- Medical Devices

- Medical and Industrial Gloves Market

Medical and Industrial Gloves Market Size, Share, and Growth Forecast 2026 - 2033

Medical and Industrial Gloves Market by Product Type (Reusable Gloves, Fabric Supported Gloves, Industrial & Household Gloves, Disposable Examination Gloves, Surgical Gloves, Disposable Industrial Gloves), by End Users, by Regional Analysis, 2026-2033

Medical and Industrial Gloves Market Size and Trend Analysis

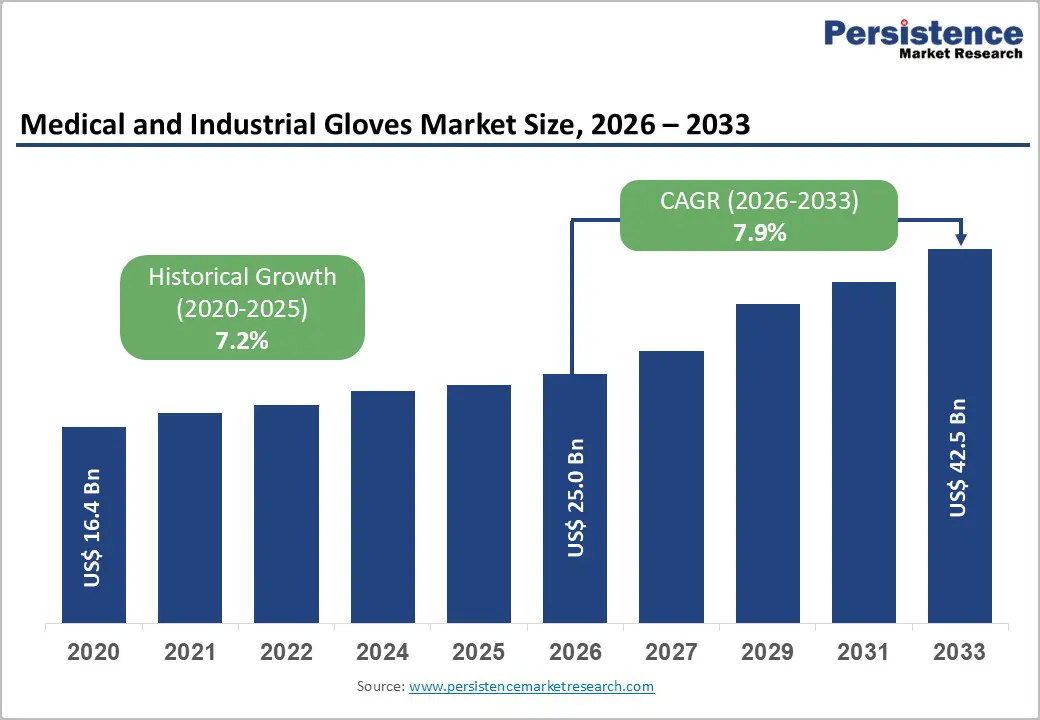

The global medical and industrial gloves market size is expected to be valued at US$ 25.0 billion in 2026 and projected to reach US$ 42.5 billion by 2033, growing at a CAGR of 7.9% between 2026 and 2033.

The medical and industrial gloves market has experienced significant growth globally, driven by increasing awareness of hygiene, workplace safety, and infection control. Disposable examination gloves are gaining the highest traction due to rising demand for natural rubber, non-powdered, and hypoallergenic options. Their ease of use, convenience, and compliance with safety standards make them highly preferred in healthcare, laboratory, and research settings. Growing concerns about hospital-acquired infections further support the adoption of disposable gloves, positioning the medical sector as the largest end-user segment.

Key market trends include the shift from powdered to non-powdered gloves, rising focus on single-use solutions, and increasing applications across industrial and household sectors. However, challenges such as bans on powdered gloves and attempts to reuse disposable gloves may limit adoption. Ongoing product innovations, enhanced safety standards, and rising global demand are expected to sustain growth during the forecast period.

Key Market highlights

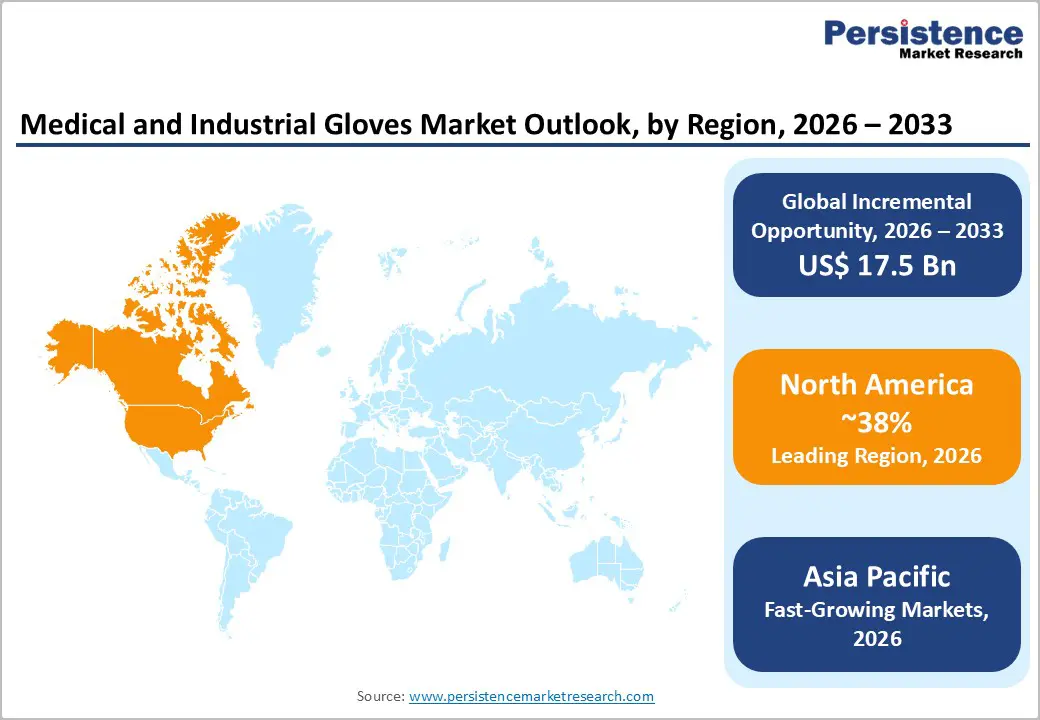

- Leading Region: North America leads with ~38% share, driven by advanced healthcare, strict safety protocols, and high glove usage.

- Fastest Growing Region: Asia Pacific grows fastest, fueled by rising healthcare awareness, industrial safety adoption, and expanding local production.

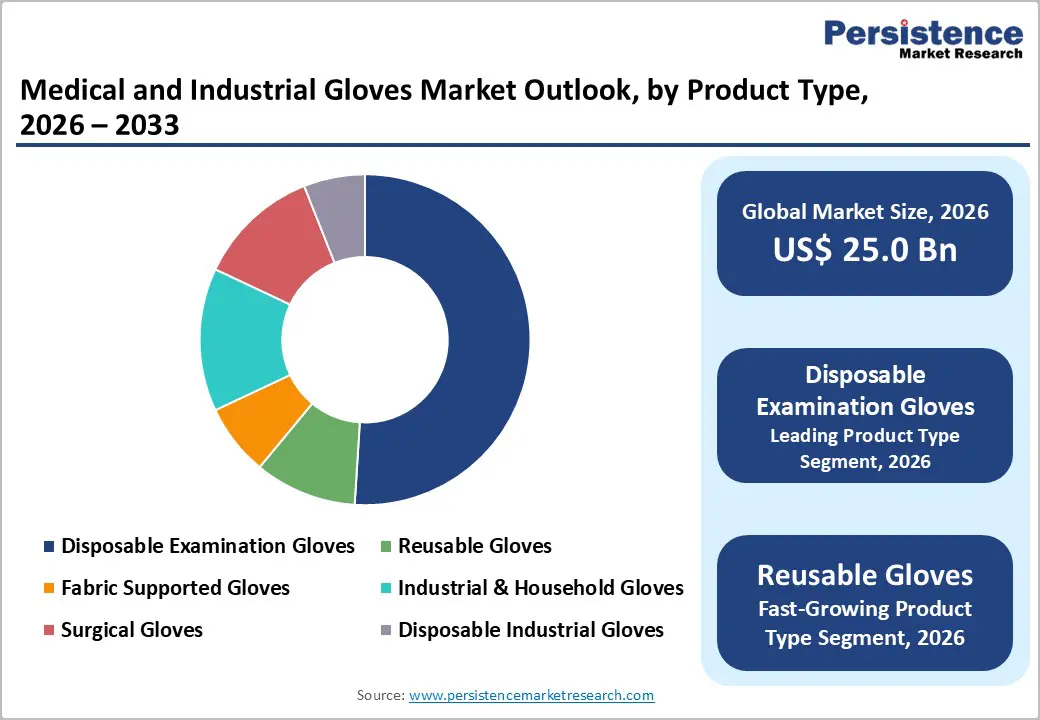

- Dominant Segment: Disposable examination gloves dominate with ~51% share, preferred for infection control, ease of use, and nitrile safety advantages.

| Report Attribute | Details |

|---|---|

|

Medical and Industrial Gloves Market Size (2026E) |

US$ 25.0 billion |

|

Market Value Forecast (2033F) |

US$ 42.5 billion |

|

Projected Growth CAGR (2026-2033) |

7.9% |

|

Historical Market Growth (2020-2025) |

7.2% |

Market Dynamics

Driver- Surge in Healthcare and Hygiene Needs

The global demand for medical and industrial gloves is being strongly driven by heightened healthcare and hygiene requirements, particularly in the post-pandemic era. Hospitals, laboratories, and diagnostic centers are increasingly adopting stringent infection control protocols recommended by authorities like the CDC, significantly raising the use of disposable gloves to prevent cross-contamination. Studies indicate that over 90% of hospitals in the U.S. now comply with such protocols, which has notably increased the preference for nitrile gloves due to their superior durability, chemical resistance, and reduced allergy risk compared to latex.

In addition, rising surgical volumes, expanding outpatient procedures, and growing patient awareness in emerging markets are further propelling glove consumption. Healthcare providers increasingly tie glove usage to patient safety metrics and quality care outcomes, making gloves an essential component of routine operations. This trend is complemented by growing laboratory, research, and diagnostic activities worldwide, where gloves are crucial for personnel safety and contamination prevention. Collectively, these factors are sustaining strong growth in both medical and industrial glove segments globally.

Restraint- Raw Material Supply Chain Disruptions

The growth of the medical and industrial gloves market is restrained by frequent disruptions in raw material supply, particularly for nitrile and latex. Geopolitical tensions, natural disasters, and fluctuations in the availability of key raw materials in Asia the primary sourcing hub have resulted in production delays and inflated costs. Such volatility affects roughly 20–30% of global glove output, creating challenges for manufacturers to maintain consistent supply.

Smaller and mid-sized glove manufacturers face additional difficulties, as rising raw material prices increase operational costs and compliance pressures. In regions with limited local production, dependency on imports exacerbates shortages, leading to delayed deliveries and occasional stockouts. These supply chain constraints can hinder the ability to meet the rising demand in both healthcare and industrial sectors, limiting overall market expansion despite strong consumption trends.

Opportunity- Expansion in Non-Medical Sectors

Beyond healthcare, significant growth opportunities exist for medical and industrial gloves in non-medical sectors such as food processing, pharmaceuticals, cleanrooms, and manufacturing. Stringent hygiene and safety regulations in these industries are increasing the demand for disposable gloves to prevent contamination, ensure worker safety, and comply with regulatory standards. The rising focus on occupational health, particularly in emerging markets like ASEAN countries, is further boosting market potential.

Advances in glove technology, such as nitrile gloves with enhanced tactile sensitivity and touchscreen compatibility, are expanding usability across diverse applications. Industries requiring precision, chemical resistance, or extended wear are adopting these innovations to improve operational efficiency. Moreover, as businesses prioritize worker protection and hygiene, bulk procurement and standardization of glove usage are becoming more common, creating long-term demand. Together, these factors position non-medical sectors as a high-growth avenue for manufacturers seeking to diversify beyond traditional healthcare markets.

Category-wise Insights

Product Type Analysis

Disposable examination gloves are the leading product type in the medical and industrial gloves market, capturing approximately 51% of the global share in 2025. Their dominance is primarily driven by widespread use in infection prevention across hospitals, laboratories, and diagnostic centers. These gloves play a critical role in minimizing cross-contamination risks during clinical procedures, aligning with stringent guidelines from organizations such as the CDC. Hospitals report usage of disposable gloves in over 60% of routine examinations, highlighting their integral role in daily healthcare operations.

Among disposable gloves, nitrile variants are particularly favored due to their superior chemical resistance, durability, and reduced risk of allergic reactions. Latex allergies, which affect 5–10% of healthcare workers, make nitrile a safer alternative, offering reliable barrier protection without compromising dexterity. Ease of use, single-use convenience, and compliance with infection control standards further reinforce their preference. Overall, the combination of safety, regulatory alignment, and healthcare sector dependence ensures that disposable examination gloves remain the most adopted and fastest-growing product type within the medical and industrial gloves market.

End Use Analysis

The medical sector, particularly acute care settings, represents the largest end-use segment for medical and industrial gloves, accounting for around 48% of the market share in 2025. Hospitals, intensive care units (ICUs), and emergency departments are the primary consumers, where high-volume glove usage is essential for patient safety, infection prevention, and staff protection. Gloves are indispensable during surgeries, invasive procedures, and routine examinations, making procurement a critical part of hospital operations.

Regulatory mandates from OSHA and CDC strongly influence glove usage in acute care, ensuring adherence to hygiene protocols and reducing hospital-acquired infections. Hospitals procure approximately 47.7% of gloves for these purposes, with powder-free gloves preferred for precision tasks and patient safety. Beyond surgeries, gloves are essential in laboratory services, diagnostic testing, and research applications, all of which are integral to acute care facilities. The combination of high procedural demand, regulatory compliance, and infection control measures sustains the medical sector’s dominance as the leading end-user segment in the global gloves market.

Regional Insights

North America Medical and Industrial Gloves Market Trends and Insights

North America dominates the medical and industrial gloves market, with the United States accounting for the largest regional share in 2025. Growth is driven by advanced healthcare infrastructure, stringent regulatory frameworks, and high awareness of occupational safety and infection control. Disposable gloves, particularly nitrile and latex-free options, are widely used across hospitals, laboratories, and diagnostic centers to prevent cross-contamination. CDC and OSHA guidelines reinforce glove usage in surgeries, intensive care units, and routine examinations, contributing to high consumption levels.

The region also benefits from robust domestic manufacturing and well-established supply chains, ensuring reliable availability of medical and industrial gloves. Increasing surgical volumes, rising hospital admissions, and heightened emphasis on worker protection in industrial settings further support demand. Additionally, technological advancements such as powder-free gloves, improved tactile sensitivity, and ergonomic designs are driving adoption. With continued focus on hygiene standards and patient safety, North America is expected to maintain its leadership position, while ongoing R&D and regulatory support will sustain steady growth in both medical and industrial glove segments.

Asia Pacific Medical and Industrial Gloves Market Trends and Insights

Asia Pacific is the fastest-growing region in the medical and industrial gloves market, led by countries such as China, India, Japan, and Southeast Asian nations. Growth is fueled by increasing healthcare awareness, expanding hospital networks, and rising adoption of advanced hygiene protocols. Disposable examination gloves, particularly nitrile and non-allergenic variants, are gaining traction due to infection control requirements in hospitals, laboratories, and research facilities. Rapid urbanization, rising middle-class populations, and greater healthcare expenditure are also contributing to regional demand.

The industrial sector in Asia Pacific is driving growth as well, with expanding manufacturing, food processing, and cleanroom operations requiring high volumes of protective gloves. Local manufacturing hubs in countries like Malaysia, Thailand, and China enhance production capacity and cost-efficiency, supporting both domestic consumption and exports. Innovation in glove design, such as touchscreen-compatible nitrile gloves and powder-free options, further boosts adoption. Overall, rising regulatory compliance, industrial expansion, and growing awareness of occupational and medical hygiene are expected to maintain strong market growth across the Asia Pacific region.

Competitive Landscape

Market Structure Analysis

The medical and industrial gloves market is moderately consolidated, with a mix of global leaders and regional manufacturers shaping competition. Key players such as Ansell, Top Glove, Hartalega, and Kossan dominate through large-scale production, advanced R&D, and extensive distribution networks. Market structure is segmented by product type (disposable examination, surgical, reusable, industrial gloves), material (nitrile, latex, vinyl), and end use (medical, industrial, household). High entry barriers exist due to stringent regulatory compliance, quality standards, and raw material sourcing. Strategic mergers, acquisitions, and partnerships are common to expand geographic presence and product portfolios, ensuring market growth and competitive advantage.?

Key Market Developments

- In May 2025, Hyderabad-based Wadi Surgicals, India’s leading nitrile glove manufacturer, achieved a significant innovation milestone by introducing accelerator-free nitrile gloves under its flagship brand, Enliva.

Companies Covered in Medical and Industrial Gloves Market

- Ansell

- Comfort Rubber Gloves Industries Sdn Bhd

- Top Glove Corporation Bhd

- Rubberex

- Cardinal Health, Inc.

- B.Braun Melsungen AG

- Kossan Rubber Industries Bhd

- Semperit AG Holding

- Hartalega Holdings Berhad

- Supermax Corporation Berhad.

- Others

Frequently Asked Questions

The global medical and industrial gloves market is valued at US$ 25.0 billion in 2026.

OSHA regulations and CDC hygiene protocols boost usage in healthcare and industry.

North America leads with 38% share in 2025.

Sustainable reusables in non-medical sectors amid eco-policies.

Top Glove, Kossan, Ansell lead with expansions and innovations.