- Healthcare Services

- On-Site Laboratory Service Market

On-Site Laboratory Service Market Size, Share, and Growth Forecast 2026 - 2033

On-Site Laboratory Service Market by Sample Type (Blood & Urine, Saliva, Soil, Water, Air, Food, Chemicals, Others), Mode of Operation (Automated Testing, Manual Testing, Robotic Testing), Industry, and Regional Analysis, 2026 - 2033

On-Site Laboratory Service Market Size and Trend Analysis

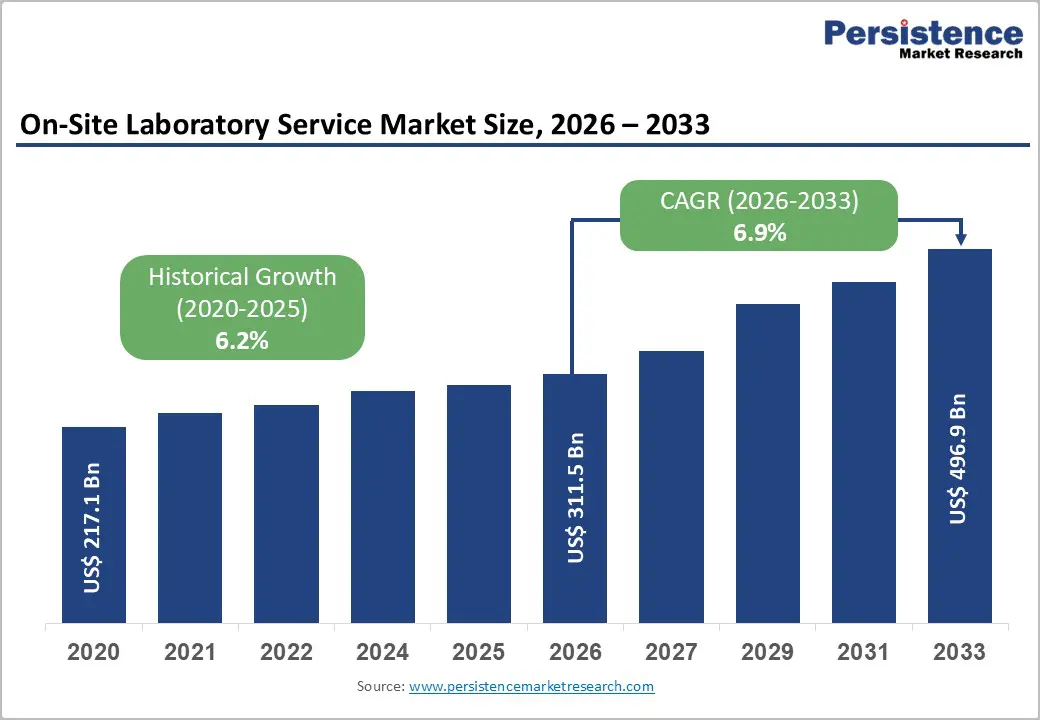

The global on-site laboratory service market size is expected to be valued at US$ 311.5 billion in 2026 and projected to reach US$ 496.9 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033.

On-site laboratory service refers to the provision of laboratory services directly at the location of work or any type of commercial set-up. This type of service aims at providing on-time and accurate testing and analysis of substances/materials, which ensures adherence to safety compliance and regulations. The market encompasses several industries, including manufacturing, forensic, oil and gas, healthcare, environmental monitoring, pharmaceuticals, and construction.

Key Industry Highlights

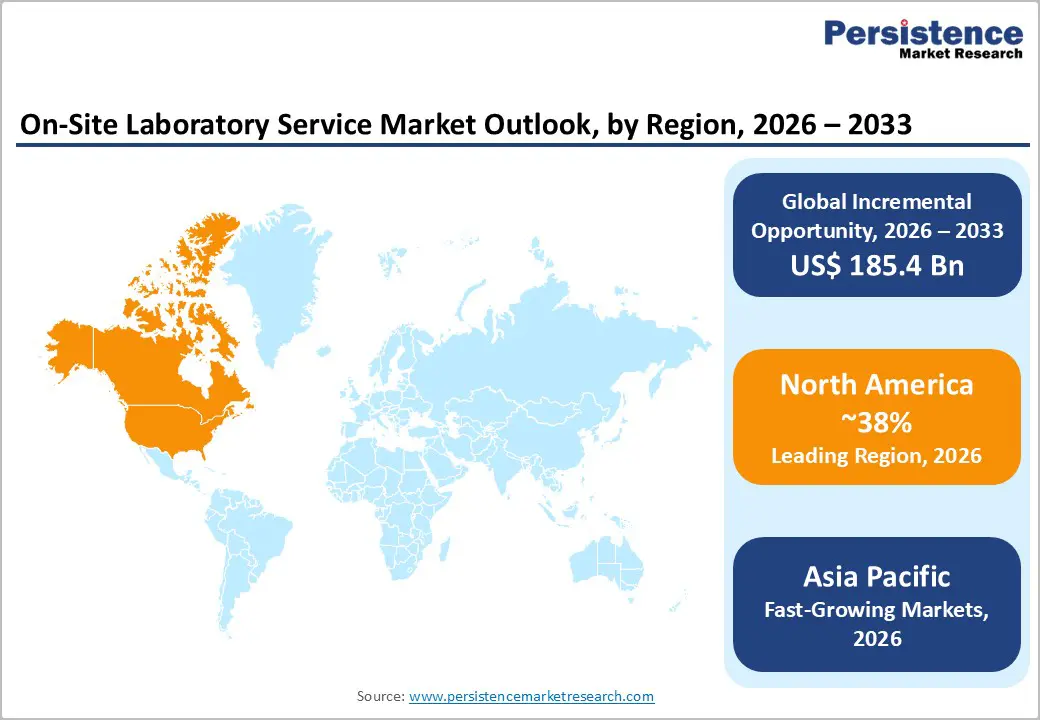

- Leading Region - North America is anticipated to hold a share of about 38% in 2026 and further dominate the market. The dominance is attributed to the presence of advanced healthcare settings and companies in the region, focusing on facility expansion to maintain their stronghold.

- Fastest Growing Region - Asia Pacific is the fastest-growing region, powered by China's SAMR and NMPA regulatory tightening, India's NGT-driven environmental testing mandates, rapidly expanding private hospital networks, and Southeast Asia's strengthening ASEAN food safety and industrial compliance frameworks.

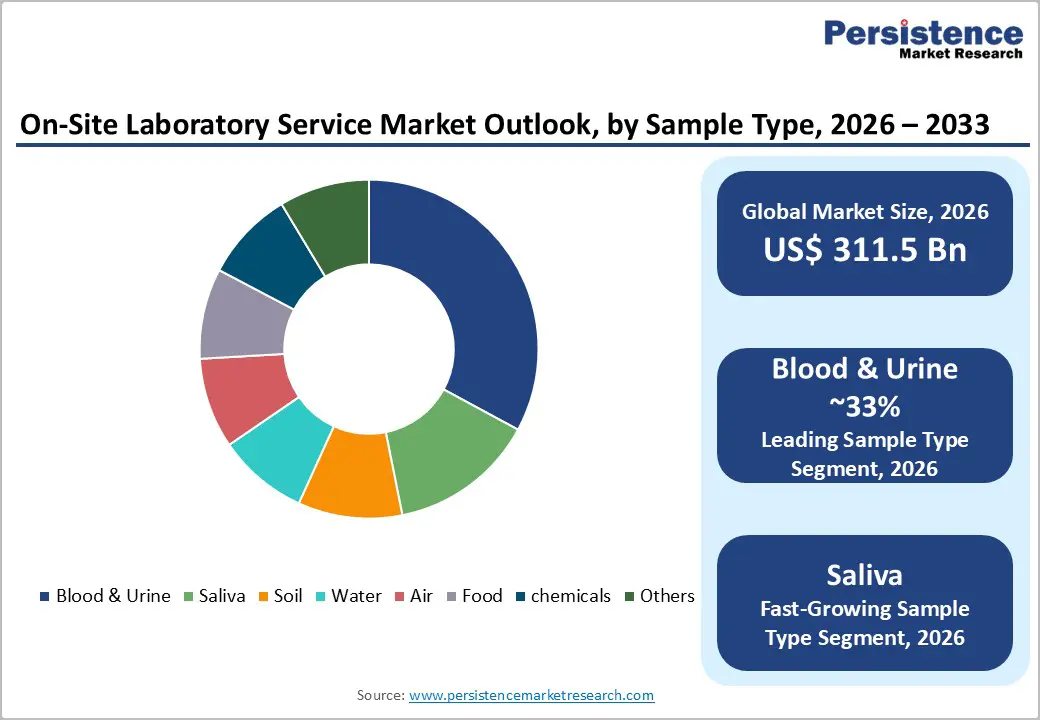

- Dominant Sample Type Segment - Based on sample type, the blood & urine segment is expected to hold a share of about 33% in 2026, driven by increasing prevalence of chronic diseases leading to high adoption of blood & urine tests.

- Fast-Growing Sample Type Segment - Saliva testing is the fastest-growing sample type, catalysed by FDA COVID-era authorizations, U.S. DOT finalization of oral fluid drug testing rules in 2023, and growing adoption in workplace screening and genomic self-collection programs globally.

Market Dynamics

Drivers - Increasing Demand for Technologically Advanced Portable Instruments to Bolster Growth

Portable instruments enable rapid, real-time analysis, which is crucial for immediate decision-making in fields like environmental monitoring, healthcare, and food safety. This capability allows quick responses to emergencies and compliance with regulatory standards. Manufacturers invest in the development of portable, compact and user-friendly diagnostic devices of on-site testing across multiple industries, which is projected to propel the market growth during the forecast period.

For instance, Thermo Fisher Scientific offers portable instruments like the Thermo Scientific TruDefender, a handheld FTIR spectrometer used for rapid chemical analysis in forensic and hazardous material identification.

Growth of Point-of-Care and Decentralized Healthcare Testing Driving On-Site Clinical Lab Demand

The rapid global adoption of point-of-care (POC) and decentralized diagnostic testing accelerated significantly during and after the COVID-19 pandemic is a major growth engine for on-site laboratory services in the healthcare sector. The U.S. Centers for Medicare & Medicaid Services (CMS) regulates CLIA-waived and moderately complex on-site laboratory testing across hospitals, clinics, urgent care centers, and long-term care facilities, with over 260,000 CLIA-certified laboratory sites in the U.S. alone according to CMS data.

The WHO estimates that strengthening laboratory capacity at primary and secondary healthcare levels is essential for universal health coverage, stimulating government investment in embedded on-site laboratory capabilities globally. The expansion of hospital-based clinical chemistry, hematology, and microbiology on-site services continues to drive the largest revenue segment within this market.

Restraint - Regulatory Landscape Challenges Market Growth

Clinical laboratories are required adhere to a wide range of regulatory standards, including CLIA (Clinical Laboratory Improvement Amendments) in the U.S., ISO 15189 for medical laboratories, and FDA guidelines for medical equipment. These standards vary by region and type of testing, making compliance complex and resource intensive. The absence of standardized regulations creates barriers for international operations. Laboratories need to comply with different standards and regulations in all countries, increasing operational costs and complexity. Such factors are projected to challenge the market growth.

Shortage of Qualified Laboratory Personnel and Accreditation Challenges

Operating accredited on-site laboratory facilities requires certified laboratory scientists, quality managers, and instrument operators whose availability is constrained globally. The American Society for Clinical Pathology (ASCP) has documented persistent workforce shortages in laboratory medicine across the U.S., with vacancy rates for medical laboratory scientists exceeding 7%. In remote industrial locations including offshore oil platforms, mining sites, and agricultural processing facilities recruiting and retaining qualified laboratory staff presents an acute operational challenge that increases service cost and limits the geographic expansion of on-site laboratory offerings.

Opportunities - Public-Private Partnerships (PPPs) to Present New Growth Avenues for Market Players

Public-Private Partnerships (PPPs) are expected to help businesses bridge gaps in resources, expertise, and funding. Partnerships with public entities provide private companies access to training programs and regulatory expertise while enhancing their capacity to meet quality standards and regulatory experiments. In addition, by sharing risks with public partners, private businesses mitigate financial risks associated with large-scale investments in laboratory infrastructure.

For instance, the partnership between PEPFAR (U.S. President's Emergency Plan for AIDS Relief) and BD (Becton, Dickinson and Company) is a notable example of a successful public-private collaboration in the healthcare sector. This partnership has significantly contributed to strengthening laboratory systems in African countries of Ethiopia, Kenya, Tanzania, Uganda, and others, heavily burdened by diseases such as HIV/AIDS and tuberculosis.

Saliva-Based Testing Driving the Fastest Growth in Non-Invasive On-Site Diagnostics

Saliva as a sample type is the fastest-growing segment within on-site laboratory services, propelled by its non-invasive collection, elimination of needlestick risks, and suitability for self-collection in workplace, sports, and community health screening programs. During the COVID-19 pandemic, the FDA authorized multiple emergency-use saliva-based SARS-CoV-2 tests, validating saliva as a credible clinical sample matrix and significantly expanding laboratory familiarity with salivary analyte testing.

Beyond infectious disease, saliva-based testing is gaining traction in workplace drug screening with the U.S. Department of Transportation (DOT) finalizing rules permitting oral fluid drug testing for federally mandated safety-sensitive employment categories in 2023. The U.S. Substance Abuse and Mental Health Services Administration (SAMHSA) has updated its oral fluid guidelines accordingly. Growing adoption of salivary diagnostics for hormonal health monitoring and genomic saliva sampling programs further amplifies on-site service demand for this fastest-growing sample type.

Category-wise Analysis

Sample Type Insights

Based on sample type, the blood & urine segment is likely to dominate with a share of approximately 32.4% in 2026. The dominance of the segment is expected to be largely due to increasing prevalence of chronic diseases that is driving the demand for blood & urine tests globally. This test is essential for early detection and management of diseases such as diabetes, cardio-vascular diseases, and others. Besides, the rising geriatric population is leading to a continual need for health monitoring and diagnosis, which is anticipated to favor growth of the segment.

For instance, in August 2024, Labcorp reported its annual sale growth between 6.4% and 7.5%, up from its previous range of 4.8% to 6.4%. This growth is primarily due to the increasing demand for diagnostic testing in their healthcare business.

Mode of Operation Insights

Based on mode of operation, the automated testing segment is anticipated to hold a share of 26.5% in 2026. Automated testing is widely preferred in the healthcare settings to its ability to provide accurate and consistent results, particularly in the areas such as high-throughput screening and minimizing human error. Moreover, automated systems streamline repetitive tasks and enable labs to process more samples and tests in less time. Overall, the high demand for automation in testing is likely to favor growth in the forthcoming years.

Regional Insights

North America On-Site Laboratory Service Market Trends and Insights

North America is likely to dominate and account for 38.5% share in 2026. Presence of a robust healthcare infrastructure in this region, particularly the U.S., supports the integration of on-site laboratory services to enhance patient care through rapid diagnostics. The U.S. companies focus on expanding their manufacturing capabilities to cater to the rising demand for accurate testing results.

For example, in October 2024, Torrent Laboratory, California’s premier environmental testing provider, announced its expansion in Alaska. The company plans to set up a new 20,000 sq.ft state-of-the-art testing facility to offer its signature advanced testing methods such as soil and water testing, soil vapor monitoring and testing, dioxin and furan testing, and others. Such initiatives, led with high demand for rapid, accurate, and accessible testing solutions is anticipated to drive the growth in the U.S. during the forecast period.

U.S. On-Site Laboratory Service Market Size

The U.S. dominates North America with ~87% of regional revenue in 2026, estimated at around US$ 103 billion. Over 260,000 CLIA-certified laboratory sites, FDA FSMA food safety mandates, and EPA NPDES environmental compliance requirements collectively create one of the world's deepest institutional demand bases for on-site laboratory services.

Europe On-Site Laboratory Service Market Trends and Insights

Europe is likely to hold a market share of about 31% in 2026 and is expected to showcase considerable growth in the forthcoming years. In Europe, the primary focus is to ensure agricultural sustainability by balancing three fundamental components, i.e., environmental health, economic profitability, and social and economic equity. The European Union's stringent regulations on food quality and environmental protection drive the demand for agricultural testing services. This includes regular testing for soil health, water quality, and crop contaminants, which on-site laboratories can provide efficiently.

The integration of precision farming techniques, which rely heavily on on-site testing data helps farmers optimize crop yields while minimizing environmental impact. This approach supports the adoption of on-site laboratory services to ensure compliance with EU regulations and enhance sustainability. Owing to the high demand for testing services from the agriculture industry in Europe, the regional companies are focusing on collaboration, partnerships, and product innovation strategies to gain a strong foothold.

For instance, In June 2023, SGS and AgriCircle collaborated to offer soil health measurement tools for regenerative agriculture. This helps farmers and other agri-food industry stakeholders promote sustainable agriculture methods.

Germany On-Site Laboratory Service Market Size

Germany is Europe's largest on-site laboratory service market, estimated at ~US$ 16.5 billion in 2026 representing around 25% of European revenue. Germany's dense chemical and pharmaceutical manufacturing base, stringent DIN EN ISO/IEC 17025 accreditation requirements for industrial testing laboratories, and leadership in environmental monitoring technology underpin consistent high-value on-site service demand.

UK On-Site Laboratory Service Market Size

UK is likely to account for ~17% of the regional share in 2026. NHS hospital laboratory networks, UK Accreditation Service (UKAS) ISO 15189-accredited medical laboratories and growing environmental monitoring service demand from the Environment Agency sustain a well-developed on-site laboratory services market.

Asia Pacific On-Site Laboratory Service Market Trends and Insights

Asia Pacific is anticipated to witness a substantial growth during the forecast period driven by factors such as increasing investments in healthcare sector and expanding pharmaceutical and biotech industries. Further, governments are implementing policies that support private investments in healthcare, with significant growth opportunities and ease of business for the companies. The increasing private investments is expected to boost infrastructure development, promote technological advancements, and forge strategic partnerships supporting the on-site laboratory service market growth.

India On-Site Laboratory Service Market Size

India is a high-growth on-site laboratory service market, estimated at ~US$ 8.4 billion in 2025, accounting for around 11% of Asia Pacific revenue. Rapid hospital network expansion, growing FSSAI food safety compliance requirements, and escalating industrial environmental testing mandates under the National Green Tribunal (NGT) orders are collectively driving on-site laboratory service demand.

Japan On-Site Laboratory Service Market Size

Japan represents Asia Pacific's second-largest on-site laboratory market, valued at ~US$ 14.8 billion in 2025, representing around 19% of regional revenue. Japan's advanced clinical laboratory sector governed by the Japan Accreditation Board (JAB) and rigorous food safety standards enforced by the Ministry of Health, Labour and Welfare (MHLW) sustain high institutional demand for certified on-site testing services.

Competitive Landscape

The global market is supported by the presence of large multinational companies and specialized service providers. These companies adopt strategies such as collaboration, mergers and acquisitions, and investments in research and development activities to gain a stronghold in the market.

Companies are investing in advanced technologies such as automation and AI to improve their overall operational efficiency and differentiate themselves from the competition. Factors such as the rising demand for rapid testing and increasing focus on environmental regulations are likely to propel the companies to adapt quickly to technological and regulatory requirements to maintain dominance.

Key Developments:

- In September 2025, Quest Diagnostics and Epic announced a first-of-its-kind collaboration aimed at streamlining laboratory testing processes and enhancing the overall experience for healthcare providers and patients across the U.S.

- In June 2024, Agilent technology launched EnviroTrack 5000, a field-deployable air quality monitoring tool with IoT-enabled reporting, for the detection of urban pollution hotspots. This tool can detect nitrogen dioxide, ozone, and PM 2.5 pollutants.

- In May 2024, Siemens Healthineers introduced integrated AI-based analysis tool to a mobile diagnostic lab dealing with respiratory disorders. This tool provides real-time lab support to hospitals to control respiratory epidemics.

- In March 2024, PerkinElmer developed portable tool for soil toxicity testing in agricultural and mining sites. Results on heavy metal contamination were reported within fifteen minutes. Bio-Rad Laboratories introduced Mobile quality control (QC) labs for facilities manufacturing biologics. Such facilities were established in South Korea and India where the biotech sector is rapidly emerging.

Companies Covered in On-Site Laboratory Service Market

- Abbott Laboratories

- Quest Diagnostics

- Eurofins Scientific

- SGS Group

- Bureau Veritas

- ALS Limited

- Intertek Group

- Charles River Laboratories

- Pace Analytical, Catalent

- Lonza Group

- Exova Group

- MISTRAS Group

- NSF International

- Schlumberger

- Halliburton

- Others

Frequently Asked Questions

The global on-site laboratory market is estimated at US$ 311.5 billion in 2026.

FDA food safety mandates, EPA compliance rules, CLIA-certified labs, WHO initiatives, and rising laboratory automation are major market drivers.

North America leads with ~38% of the global share in 2026.

Automated robotic on-site laboratories and saliva-based testing offer strong growth opportunities through faster, compliant, and non-invasive diagnostic solutions.

A few of the leading players in the market are Abbott Laboratories, Quest Diagnostics, Eurofins Scientific, SGS Group, Bureau Veritas, ALS Limited, and Intertek Group.