- Telecommunications

- Dark Fibre Network Market

Dark Fibre Network Market Size, Share, and Growth Forecast, 2026 - 2033

Dark Fiber Network market by Fiber Type (Single-Mode Fiber (SMF), Multi-Mode Fiber (MMF)), Network Type (Metro Network, Long-Haul Network, Ultra-Long-Haul / Submarine), Deployment Type (Underground Fiber, Aerial Fiber, Hybrid Deployment) End user (Telecom Operators & ISPs, Data Centers & Cloud Service Providers, Enterprises & Corporates, Government & Defense, Smart Cities / IoT Applications), Bandwidth Capacity (Low Capacity (<10 Gbps), Medium Capacity (10–100 Gbps), High Capacity (>100 Gbps)) and Regional Analysis for 2026 - 2033

Dark Fiber Network Market Size and Trends Analysis

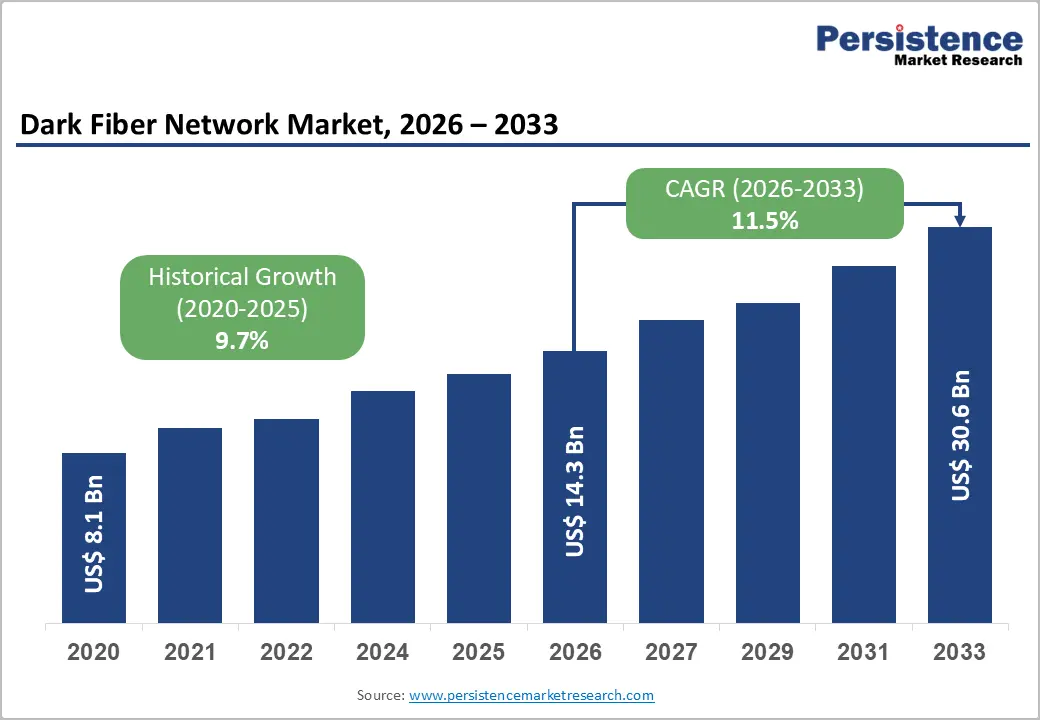

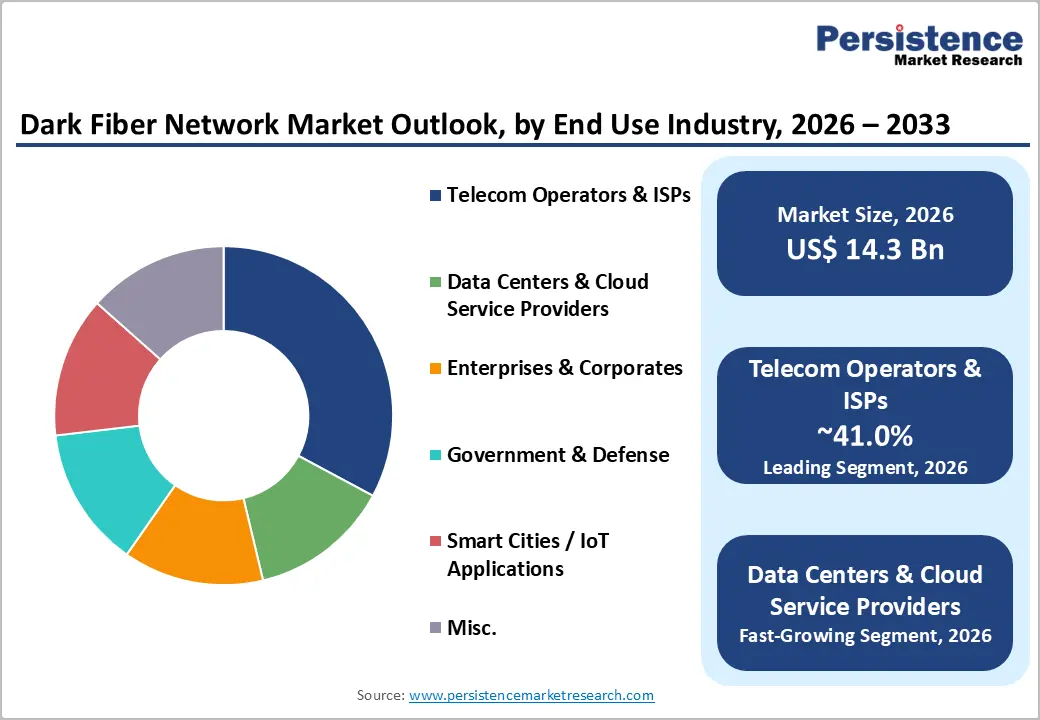

The global dark fiber network market size is likely to be valued at US$ 14.3 billion in 2026 and is projected to reach US$ 30.6 billion by 2033, growing at a CAGR of 11.5% during the forecast period. The global market is experiencing unprecedented momentum driven by the exponential surge in bandwidth-intensive applications, cloud infrastructure expansion, and 5G network densification. The market's robust growth trajectory reflects fundamental shifts in how enterprises prioritise network architecture, transitioning from carrier-managed connectivity services toward sovereign, dedicated optical fiber infrastructure.

Three primary catalysts propel this expansion: the extraordinary computational demands of artificial intelligence and machine learning workloads, global deployment of next-generation mobile networks requiring high-capacity backhaul architecture and accelerating digitalisation of emerging economies through government-led broadband initiatives. Organisations increasingly recognise dark fibre as strategic infrastructure rather than excess capacity, valuing the combination of scalable bandwidth, deterministic performance, and full operational control.

Key Industry Highlights:

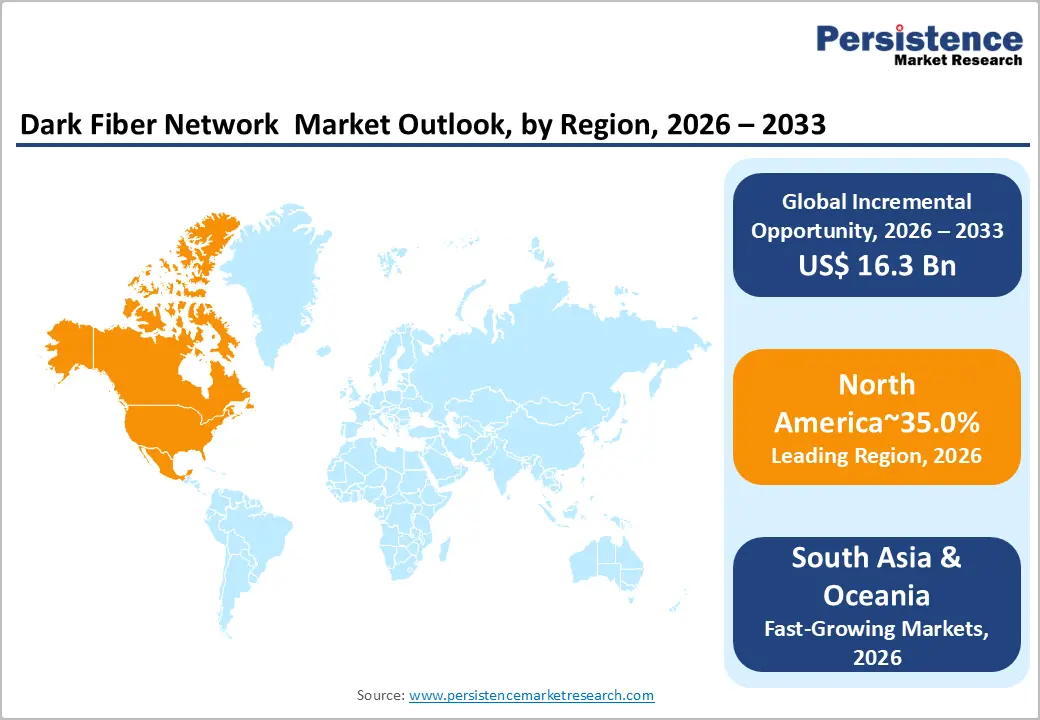

- Leading Region: North America dominates the Dark Fiber Network Market with ~35% share in 2025, driven by extensive telecom infrastructure, hyperscale data centre expansion, and major operators such as AT&T, Verizon, Zayo, and Uniti Group.

- Fastest-Growing Region: East Asia accounts for ~20% share, fueled by China’s state-backed fiber deployments, Japan’s advanced telecom infrastructure, and emerging open-access networks in India.

- Dominant Fiber Type Segment: Single-Mode Fiber leads the market with ~82% share in 2026, reflecting its suitability for long-haul, high-capacity transmissions connecting data centres, backbone networks, and metro systems.

- Fastest-Growing Network Type Segment: Long-Haul networks are expanding rapidly, driven by transcontinental data center interconnections, international cloud provider investments, and cross-border telecom backbone projects.

- Key End-user: Telecommunications Operators & ISPs lead with ~41% share, relying on dark fiber for 5G backhaul, metro capacity expansion, and broadband service delivery.

- Fastest-Growing End-user: Data Centers & Cloud Service Providers represent the fastest-growing segment, driven by AI workloads, multi-cloud strategies, and hyperscale infrastructure requirements.

- Strategic Developments: Key acquisitions and high-capacity network deployments, including NGN’s acquisition of netcon AG and DFA’s 1.6 Tbps single-wavelength transmission milestone, reinforce infrastructure expansion and technological leadership.

| Key Insights | Details |

|---|---|

|

Dark Fiber Network Market Size (2026E) |

US$ 14.3 Bn |

|

Market Value Forecast (2033F) |

US$ 30.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

11.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.7% |

Market Dynamics

Growth Drivers

Exponential Growth in Cloud Computing and AI Infrastructure Demand

Artificial intelligence and cloud computing have fundamentally transformed network infrastructure requirements across enterprise and hyperscale ecosystems. The explosive proliferation of large language models, GPU-accelerated workloads, and real-time data analytics necessitate connectivity solutions capable of supporting terabit-scale throughput with sub-millisecond latency characteristics. Dark fiber networks deliver precisely these performance attributes, enabling organisations to scale capacity from 10 Gbps to 400 Gbps and beyond without renegotiating service contracts or incurring recurring bandwidth fees.

Major cloud hyperscalers, including Amazon Web Services, Microsoft Azure, and Google Cloud, have substantially expanded dark fiber procurement to support inter-data-centre traffic, distributed AI training synchronisation, and low-latency multi-cloud strategies. Industry analysis indicates that AI processing infrastructure investments will compound at unprecedented rates through 2030, with dark fiber connectivity representing the critical backbone enabling these deployments.

The Dark Fiber Network Market benefits directly from this transition, as enterprises increasingly recognise that dedicated optical pathways provide superior total cost of ownership compared to managed lighting services when handling sustained, high-volume traffic profiles. This is particularly pronounced among financial trading firms, which rely on dark fiber to achieve deterministic latency of 93 microseconds between major trading hubs, and among content delivery networks requiring carrier-neutral, fully controllable transmission paths.

5G and Next-Generation Mobile Network Densification

The worldwide rollout and expansion of 5G infrastructure has substantially elevated demand for dark fiber networks capable of supporting high-capacity backhaul and fronthaul connectivity between distributed radio units, centralised processing units, and core network facilities. The transition to Open RAN architectures mandates ultra-low-latency fibre pathways meeting sub-250 microsecond timing requirements, a performance threshold that dark fiber delivers through dedicated, uncontended transmission paths. Telecommunications operators, including AT&T, Verizon, and major European carriers, have accelerated dark fiber network deployments to address the technical requirements of 5G small-cell densification, particularly within metropolitan areas where subscriber density justifies massive infrastructure investment.

Government initiatives are catalysing this expansion on a large scale. India's BharatNet program has connected 2,14,325 Gram Panchayats with 6.93 lakh kilometres of optical fiber cable, establishing foundational dark fiber infrastructure supporting 4G, 5G, and future broadband services across rural and underserved regions.

The Market expands in tandem with these state-sponsored deployments, as operators recognise that fibre-based transport infrastructure provides the flexibility and future-proofing necessary to accommodate successive technology generations from current 5G implementations toward anticipated 6G developments. This durability explains why telecommunications service providers view dark fiber deployment as strategic capital allocation.

Restraint - High Initial Capital Expenditure and Complex Deployment Economics

Dark fiber network deployment requires substantial upfront capital investment for fiber acquisition, route rights procurement, conduit infrastructure, and network illumination equipment. Organizations must finance these infrastructure costs before generating revenue, creating significant financial barriers particularly for smaller providers and regional operators lacking access to large-scale capital markets.

The complexity of coordinating with multiple utility companies, municipal authorities, and real estate entities to secure fiber routes and deployment rights substantially extends project timelines and increases implementation costs, limiting expansion velocity and favouring large, well-capitalised providers.

Opportunity - Rural Broadband Expansion Through Public-Private Infrastructure Models

Governments across Asia, Africa, and Latin America are accelerating rural broadband deployment to narrow persistent digital access gaps, creating substantial procurement opportunities for dark fiber infrastructure providers. India's BharatNet initiative represents a transformational model connecting over 2.13 lakh Gram Panchayats through optical fiber networks while establishing platforms for future connectivity expansion.

The Amended BharatNet Program extends this ambition by targeting optical fiber connectivity for an additional 42,000 uncovered Gram Panchayats and on-demand service to 3.84 lakh villages. Similarly, eX² Technology initiated a 100-mile middle-mile open-access dark fiber network deployment in Navajo County, Arizona, through public-private partnership models, demonstrating how strategic fiber infrastructure enables broadband access, telehealth services, and municipal connectivity across previously unserved territories.

These initiatives underscore a broader structural shift: governments and regulatory bodies increasingly treat dark fiber as national digital infrastructure essential for economic development and competitive positioning. The Dark Fiber Network Market stands to benefit substantially from this policy reorientation, as procurement for government-sponsored broadband programs typically involves multi-year commitments and substantial capital allocation.

The addressable market for rural connectivity represents billions of dollars in potential infrastructure investment, with dark fiber serving as the foundational technology enabling subsequent service delivery and economic development across underserved populations.

AI and Hyperscale Data Centre Interconnection Requirements

The explosive growth of distributed artificial intelligence workloads, hyperscale data centre expansion, and multi-cloud enterprise strategies is creating unprecedented demand for dark fibre networks linking data centres across metropolitan regions, national territories, and international geographies. Light Source Communications deployed strategically located dark fibre networks in high-demand data center markets, including Las Vegas, Kansas City, and Phoenix, targeting hyperscaler and enterprise customers requiring carrier-neutral, ultra-low-latency connectivity. These deployments directly support GPU cluster synchronisation, distributed model training, and real-time workload migration critical requirements for organizations deploying AI infrastructure at scale.

The global market is positioned at the epicentre of AI infrastructure expansion, with demand from cloud service providers, artificial intelligence-specialised companies, and enterprises undertaking digital transformation initiatives, creating a multi-year growth runway. Industry forecasts indicate that data centre connectivity investments will remain elevated through 2030, driven by the continuous evolution of AI capabilities, expansion of edge computing infrastructure, and proliferation of specialised AI chips requiring dedicated, controllable network pathways. Organisations leveraging dark fibre achieve 60% or greater cost savings over five-year periods when managing traffic volumes exceeding 10 Gbps, creating compelling financial incentives for sustained procurement and network expansion.

Category-wise Analysis

Fibre Type Insights

Single-Mode Fiber dominates the Dark Fiber Network Market by capturing 82.0% of the market share in 2026, reflecting its superior performance characteristics for long-distance transmission and high-capacity applications. SMF's capability to transmit signals over extended distances without signal degradation makes it indispensable for long-haul network architectures supporting national backbone deployments and inter-regional connectivity. Telecommunications operators, hyperscale data centre providers, and international carriers prioritise SMF infrastructure for strategic network segments where distance or capacity requirements exceed Multi-Mode Fibre capabilities. This dominant position reflects market maturity and established deployment standards across telecommunications and enterprise networking domains.

Multi-Mode fiber represents the fastest-growing segment within the Fiber Type category, driven by metro network densification, data centre interconnection applications, and edge computing infrastructure buildout. MMF delivers cost-effective solutions for short-to-medium distance applications, enabling organisations to optimize infrastructure economics by matching fibre type to specific transmission distance and bandwidth requirements.

Network Type Insights

Metro networks capture 48.0% of the dark fibre network market in 2026, reflecting the concentration of data center, financial services, and enterprise connectivity demand within metropolitan areas. Metropolitan regions host the highest concentration of data centers, cloud service provider facilities, and enterprise customer premises, driving sustained dark fiber procurement for intra-city and metropolitan-region connectivity. Major urban centers, including New York, London, Tokyo, and Singapore, represent high-value metro network markets where competitive intensity justifies extensive dark fiber deployments and premium pricing reflects limited available infrastructure alternatives. This leading position demonstrates that dark fiber deployment prioritizes high-value, densely connected geographic markets where customer concentration justifies substantial infrastructure investment.

Long-Haul networks represent the fastest-growing network type segment, driven by transcontinental data center expansion, international cloud provider investments, and strategic telecommunications backbone buildout. Organizations, including C3ntro Telecom, advanced the Tikva Project, a 2,500-kilometer fiber optic network connecting Phoenix, Arizona to Querétaro, Mexico, establishing fully underground, low-latency, redundant cross-border connectivity. Uniti Group executed a long-term agreement with a global internet provider to deliver long-haul dark fiber across 12 cities in the Central and Southeastern United States, covering approximately 3,100 route miles.

End-user Insights

Telecommunications operators and internet service providers capture 41.0% of the Dark Fiber Network Market, reflecting their fundamental reliance on fiber infrastructure for backbone transport, mobile network backhaul, and broadband service delivery. Telecom operators, including AT&T, Verizon, and major European carriers, utilise dark fiber networks to support 5G small-cell densification, increase metro capacity, and establish regional backbone redundancy. ISPs leverage dark fiber to extend broadband coverage into underserved territories and establish carrier-neutral interconnection points supporting multi-provider competitive markets. The leading position of telecommunications operators underscores that the Dark Fiber Network Market remains fundamentally anchored to traditional telecommunications infrastructure requirements.

Data centers and cloud service providers represent the fastest-growing end-user segment, reflecting hyperscale infrastructure expansion, artificial intelligence workload concentration, and multi-cloud enterprise strategies. Major operators, including Equinix and Digital Realty, have substantially expanded dark fiber procurement and provisioning capabilities, with Equinix offering Fiber Connect dark fiber links between customer facilities within multiple data centres and Digital Realty achieving record leasing activity in 2024, driven substantially by hyperscale data center demand.

Regional Insights and Trends

North America Market Trend

North America represents the largest regional market for dark fiber networks, accounting for 35% of global market share and demonstrating sustained growth driven by telecommunications infrastructure investment, cloud hyperscaler expansion, and financial services connectivity requirements. The United States dominates North American dark fiber deployment, with major telecommunications carriers including AT&T, Verizon, and CenturyLink/Lumen Technologies maintaining extensive dark fiber networks spanning metropolitan and long-haul routes. AT&T announced in 2025 that it would deploy billions in tax savings toward accelerated fiber expansion, targeting over 60 million locations by 2030, representing one of the largest private infrastructure investments in broadband history.

Zayo Group, a native dark fiber provider, operates across 400 markets worldwide, providing access to over 44,000 on-net buildings and 1,400 on-net data centers. Light Source Communications expanded its aggressive market presence through strategic deployments, including a 35-mile dark fiber network in Kansas City, Missouri and a 60-mile network in Las Vegas, Nevada, specifically targeting hyperscaler and enterprise customers requiring carrier-neutral connectivity. Uniti Group owns and operates 135,000 route miles of dark fiber, serving approximately 300 metro markets and reaching over 275,000 on-net and near-net buildings. Windstream Holdings operates a nationwide dark and lit fiber network covering 170,000 route miles, with significant portions owned rather than leased a strategic positioning supporting long-term margin optimization.

East Asia Dark Fiber Network Market Trends

East Asia represents a rapidly expanding dark fiber market driven by China's infrastructure-focused development model, India's government broadband initiatives, and Japan's advanced telecommunications requirements. China leads the region through state-sponsored backbone fiber deployments coordinated by telecommunications operators, including China Telecom, China Mobile, and China Unicom. The "New Infrastructure" policy, emphasising 5G, data centres, and digital connectivity, has accelerated dark fibre deployment across nationwide routes and high-speed railway corridors.

Japan maintains an advanced telecommunications infrastructure with widespread fiber-optic network coverage supporting enterprise connectivity, financial services operations, and consumer broadband services. Regional dark fibre providers, including Dr. Peng Telecom in China and emerging operators in India are establishing open-access networks serving enterprises and cloud providers.

The region's combination of government-led infrastructure initiatives, sustained enterprise demand, and hyperscale data centre expansion positions East Asia for accelerating dark fiber market growth, supported by structural improvements in digital infrastructure accessibility and application development.

Europe Dark Fibre Market Trends

Europe represents a mature, sophisticated dark fiber market driven by extensive telecommunications infrastructure, data center concentration, and regulatory frameworks supporting competitive open-access connectivity. Native dark fiber providers, including euNetworks, Eurofiber, and Colt Technology Services, maintain extensive metropolitan and long-haul networks supporting cross-border connectivity and regional integration requirements. euNetworks operates a dark fiber network spanning 45,800 kilometres throughout Western Europe, managing 17 fibre-based metropolitan networks interconnected by 42,600 kilometres of long-haul infrastructure directly connecting 2,539 locations, including over 510 data centers.

Eurofiber owns and operates dark fiber networks in the Netherlands, Belgium, France, and Germany, with infrastructure spanning over 61,700 kilometers and connecting to 12,000 locations. euNetworks extended its dark fiber network in Belgium through the acquisition of a Belgian utility's dark fiber business in March 2023, adding 1,660 kilometers of duct-based fiber routes connected to major data centres. These transactions reflect active consolidation within European dark fiber markets and substantial investment in infrastructure expansion supporting cloud providers, hyperscalers, and mobile network operators.

European regulatory frameworks, including the European Electronic Communications Code establish open-access requirements and promote competition within fiber markets, creating incentives for dark fiber deployment competing with incumbent telecommunications operators.

Competitive Landscape

The global dark fiber network market is moderately consolidated, dominated by a few large players while still featuring fragmentation at regional levels. Leading companies such as Zayo Group, AT&T Inc., Verizon Communications, Lumen Technologies, Crown Castle, and euNetworks hold significant market share through extensive fiber assets, long-haul networks, and strategic partnerships with hyperscalers and enterprises. High capital requirements and entrenched infrastructure agreements create barriers to entry, giving incumbents a competitive advantage.

Smaller regional providers and niche players contribute to market fragmentation, serving localised enterprises and metropolitan segments. Mergers and acquisitions are commonly used to expand network footprints and service offerings. The market is driven by rising demand for 5G backhaul, cloud connectivity, and low-latency networks, reinforcing the positions of top-tier firms while maintaining competitive pressures at the edges.

Key Industry Developments

- On 05 December 2025, NGN Fiber Network GmbH & Co. KG acquired netcon AG, significantly enhancing its position in the German dark fiber market. This acquisition expanded NGN’s open-access digital infrastructure, complemented its existing network, and increased its dark fiber footprint to approximately 21,000 km, supporting long-term growth and network synergies.

- On 27 August 2025, Dark Fibre Africa (DFA), in partnership with Ciena and Willcom, achieved a world-first transmission of 1.6 Tbps over a single wavelength on its dark fiber network in South Africa. This milestone underscores DFA’s capability to deliver next-generation high-capacity services, demonstrating the scalability, reliability, and future-readiness of dark fiber infrastructure to meet growing demand from cloud, AI, and 5G applications.

Companies Covered in Dark Fibre Network Market

- AT&T Inc.

- Colt Technology Services Group Limited

- Comcast Corporation

- Consolidated Communications

- GTT Communications, Inc.

- Lumen Technologies, Inc.

- Verizon Communications, Inc.

- Windstream Intellectual Property Services, LLC

- Zayo Group, LLC

- Fiber Light, LLC

Frequently Asked Questions

The global Dark Fiber Network market is projected to be valued at US$ 14.3 Bn in 2026.

The Telecom Operators & ISPs End User segment is expected to account for approximately 41% of the global Dark Fiber Network market by component type in 2026.

The market is expected to witness a CAGR of 11.5% from 2026 to 2033.

The Dark Fiber Network Market is primarily driven by the explosive demand for cloud computing, AI infrastructure, and 5G network densification, requiring scalable, low-latency, high-capacity fiber connectivity for hyperscalers, enterprises, and telecom operators.

The Dark Fiber Network Market presents significant opportunities in rural broadband expansion through public-private infrastructure initiatives and interconnection of hyperscale data centers to support AI, multi-cloud, and low-latency enterprise workloads.

Key players in the Dark Fiber Network market include AT&T Inc., Verizon Communications, Lumen Technologies, Comcast Corporation, and Zayo Group.