- Pharmaceuticals

- Medical Marijuana Market

Medical Marijuana Market Size, Share, and Growth Forecast, 2026 - 2033

Medical Marijuana Market by Product Type (Flowers, Edibles, Concentrates, Others), Application (Chronic Pain, Cancer, Mental Disorders, Others), End-user (Research & Development, Pharmaceutical), and Regional Analysis for 2026 - 2033

Medical Marijuana Market Size and Trends Analysis

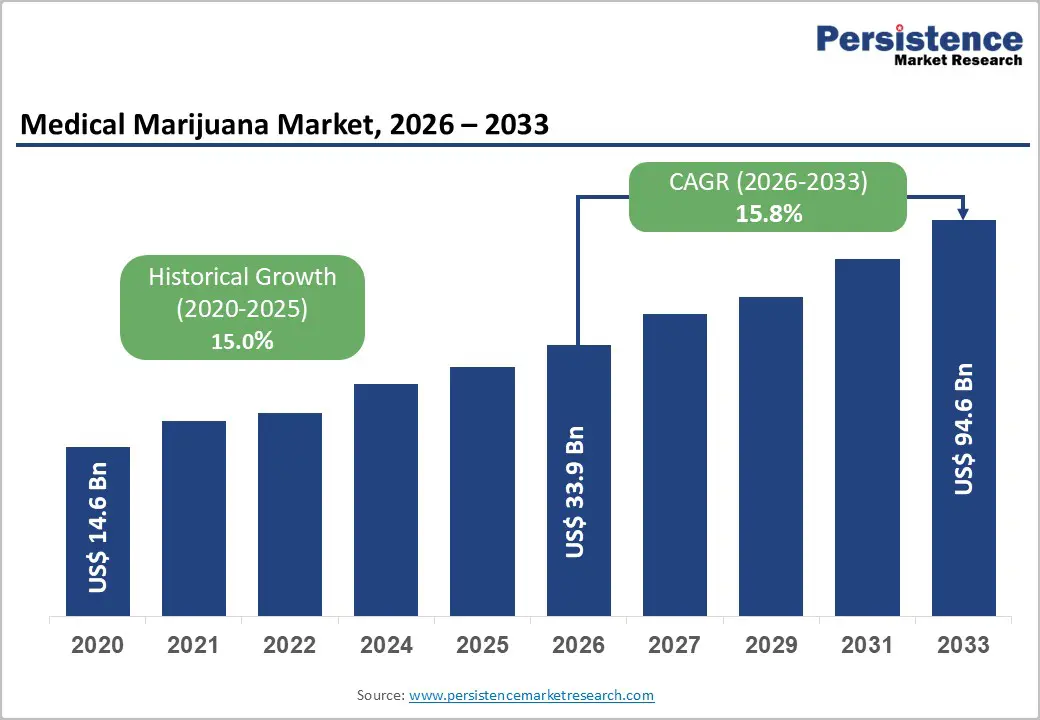

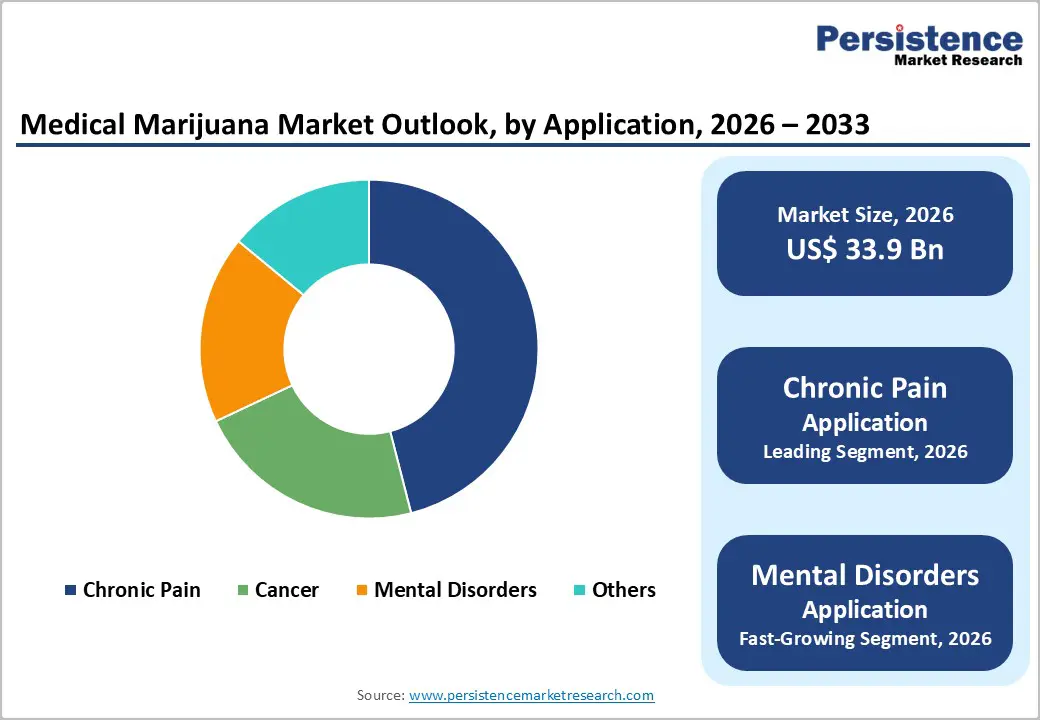

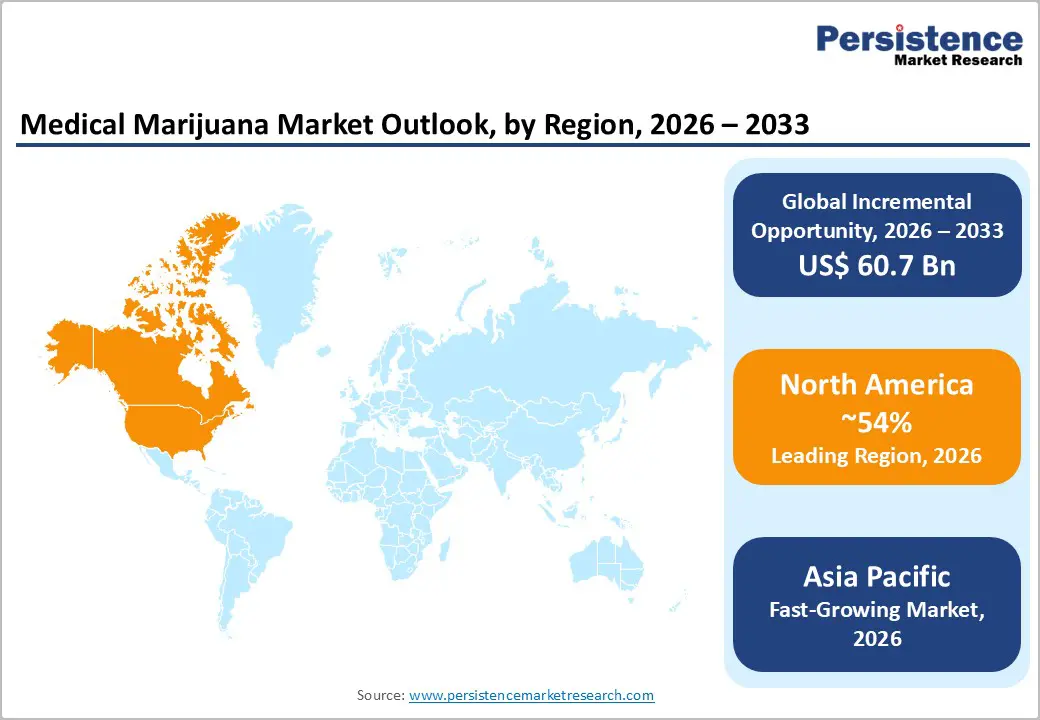

The global medical marijuana market size is likely to be valued at US$33.9 billion in 2026, and is expected to reach US$94.6 billion by 2033, growing at a CAGR of 15.8% during the forecast period from 2026 to 2033, driven by the increasing legalization of cannabis for medical use across multiple countries and rising acceptance among healthcare professionals for pain management, neurological disorders, cancer-related symptoms, and chronic diseases. Growing research on cannabinoid-based therapeutics and expanding patient awareness regarding alternative treatment options are accelerating market demand.

Key Industry Highlights:

- Dominant Region: North America is projected to dominate the medical marijuana market with around 54% revenue share in 2026, driven by widespread legalization in the U.S. and Canada, rising physician acceptance, and the growing demand for cannabinoid-based therapies.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing medical marijuana market, driven by gradual legalization in countries like Thailand and Australia, along with rising research, healthcare investment, patient awareness, and government support for cannabinoid-based therapies and cultivation.

- Leading Product Type: Cannabis flowers are expected to dominate the market with 42% revenue share in 2026, driven by their widespread use and preference for vaporization as a primary medical delivery method.

- Dominant Application: Chronic pain is expected to dominate with 46% share in 2026 due to its widespread use across neuropathic, musculoskeletal, cancer-related, and inflammatory pain conditions.

DRO Analysis

Driver - Accelerating Global Regulatory Reform and Legalization Momentum

The biggest factor driving growth in the global medical marijuana market is the rapid shift in government regulations that are legalizing and supporting medical cannabis use across major countries. These regulatory changes are helping transform the industry from an informal and fragmented market into a more structured healthcare sector with standardized products, regulated distribution systems, and wider patient access.

In the U.S., which is the world’s largest medical marijuana market, the Drug Enforcement Administration (DEA) proposed in May 2024 to reclassify cannabis from Schedule I to Schedule III under the Controlled Substances Act, following recommendations from the Department of Health and Human Services (HHS). This is considered the most important federal cannabis policy change in more than 50 years. If approved, Schedule III status would reduce major legal barriers to cannabis research, make banking access easier for cannabis companies, and provide potential tax benefits by removing restrictions under IRS Section 280E. These changes would significantly improve the business environment and growth opportunities for medical marijuana companies.

Restraint- Product Standardization Challenges and Quality Variability

The natural complexity of cannabis creates major challenges for producing standardized medical products. Cannabis contains hundreds of cannabinoids, terpenes, and flavonoids that can interact in different ways, often referred to as the “entourage effect.” Owing to this, it is difficult to create medical cannabis products with consistent quality and effects. Unlike traditional pharmaceutical drugs that have fixed chemical structures and predictable performance, cannabis plants can vary from batch to batch in potency, cannabinoid content, terpene profile, and contamination levels. This makes quality control and pharmaceutical-grade standardization more difficult.

Another key challenge limiting market growth is the hesitation among physicians to recommend medical cannabis. A study published in the Journal of General Internal Medicine in 2020 found that only around 30-40% of primary care physicians in U.S. states with medical marijuana programs felt confident enough to advise patients on cannabis use. Many doctors reported limited education on cannabis pharmacology during medical training, lack of strong clinical trial evidence comparable to traditional medicines, and concerns about legal or professional liability related to cannabis-related side effects.

Opportunity - Pharmaceutical-Grade Cannabinoid Drug Development and FDA Approval Pipeline

The largest long-term opportunity in the medical cannabis market is the development of pharmaceutical-grade cannabinoid medicines that receive formal regulatory approval and can be covered through mainstream healthcare reimbursement systems. Unlike plant-based medical cannabis products, these standardized medicines can achieve wider acceptance among doctors, insurers, and healthcare providers. The success of GW Pharmaceuticals’ Epidiolex/Epidyolex has already proven this business model.

As a cannabis-derived medicine approved by both the FDA and EMA, it benefits from insurance coverage, physician prescriptions, and access to patients even in regions where traditional medical cannabis laws are restrictive. This gives pharmaceutical cannabinoid products higher revenue potential, broader market reach, and stronger competitive protection compared to botanical cannabis products.

The pipeline for cannabinoid-based pharmaceuticals is also expanding rapidly. Zynerba Pharmaceuticals is developing ZYN002, a synthetic CBD transdermal gel currently in Phase 3 clinical trials for Fragile X syndrome and certain epilepsy-related disorders. In 2021, Jazz Pharmaceuticals strengthened its position in the sector by acquiring GW Pharmaceuticals for US$7.2 billion, highlighting strong industry confidence in cannabinoid-based therapies.

At the same time, several biotechnology companies are researching synthetic cannabinoid receptor modulators designed to deliver the medical benefits of cannabis while avoiding the production and consistency challenges associated with plant-based cannabis sources.

Category-wise Analysis

Product Type Insights

Cannabis flowers are expected to remain the leading product segment, accounting for around 42% of total market revenue in 2026. Their strong market position is mainly due to their long-standing familiarity among medical cannabis patients and healthcare providers. Flowers are commonly used through vaporization, which is considered a safer and more clinically preferred method than smoking because it allows faster symptom relief and better dosage control. For example, Tilray Brands supplies medical cannabis flower products designed for vaporization-based therapy, particularly for managing conditions such as chronic pain.

Meanwhile, concentrates are expected to be the fastest-growing product category. This segment includes cannabis oils, tinctures, full-spectrum extracts, distillates, waxes, and resin products. Concentrates are gaining popularity because they provide more accurate dosing, smokeless consumption, longer shelf life, standardized cannabinoid content, and higher potency in smaller quantities. Aurora Cannabis is one of the companies producing medical cannabis concentrates, including THC oil drops and distillates made using CO2 extraction technology. These products are designed to deliver precise and consistent dosing for patients with chronic pain and neurological conditions.

Application Insights

Chronic pain is expected to remain the leading application segment, accounting for around 46% of total revenue in 2026. Conditions such as neuropathic pain, musculoskeletal pain, cancer-related pain, fibromyalgia, and inflammatory pain disorders are among the most commonly approved indications for medical cannabis across global markets. As a result, chronic pain represents the largest patient population in terms of both treatment demand and revenue generation. Tilray Brands supplies medical cannabis products for chronic pain management, including standardized flower and oil-based formulations prescribed in markets across Canada and Europe.

Mental health disorders are projected to be the fastest-growing application segment during the forecast period. Rising global cases of PTSD, anxiety, and depression, along with increasing clinical research supporting cannabinoid-based therapies for psychiatric conditions, are driving this growth. Jazz Pharmaceuticals markets Epidiolex, a cannabidiol-based therapy initially approved for epilepsy treatment, which is also being explored for wider neurological and mental health-related applications.

End-user Insights

The pharmaceutical segment is projected to lead the market, representing approximately 58% of total market value in 2026. This segment includes pharmaceutical companies engaged in the development and commercialization of standardized cannabinoid-based medicines, along with pharmaceutical distribution networks that supply physician-prescribed medical cannabis products to patients. Jazz Pharmaceuticals is a key participant in this segment through its commercialization of Epidiolex, an FDA-approved prescription cannabinoid therapy indicated for epilepsy treatment.

The research and development segment is expected to register the fastest growth during the forecast period. The U.S. Drug Enforcement Administration’s expansion of registered cannabis research manufacturers has significantly improved the availability of research-grade cannabis for clinical investigators, enabling a broader pipeline of Phase 1-3 clinical trials that were previously constrained by limited supply access. Tilray Brands is actively contributing to this growth through its dedicated medical cannabis R&D operations, which focus on clinical research involving standardized cannabinoid formulations and support investigator-led studies targeting pain management, neurological disorders, and oncology applications.

Regional Insights

North America Medical Marijuana Market Trends

North America regional market is projected to dominate capturing around 54% of total revenues in 2026, propelled by widespread legalization of medical cannabis across the U.S. and Canada, increasing physician acceptance, and rising demand for cannabinoid-based therapies for chronic pain, cancer, epilepsy, and neurological disorders. The region is also witnessing strong investment in pharmaceutical-grade cannabis products, dispensary expansion, and ongoing clinical research supporting medical marijuana applications.

U.S. Medical Marijuana Market Insights

The U.S. medical marijuana market is characterized by a fragmented state-level regulatory framework, with 40 states operating active medical cannabis programs that differ in qualifying medical conditions, dispensary licensing systems, possession restrictions, and permitted product categories. The anticipated federal rescheduling of cannabis is expected to trigger one of the most transformative shifts in the history of the U.S. cannabis industry by potentially paving the way for interstate commerce, expanded access to banking and financial services, and pharmaceutical reimbursement opportunities, collectively creating the potential for hundreds of billions of dollars in additional market growth.

Canada Medical Marijuana Market Insights

Canada remains one of the world’s most mature markets, supported by a federally legal framework under the Cannabis Act (2018). Major producers, including Tilray Brands, Aurora Cannabis, Canopy Growth, and Cronos Group, supply standardized medical cannabis products through regulated distribution channels.

Europe Medical Marijuana Market Trends

Europe market is growing due to expanding legalization of medical cannabis programs across countries such as Germany, U.K., and Italy, along with increasing adoption of cannabinoid-based treatments for chronic pain, epilepsy, and multiple sclerosis. Rising government support for clinical research, pharmaceutical-grade cannabis production, and improved patient access through regulated healthcare systems are further driving market growth.

Germany Medical Marijuana Market Trends

Germany represents Europe’s largest and most transformative medical cannabis market. The country’s 2017 Cannabis-as-Medicine legislation created the regulatory framework that enabled more than 300,000 patients to obtain medical cannabis through prescription-based pharmacy dispensing by 2023. Under the GKV statutory health insurance system, reimbursement for medical cannabis prescriptions is required for patients with serious medical conditions when conventional treatment options have proven ineffective.

U.K. Medical Marijuana Market Trends

The U.K. medical cannabis framework, established by the Home Secretary’s November 2018 rescheduling of cannabis-based products for medicinal use (CBPMs) to Schedule 2, allows specialist physicians to prescribe medical cannabis for conditions where clinical need is demonstrated and licensed alternatives have failed.

Asia Pacific Medical Marijuana Market Trends

Asia Pacific is likely to be the fastest-growing regional market emerging rapidly due to gradual legalization of medical cannabis in countries such as Thailand and Australia, along with increasing research on cannabinoid-based therapies for chronic pain, epilepsy, and cancer care. Rising healthcare investments, growing patient awareness, and government support for controlled cannabis cultivation and pharmaceutical development are further supporting regional market growth.

Australia Medical Marijuana Market Trends

Australia is the region’s largest commercial and fastest-growing medical cannabis market, experiencing one of the world’s most rapid rates of medical cannabis adoption. The country’s market growth has been accelerated by the Therapeutic Goods Administration through the progressive streamlining of the Special Access Scheme (SAS) and Authorized Prescriber (AP) pathways. Expanding domestic cannabis cultivation, rising investment in pharmaceutical-grade cannabinoid products, and increasing physician acceptance are also contributing significantly to market expansion.

Thailand Medical Marijuana Market Trends

Thailand became the first Southeast Asian nation to decriminalize cannabis by removing it from the narcotics list in June 2022, resulting in a period of regulatory uncertainty that authorities are gradually addressing through the development of structured pharmaceutical cannabis regulations. The country’s Government Pharmaceutical Organization has introduced cannabis-derived therapies, including cannabis extract oils and combined THC:CBD formulations, for distribution through public healthcare hospitals. Thailand’s ambition to establish itself as a leading medical cannabis hub in Southeast Asia is further supported by its well-developed medical tourism sector and healthcare infrastructure.

Competitive Landscape

The global medical marijuana market demonstrates a dual-layered competitive structure, reflecting its position at the intersection of agricultural commodity production and the regulated pharmaceutical industry. On one side, the market includes botanical medical cannabis producers focused on cultivation and distribution, while on the other, it encompasses pharmaceutical companies developing standardized cannabinoid-based therapies. At the pharmaceutical forefront, GW Pharmaceuticals holds a leading position through products such as Epidiolex and Sativex, which remain among the few globally approved and widely reimbursable cannabis-derived pharmaceutical products.

Companies featured in this market landscape, including Cara Therapeutics, Growblox Sciences, CannaGrow Holdings, Cannabis Sativa Inc., United Cannabis Corporation, GreenGro Technologies, and Lexaria Bioscience, represent the innovation-driven and specialty-focused segments of the competitive ecosystem. In particular, Lexaria Bioscience’s proprietary DehydraTECH™ platform is designed to address a longstanding challenge in oral cannabinoid pharmacology by improving bioavailability and reducing variability associated with extensive first-pass liver metabolism.

Key Industry Developments:

- In April 2026, The U.S. Department of Justice reclassified FDA-approved marijuana products and state-licensed medical cannabis from Schedule I to Schedule III under the Controlled Substances Act. It stated that the move aimed to support medical research, improve patient access to regulated treatments, and better align federal policy with state-level medical cannabis programs while maintaining regulatory oversight.

- In April 2025, Aurora Cannabis Inc., the Canadian-based leading global medical cannabis company, announced the completion of a multi-year investment of USD 3 million in improvements to its manufacturing facility in Pemberton, British Columbia. These upgrades are a combination of Aurora's proprietary high-performing genetics and state-of-the-art engineering design, which have resulted in optimal cultivation conditions, expanded output, and superior product quality.

Companies Covered in Medical Marijuana Market

- Cara Therapeutics Inc.

- Growblox Sciences Inc.

- CannaGrow Holdings Inc.

- International Consolidated Companies Inc.

- Cannabis Sativa Inc.

- United Cannabis Corporation

- GreenGro Technologies Inc.

- GW Pharmaceuticals plc

- Lexaria Corp.

Frequently Asked Questions

The global medical marijuana market is projected to reach US$33.9 billion in 2026.

The primary drivers are the global wave of medical cannabis legalization and regulatory reform including U.S. DEA rescheduling to Schedule III, Germany’s 2024 Cannabis Act, and Australia’s TGA pathway expansion and the growing clinical evidence base supporting cannabinoid efficacy in chronic pain, epilepsy, cancer palliative care, and mental disorders.

The medical marijuana market is poised to witness a CAGR of 15.8% from 2026 to 2033.

Key opportunities in the Medical Marijuana Market include the development of pharmaceutical-grade cannabinoid drugs with FDA/EMA approvals and insurance reimbursement, expansion into emerging markets such as Brazil, Colombia, Thailand, and India, and rising use of medical cannabis for mental health conditions like PTSD and anxiety.

Key players include GW Pharmaceuticals (AbbVie/Jazz), Cara Therapeutics, Growblox Sciences, Cannabis Sativa Inc., United Cannabis Corporation, GreenGro Technologies, Lexaria Bioscience Corp., CannaGrow Holdings, and International Consolidated Companies.