- Medical Devices

- Medical Fiber Optics Market

Medical Fiber Optics Market Size, Share, and Growth Forecast, 2026 - 2033

Medical Fiber Optics Market by Product Type (Imaging Fiberscopes, Laser Fibers, Others), Fiber Type (Pure Silica Fiber, Polycrystalline Fiber, Others), Application (Endoscopy, Biomedical Sensing & Monitoring, Laser Surgery, Others), and Regional Analysis for 2026 - 2033

Medical Fiber Optics Market Share and Trends Analysis

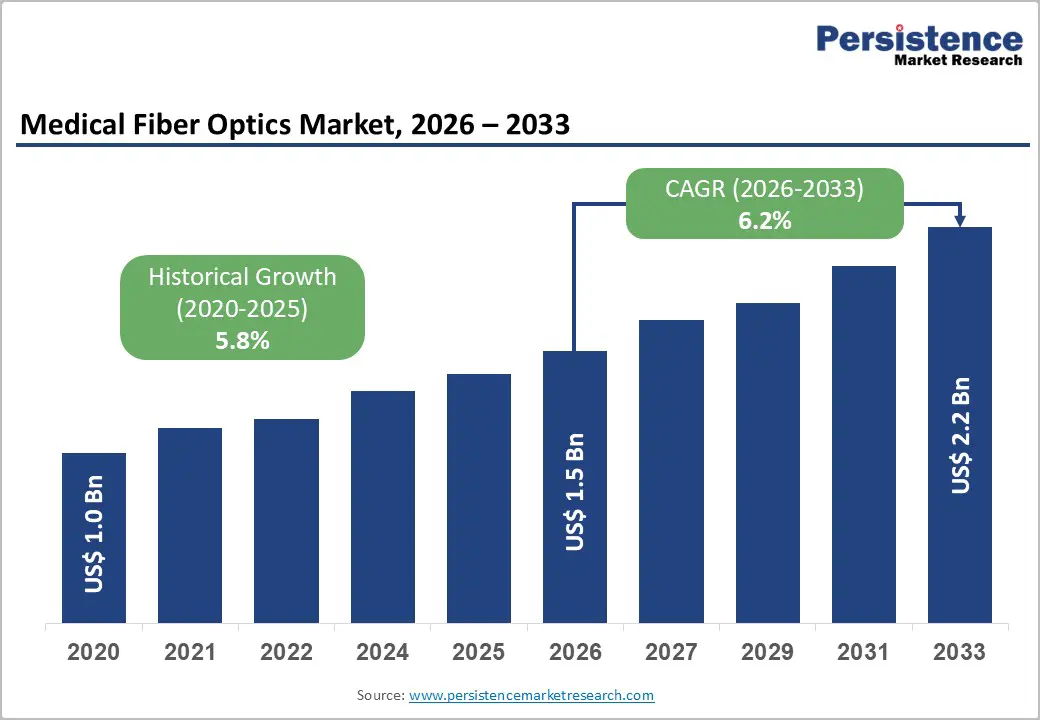

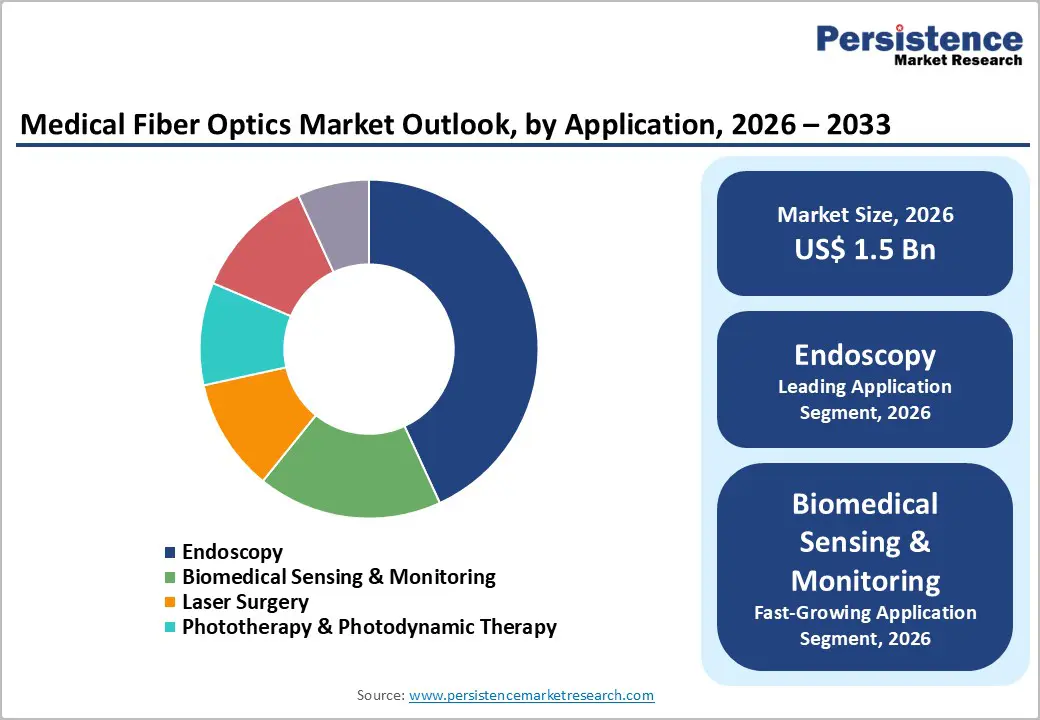

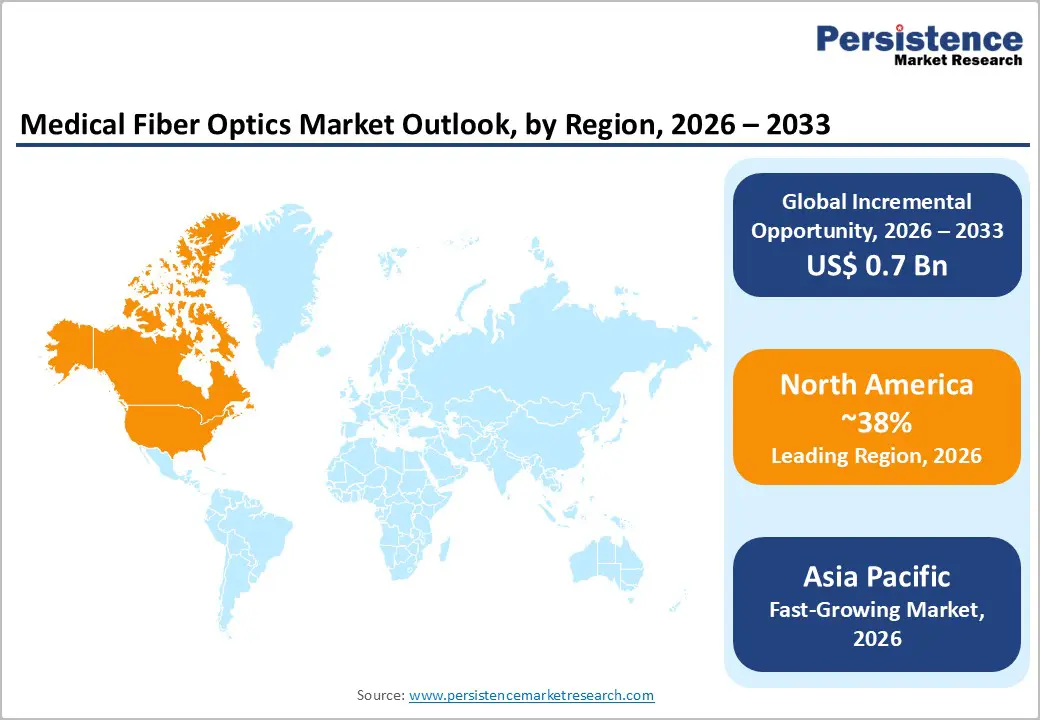

The global medical fiber optics market size is likely to be valued at US$1.5 billion in 2026 and is estimated to reach US$2.2 billion by 2033, growing at a CAGR of 6.2% during the forecast period from 2026 to 2033, driven by the rising prevalence of chronic diseases requiring minimally invasive diagnostic and therapeutic interventions.

An aging global population is generating sustained demand for endoscopic procedures, laser surgeries, and photodynamic therapies, each of which depends on precision-grade fiber-optic transmission systems. Regulatory approvals from bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) for fiber-guided surgical instruments are accelerating adoption across tertiary care facilities.

Key Industry Highlights:

- Leading Product Type: Imaging fiberscopes are set to hold around 38% market share in 2026, driven by primary clinical demand for high-resolution internal visualization.

- Fastest-Growing Product Type: Fiber-optic sensors are projected as the fastest-growing segment, supported by the growing adoption of real-time physiological monitoring systems.

- Leading Application: Endoscopy is estimated to hold roughly 44% market share in 2026, due to the global standardization of minimally invasive diagnostic workflows.

- Fastest-Growing Application: The biomedical sensing & monitoring segment is forecast to record the fastest growth, driven by the widespread transition toward smart, interconnected healthcare infrastructure.

- Regional Leadership: North America is projected to capture roughly 38% of the market share by 2026, while Asia Pacific is forecast to record the fastest growth due to rapid healthcare infrastructure expansion.

- Competitive Environment: The market reflects a moderately fragmented structure, with key players such as SCHOTT AG and Coherent, Inc. leveraging specialized material innovation and deep original equipment manufacturer integration to maintain market positioning.

DRO Analysis

Driver - Advancements in Diagnostic Imaging and Laser-Assisted Therapies

Continuous innovation in high-power laser delivery systems and high-resolution diagnostic modalities accelerates market growth. Modern clinical settings require real-time, micro-scale visualization and precise energy delivery for complex interventions like lithotripsy, tumor ablation, and ophthalmic corrections. Standard copper or lower-grade structural elements fail to support the transmission bandwidth and energy density required by these modern systems. Consequently, advanced material fibers capable of managing high power thresholds without degradation become critical components in newly cleared therapeutic configurations.

The integration of advanced optical configurations optimizes energy transmission efficiency and reduces heat generation during long surgical procedures. Original equipment manufacturers increasingly adopt specialized silica and polymer configurations to comply with changing regulatory safety thresholds. As therapeutic lasers transition to shorter pulse widths and higher peak power levels, specialized fiber configurations become essential to prevent fiber damage. This dependency creates a steady replacement and installation cycle across public and private clinical institutions worldwide.

Restraint - High Manufacturing Complexity and Calibration Constraints

Production of medical-grade fiber optic components requires high-purity materials and precision alignment systems. Manufacturing complexity increases production time and limits scalability. Calibration requirements for medical applications increase operational costs and restrict entry for smaller manufacturers.

This structure reduces margin flexibility and increases dependency on specialized fabrication facilities. Supply chain constraints in optical-grade silica and polymer materials further restrict cost optimization and delay large-scale deployment across emerging healthcare facilities.

Opportunity - Integration of Fiber-Optic Sensors in Smart Medical Wearables

The development of specialized fiber-optic sensors provides a viable growth pathway in patient monitoring and personalized medicine. Conventional electronic sensors are susceptible to electromagnetic interference, making them unsuitable for use during magnetic resonance imaging procedures. Fiber-optic sensors operate via light modulation, ensuring complete immunity to electromagnetic disruptions while maintaining highly accurate readings for vital physiological parameters. This capability allows medical device manufacturers to integrate flexible fiber sensors into diagnostic catheters and wearable monitoring platforms.

The expansion of digital health infrastructure supports the integration of optical sensing networks within specialized care facilities. Continuous real-time tracking of parameters like intracranial pressure, intravascular blood pressure, and localized temperature shifts creates a need for durable, biocompatible sensor components. Original equipment manufacturers can capitalize on this trend by partnering with telehealth infrastructure developers to deliver pre-validated, sensor-enabled medical disposables. This strategy provides access to a stable revenue stream driven by the growth of remote diagnostic platforms.

Category-wise Analysis

Product Type Insights

Imaging fiberscopes are anticipated to secure around 38% of the medical fiber optics market share in 2026, reflecting the primary clinical demand for high-resolution internal visualization. Modern diagnostic protocols require clear visual data to accurately identify early-stage malignancies. Clinicians utilize flexible imaging bundles during complex bronchoscopy procedures to examine deep pulmonary structures without causing extensive tissue trauma.

Fiber-optic sensors are expected to be the fastest-growing segment, propelled by the growing adoption of real-time physiological monitoring systems. Healthcare providers increasingly require continuous, interference-free biological feedback during complex surgical procedures. Intravascular pressure monitoring assemblies utilize miniature optical sensor tips to track hemodynamic shifts inside cardiac cath labs.

Fiber Type Insights

Pure silica fibers are poised to dominate with a forecast market share of over 52% of the medical fiber optics market in 2026, powered by their exceptional optical transmission properties and high damage threshold. Surgical laser systems require core materials capable of transferring intense thermal energy without structural degradation. High-power holmium-YAG laser systems utilize pure silica cores to fragment urinary calculi safely during endourological interventions.

Polymer optical fiber is estimated to be the fastest-growing segment, fueled by rising demand for highly flexible, cost-effective, and break-resistant diagnostic components. Short-distance data transmission and single-use illumination systems benefit from the high mechanical flexibility of polymer formulations. Ophthalmic surgical illumination probes integrate polymer structures to navigate narrow ocular pathways without risking internal breakage.

Application Insights

Endoscopy is likely to be the leading segment with a projected 44% of the medical fiber optics market share in 2026, due to the global standardization of minimally invasive diagnostic workflows. Gastroenterology clinics rely on endoscopes to conduct routine colorectal cancer screenings. Visualizing mucosal linings via high-density fiber bundles allows for immediate polyp identification and biopsy collection during standard outpatient procedures.

Biomedical sensing & monitoring is anticipated to be the fastest-growing segment, fueled by the widespread transition toward smart, interconnected healthcare infrastructure. Real-time patient tracking requires continuous data collection without electromagnetic interference. Advanced neonatal incubators employ non-invasive optical fiber sensors to track infant respiration patterns safely without using electronic leads.

Regional Insights

North America Medical Fiber Optics Market Trends

North America is expected to lead with an estimated 38% of the medical fiber optics market share in 2026, supported by an advanced healthcare infrastructure and rapid adoption of minimally invasive clinical protocols. Well-funded research environments allow major medical technology companies, such as Integra LifeSciences and Coherent Inc., to continuously develop advanced optical components.

U.S. Medical Fiber Optics Market Insights

The U.S. market is projected to expand steadily due to high private and public healthcare expenditures aimed at optimizing outpatient surgical workflows. Surgical facilities are increasingly integrating advanced laser delivery fibers to reduce patient recovery times and increase daily procedure volume. This focus on operational efficiency leads to stable component sales for major device manufacturers.

Canada Medical Fiber Optics Market Insights

Canada is forecast to record sustained procurement increases driven by federal investments intended to upgrade regional diagnostic infrastructure. Public health networks are expanding their telemedicine and remote sensing frameworks, which increases the utilization of fiber-optic sensor arrays. This infrastructure expansion supports long-term market growth within provincial hospital networks.

Europe Medical Fiber Optics Market Trends

Europe is expected to maintain a significant market share, driven by a well-established medical device manufacturing sector and clear clinical safety guidelines. Strict compliance with the European Medical Device Regulation (MDR) encourages continuous improvements in component tracing and material purity. Renowned optical technology enterprises, such as SCHOTT AG and LEONI AG, focus on developing specialized fibers for diagnostic and therapeutic systems.

Germany Medical Fiber Optics Market Insights

Germany is likely to remain a key regional contributor due to its advanced engineering base and high concentration of specialized outpatient clinics. Local manufacturing facilities focus on developing high-precision illumination fibers for complex robotic surgery systems. This specialized production supports steady domestic consumption and export growth.

U.K. Medical Fiber Optics Market Insights

The U.K. market is expected to witness increased adoption of disposable fiber-optic components as National Health Service facilities seek to lower hospital-acquired infection rates. This shift toward single-use instruments alters procurement dynamics, favoring high-volume polymer fiber assemblies. The resulting change in buying patterns benefits suppliers of scalable, cost-efficient optical components.

Asia Pacific Medical Fiber Optics Market Trends

Asia Pacific is forecast to be the fastest-growing market for medical fiber optics, stimulated by rapid infrastructure development and growing medical tourism across emerging economies. Expanding public hospital networks in developing nations creates a substantial market for diagnostic and therapeutic endoscopes. Regional manufacturers are increasing production capacity to meet the growing domestic demand for accessible healthcare solutions.

China Medical Fiber Optics Market Insights

China is projected to experience rapid market expansion, driven by government initiatives focused on modernizing medical device manufacturing and widening healthcare access. Domestic component suppliers are advancing their production capabilities to deliver high-quality silica fibers for regional medical equipment integrators. This manufacturing growth reduces dependence on imported components.

India Medical Fiber Optics Market Insights

India is expected to register strong growth, supported by a rising volume of elective surgeries and expanding private healthcare networks. Corporate hospital chains are investing in advanced diagnostic and therapeutic systems to attract international patients seeking affordable, high-quality care. This trend drives the continuous procurement of advanced fiber-optic sub-assemblies.

Competitive Landscape

The global medical fiber optics market is moderately fragmented, with competition driven by technological capability, material precision, and integration into surgical systems. Entry barriers remain high due to manufacturing complexity and regulatory compliance requirements. Key companies include SCHOTT AG, Coherent, Inc., Integra LifeSciences Corporation, LEONI AG, Amphenol Corporation, and Fiberoptics Technology Incorporated.

Market structure reflects consolidation around established device manufacturers with strong distribution networks. Specialized optical component suppliers contribute to upstream supply chain stability and innovation cycles across diagnostic and surgical applications.

Key Industry Developments:

- In June 2025, Coherent, Inc. launched disposable surgical fiber assemblies designed for laser lithotripsy and minimally invasive procedures, improving high-power laser energy delivery and precision in urology and soft tissue surgical applications.

Companies Covered in Medical Fiber Optics Market

- SCHOTT AG

- Coherent, Inc.

- Integra LifeSciences Corporation

- LEONI AG

- Amphenol Corporation

- Fiberoptics Technology Incorporated

- AFL

- Timbercon, Inc.

- Gulf Fiberoptics

- Newport Corporation

- LEMO

- Hirose Electric Co., Ltd.

- Fischer Connectors

Frequently Asked Questions

The global medical fiber optics market is projected to reach US$1.5 billion in 2026.

Rising demand for minimally invasive surgeries, increasing adoption of fiber-based imaging and laser systems, and growing use of precision diagnostic and therapeutic technologies drive the medical fiber optics market.

The medical fiber optics market is poised to witness a CAGR of 6.2% from 2026 to 2033.

Expansion of robotic-assisted surgery, growth in wearable and implantable fiber optic sensing devices, and increasing adoption of advanced endoscopic and laser-based treatment systems create key market opportunities.

Some of the key market players include SCHOTT AG, Coherent, Inc., Integra LifeSciences Corporation, LEONI AG, Amphenol Corporation, and Fiberoptics Technology Incorporated.