, AIOps integration, and expanding 5G and managed network operations create major growth opportunities in the Network Traffic Analyzer market.

Key players in the Network Traffic Analyzer market include NETSCOUT Systems, SolarWinds, Broadcom, Kentik, Arista Networks, and Cloudflare.