- Healthcare Services

- Clinical Laboratory Services Market

Clinical Laboratory Services Market Size, Share, and Growth Forecast 2026 - 2033

Clinical Laboratory Services Market by Test Type (Clinical Chemistry, Hematology, Microbiology, Immunology, Others), by Application (Disease Diagnosis, Drug Development, Routine Health Checkups), by Service Provider (Hospitals, Diagnostic Laboratories, Clinics, Research Institutes), by Regional Analysis, 2026 - 2033

Clinical Laboratory Services Market Share and Trends Analysis

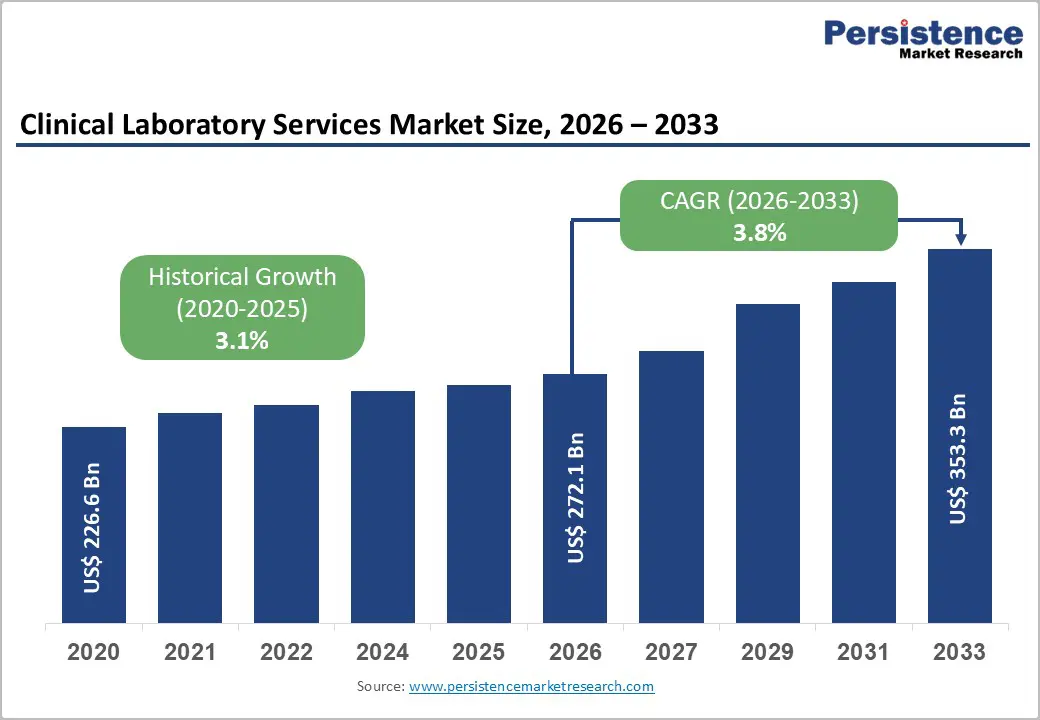

The global clinical laboratory services market size is expected to be valued at US$ 272.1 billion in 2026 and projected to reach US$ 353.3 billion by 2033, growing at a CAGR of 3.8% between 2026 and 2033.

The market expansion is driven by rising prevalence of chronic and infectious diseases worldwide, combined with an aging global population requiring more frequent diagnostic testing. According to the Centers for Disease Control and Prevention (CDC), chronic diseases account for 7 out of 10 leading causes of death in the United States, necessitating comprehensive laboratory screening programs. Additionally, technological advancements in laboratory automation and artificial intelligence integration are enhancing diagnostic accuracy and reducing turnaround times, thereby accelerating market adoption across healthcare settings.

Key Industry Highlights:

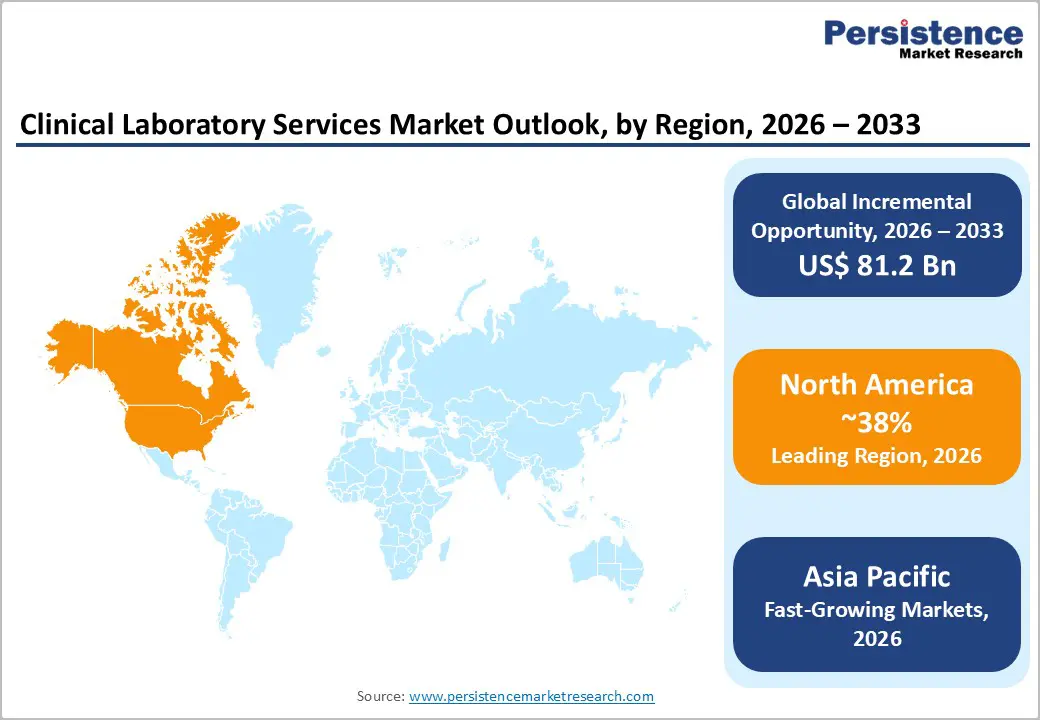

- North America maintains market leadership with approximately 38% global share in 2025, supported by advanced healthcare infrastructure, stringent CLIA regulatory frameworks, and innovation ecosystems driven by Quest Diagnostics and Labcorp pursuing strategic diversification beyond traditional laboratory testing into drug development and clinical trials management.

- Asia Pacific emerges as fastest-growing region with projected 7.84% CAGR through 2031, fueled by universal health coverage expansion in China and India, mandatory infectious disease screening requirements, government infrastructure investments, and diagnostic chain penetration into Tier 2 and Tier 3 cities delivering affordable testing services.

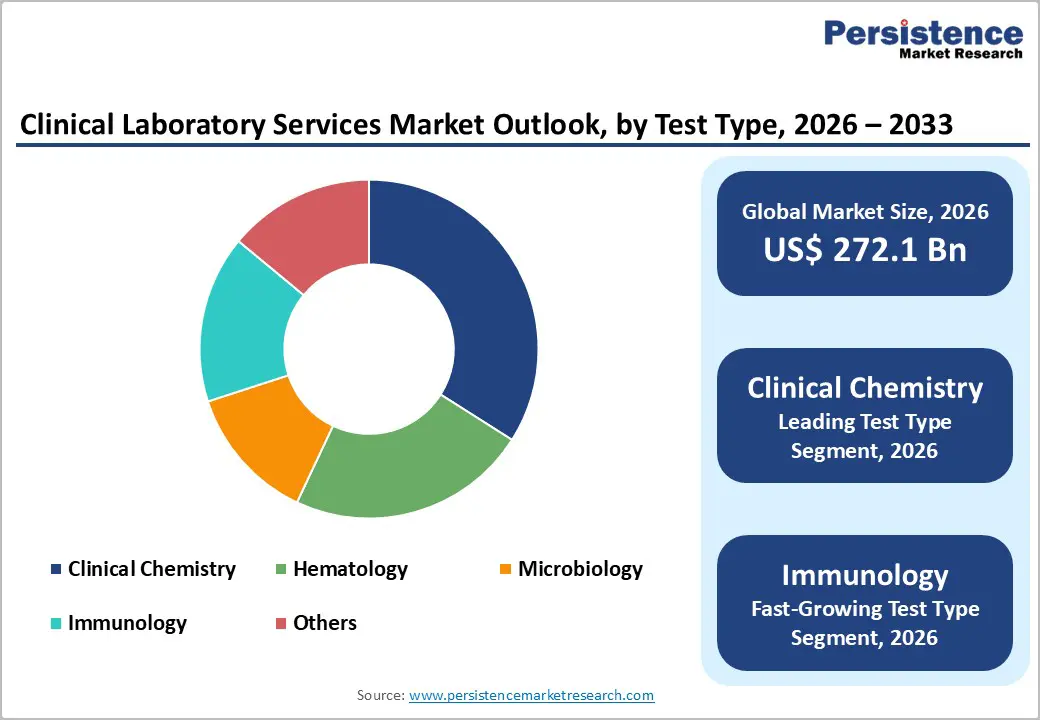

- Clinical chemistry testing dominates with 34% market share in 2025, reflecting universal application across disease states for metabolic panels, organ function assessments, and biochemical monitoring, supported by continuous technological innovation in automated analyzers and artificial intelligence integration for enhanced diagnostic precision and operational efficiency.

- Immunology testing represents fastest-growing segment with immunodiagnostics market expanding from US$ 24.20 billion in 2025 to US$ 70.9 billion by 2034 at 12.84% CAGR, driven by autoimmune disorder prevalence, cancer biomarker testing, infectious disease monitoring, and advanced technologies including chemiluminescence immunoassays and AI-enabled analytical platforms.

- Point-of-care testing expansion presents substantial growth opportunity with global POCT market projected to reach US$ 93.1 billion by 2033 growing at 8.3% CAGR, enabling decentralized diagnostic ecosystems through portable platforms delivering real-time results at patient bedsides, particularly benefiting emergency departments, intensive care units, and operating room applications.

| Key Insights | Details |

|---|---|

| Global Clinical Laboratory Services Market Size (2026E) | US$ 272.1 Bn |

| Market Value Forecast (2033F) | US$ 353.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.1% |

Market Dynamics

Drivers - Rise in Burden of Chronic and Infectious Diseases Driving Laboratory Testing Demand

The global surge in chronic disease prevalence is fundamentally transforming clinical laboratory services' demand patterns. According to the World Health Organization (WHO), noncommunicable diseases accounted for 71% of all global deaths in 2023, with cardiovascular diseases alone resulting in 17.9 million years of life lost annually. The CDC reports that chronic diseases such as diabetes, heart disease, and cancer affect approximately 6 in 10 American adults, requiring frequent laboratory monitoring for disease progression and treatment efficacy. Furthermore, infectious disease outbreaks continue to strain healthcare systems globally, with tuberculosis affecting over 10 million people worldwide annually according to WHO data. Clinical laboratories play an indispensable role in early detection, disease monitoring, and therapeutic decision-making, establishing them as critical infrastructure in modern healthcare delivery systems. The convergence of aging demographics with lifestyle-related disease proliferation ensures sustained demand for comprehensive diagnostic testing services across all geographic markets.

Laboratory Automation and Artificial Intelligence Integration: Enhancing Operational Efficiency

The rapid adoption of laboratory automation systems is revolutionizing clinical diagnostics by addressing critical challenges, including staffing shortages, budget constraints, and quality standardization requirements. Automated platforms now handle complex workflows from sample preparation through analysis, significantly reducing manual processing time and human error rates. According to the American Society for Clinical Laboratory Science, automation systems deployed during the pandemic continue expanding their applications, with digitalization levels in advanced laboratories now exceeding 70% in facilities like SYNLAB's Munich location. Artificial intelligence algorithms are transforming diagnostic accuracy by analyzing medical images to detect early-stage diseases such as cancer and cardiovascular conditions with precision exceeding traditional methods. Machine learning capabilities enable pattern recognition from vast datasets, facilitating personalized medicine approaches tailored to individual patient profiles. The Clinical Laboratory Improvement Amendments (CLIA) regulatory framework mandates stringent quality control measures, further driving automated system adoption to ensure compliance and enhance result reliability. These technological advancements position clinical laboratories to deliver faster, more accurate diagnostic information essential for timely therapeutic interventions.

Restraints - Critical Shortage of Skilled Laboratory Professionals Constraining Service Capacity

The clinical laboratory industry faces an acute shortage of qualified professionals capable of performing complex diagnostic tests with the required accuracy. Laboratory work demands specialized expertise due to the intricate nature of modern testing methodologies, including molecular diagnostics, genomics, and advanced immunoassays. This skills gap impacts service quality and creates bottlenecks in test result turnaround times, potentially delaying critical treatment decisions. Workforce development challenges are compounded by insufficient training infrastructure and competitive pressure from other healthcare sectors. The shortage particularly affects high-complexity testing areas requiring advanced technical knowledge and certification, limiting laboratory capacity to adopt cutting-edge diagnostic technologies despite growing demand from healthcare providers and patients.

Reimbursement Pressures and Regulatory Compliance Costs Impacting Laboratory Margins

Clinical laboratories operate under intense financial pressure from declining reimbursement rates and escalating regulatory compliance costs. In the United States, the Protecting Access to Medicare Act (PAMA) has imposed ongoing cuts to Medicare reimbursement for laboratory testing, directly impacting revenue streams for diagnostic service providers. Laboratories must simultaneously invest in expensive quality management systems to meet stringent standards established by CLIA, FDA, and state-level regulatory authorities. The regulatory burden is particularly pronounced for laboratories performing laboratory-developed tests, which face evolving oversight requirements affecting operational flexibility. International laboratories confronting the European Union's In Vitro Diagnostic Regulation (IVDR) requirements must allocate substantial resources to achieve and maintain CE marking compliance. These combined financial pressures force laboratories to implement cost-reduction strategies, including consolidation, which may reduce geographic access to specialized testing services in underserved regions.

Opportunities - Point-of-Care Testing Expansion Creating Decentralized Diagnostic Ecosystems

The point-of-care testing segment presents substantial growth opportunities as healthcare delivery models shift toward decentralization and patient-centric care. The global Point-of-Care Testing (POCT) market is projected to reach US$ 93.1 billion by 2033, growing at 8.3% CAGR, significantly outpacing traditional centralized laboratory services growth rates. Hospital-based POCT specifically is expected to reach US$ 44.7 billion by 2033 with a 7.7% CAGR, driven by demand for rapid diagnostic results in emergency departments, intensive care units, and operating rooms. These portable diagnostic platforms enable real-time clinical decision-making at the patient's bedside, reducing treatment delays and improving outcomes for acute conditions. Technological innovations, including microfluidics, lateral flow assays, and smartphone-integrated testing systems, are expanding POCT capabilities beyond simple tests to include complex molecular diagnostics and immunoassays. Clinical laboratories positioned to integrate POCT services with centralized testing operations can capture market share across the entire diagnostic continuum, from simple screening tests to sophisticated genetic analysis, while meeting evolving customer preferences for convenience and speed.

Immunology Testing Segment Acceleration Through Advanced Biomarker Discovery

Immunology testing represents the fastest-growing segment within clinical laboratory services, fueled by breakthrough discoveries in autoimmune disease biomarkers and infectious disease diagnostics. The global immunodiagnostics market is expanding from US$ 24.20 billion in 2025 to an anticipated US$ 70.9 billion by 2034, reflecting a robust 12.84% CAGR. This acceleration stems from the increasing incidence of autoimmune disorders, cancer, and persistent infectious disease burdens requiring sophisticated immune response monitoring. According to the American Cancer Society, breast cancer alone affects over 2.3 million women globally annually, driving demand for immunohistochemistry and tumor marker testing. The CDC reports more than 1.2 million Americans living with HIV, necessitating ongoing immunological monitoring. Technological innovations including chemiluminescence immunoassays, multiplex testing platforms, and AI-enabled analytical systems are enhancing diagnostic precision while reducing testing timeframes. Laboratory service providers investing in specialized immunology testing capabilities, particularly for emerging applications like minimal residual disease detection in oncology and early Alzheimer's disease biomarker assays, position themselves to capture high-value testing volumes. Strategic partnerships between clinical laboratories and pharmaceutical companies for companion diagnostics development create additional revenue streams beyond traditional diagnostic services.

Category-wise Analysis

Test Type Insights

Clinical chemistry testing dominates the clinical laboratory services market with approximately 34% market share in 2025, reflecting its foundational role in disease diagnosis and health monitoring. Clinical chemistry analyzers evaluate internal body fluids to provide precise diagnostic information about metabolic function, organ health, and biochemical imbalances. The segment's market leadership stems from universal application across virtually all disease states, with basic metabolic panels, liver function tests, kidney function assessments, and lipid profiles representing essential diagnostic protocols in both routine checkups and acute care settings. According to market analysis, the global clinical chemistry market reached US$ 15.16 billion in 2024 and demonstrates a sustained growth trajectory toward US$ 22.82 billion by 2032, expanding at 5.25% CAGR.

Modern clinical chemistry has evolved from traditional manual laboratory methods to sophisticated automated testing utilizing advanced chemical analyzers capable of high-throughput sample processing. Major technological advancements include the integration of artificial intelligence for result interpretation and laboratory information systems, enabling seamless data management. The segment benefits from continuous innovation in testing methodologies, expanding biomarker panels, and regulatory standardization requirements that drive adoption of validated commercial systems. Hospital laboratories and diagnostic service providers prioritize clinical chemistry capabilities as core competencies, ensuring sustained demand across all healthcare delivery settings from primary care clinics to specialized research institutions.

Service Provider Insights

Hospital-based laboratories maintain market leadership within the service provider category, accounting for approximately 54-58% market share in 2025 according to industry assessments. This dominance reflects hospitals' integrated role in acute care delivery, where immediate access to diagnostic information proves essential for emergency treatment, surgical decision-making, and critical care management. Hospital laboratories benefit from proximity to patient care areas, enabling rapid sample collection, processing, and result delivery that proves crucial for time-sensitive clinical decisions. The segment serves diverse patient populations across emergency departments, intensive care units, operating rooms, and inpatient wards requiring comprehensive testing capabilities spanning routine chemistry to specialized molecular diagnostics. However, market dynamics are shifting with stand-alone diagnostic laboratories projected as the fastest-growing service provider segment during the forecast period.

Independent laboratories like Quest Diagnostics and Labcorp leverage economies of scale through centralized high-throughput testing facilities, advanced automation platforms, and specialized testing menus unavailable at most hospital laboratories. Quest Diagnostics reported an impressive 14.5% revenue growth in the fourth quarter of 2024, including approximately 5% organic growth, driven by robust utilization trends and strategic acquisitions expanding geographic reach. Independent laboratories are diversifying beyond traditional testing into drug development partnerships, clinical trials support, and advanced genomics services, creating differentiated value propositions. The convenience factor of extensive collection point networks and direct consumer access programs positions stand-alone laboratories to capture market share from hospital-based providers, particularly for routine testing and wellness screening applications.

Regional Insights

North America Clinical Laboratory Services Market Trends and Insights

North America dominates the clinical laboratory services market due to its advanced healthcare infrastructure, high diagnostic testing volumes, and strong adoption of innovative laboratory technologies. The region benefits from a well-established network of hospitals, diagnostic centers, and reference laboratories that support large-scale clinical testing. Rising prevalence of chronic diseases such as diabetes, cardiovascular disorders, and cancer has significantly increased the demand for routine and specialized diagnostic tests. Additionally, growing awareness of preventive healthcare and regular health screening programs has boosted laboratory service utilization. The presence of major laboratory service providers and continuous investments in automation, molecular diagnostics, and AI-enabled laboratory systems further strengthen market growth. Favorable reimbursement policies and government support for disease screening programs also contribute to the region’s dominance. Furthermore, increasing demand for personalized medicine and advanced genetic testing is encouraging laboratories to expand their testing capabilities across the United States and Canada.

Asia Pacific Clinical Laboratory Services Market Trends and Insights

The Asia Pacific clinical laboratory services market is emerging rapidly due to expanding healthcare infrastructure, rising healthcare spending, and increasing awareness of early disease diagnosis. Growing prevalence of chronic diseases such as diabetes, cancer, and cardiovascular disorders has significantly increased the demand for laboratory testing across the region. Countries such as China, India, and Japan are witnessing a strong expansion of diagnostic laboratories and hospital-based testing facilities. Governments are also investing in healthcare modernization and promoting screening programs to improve disease detection rates. In addition, the rising middle-class population and improved access to healthcare services are encouraging more individuals to undergo routine diagnostic tests. The growth of private diagnostic chains and the adoption of advanced technologies such as molecular diagnostics and automated laboratory systems are further strengthening the market. Increasing medical tourism and the development of specialized diagnostic centers are also supporting the expansion of clinical laboratory services across the Asia Pacific region.

Competitive Landscape

The clinical laboratory services market is highly competitive and characterized by the presence of numerous regional and global service providers offering a wide range of diagnostic testing solutions. Competition is primarily based on service quality, test accuracy, turnaround time, pricing, and the ability to offer advanced diagnostic technologies. Many laboratories are focusing on expanding their test portfolios, including molecular diagnostics and specialized pathology services, to meet the growing demand for precise disease detection. Strategic collaborations with hospitals and healthcare providers, along with investments in automated laboratory systems and digital reporting platforms, are strengthening market positioning.

Key Developments:

- In July 2025, RQM+ launched its SMART Solutions Life Cycle Partnership model, designed to provide integrated, end-to-end support for medical device and in-vitro diagnostic companies throughout the product lifecycle. The model combined regulatory, quality, clinical, laboratory, reimbursement, and market access services under a single governance structure to streamline product development and commercialization.

- In November 2025, telehealth company Hims & Hers launched “Labs by Hims & Hers,” a direct-to-consumer laboratory testing platform designed to improve access to preventive health diagnostics. The platform offered up to 120 biomarker tests across 10 health categories, including heart health, metabolism, hormones, inflammation, and stress.

- In October 2024, QIAGEN launched its new QIAcuityDx digital PCR system, designed specifically for clinical diagnostic applications in oncology. The platform aims to deliver highly sensitive and accurate molecular testing, enabling precise detection of cancer-related genetic mutations.

- In August 2024, QIAGEN Singapore Pte. Ltd. partnered with Parkway Laboratories to advance healthcare services through the installation of the QIAstat-Dx syndromic testing system in three of IHH Healthcare's hospitals in Singapore.

Companies Covered in Clinical Laboratory Services Market

- Quest Diagnostics

- Labcorp

- Eurofins Scientific

- Sonic Healthcare

- SYNLAB Group

- NeoGenomics Laboratories

- BioReference Laboratories

- ARUP Laboratories

- Charles River Laboratories

- Qiagen

- SGS SA

- Almac Group

- Others

Frequently Asked Questions

The global clinical laboratory services market is expected to be valued at US$ 272.1 billion in 2026, driven by rising chronic disease prevalence, aging populations, and technological advancements in laboratory automation and artificial intelligence integration enhancing diagnostic accuracy and operational efficiency.

Primary demand drivers include escalating chronic and infectious disease burden with CDC reporting 6 in 10 American adults affected by chronic conditions requiring frequent laboratory monitoring, laboratory automation adoption addressing staffing shortages and enhancing quality standardization, and preventive healthcare emphasis driving routine screening programs across all demographics.

North America dominates with approximately 38% global market share in 2025, supported by advanced healthcare infrastructure, comprehensive CLIA regulatory frameworks administered by CMS, FDA, and CDC, and innovation ecosystems led by Quest Diagnostics and Labcorp pursuing strategic diversification and acquisitions expanding geographic reach and specialized testing capabilities.

Point-of-care testing expansion represents substantial opportunity with global POCT market projected to reach US$ 93.1 billion by 2033 at 8.3% CAGR, enabling decentralized diagnostic ecosystems through portable platforms delivering real-time results essential for emergency departments, intensive care units, and operating rooms, while immunology testing acceleration through advanced biomarker discovery drives market from US$ 24.20 billion in 2025 toward US$ 70.9 billion by 2034.

Leading market participants include Quest Diagnostics and Labcorp in North America pursuing strategic acquisitions and diversification, Eurofins Scientific and SYNLAB Group dominating European markets through consolidation strategies, NeoGenomics Laboratories specializing in oncology diagnostics, ARUP Laboratories focusing on innovation partnerships, and regional leaders including Dr Lal PathLabs, Metropolis Healthcare, and Thyrocare Technologies expanding across Asia Pacific markets.