- Healthcare Services

- Laboratory Management Services Market

Laboratory Management Services Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Laboratory Management Services Market by Component (Software and Services), by Deployment (On-premise, Web Hosted, and Cloud-based), by End User (Life Science Institutes & Laboratories, Clinical Research Organizations (CROs), Chemical & Petrochemical Industries, Food & Beverages and Agriculture, and Others), and Regional Analysis from 2026 to 2033.

Laboratory Management Services Market Share and Trend Analysis

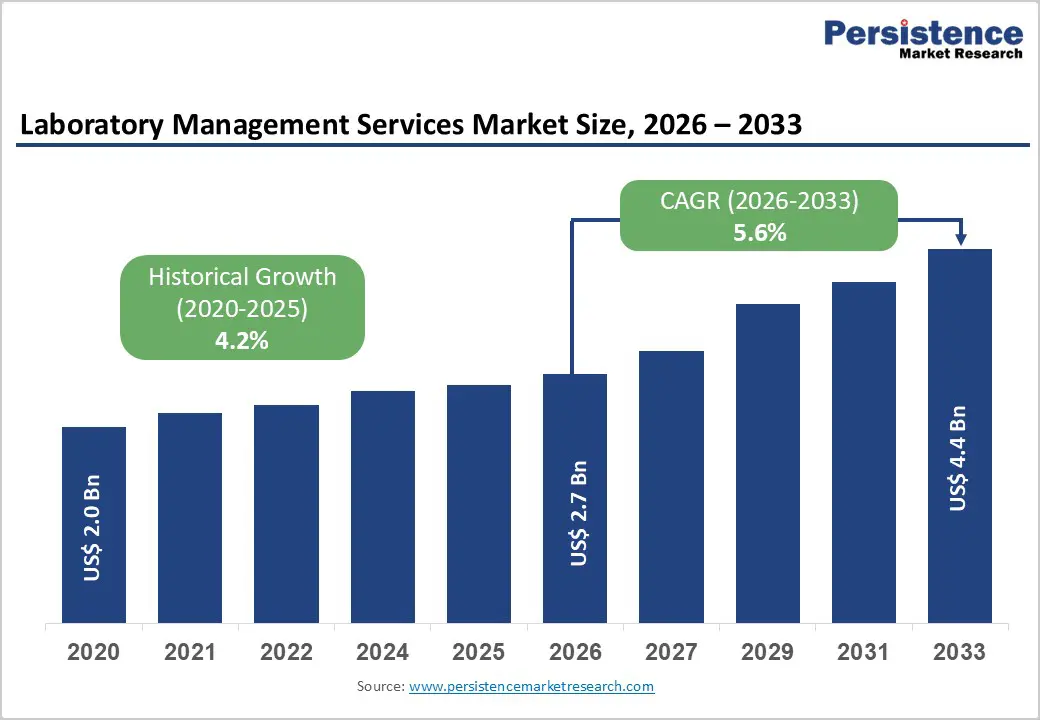

The global laboratory management services market size is estimated to grow from US$ 2.7 Bn in 2026 to US$ 4.4 Bn by 2033. The market is projected to record a CAGR of 5.6% during the forecast period from 2026 to 2033.

Global demand for laboratory management services is increasing steadily, driven by rising diagnostic and analytical workloads, expansion of preventive healthcare programs, and growing reliance on digital, data-driven laboratory operations. Hospitals, diagnostic laboratories, research institutes, and industrial labs are increasingly adopting laboratory management solutions to improve operational efficiency, ensure data accuracy, and support regulatory compliance. Aging populations, higher prevalence of chronic diseases, and expanding screening programs for infectious and metabolic disorders are significantly increasing test volumes worldwide, placing pressure on laboratories to optimize workflows and turnaround times. Laboratory management services are widely deployed across clinical, research, and industrial environments to enhance sample tracking, automate processes, reduce pre-analytical and post-analytical errors, and improve overall productivity. Growing emphasis on standardization, quality assurance, and laboratory accreditation is accelerating adoption, particularly as healthcare systems focus on patient safety and outcome-driven diagnostics. Technological advancements in software platforms, analytics, interoperability, and cloud deployment are further enhancing system capabilities and usability. In parallel, strengthening healthcare infrastructure in emerging economies and rising investments in diagnostic and research capacity are reinforcing sustained global demand for laboratory management services.

Key Industry Highlights

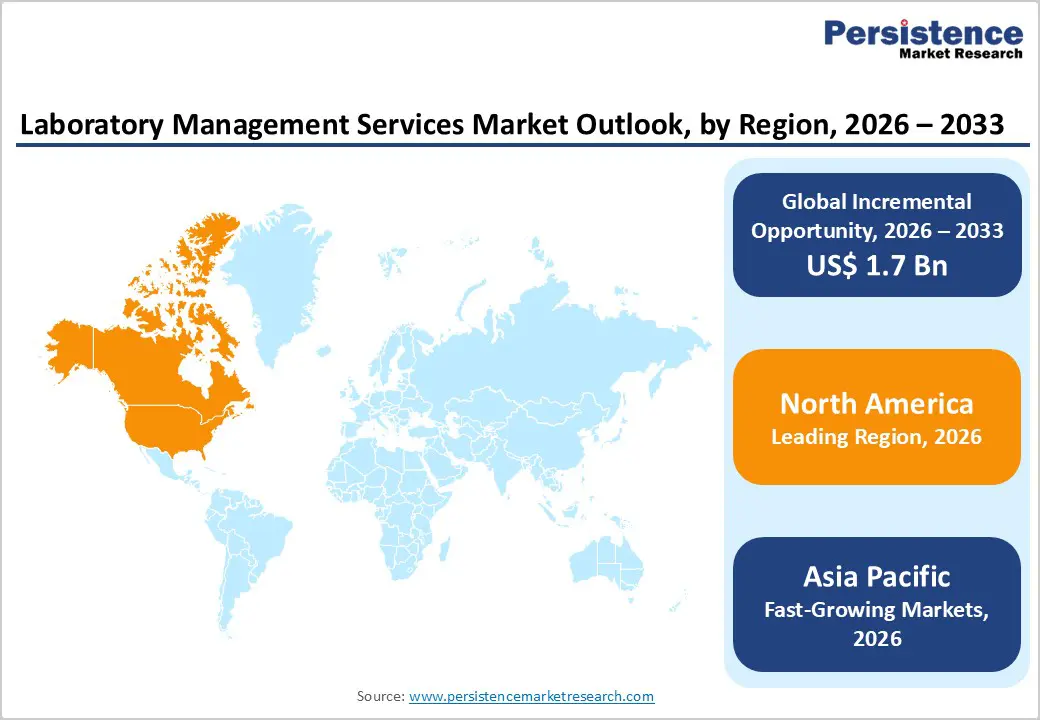

- Leading Region: North America holds the largest share at 47.3%, supported by advanced healthcare infrastructure, high diagnostic and research activity, strong regulatory frameworks, and widespread adoption of laboratory automation and informatics solutions.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace due to rapid healthcare infrastructure development, rising disease burden, increasing diagnostic awareness, and growth of private hospitals, laboratories, and CROs.

- Leading Component Segment: Software dominates the market due to its central role in workflow automation, data integrity, regulatory compliance, and integration with laboratory instruments and enterprise systems.

- Fastest-Growing Component Segment: Services are growing rapidly as laboratories increasingly outsource implementation, validation, customization, and ongoing system support to manage rising operational complexity.

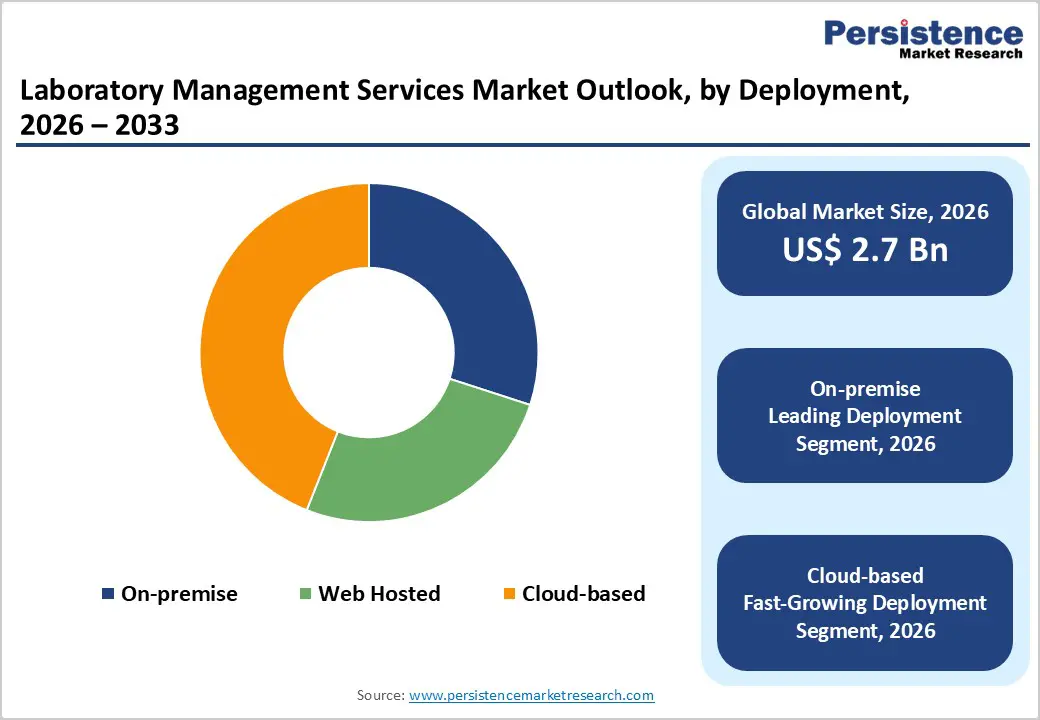

- Leading Deployment Segment: On-premise remains the top segment, driven by the need for greater control over sensitive laboratory data, seamless integration with existing instruments and legacy systems, and reliable performance in high-volume diagnostic environments. Fastest-Growing Deployment Segment: Cloud-based solutions are scaling rapidly as laboratories seek flexible, scalable, and cost-efficient platforms to manage rising testing volumes. Growing investments in automation, multi-site laboratory networks, and remote data access, along with lower infrastructure requirements and faster deployment, are accelerating adoption of cloud-based laboratory management services.

| Global Market Attributes | Key Insights |

|---|---|

| Laboratory Management Services Market Size (2026E) | US$ 2.7 Bn |

| Market Value Forecast (2033F) | US$ 4.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Dynamics

Driver – Increasing Diagnostic Workloads, Digital Transformation of Laboratories, and Compliance Requirements

Growth momentum is strongly influenced by the rapid increase in diagnostic and analytical workloads across clinical, research, and industrial laboratories. Rising incidence of chronic diseases, infectious outbreaks, and preventive health screening programs has significantly expanded test volumes, placing pressure on laboratories to manage samples, data, and workflows more efficiently. To address this complexity, laboratories are increasingly adopting management services that support automation, standardization, and real-time visibility across operations. Another key growth catalyst is the accelerated digital transformation of laboratory environments. Manual data entry, paper-based tracking, and siloed systems are being replaced by integrated platforms that improve traceability, reduce turnaround time, and minimize operational errors.

Laboratory management services enable centralized control over sample lifecycle management, instrument connectivity, quality assurance, and reporting. Regulatory and accreditation requirements further reinforce adoption. Compliance with standards related to data integrity, audit trails, and quality control has become non-negotiable for laboratories operating in regulated environments. Management services help laboratories meet these obligations consistently while supporting scalability. As diagnostic complexity rises and laboratories seek operational resilience, demand for robust laboratory management services continues to grow steadily.

Restraints – High Implementation Costs, Integration Complexity, and Skilled Workforce Gaps

Despite strong demand drivers, adoption is constrained by financial and operational challenges, particularly for small and mid-sized laboratories. Implementation of laboratory management services often involves substantial upfront costs related to software licensing, system configuration, validation, and staff training. Budget limitations can delay purchasing decisions, especially in publicly funded or resource-constrained healthcare systems. Integration complexity presents another barrier. Many laboratories operate with legacy instruments, fragmented IT systems, and customized workflows that require significant effort to harmonize with modern management platforms. Data migration, interoperability issues, and temporary workflow disruptions during deployment can affect productivity, discouraging rapid adoption.

In addition, effective utilization of laboratory management services depends on skilled personnel capable of system administration, data interpretation, and compliance management. Shortages of trained laboratory informatics professionals, particularly in emerging markets, limit the ability of organizations to fully leverage these solutions. Resistance to workflow change among laboratory staff can further slow implementation. Collectively, cost pressures, technical complexity, and human resource limitations restrict adoption rates in certain laboratory environments, despite the long-term efficiency benefits offered by management services.

Opportunity – Expansion of Decentralized Testing, Cloud Adoption, and Emerging Laboratory Ecosystems

Substantial growth opportunities are emerging from the shift toward decentralized and distributed diagnostic models. Expansion of point-of-care testing, satellite laboratories, and multi-site research operations has increased the need for centralized digital oversight and remote data access. Laboratory management services are increasingly positioned as essential infrastructure to coordinate workflows, ensure consistency, and maintain quality across geographically dispersed facilities. Cloud-based deployment models present additional opportunity by reducing infrastructure costs, improving scalability, and enabling faster system upgrades. Laboratories seeking flexible solutions that support remote collaboration and real-time analytics are accelerating cloud adoption, particularly in private diagnostics and contract research settings.

Emerging economies across Asia Pacific, Latin America, and the Middle East represent high-growth potential as investments in healthcare infrastructure, pharmaceutical manufacturing, and clinical research continue to rise. New laboratories in these regions are more inclined to adopt modern management systems from inception, bypassing legacy constraints. Opportunities also exist in specialized domains such as genomics, biobanking, and personalized medicine, where data complexity is high. Strategic partnerships, training initiatives, and modular service offerings can further unlock long-term growth potential.

Category-wise Analysis

By Component, Software Leads Due to Workflow Automation, Data Integrity, and Regulatory Compliance

Software is projected to dominate the global laboratory management services market in 2026, accounting for a revenue share of 42.0%. This leadership is driven by the critical role of laboratory management software in streamlining workflows, ensuring data accuracy, and supporting regulatory compliance across clinical, research, and industrial laboratories. Software platforms enable centralized sample tracking, test scheduling, result validation, audit trails, and real-time data access, which are essential for managing rising diagnostic and research workloads. Increasing adoption of automation, digital reporting, and analytics-driven decision-making further strengthens demand. Laboratories are also prioritizing software solutions that integrate seamlessly with analyzers, electronic health records (EHRs), and enterprise resource planning (ERP) systems to reduce manual errors and improve turnaround times. Additionally, stringent regulatory requirements related to data traceability, quality assurance, and laboratory accreditation continue to reinforce the dominance of software solutions within laboratory management services.

By Deployment, On-premise Leads Due to Data Control, Customization, and Legacy System Integration

On-premise deployment is expected to dominate the global laboratory management services market in 2026, capturing a revenue share of 30.0%. This dominance is primarily attributed to the preference for greater control over sensitive laboratory data, system customization, and seamless integration with existing legacy infrastructure. Many large hospitals, reference laboratories, and regulated industrial labs rely on on-premise systems to meet strict internal IT policies and regional data sovereignty requirements. On-premise solutions also offer high reliability, consistent system performance, and direct compatibility with in-house instruments and automation platforms. Established laboratories with long-standing workflows continue to favor these deployments due to familiarity and reduced dependency on external networks. While cloud adoption is increasing, on-premise systems remain the preferred choice for high-throughput environments requiring stable performance, advanced customization, and full ownership of laboratory data assets.

By End User, Life Science Institutes & Laboratories Lead Due to High Testing Volumes and Research Intensity

Life science institutes & laboratories are projected to dominate the global laboratory management services market in 2026, accounting for a revenue share of 41.0%. This leadership is driven by intensive research activity, high sample throughput, and continuous demand for accurate data management across pharmaceutical, biotechnology, and academic research laboratories. These facilities handle complex workflows involving large datasets, multi-site collaborations, and strict compliance requirements, making laboratory management services essential. The growing focus on drug discovery, genomics, proteomics, and translational research further increases reliance on advanced laboratory software and services. Life science laboratories also require scalable systems to support evolving research protocols and regulatory audits. While CROs and industrial laboratories are expanding their adoption, life science institutes remain the largest contributors due to sustained R&D investments, long-term system usage, and the need for highly specialized laboratory management solutions.

Region-wise Insights

North America Laboratory Management Services Market Trends

North America is expected to dominate the global laboratory management services market with a value share of 47.3% in 2026, led primarily by the United States. The region benefits from a highly advanced healthcare and research ecosystem, with widespread adoption of digital laboratory solutions across hospitals, reference laboratories, pharmaceutical companies, and academic institutions. High diagnostic testing volumes, strong clinical research activity, and early adoption of automation technologies significantly support market growth. Regulatory frameworks emphasizing data integrity, quality control, and compliance with standards such as CLIA, CAP, and FDA guidelines further drive demand for robust laboratory management services.

Healthcare and research organizations in North America actively invest in software platforms that improve operational efficiency, reduce errors, and support interoperability with analyzers and health information systems. High healthcare expenditure, strong reimbursement structures, and mature IT infrastructure accelerate adoption. The presence of major market players, continuous innovation in analytics and AI integration, and growing demand for remote and hybrid laboratory operations reinforce North America’s leadership as the most mature and revenue-dominant regional market.

Europe Laboratory Management Services Market Trends

The Europe laboratory management services market is expected to grow steadily, supported by well-established healthcare systems and strong regulatory oversight across countries such as Germany, the U.K., France, Italy, and Spain. European laboratories place significant emphasis on data accuracy, process standardization, and compliance with stringent regulatory frameworks, including GDPR and medical device regulations. These factors drive consistent adoption of laboratory management software and associated services.

Rising aging populations across Europe contribute to increasing diagnostic testing volumes, particularly for chronic disease monitoring, oncology, and preventive healthcare. Public healthcare systems are increasingly digitizing laboratory operations to improve efficiency, transparency, and patient outcomes. Expansion of centralized diagnostic laboratories, reference labs, and cross-border research collaborations further supports market growth. Additionally, European laboratories are investing in automation and interoperability to reduce turnaround times and optimize resource utilization. Continuous modernization of laboratory infrastructure and a strong focus on quality assurance position Europe as a stable and steadily expanding regional market.

Asia Pacific Laboratory Management Services Market Trends

The Asia Pacific laboratory management services market is expected to register a relatively higher CAGR of around 7.6% between 2026 and 2033, driven by rapid healthcare infrastructure development and expanding diagnostic and research capabilities. Countries such as China, India, Japan, South Korea, and Australia are witnessing significant investments in hospital expansion, diagnostic laboratories, pharmaceutical manufacturing, and clinical research. Rising awareness of early disease detection and preventive healthcare is substantially increasing diagnostic testing volumes.

Growing adoption of digital laboratory solutions is helping facilities manage rising workloads efficiently while maintaining accuracy and compliance. Expansion of private hospitals, specialty clinics, and contract research organizations is improving market penetration. Cost-effective laboratory management solutions are gaining traction in emerging economies, while advanced institutions are adopting sophisticated platforms with analytics and cloud capabilities. Government initiatives to strengthen healthcare systems, coupled with increasing medical tourism and biopharmaceutical outsourcing, position Asia Pacific as the fastest-growing regional market for laboratory management services.

Market Competitive Landscape

The global laboratory management services market is highly competitive, with strong participation from companies such as Siemens AG, Genetic Technologies Inc, LabLynx Inc, Agilent Technologies, and Thermo Fisher Scientific Inc. These players leverage extensive global distribution networks, strong brand recognition, and diversified laboratory software and service portfolios to address the growing demand for efficient, compliant, and integrated laboratory operations across research, clinical, and industrial settings.

Their offerings emphasize system reliability, data integrity, regulatory compliance, workflow automation, scalability, and seamless integration with laboratory instruments, enterprise systems, and digital health infrastructures in hospitals, CROs, life science laboratories, and industrial labs. Continuous innovation in cloud deployment, analytics, interoperability, cybersecurity, and adherence to international laboratory and data standards remains critical for sustaining competitive positioning in the global laboratory management services market.

Key Industry Developments:

- In January 2026, Minaris, a global contract development and manufacturing organization (CDMO) specializing in cell and gene therapy (CGT) and multimodality biosafety testing, announced an enhancement of its Viral Clearance laboratory capabilities at its Philadelphia campus. The upgrade increases capacity to four advanced client suites, designed to support efficient operational execution and an improved client experience through the use of advanced digital tools, optimized workflows, and a newly designed facility layout.

- In March 2025, LabWare®, a global leader in Laboratory Information Management Systems (LIMS), expanded its SaaS portfolio with the introduction of LabWare ASSURE, complementing LabWare QAQC and LabWare GROW. This launch represents a significant evolution in laboratory informatics, providing laboratories with greater flexibility in how they deploy, scale, and manage informatics platforms while enhancing compliance, operational efficiency, and system accessibility.

- In March 2025, IQVIA Laboratories, a leading global provider of drug discovery and development laboratory services, announced the launch of Site Lab Navigator, an advanced solution suite designed to automate and streamline laboratory workflows for clinical trial sponsors and investigator sites.

Companies Covered in Laboratory Management Services Market

- Siemens AG

- Genetic Technologies Inc

- LabLynx Inc

- Agilent Technologies

- Thermo Fisher Scientific Inc.

- PerkinElmer Inc

- Creliohealth Inc

- Abbott Laboratories

- Labworks

- Accelerated Technology Laboratories Inc.

- Waters Corporation

- Autoscibes Informatics

- LabWare

- LabVantage Solutions

Frequently Asked Questions

The global laboratory management services market is projected to be valued at US$ 1.7 Bn in 2026.

Rising prevalence of chronic and lifestyle diseases requiring frequent blood tests, growing demand for point-of-care and minimally invasive sampling, technological advancements in microtainer designs improving ease and safety, and expanding adoption in paediatric, geriatric, and home healthcare settings.

The global laboratory management services market is poised to witness a CAGR of 5.7% between 2026 and 2033.

Integration of AI, machine learning, and cloud-based tracking solutions to enhance real-time instrument visibility, workflow efficiency, and predictive asset management.

Siemens AG, Genetic Technologies Inc, LabLynx Inc, Agilent Technologies, and Thermo Fisher Scientific Inc., are some of the key players in the body laboratory management services market.