- Inks, Coatings, Adhesives & Sealants (ICAS)

- Medical Device Coatings Market

Medical Device Coatings Market Size, Share, and Growth Forecast 2026 - 2033

Medical Device Coatings Market by Product (Hydrophilic Coatings, Antimicrobial Coatings, Drug-eluting Coatings, Anti-thrombogenic Coatings, Others), by Substrate (Metals (Stainless Steel, Titanium, Nickel, Others), Ceramics, Polymers (Silicone, Polyurethane, Polypropylene, Others)), Application, and Regional Analysis, 2026 - 2033

Medical Device Coatings Market Size and Trend Analysis

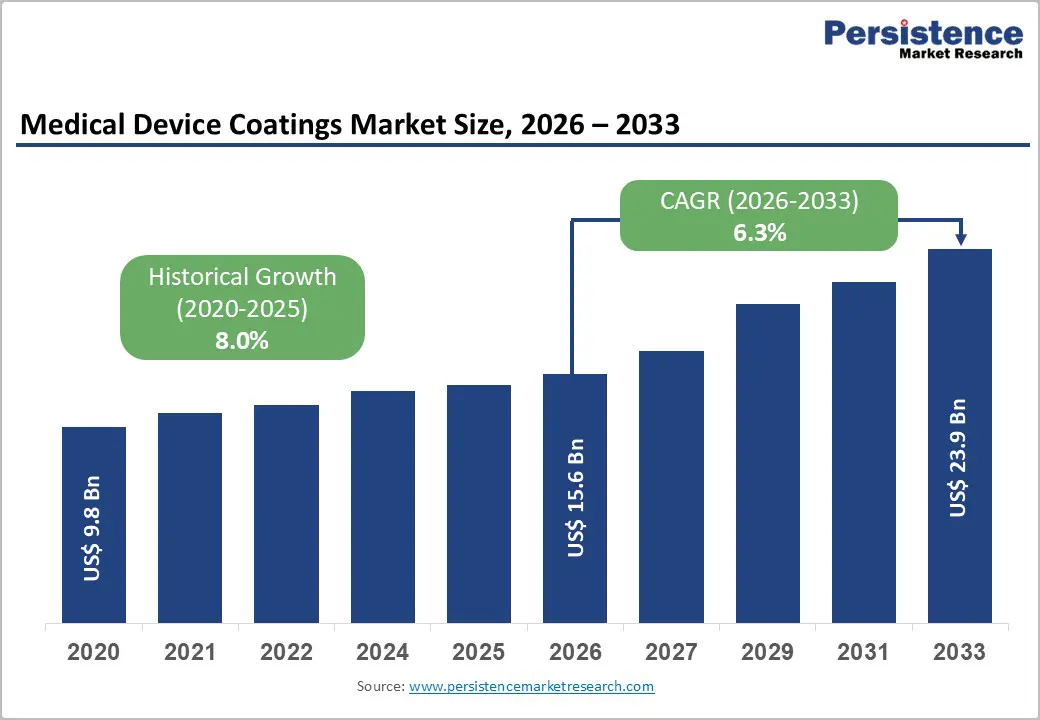

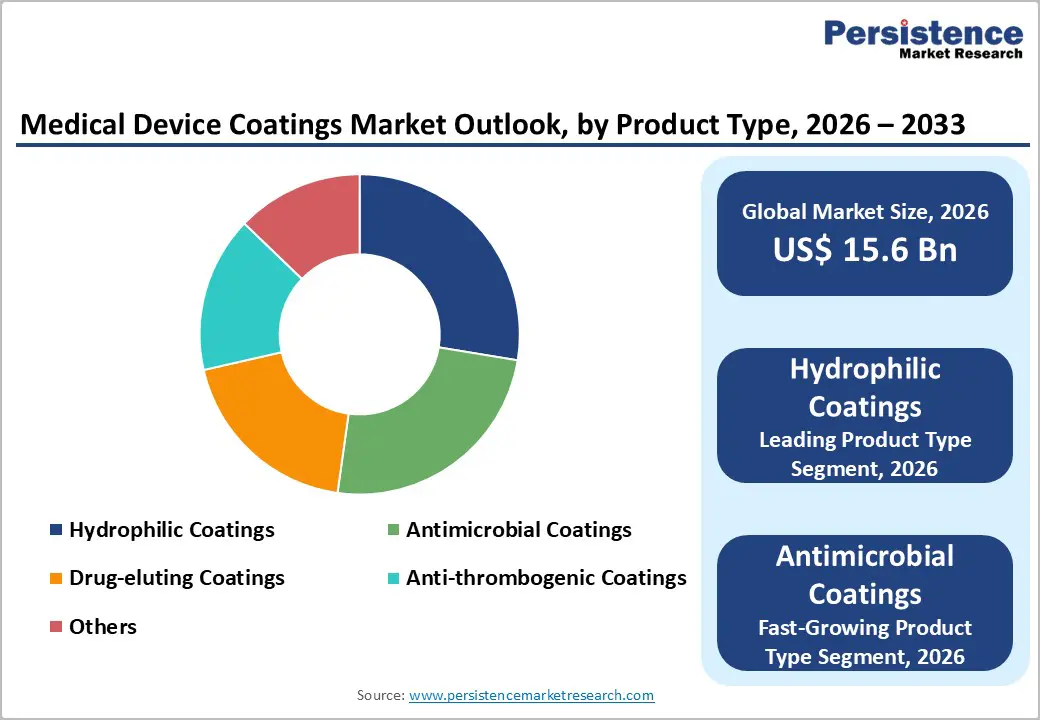

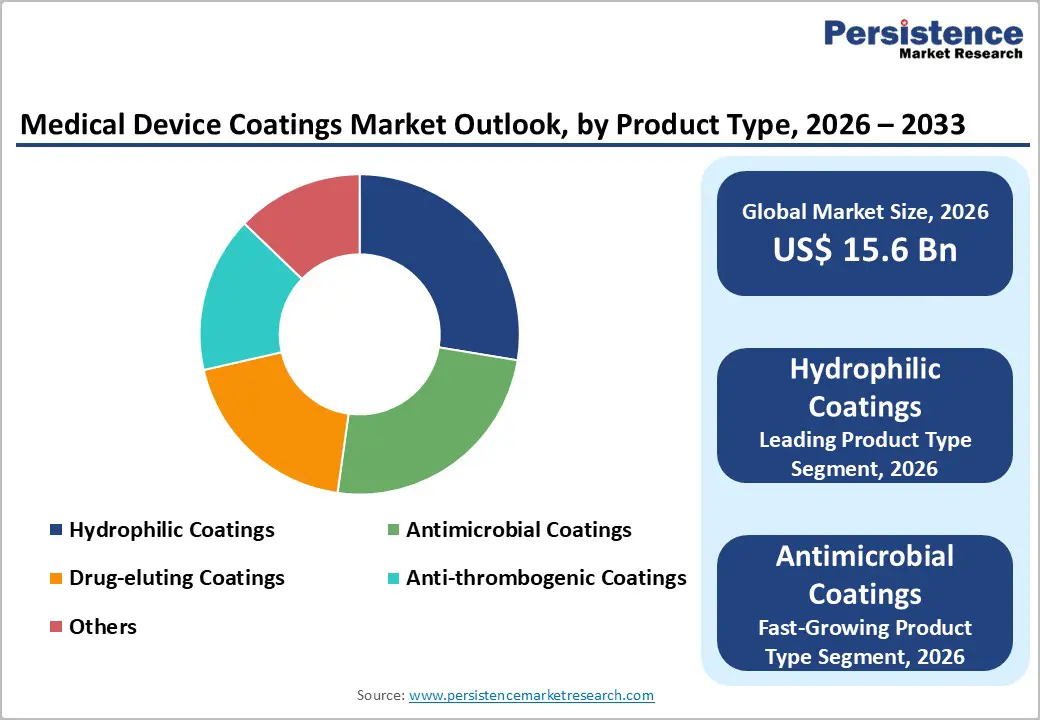

The global medical device coatings market size is expected to be valued at US$ 15.6 billion in 2026 and projected to reach US$ 23.9 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033. Growth is driven by rising demand for advanced medical devices, fueled by the increasing prevalence of minimally invasive surgeries and chronic diseases.

The aging population is creating a greater need for biocompatible coatings that improve device performance, safety, and patient outcomes. Innovations in nanotechnology and multifunctional coatings are enhancing durability and functionality, supporting sustained expansion across cardiovascular, orthopedic, dental, and other medical applications.

Key Industry Highlights:

- Leading Region: North America leads the Medical Device Coatings Market with a 38% share in 2025, supported by FDA innovations and high procedure volumes.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, projected at an 8.5% CAGR from 2025 to 2032, driven by manufacturing hubs in China and India.

- Leading Product Category: Hydrophilic coatings dominate the product segment with a 35% share in 2025, crucial for low-friction performance in cardiovascular devices.

- Fastest-Growing Application: Cardiovascular applications are expanding rapidly, driven by anti-thrombogenic and drug-eluting coatings amid rising heart disease prevalence.

- Key Opportunity: Nanotechnology innovations provide growth potential, enabling smart coatings that enhance device efficacy and performance in emerging markets.

| Key Insights | Details |

|---|---|

| Medical Device Coatings Size (2026E) | US$ 15.6 billion |

| Market Value Forecast (2033F) | US$ 23.9 billion |

| Projected Growth CAGR (2026 - 2033) | 6.3% |

| Historical Market Growth (2020 - 2025) | 8.0% |

Market Dynamics

Drivers - Rising Chronic Disease Burden Driving Demand for Advanced Coated Medical Devices

The growing prevalence of chronic diseases such as diabetes, cardiovascular disorders, and obesity is significantly increasing demand for coated medical devices. Patients increasingly require stents, catheters, and implants with hydrophilic or drug-eluting coatings to enhance drug delivery, improve biocompatibility, and reduce complications. Coatings that improve device performance are becoming critical for effective chronic disease management.

Regulatory support and clinical evidence further reinforce adoption, with coated devices demonstrating notable reductions in restenosis and complications. Innovations in coating technology, including multifunctional and bioactive surfaces, are accelerating their integration into chronic care, positioning medical device coatings as essential for improving patient outcomes and extending device longevity across cardiovascular, orthopedic, and other applications.

Expansion of Minimally Invasive Procedures Fueling Market Growth

The rising adoption of minimally invasive surgeries (MIS) is a key driver for the medical device coatings market. Coatings, particularly hydrophilic types, reduce friction, enable smoother device insertions, and minimize tissue trauma, aligning with surgeons’ preference for precision and efficiency. MIS procedures are increasing annually, creating higher demand for devices with enhanced surface properties.

Enhanced patient outcomes, lower infection risks, and regulatory approvals for coated MIS devices are reinforcing this trend. Studies show hydrophilic coatings can reduce insertion forces by up to 70%, while FDA clearance data indicates growing approval rates for coated instruments. Overall, MIS advancements are expanding the market by broadening device applications and supporting superior procedural safety.

Restraints - Stringent Regulatory Approval Processes Limit Market Entry

Lengthy and complex regulatory requirements from agencies like the FDA, EMA, and other equivalents create significant barriers for coated medical devices. Approval timelines often span 2-3 years, with many submissions delayed due to rigorous biocompatibility testing under ISO 10993 standards. These challenges increase operational costs, slow innovation, and disproportionately affect smaller players seeking market entry.

High failure rates in preclinical and clinical trials, combined with strict safety standards, further constrain product launches. As a result, market penetration is limited, and the diversity of available coated devices is restricted. Regulatory hurdles remain a key restraint, impacting development cycles, investment incentives, and the speed at which new coatings reach clinical adoption.

High Development and Material Costs Hinder Market Growth

Elevated R&D and material costs pose major challenges in the medical device coatings market. Developing specialized coatings, such as antimicrobial or anti-thrombogenic formulations, can require $5-10 million per product, driven by expensive raw materials like silver nanoparticles and other advanced compounds. Supply chain fluctuations exacerbate cost pressures, particularly in emerging markets.

These high expenses limit scalability and accessibility for cost-sensitive applications, while reimbursement constraints further challenge affordability. The financial burden on manufacturers slows commercialization and adoption, restraining overall market expansion despite growing clinical demand for advanced and multifunctional coated devices.

Opportunity - Expansion into Emerging Markets Presents Significant Growth Potential

Medical device coatings manufacturers have substantial opportunities in emerging regions such as Asia Pacific and Latin America, driven by rising healthcare infrastructure investments. Growing medical device demand in countries like India and China creates strong markets for cost-effective hydrophilic and antimicrobial coatings. Local manufacturing hubs further reduce production costs, enabling wider adoption in high-volume applications like orthopedics, cardiology, and general surgery.

Supportive government initiatives and favorable regulatory changes, including streamlined approvals and health policy programs, enhance market accessibility. By leveraging these expanding markets, companies can achieve higher revenue, increase device penetration, and establish a strong foothold in regions with rapidly growing healthcare needs.

Nanotechnology and Smart Coatings Unlock Next-Generation Market Opportunities

Advances in nanotechnology and smart coating systems offer transformative potential, particularly in drug-eluting and on-demand therapeutic release devices. Nanoparticle integration improves efficacy and reduces complications, such as thrombosis in cardiovascular applications, while self-healing polymers extend device longevity.

Companies focusing on neurology and chronic disease applications, including Alzheimer’s care, can capitalize on rising demand driven by the growing patient population. By adopting these innovative technologies, manufacturers can differentiate their products, enhance clinical outcomes, and secure a competitive edge in the expanding medical device coatings market.

Category-wise Analysis

Product Insights

Hydrophilic coatings lead the market with a 35% share in 2025, driven by their essential role in cardiovascular and general surgery devices that require low-friction performance. Over 500 FDA premarket approvals since 2020 highlight their widespread adoption, with studies showing a 60% reduction in procedural complications. Their water-attracting properties ensure lubricity in minimally invasive devices, while biocompatibility under ISO 10993 standards reinforces reliability. High procedure volumes, including 15 million annual angioplasties globally, further cement hydrophilic coatings as the frontrunner in the market.

Antimicrobial coatings represent the fastest-growing segment, responding to increasing demand for infection-resistant devices across hospitals and outpatient settings. Their adoption in orthopedic implants, catheters, and wound care products is rising rapidly. Innovations in material science, such as nanoparticle-based formulations and multifunctional surfaces, are enhancing antimicrobial efficacy and device safety, supporting broader clinical applications and accelerating market growth in response to infection-control priorities.

Substrate Analysis

Metal substrates, particularly stainless steel and titanium, dominate the market with a 45% share in 2025, owing to their durability in high-stress implants such as stents and orthopedic devices. Standards from ASTM International and industry data show that 70% of hip and knee implants utilize coated titanium, reducing wear by up to 50%. Widespread use in cardiovascular applications, including 1.5 million U.S. stents annually, highlights the importance of metals for load-bearing devices and biocompatibility enhancements.

Polymer substrates are emerging as the fastest-growing segment, driven by flexible applications in catheters, tubing, and minimally invasive instruments. Silicone, polyurethane, and polypropylene provide an ideal base for hydrophilic and antimicrobial coatings, enhancing surface performance, device safety, and patient comfort. The adaptability of polymers to new coating technologies is expanding clinical applications and supporting rapid adoption in diverse medical procedures.

Application Analysis

Cardiovascular applications hold the leading position with a 40% share in 2025, supported by rising heart disease interventions. Coated stents, grafts, and vascular devices reduce clotting and restenosis risks, with anti-thrombogenic and drug-eluting coatings cutting clot incidence by 45%. Guidelines from the ESC mandate coated devices for most percutaneous coronary interventions, accounting for 80% of procedures. High prevalence of cardiovascular disease, with 18 million global deaths annually, underpins sustained demand and market leadership in this segment.

Neurology applications are among the fastest-growing areas, driven by rising demand for minimally invasive neurovascular interventions and specialized devices for chronic neurological disorders. Coatings improve the precision, safety, and biocompatibility of catheters, microstents, and medical electrodes. Advancements in drug-eluting and bioactive coatings for neurology devices further expand clinical applications, creating new growth avenues in response to increasing neurological care requirements worldwide.

Regional Insights

North America Medical Device Coatings Market Trends and Insights

North America leads the global medical device coatings market with a 38% share in 2025, driven primarily by the United States. The region benefits from strong innovation, with over 200 FDA 510(k) approvals for coated devices in 2024 alone. Significant NIH funding exceeding $1 billion for biomaterials research supports product development and clinical trials, while stringent regulatory frameworks like 21 CFR Part 820 ensure high quality standards. Hubs such as Boston and Silicon Valley facilitate advanced device testing, delivering efficacy gains up to 30% in cardiovascular and minimally invasive applications.

Canada also contributes to regional growth through supportive policies and adoption of advanced coatings in orthopedic and surgical devices. Robust healthcare infrastructure, high procedure volumes, and favorable reimbursement systems sustain leadership, making North America a mature and highly lucrative market for hydrophilic, antimicrobial, and drug-eluting coatings.

Europe Medical Device Coatings Market Trends and Insights

Europe maintains a strong presence in the medical device coatings market, growing at an estimated CAGR of 6.1% from 2025 to 2032. Germany leads via compliance with the MDR framework, with coated implant growth averaging 15% annually. The U.K.’s MHRA harmonizes standards across the region, boosting exports, while France and Spain are notable for cardiovascular device innovations. EU MDR enforcement has driven a 20% increase in new product development since 2021, particularly in biocompatible and antimicrobial coatings.

Smaller Western European countries are gradually adopting advanced coating technologies for minimally invasive and orthopedic applications. Strong regulatory oversight, high clinical procedure rates, and established healthcare infrastructure position Europe as a steadily growing and strategically important region in the global market.

Asia Pacific Medical Device Coatings Market Trends and Insights

Asia Pacific is the fastest-growing region, projected at an 8.5% CAGR from 2025 to 2032, capturing a 32% share in 2025. China leads in manufacturing output, while Japan focuses on hydrophilic coating innovation. India and ASEAN countries expand via initiatives like Make in India, with CDSCO approvals increasing, leveraging cost advantages for both domestic use and exports.

Growth is fueled by rising healthcare access, infrastructure investments, and increasing demand for minimally invasive procedures. The region’s combination of manufacturing capabilities, regulatory modernization, and adoption of advanced coatings makes it a high-potential market for hydrophilic, antimicrobial, and drug-eluting devices across multiple clinical applications.

Competitive Landscape

The medical device coatings market is moderately consolidated, with leading players investing heavily in R&D and strategic partnerships to enhance technological capabilities. Companies are expanding through acquisitions and capacity development, focusing on innovations such as nanotechnology and multifunctional coatings with self-healing and bioactive properties. These initiatives help maintain a competitive edge in high-demand applications like cardiovascular, orthopedic, and minimally invasive devices.

At the same time, the market sees fragmentation among smaller and niche providers, particularly in antimicrobial and specialized coating segments. This diversity fosters innovation in drug-eluting and smart coatings, driving new product development and catering to evolving clinical needs.

Key Market Developments

- In March 2025, Surmodics introduced a next-generation hydrophilic coating for neurovascular devices, designed to improve glide and maneuverability during complex minimally invasive procedures, enhancing procedural efficiency and patient safety.

- In July 2024, Biocoat expanded its antimicrobial coating production facility in Pennsylvania to meet growing demand in cardiology applications, aiming to reduce device-associated infections and support broader clinical adoption of coated cardiovascular devices.

- In November 2023, Harland Medical Systems collaborated with Medtronic to develop drug-eluting coatings for stents, enhancing controlled drug release, improving elution rates, and increasing device efficacy in cardiovascular interventions.

Companies Covered in Medical Device Coatings Market

- Surmodics Inc.

- Biocoat Inc.,

- Harland Medical Systems

- DSM Biomedical

- AST Products Inc.

- Medicoat, Aphria Pharma

- Sonocoating

- Materion Corporation

Frequently Asked Questions

The global Medical Device Coatings Market is expected to reach US$ 15.6 billion in 2026 and grow to US$ 23.9 billion by 2033 at a CAGR of 6.3%.

Rising chronic diseases and minimally invasive procedures drive demand for hydrophilic and anti-thrombogenic coatings.

North America leads with a 38% share in 2025, supported by FDA approvals and innovation hubs.

Nanotechnology innovations for smart coatings present growth potential, especially in emerging markets.

Key players include Surmodics, Inc., DSM, PPG Industries, Inc., Sono-Tek Corporation, and Materion Corporation.