- Medical Devices

- Laboratory Electronic Balance Market

Laboratory Electronic Balance Market Size, Share, and Growth Forecast 2026 - 2033

Laboratory Electronic Balance Market by Product Type (Analytical balances, Precision balances, Micro & semi-micro balances, Top-loading balances), Capacity (Up to 200 g, 200 g – 1 kg, Above 1 kg), Application (Pharmaceutical & biotechnology, Chemical testing, Food & beverage testing, Academic & research, Environmental testing), End-user (Pharmaceutical & biotech companies, Research & academic institutes, Testing laboratories, Industrial quality control), and Regional Analysis, 2026 - 2033

Laboratory Electronic Balance Market Share and Trends Analysis

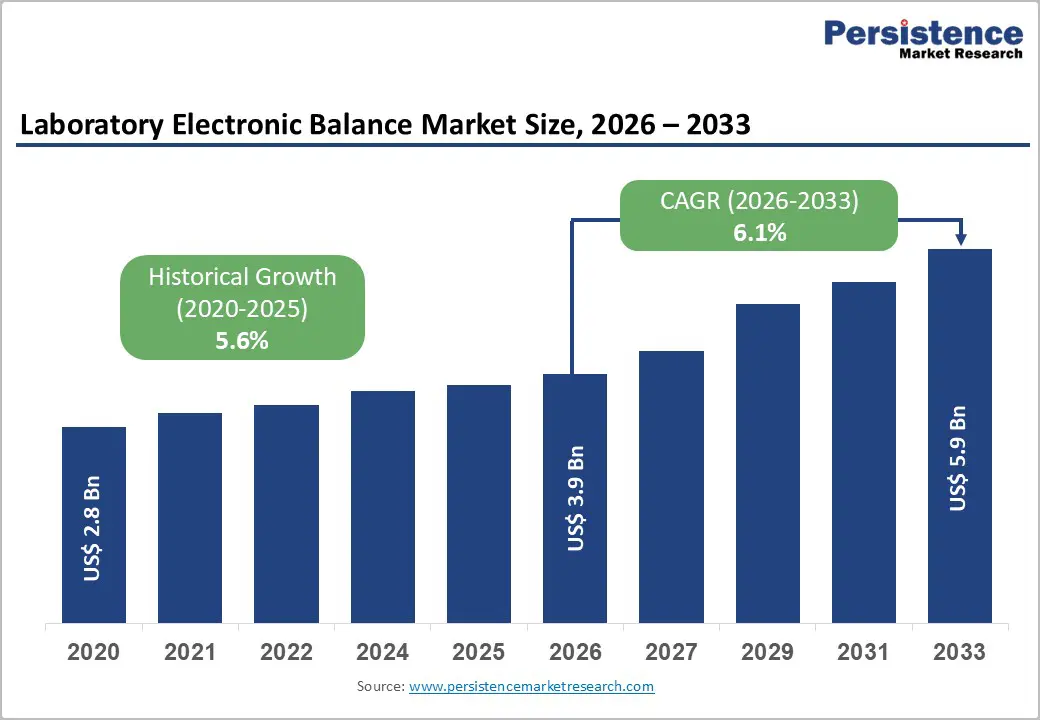

The global laboratory electronic balance market size is expected to be valued at US$ 3.9 billion in 2026 and projected to reach US$ 5.9 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033. This robust growth trajectory is primarily driven by the escalating demand for precision measurement instruments across the pharmaceutical and biotechnology sectors, where regulatory compliance mandates exact measurements for drug formulation and quality control processes.

The pharmaceutical industry's R&D spending reached approximately US$ 280 billion in 2024, with continued investments creating substantial opportunities for advanced laboratory equipment including electronic balances. Additionally, stringent food safety regulations such as the FDA's Laboratory Accreditation for Analyses of Foods (LAAF) program are compelling testing laboratories to adopt high-precision weighing instruments that meet international quality standards, thereby accelerating market adoption across multiple application sectors.

Key Market Highlights

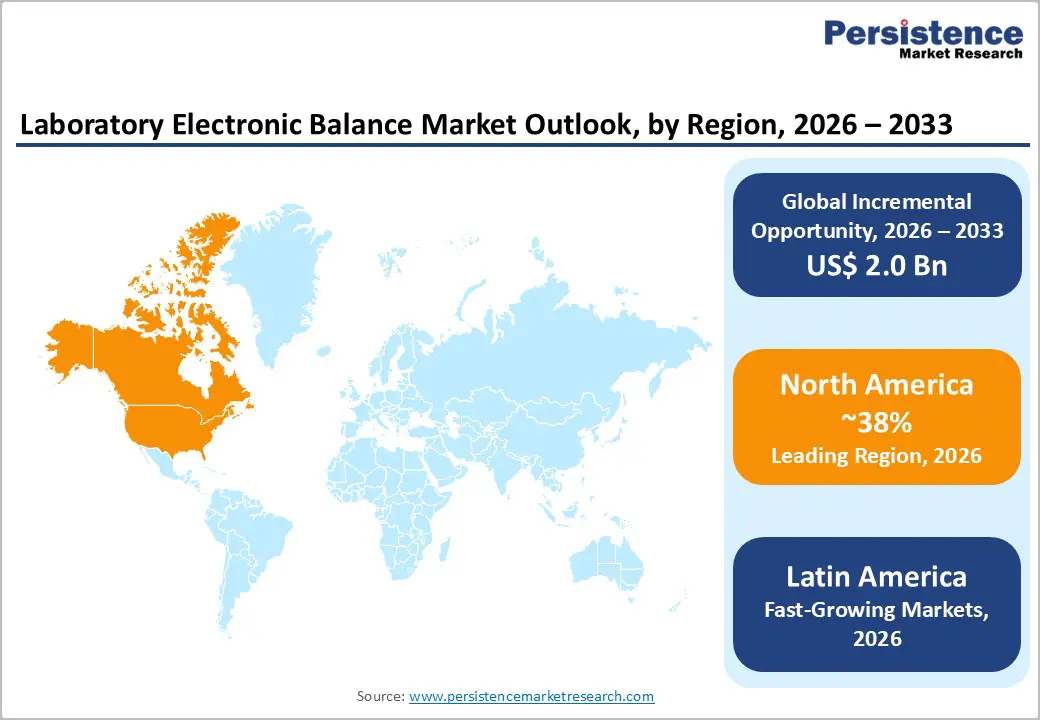

- Leading Region: North America leads the laboratory electronic balance market with about 38% share, supported by strong pharmaceutical and biotechnology R&D, tight FDA regulations, and the presence of major global instrument manufacturers that ensure early access to cutting-edge balances and robust service networks.

- Fastest Growing Region: Latin America is emerging as one of the fastest-growing regional markets, with expected CAGRs above 6.8%, driven by the expansion of pharmaceutical manufacturing in Brazil and Mexico, growing clinical and environmental testing capacity, and progressive adoption of international laboratory accreditation and quality standards.

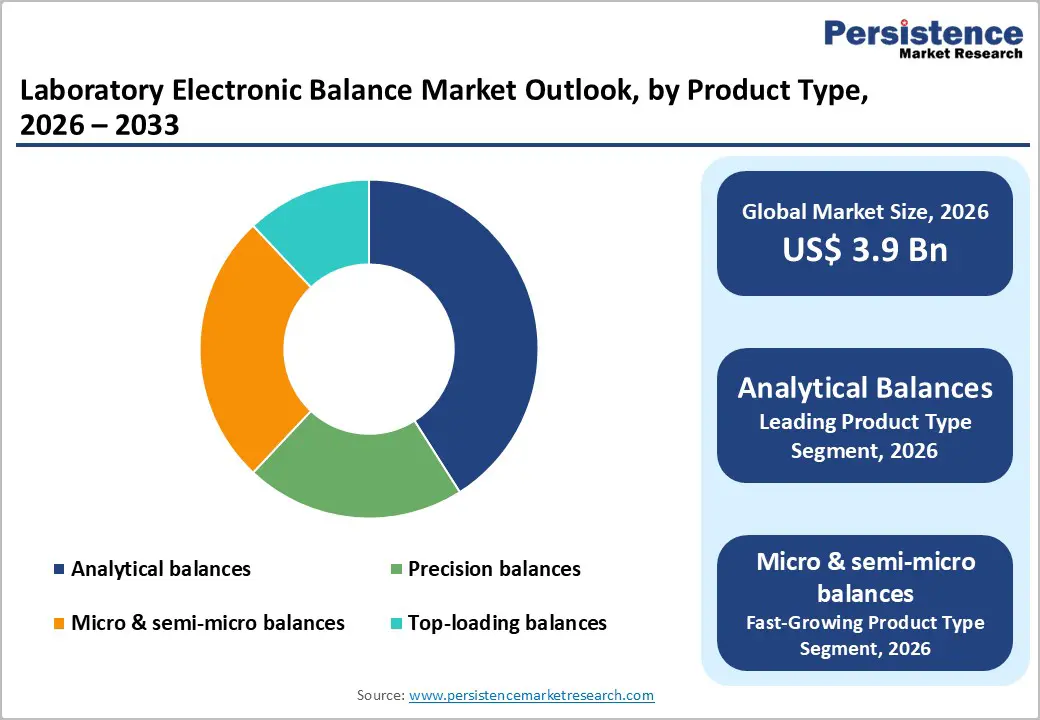

- Dominant Product: Analytical balances are the dominant product segment, holding around 41% share, as they are indispensable for high-precision tasks in pharmaceuticals, biotechnology, and advanced chemical analysis, where readabilities down to 0.01 mg and robust compliance documentation are required for regulated workflows.

- Fastest Growing Product Segment: The Above 1 kg capacity segment is projected to grow fastest at about 6.8% CAGR, propelled by industrial quality control, food and beverage laboratories handling larger samples, and academic labs seeking versatile, robust balances capable of serving multiple disciplines and teaching needs.

| Key Insights | Details |

|---|---|

|

Laboratory Electronic Balance Market Size (2026E) |

US$ 3.9 Bn |

|

Market Value Forecast (2033F) |

US$ 5.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.6% |

Market Dynamics

Drivers - Surging Pharmaceutical and Biotechnology R&D Investments Driving Precision Measurement Demand

The pharmaceutical and biotechnology sectors account for over 30% of global laboratory electronic balance demand, propelled by unprecedented R&D expenditures that surpassed US$ 280 billion in 2024. Drug makers face a collective patent-expiry cliff threatening approximately US$ 150 billion in sales by 2027, prompting record investment in discovery and process-development laboratories that require ultra-precise weighing technologies. Leading pharmaceutical companies, including Merck, Johnson & Johnson, and Roche, each deployed more than US$ 15 billion in R&D budgets during 2024, with significant capital channeled into high-precision analytical instruments. The biotechnology sector’s compound annual growth rate of nearly 10% further amplifies demand, as biopharmaceutical development increasingly requires ultra-precise weighing technologies for mRNA vaccines, cell therapies, and other advanced treatments. Electronic balances with readabilities ranging from 0.01 mg to 0.0001 g play critical roles in drug formulation, quality control, and research applications where measurements must be reproducible and compliant with regulatory standards set by bodies such as the FDA and EMA.

Stringent Quality Control and Regulatory Compliance Standards Across Multiple Industries

Regulatory bodies worldwide are implementing increasingly stringent requirements for accurate and reproducible measurements across healthcare, food, and chemical industries, creating substantial demand for calibrated electronic balances. The FDA's Laboratory Accreditation for Analyses of Foods (LAAF) program, fully implemented in 2024, mandates that testing laboratories use accredited methods and precision instruments to ensure accuracy and reliability of food safety testing, compelling many facilities to upgrade their weighing equipment. In environmental testing, EPA regulations codified under 40 CFR Good Laboratory Practice (GLP) standards require precise measurements for chemical fate testing and pollution monitoring. The International Organization for Standardization (ISO) strengthened the requirements for testing and calibration laboratories under ISO/IEC 17025, necessitating documented quality systems that include regular calibration and validation of electronic balances. In addition, Good Manufacturing Practice (GMP) guidelines mandate that pharmaceutical manufacturers maintain weighing instruments capable of detecting fine mass increments with documented traceability, ensuring product quality and patient safety while driving recurring equipment replacement and upgrade cycles in regulated industries.

Restraints - High Initial Capital Investment and Maintenance Requirements

The acquisition cost of advanced electronic balances, particularly analytical and micro balances offering readabilities of 0.01 mg or finer, represents a significant capital expenditure that can range from about US$ 5,000 to over US$ 30,000 per unit, depending on precision and features. High-precision instruments demand dedicated environments with minimal vibration, controlled temperature, and humidity, necessitating additional infrastructure investments that increase the total cost of ownership. These balances require frequent calibration with certified reference weights traceable to national or international standards, and annual maintenance and calibration costs often reach 15–20% of the equipment’s purchase price. For small and medium-sized laboratories, research institutions with constrained budgets, and facilities in emerging markets, these cumulative costs present formidable barriers to adoption, extending equipment replacement cycles and limiting market penetration in cost-sensitive segments, even when the operational benefits of precision weighing are clear.

Availability of Lower-Cost Alternative Weighing Technologies

Traditional mechanical balances and lower-precision digital scales continue to serve as cost-effective alternatives for applications where ultra-high accuracy is not mandatory, particularly in educational institutions, routine quality checks, and basic laboratory workflows. While electronic balances offer superior accuracy, automated calibration, and digital connectivity, many laboratories conducting simple weighing tasks find that basic instruments costing 50–70% less can adequately meet their operational needs. The availability of used and refurbished laboratory balances in secondary markets further intensifies price competition, as budget-conscious buyers can acquire previously owned premium equipment at substantial discounts. Economic fluctuations and funding constraints affecting research budgets, particularly visible during 2024–2025, when life science tool spending was mixed, and some organizations reported flat or declining instrument budgets, create additional downward pressure on premium equipment sales, as laboratories defer major capital investments in favor of repair and extending the life of existing weighing instruments.

Opportunities - Rapid Expansion of Emerging Market Laboratory Infrastructure

The Asia Pacific region presents significant growth opportunities as countries, including China, India, and Southeast Asian nations, accelerate investments in research infrastructure and healthcare diagnostics. China’s 14th Five-Year Plan emphasizes biotechnology and R&D with large-scale construction of laboratories in hubs such as Beijing, Shanghai, and Wuxi, creating demand for thousands of precision weighing instruments. India’s expanding pharmaceutical manufacturing base, positioned as a leading supplier of generics and vaccines, requires laboratory equipment that meets international quality standards for both domestic regulation and export certification.

The Asia Pacific laboratory automation equipment market is estimated at around US$ 900 million+ in the mid-2020s and projected to grow at a CAGR above 7% through 2033, outpacing global averages. Supportive government initiatives and rising clinical trial activity in the region are driving laboratory modernization. International bodies such as the World Health Organization (WHO) highlight that a growing share of diagnostic laboratories in the Asia Pacific are adopting automation and precision instruments to reduce human error and improve reproducibility, creating sustained demand for electronic balances as foundational infrastructure.

Integration of Smart Technologies and Laboratory Digitalization

The integration of electronic balances with AI, IoT, and cloud-based laboratory information management systems (LIMS) is creating a new wave of value-added offerings in the market. Modern balances now incorporate features such as electrostatic charge detection, advanced draft-shield designs that minimize air turbulence, and visual status indicators that help ensure correct operation and reduce user error. Leading manufacturers such as Mettler-Toledo have introduced new-generation balance platforms with enhanced connectivity via USB, RS232, and Ethernet/LAN, enabling seamless transfer of weighing data directly into LIMS and ELN environments and supporting compliance with 21 CFR Part 11 for electronic records. Some models integrate automated dispensing capabilities for powders and liquids, real-time data integrity checks, and predictive maintenance analytics based on usage patterns. As laboratories move toward digital workflows, electronic balances with embedded software for method management, audit trails, and secure user authentication are becoming critical, allowing suppliers to command premium pricing and creating differentiation opportunities around data integrity and connectivity rather than just hardware precision.

Category-wise Analysis

Product Type Insights

Analytical balances are the leading product type in the laboratory electronic balance market, accounting for around 41% market share in 2025. Their dominance stems from their central role in pharmaceutical, chemical, and biotechnology laboratories that require readabilities in the 0.1 mg to 0.01 mg range for formulation, assay preparation, and reference standard handling. Pharmaceutical protocols and compendial methods frequently specify analytical balances for weighing active pharmaceutical ingredients and excipients under GLP and GMP conditions. Major suppliers such as Mettler-Toledo and Sartorius collectively hold a large share of this segment, supported by strong brand trust and regulatory acceptance. While analytical balances hold the largest share, micro and semi-micro balances are the fastest-growing sub-segment, with expected CAGRs above 6.5% for the forecast period, driven by ultra-trace analysis, nanomaterials research, and high-end pharmaceutical applications where sub-milligram precision is essential.

Capacity Insights

Within the capacity spectrum, the 200 g – 1 kg range is expected to be the leading segment, with an estimated 44% share in 2025. Balances in this range provide an optimal balance between precision and usable capacity, making them suitable for a wide variety of tasks, including sample preparation, formulation studies, and general QC in chemical and pharmaceutical laboratories. Their versatility reduces the need for multiple overlapping instruments, which appeals to laboratories focused on space and budget optimization. At the same time, the Above 1 kg segment is projected to be the fastest-growing, with an anticipated CAGR of about 6.8% during 2025–2032. This growth is associated with increasing use in industrial quality control, bulk sample handling in food and beverage testing, and academic laboratories where higher-capacity balances are needed for teaching and pilot-scale experiments, while still providing sufficient accuracy for standards and test methods.

Application Insights

Pharmaceutical and biotechnology applications are the largest segment, accounting for roughly 36% in 2025. These users rely heavily on electronic balances for tasks such as formulation, stability testing, sample preparation, reference standard weighing, and in-process control during manufacturing. Biopharmaceutical development, including monoclonal antibodies, vaccines, and cell and gene therapies, requires precise measurement of small amounts of critical components, thereby increasing the need for analytical and micro balances that deliver repeatable results with tight tolerances. Regulatory frameworks from the FDA, EMA, and ICH stipulate controls on weighing processes and documentation, reinforcing recurring demand and driving the replacement of older equipment with models offering automated calibration and data integrity features. Environmental testing is the fastest-growing application area, with projected CAGRs of nearly 7.2%, driven by tighter environmental regulations, national pollution monitoring programs, and climate-related research. Laboratories analyzing soil, water, and air samples for contaminants must follow protocols that rely on precise mass measurements, particularly at trace and ultra-trace concentrations.

End-user Insights

Research and academic institutes are expected to be the leading end-user group, contributing about 38% of market share in 2025. Universities, public research bodies, and government laboratories run large numbers of multidisciplinary labs that require multiple balances for teaching and research in chemistry, biology, materials science, and engineering. Public and competitive grant funding from agencies such as the NIH in the U.S. and national science foundations in Europe and Asia supports ongoing procurement and lifecycle replacement of balances, often with emphasis on models that can be shared across departments while meeting varied precision requirements. Testing laboratories, including independent contract labs and specialized analytical service providers, are the fastest-growing end-user category, with an anticipated growth near 6.9% CAGR through 2032. The rise of outsourcing in pharmaceuticals, food and beverage, and environmental analysis, combined with accreditation standards such as ISO/IEC 17025 and programs such as LAAF, drives investment in compliant, regularly calibrated balances to ensure that reported results withstand regulatory and legal scrutiny.

Regional Insights

North America Laboratory Electronic Balance Market Trends and Insights

North America is the leading regional market, accounting for approximately 38% share in 2025. The region’s strength is anchored in the United States, which hosts a dense concentration of global pharmaceutical companies, biotechnology firms, CROs, and academic medical centers. U.S. pharmaceutical R&D spending alone exceeded US$ 100 billion in 2024, generating strong, recurring demand for high-precision laboratory equipment. Regulatory oversight by the FDA requires robust control and documentation of all weighing activities in GMP and GLP environments, including routine calibration and verification, pushing laboratories to use modern electronic balances with internal calibration, audit trails, and integration with electronic systems.

North America also benefits from being home to major equipment manufacturers such as Mettler-Toledo International (headquartered in Ohio), Thermo Fisher Scientific (Massachusetts), and Ohaus Corporation (New Jersey), which ensures a strong local supply chain, rapid service support, and early access to new technologies. Top research institutions, including Harvard, MIT, Stanford, and leading state university systems, maintain extensive laboratory infrastructure that sets high expectations for instrument performance. In addition to pharma and biotech, environmental and food testing laboratories are expanding capacity to meet evolving EPA and food safety regulations, further reinforcing the region’s demand base for analytical, precision, and high-capacity balances.

Asia Pacific Laboratory Electronic Balance Market Trends and Insights

Asia Pacific is the fastest-growing regional market and is projected to achieve a CAGR above 7.5%. China plays a central role, accounting for an estimated 38% of global analytical balance manufacturing capacity and acting as both a major producer and consumer. National strategies embedded in China’s 14th Five-Year Plan promote innovation in biomedicine, advanced materials, and environmental protection, all of which require sophisticated laboratory ecosystems equipped with precision balances. R&D clusters in cities such as Beijing, Shanghai, Shenzhen, and Wuxi are witnessing rapid lab build-outs, backed by government and private investment.

Indian market is another pivotal growth engine, serving as a global hub for generics and vaccines, and requiring internationally compliant testing infrastructure for export markets regulated by the USFDA, EMA, and other authorities. Japanese manufacturers, including Shimadzu Corporation and A&D Company, Ltd., contribute cutting-edge instrumentation and support high standards in domestic and regional laboratories. Across ASEAN countries such as Singapore, Malaysia, Thailand, and Vietnam, governments are promoting pharmaceutical, biotech, and food processing industries, which directly increases demand for compliant laboratory equipment. Broader growth of laboratory automation and rising healthcare spending across the region, combined with cost advantages in manufacturing and skilled technical labor, positions Asia Pacific as a strategic focal point for both global suppliers and local producers of electronic balances.

Competitive Landscape

The laboratory electronic balance market shows moderate to high competition, driven by continuous innovation, precision requirements, and regulatory compliance. Manufacturers compete mainly on accuracy, reliability, automation, and digital integration. Demand for higher sensitivity, faster stabilization time, and user-friendly interfaces has intensified product differentiation. Price competitiveness remains important, especially in academic and routine testing laboratories, while premium products dominate pharmaceutical and advanced research settings. Strong distribution networks, after-sales service, and calibration support play a critical role in customer retention.

Key Developments:

- In August 2025, TetraScience, the Scientific Data and AI Cloud company, announced the launch of Tetra Workflows, a comprehensive solution that fundamentally transformed how laboratories managed and automated scientific data workflows at scale. Built on TetraScience’s next-generation Scientific Data Management System (SDMS), the platform addressed a critical challenge faced by global life sciences organizations by eliminating manual, error-prone processes that had delayed key discoveries and slowed time to clinic.

Companies Covered in Laboratory Electronic Balance Market

- Mettler-Toledo International

- Sartorius AG

- Thermo Fisher Scientific

- Shimadzu Corporation

- A&D Company, Ltd.

- Ohaus Corporation

- Radwag Balances and Scales

- KERN & SOHN GmbH

- Adam Equipment

- Precisa Gravimetrics AG

- BEL Engineering

- Citizen Scales India Pvt. Ltd.

- Others

Frequently Asked Questions

The global laboratory electronic balance market is expected to be valued at about US$ 3.9 billion in 2026, reflecting strong demand from pharmaceutical, biotechnology, chemical testing, and research laboratories that rely on precision weighing instruments for compliant, traceable, and reproducible measurement workflows.

The market is driven by rising pharmaceutical and biotechnology R&D investments exceeding US$ 280 billion in 2024, stringent requirements from regulators such as the FDA, EMA, and EPA, expanded healthcare and testing infrastructure in emerging markets, and adoption of smart, connected balances integrating AI, IoT, and automated calibration to enhance accuracy, data integrity, and overall laboratory efficiency.

North America is the leading region, with approximately 38% market share in 2025, supported by extensive pharma and biotech R&D capacity, strict FDA-driven quality systems, a large base of environmental and food testing labs, and the presence of global balance manufacturers that provide advanced products and comprehensive service coverage.

The Asia Pacific region offers the most significant opportunity, with expected CAGRs above 7.5% through 2032 as China, India, Japan, and ASEAN countries invest heavily in biopharma, diagnostics, environmental monitoring, and higher education, while aligning with international quality and accreditation standards that necessitate modern, high-precision electronic balances.

Key companies include Mettler-Toledo International and Sartorius AG as segment leaders, alongside Thermo Fisher Scientific, Shimadzu Corporation, A&D Company, Ltd., Ohaus Corporation, Radwag Balances and Scales, KERN & SOHN GmbH, Adam Equipment, and Precisa Gravimetrics AG, all of which offer comprehensive portfolios spanning analytical, precision, micro, and top-loading balances tailored to regulated and research-intensive markets.