- Communication Infrastructure & Services

- Mobile Virtual Network Operator Market

Mobile Virtual Network Operator Market Size, Share, and Growth Forecast 2026 - 2033

Mobile Virtual Network Operator Market by Operational Model (Reseller, Service Provider, Full MVNO), by Subscriber (Consumer, Enterprise), by Service (Postpaid, Prepaid), by Application (Discount, Cellular M2M, Business, Media & Entertainment, Migrant, Retail, Roaming, Telecom), by Regional Analysis, 2026 - 2033

Mobile Virtual Network Operator Market Size and Trend Analysis

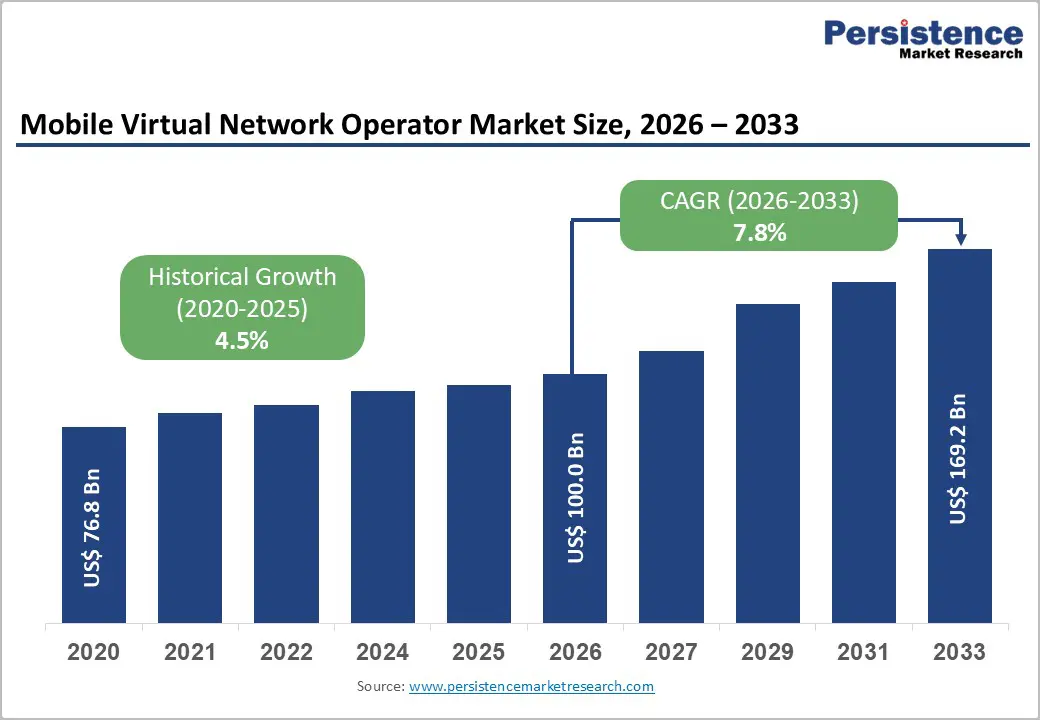

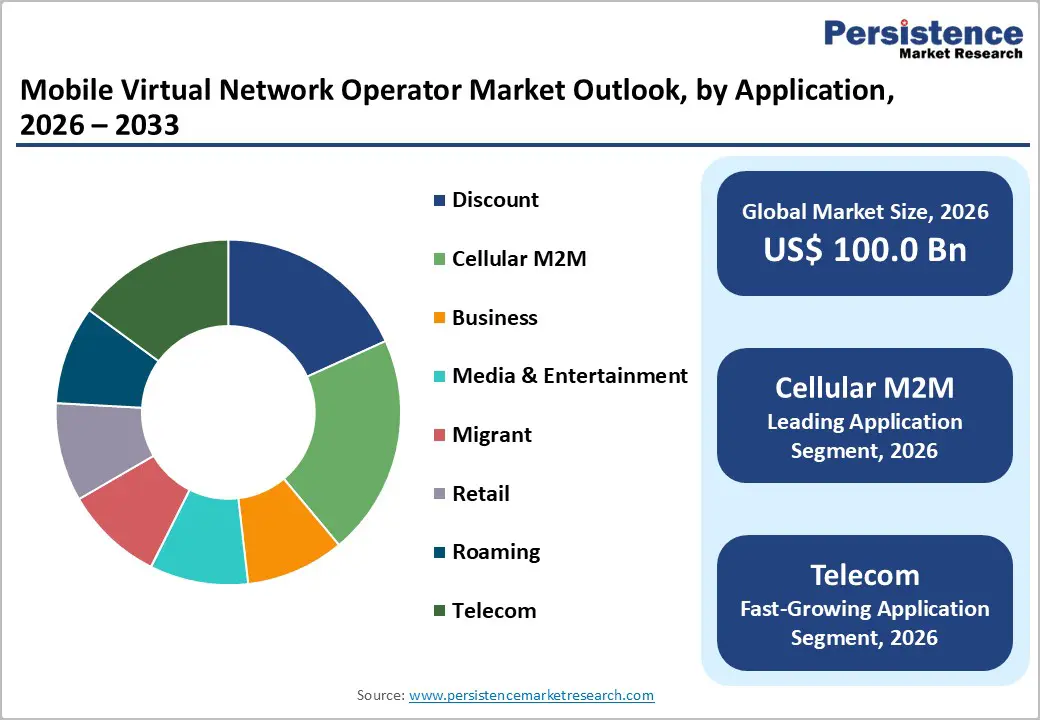

The global Mobile Virtual Network Operator market size is expected to be valued at US$ 100.0 billion in 2026 and projected to reach US$ 169.2 billion by 2033, growing at a CAGR of 7.8% between 2026 and 2033.

Growth is driven by rising demand for affordable and flexible mobile plans as data consumption and smartphone penetration accelerate worldwide. Consumers increasingly prefer prepaid and non-contract offerings, while enterprises adopt MVNO solutions for customized connectivity and IoT applications. With 5.6 billion mobile internet users globally in 2024 (GSMA), the customer base continues to expand. Expanding 5G wholesale access further strengthens MVNO competitiveness and service differentiation.

Key Industry Highlights:

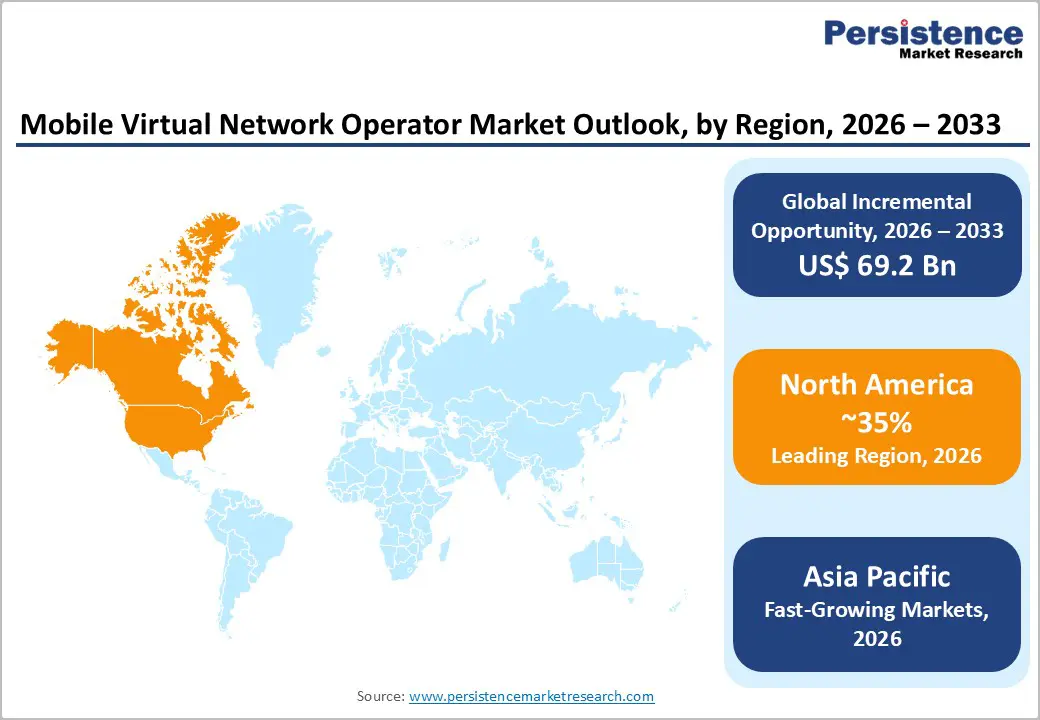

- Leading Region: North America leads the Mobile Virtual Network Operator market with a 35% share in 2025, supported by strong U.S. regulatory frameworks and advanced 5G-driven innovation.

- Fastest Growing Region: Asia Pacific, holding 30% share in 2025, is the fastest-growing region driven by expanding subscriber bases and digital adoption across India and China.

- Leading Operational Model: Full MVNO dominates with a 45% share in 2025, benefiting from greater control over the core network, billing autonomy, and enterprise scalability.

- Leading Subscriber Segment: The consumer segment accounts for 60% share in 2025, fueled by rising demand for affordable prepaid and flexible data plans.

- Key Market Opportunity: Enterprise IoT and M2M connectivity present high-margin growth opportunities as businesses adopt scalable, specialized MVNO solutions.

| Key Insights | Details |

|---|---|

|

Mobile Virtual Network Operator Size (2026E) |

US$ 100.0 billion |

|

Market Value Forecast (2033F) |

US$ 169.2 billion |

|

Projected Growth CAGR (2026-2033) |

7.8% |

|

Historical Market Growth (2020-2025) |

4.5% |

Market Dynamics

Drivers - Rising Demand for Affordable and Flexible Mobile Service Plans Driving Mass Consumer Adoption

The rising demand for affordable and contract-free mobile services is a major driver of MVNO market growth worldwide. Budget-conscious consumers increasingly prefer prepaid and low-tariff plans over traditional carrier contracts. Global mobile subscriptions reached 8.6 billion in 2023, with prepaid accounting for more than 70% in developing regions, highlighting strong demand for cost-efficient alternatives.

MVNOs leverage wholesale network agreements with major MNOs to offer services 20–40% cheaper than conventional operators. Their lean operating models, digital-first distribution, and targeted offerings enable competitive pricing. In markets such as the United States, subsidy programs supporting low-income connectivity have further accelerated MVNO adoption, strengthening penetration in highly price-sensitive and underserved customer segments.

Expansion of 5G Networks and Rapid Growth of IoT Ecosystems Supporting Enterprise-Focused Opportunities

The global rollout of 5G infrastructure is creating new growth avenues for MVNOs, particularly in enterprise and machine-to-machine connectivity. With forecasts indicating 5 billion 5G connections by 2030, MVNOs can deliver high-speed, low-latency services without investing in spectrum ownership, positioning them competitively in data-intensive and mission-critical applications.

Simultaneously, IoT expansion is reinforcing demand for specialized connectivity solutions. Global IoT connections reached approximately 15 billion in 2024, with MVNOs capturing a notable share through scalable wholesale models. Partnerships with host network operators enhance reliability for applications such as smart metering, connected vehicles, logistics tracking, and industrial automation, strengthening MVNO relevance in enterprise markets.

Restraints - Heavy Dependence on Host Mobile Network Operators Limiting Operational Control and Profit Margins

MVNOs rely entirely on host Mobile Network Operators (MNOs) for network access, exposing them to service disruptions, pricing changes, and capacity limitations. In 2023, around 20% of telecom network disruptions were linked to core network issues, which disproportionately impacted MVNOs lacking independent infrastructure or redundancy mechanisms to maintain uninterrupted service delivery.

Wholesale agreements also place MVNOs in a vulnerable negotiating position, especially as 5G deployment increases network capacity pressures. Rising wholesale access costs and limited bargaining power compress profit margins, with studies indicating margin reductions of 10–15% in highly competitive markets. This structural dependence limits operational flexibility and long-term profitability for smaller MVNOs.

Intense Price Competition and Market Saturation Reduce Differentiation and Increase Customer Churn

Aggressive pricing strategies among MVNOs have intensified competition, often driving service rates 30–50% lower than incumbent operators. While this attracts cost-sensitive consumers, it commoditizes mobile services and limits opportunities for value differentiation. Low entry barriers further encourage new players, leading to overcrowded markets and heightened competitive pressure.

Market saturation has contributed to elevated customer churn rates, estimated at around 15% in mature regions. In countries such as the United Kingdom, ongoing consolidation reflects the difficulty smaller or newer MVNOs face in sustaining profitability. Continuous price wars erode margins and weaken long-term viability, particularly for operators lacking strong brand positioning or niche specialization.

Opportunity - Expanding Enterprise M2M and IoT Connectivity Creating High-Margin Growth Avenues for MVNOs

The rapid expansion of enterprise machine-to-machine (M2M) and IoT connectivity presents a significant growth opportunity for MVNOs. Global IoT devices are projected to reach 25 billion by 2030, creating a rising demand for scalable cellular connectivity solutions across logistics, utilities, automotive, and industrial sectors. Specialized enterprise-focused MVNO offerings often generate margins up to twice that of traditional consumer plans.

Government-backed digital initiatives, including targets for widespread 5G coverage across developed regions, are accelerating wholesale partnerships between MNOs and MVNOs. Strategic collaborations, such as connectivity alliances between Verizon and KORE, have demonstrated scalability, surpassing 1 million enterprise connections in 2024. These partnerships position MVNOs as agile providers of customized, high-value IoT connectivity services.

Rising Migrant Population and Cross-Border Roaming Demand Strengthening International MVNO Prospects

The growing global migrant population, estimated at 281 million in 2023, is fueling demand for affordable international calling and roaming services. MVNOs specializing in multi-country prepaid and eSIM-based plans are well-positioned to serve expatriates, students, and frequent travelers seeking cost-efficient cross-border connectivity solutions.

Regulatory reforms and regional deregulation measures have gradually reduced roaming barriers, improving affordability and stimulating adoption. The rollout of 5G further enhances seamless network switching and service quality across borders. With rising cross-border mobility and digital dependence, roaming-focused MVNO models are projected to deliver sustained revenue growth through the end of the decade.

Category-wise Analysis

Operational Model Insights

Full MVNOs dominate the operational model segment, accounting for 45% share in 2025 due to greater control over billing systems, SIM management, and service customization. Their ownership of core network elements enables better margin control and enterprise-grade scalability. Strong adoption in IoT onboarding and corporate mobility solutions further strengthens their leadership across mature telecom markets.

The fastest-growing model is the hybrid and light MVNO structure, driven by lower capital requirements and faster market entry. These models appeal to digital-first brands and niche service providers seeking rapid scalability without heavy infrastructure investment. Increasing partnerships with host operators and flexible wholesale agreements are accelerating expansion across emerging and competitive telecom environments.

Subscriber Insights

The consumer segment leads the subscriber category with a 60% share in 2025, supported by rising demand for affordable prepaid plans and flexible data bundles. High smartphone penetration in advanced economies and expanding digital usage in developing regions continue to drive retail MVNO adoption, particularly among cost-sensitive and younger user demographics.

The enterprise subscriber segment is witnessing the fastest growth, fueled by rising demand for customized connectivity, corporate mobility management, and IoT integration. Businesses increasingly adopt MVNO solutions to optimize costs and deliver scalable data services. Growth in remote work, fleet management, and digital transformation initiatives is further strengthening enterprise-focused subscriber expansion globally.

Service Insights

Prepaid services lead the segment with a 55% share in 2025, particularly strong in emerging and price-sensitive markets. The dominance of prepaid plans is supported by flexible top-up options, no long-term commitments, and widespread digital recharge ecosystems. Large developing economies continue to rely heavily on prepaid structures for mass-market mobile accessibility.

Postpaid and bundled digital service offerings are the fastest-growing service categories, driven by increasing data consumption and demand for value-added features. Integrated entertainment, cloud storage, and roaming packages are gaining traction. As 5G adoption expands, premium data-centric plans and subscription-based enterprise solutions are accelerating growth in advanced telecom markets.

Application Insights

Cellular M2M applications hold the leading position with a 35% share in 2025, supported by approximately 15 billion connected IoT devices globally. Adoption across automotive, utilities, logistics, and smart infrastructure sectors drives dominance. Standardized connectivity frameworks and cost-efficient wholesale models enable MVNOs to provide scalable solutions across industrial ecosystems.

Consumer mobile broadband applications represent the fastest-growing category, driven by surging video streaming, gaming, and social media usage. Increasing smartphone upgrades and 5G-enabled devices are enhancing data traffic volumes. As digital lifestyles expand globally, high-speed connectivity for entertainment and remote communication continues to accelerate demand in consumer-focused segments.

Regional Insights

North America Mobile Virtual Network Operator Market Trends

North America leads the global MVNO market with a 35% share in 2025, driven primarily by the maturity of the United States telecom sector. Strong wholesale partnerships with major network operators and supportive regulatory oversight have expanded MVNO participation. Subscriber volumes remain robust, supported by widespread 5G deployment and high smartphone penetration across consumer and enterprise segments.

Regulatory frameworks promoting fair network access and competition continue to encourage market expansion in both the U.S. and Canada. MVNOs increasingly bundle IoT, enterprise mobility, and value-added digital services to differentiate offerings. Advanced 5G infrastructure and innovation-friendly policies position the region as a stable and revenue-generating hub for both consumer-focused and enterprise-driven MVNO models.

Europe Mobile Virtual Network Operator Market Trends

Europe represents a mature and steadily expanding MVNO landscape, projected to grow at a CAGR of 6.8% through the forecast period. Regulatory harmonization across EU member states and reductions in roaming charges have strengthened cross-border competitiveness. Countries such as Germany, the United Kingdom, France, and Spain remain key markets due to supportive telecom access policies.

Pro-competition measures and structured spectrum auctions have enabled the expansion of Full MVNO models across major European economies. Strong wholesale access frameworks encourage new entrants while fostering innovation in prepaid, digital-first, and enterprise mobility services. Consolidation trends are shaping competitive dynamics, yet regulatory backing continues to sustain balanced market development.

Asia Pacific Mobile Virtual Network Operator Market Trends

Asia Pacific holds approximately 30% share of the global MVNO market in 2025 and remains one of the fastest-expanding regions. Large subscriber bases in China and India, combined with rising smartphone adoption and digital service penetration, underpin regional growth. Expanding 4G and 5G infrastructure supports broader MVNO participation across both consumer and enterprise segments.

Government initiatives encouraging telecom competition and simplified wholesale access agreements are strengthening MVNO ecosystems across Japan and Southeast Asia. Rapid digitalization, expanding middle-class populations, and growing IoT adoption create scalable opportunities. The region’s strong device manufacturing ecosystem further supports affordable handset availability, enhancing MVNO accessibility in emerging markets.

Competitive Landscape

The global Mobile Virtual Network Operator market remains highly fragmented, characterized by intense competition and a diverse mix of regional and niche-focused players. Leading operators strengthen their positions through strategic alliances with host mobile network providers, enabling expanded coverage and improved service quality. Continuous investment in eSIM capabilities, digital platforms, and 5G-enabled solutions enhances operational agility and customer experience.

Competitive differentiation increasingly centers on targeted applications, flexible pricing strategies, and value-added digital bundles. Operators are integrating OTT content, financial services, and IoT solutions to boost customer retention. Ongoing consolidation and partnership activity reflect efforts to achieve scale efficiencies and sustain long-term profitability.

Key Market Developments

- In March 2025, Tracfone Wireless expanded its nationwide 5G prepaid services through a wholesale partnership with Verizon, focusing on improving connectivity access across rural and underserved U.S. regions while strengthening its competitive positioning in affordable high-speed data offerings.

- In July 2024, Lebara Group introduced eSIM-based roaming services across Europe in collaboration with Vodafone, specifically targeting migrant populations with seamless multi-country connectivity and cost-effective international communication solutions.

- In November 2024, KORE Wireless acquired Twilio IoT to enhance its global machine-to-machine capabilities, expanding enterprise IoT connectivity solutions and strengthening its position in scalable, cross-border M2M service deployment.

Companies Covered in Mobile Virtual Network Operator Market

- Lyca Mobile

- Lebara Mobile

- Giffgaff

- TracFone Wireless

- Consumer Cellular

- Virgin Mobile

- Tesco Mobile

- Talkmobile

- PosteMobile

- Truphone

- DataXoom

- Boost Mobile

- KDDI Mobile

- Citic Telecom

- Exetel

Frequently Asked Questions

The global Mobile Virtual Network Operator market is projected to reach US$ 100.0 billion in 2026.

Demand is driven by affordable prepaid services holding 55% share (2025), consumer dominance at 60% share, and expanding 5G and IoT connectivity adoption.

North America leads with a 35% share in 2025, supported by advanced telecom infrastructure and strong regulatory frameworks.

Cellular M2M, accounting for 35% share in 2025, presents a key opportunity through expanding enterprise IoT and scalable connectivity solutions.

Key leading players are Lyca Mobile, Lebara Mobile, Giffgaff, TracFone Wireless, and Consumer Cellular.