- Advanced Materials

- India Bullet-Resistant Glass Market

India Bullet-Resistant Glass Market Size, Share, and Growth Forecast 2026 - 2033

India Bullet-Resistant Glass Market by Product Type (Polycarbonate Glass, Acrylic Glass, Glass-clad Polycarbonate, Poly-vinyl Butyral (PVB), Laminated Bullet Proof Glass, and Others), BRG Class (BR1, BR2, BR3, BR4, BR5, BR6, BR7, and Others), Application (Bank Security Systems, Cash-in-Transit Vehicles, Defense & VIP Vehicles, Government & Law Enforcement, and Others), and Regional Analysis for 2026 - 2033

India Bullet-Resistant Glass Market Size and Share Analysis

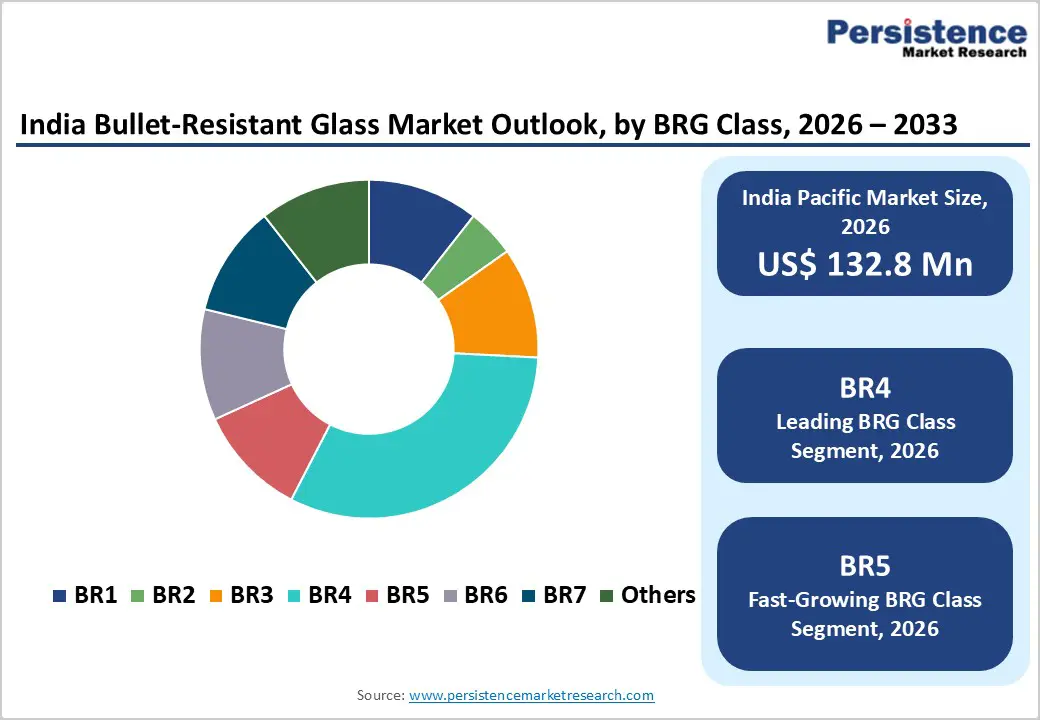

India bullet-resistant glass (BRG) market size is likely to be valued at US$ 132.8 million in 2026 and is projected to reach US$ 302.9 million by 2033, growing at a CAGR of 12.5% between 2026 and 2033.

Rise in geopolitical tensions, exponential growth in defense spending, and intensifying urbanization, which create demand for high-security commercial and residential applications, are some prominent factors driving the demand for bullet-resistant glass. India's cumulative defense spending is projected to reach $543.1 billion during 2026-30, with acquisition budgets accounting for approximately 31% of total expenditure.

Key Market Highlights

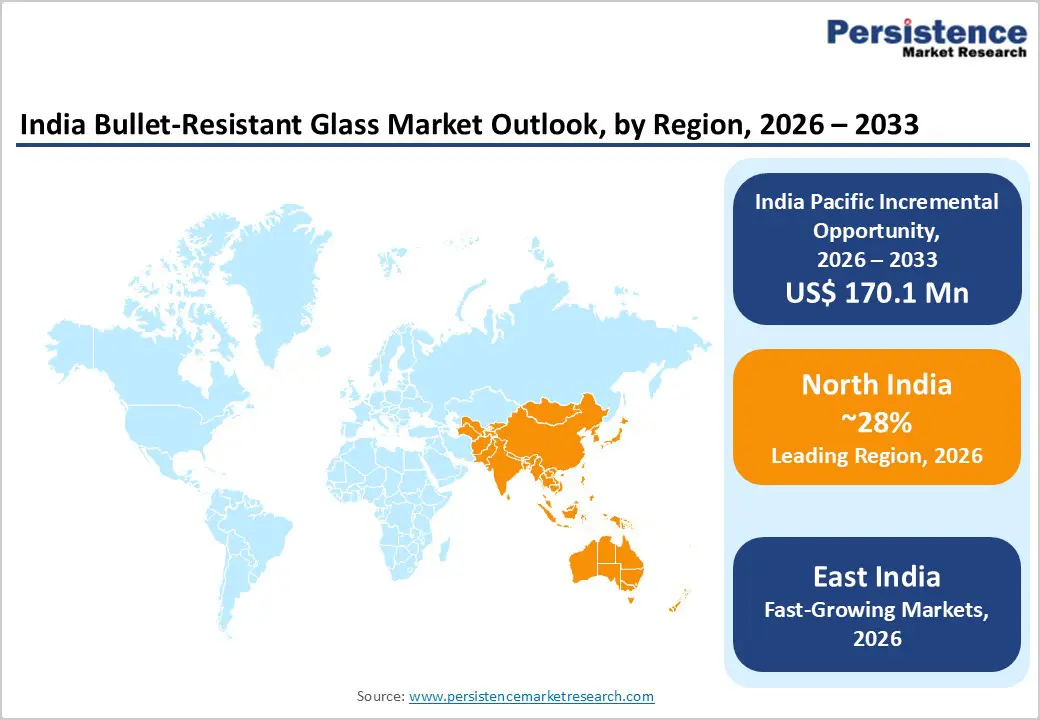

- Leading Region: North India is dominant and is poised to account for a 38% share, due to its concentration of defense bases, paramilitary deployments, border security infrastructure, and central government institutions, driving sustained and high-volume demand.

- Fastest Growing Region: East India is the fastest-growing region, supported by rising investments in border infrastructure, internal security modernization, and increased deployment of armored vehicles and fortified public facilities.

- Dominant Product Type: Laminated Bullet-Proof Glass commands 38% market share across all applications, driven by superior ballistic performance, optical clarity, established manufacturing infrastructure, and widespread institutional adoption.

- Dominant BRG Class: BR4 Classification glass achieves the highest growth rates, capturing 34% market value through optimal positioning between comprehensive threat coverage and cost-effectiveness.

- Key Market Opportunity: Armored Vehicle Manufacturing Expansion driven by government defense contracts and domestic manufacturing initiatives through AVNL-MIDHANI partnerships creates sustained multi-year procurement pipelines for integrated ballistic glazing systems across defense, paramilitary, and internal security vehicle fleets.

| Key Insights | Details |

|---|---|

| India Bullet-Resistant Glass Market Size (2026E) | US$ 132.8 Mn |

| Market Value Forecast (2033F) | US$ 302.9 Mn |

| Projected Growth CAGR (2026 - 2033) | 12.5% |

| Historical Market Growth (2020 - 2025) | 10.1% |

Market Dynamics

Drivers - Rising Defense Modernization and Internal Security Spending Driving Demand for BRG

India’s robust increase in defense and internal security expenditure is a major growth driver for the bullet-resistant glass market, reflecting the country’s strategic focus on force modernization and threat preparedness. Defense spending has expanded significantly from INR2.53 lakh crore in 2013-14 to INR6.81 lakh crore in 2025-26, underscoring long-term commitments to strengthen border security, counter cross-border terrorism, and address complex geopolitical challenges along multiple fronts. This sustained budgetary growth is translating into higher procurement of armored military vehicles, protected patrol boats, surveillance towers, and fortified command infrastructure, all of which require advanced ballistic glazing solutions to ensure personnel safety without compromising visibility and situational awareness.

Policy reforms by the Ministry of Defense have structurally strengthened demand for domestically manufactured bullet-resistant glass. The earmarking of 75% of the total acquisition budget for indigenous procurement, up from 58% in 2020-21, has created strong incentives for local manufacturers to scale production capacity, invest in advanced lamination technologies, and meet stringent military standards. Emergency funding of approximately $6 billion (INR 500 billion) allocated for weapons and equipment replenishment following Operation Sindoor has accelerated short-term procurement cycles. This has directly boosted demand for bullet-resistant components across armored vehicles, border outposts, police and paramilitary installations, and critical urban security infrastructure, reinforcing the market’s growth outlook over the medium to long term.

VIP Security Infrastructure and Law Enforcement Modernization

The Indian government's comprehensive VIP security framework, administered through the Special Protection Group (SPG), Central Reserve Police Force (CRPF), and state police agencies, extends security coverage across multiple threat categories, from SPG protection for the Prime Minister to Z+, Z, Y+, Y, and X categories for political leaders, business executives, and high-profile personalities. This tiered security architecture necessitates specialized ballistic protection across residential installations, vehicle fleets, and operational centers.

Recent large-scale security implementations, including the Mahakumbh 2025 event deploying 37,000 police personnel with 2,750 AI-powered CCTV cameras and 123 strategically positioned watchtowers, underscore the institutional commitment to advanced protective infrastructure. The proliferation of smart cities across India, with the Smart Cities Mission mobilizing INR2,01,981 crore investment and completing 7,555 projects, has necessitated the integration of bullet-resistant architectural elements in critical infrastructure hubs, financial centers, and government administrative zones.

Restraints - High Manufacturing Costs and Import Dependency

The production of certified bullet-resistant glass entails sophisticated, multi-layered fabrication processes that require advanced interlayer materials, precision lamination technology, and rigorous ballistic testing protocols. The requisite raw materials, particularly high-specification polyvinyl butyral (PVB) interlayers and specialty resins, involve substantial import costs given limited domestic production capacity. Manufacturing facilities must maintain compliance with stringent international standards, including EN 1063, NIJ Standards, and UL 752 certifications, necessitating capital-intensive testing infrastructure and quality assurance systems.

This technological barrier restricts market entry to established players with significant financial reserves, constraining production scaling and limiting cost optimization opportunities for emerging manufacturers. Import dependency on premium-grade materials inflates production costs by 15-25%, reducing profit margins and creating pricing accessibility challenges for smaller institutional buyers and regional security deployments.

Regulatory Compliance and Standardization Challenges

India's multifaceted regulatory landscape encompasses compliance with Bureau of Indian Standards (BIS) certification mandates (following Quality Control Orders enacted March 24, 2023), state-level traffic regulations, and industry-specific procurement protocols. Different applications, automotive, architectural, banking, and defense, operate under distinct regulatory frameworks, requiring manufacturers to maintain parallel production lines and testing certifications. The Motor Vehicle Act amendments requiring laminated safety glass for vehicle windshields, combined with the Central Motor Vehicle Regulations specifying minimum visible-light transmission standards, create configuration constraints for dual-purpose security glazing solutions.

Inconsistent enforcement across states, prolonged certification timelines (typically 4-6 months for BIS approval), and frequent regulatory revisions create operational inefficiencies and supply chain disruptions that constrain market expansion, particularly for small-to-medium manufacturers lacking dedicated compliance infrastructure.

Opportunity - Armored Vehicle Sector Expansion and Defense Modernization

India's armored vehicle market, projected to grow steadily amid escalating defense budgets and Make in India manufacturing initiatives, presents substantial opportunities for integrating bullet-resistant glass. The Ministry of Defense's contract awards to indigenous manufacturers, including Mahindra Defence Systems' LSV (Light Specialist Vehicle) order valued at USD 146 million (INR 1,056 crore) with delivery extending through 2025, establishes robust demand pipelines.

The government's strategic focus on manufacturing 1,300 light specialist vehicles and on the concurrent development of infantry combat vehicles, MRAPs, and support vehicles through domestic partnerships (including the January 2024 AVNL-MIDHANI MoU for vehicle development at the Jabalpur factory) creates multi-year procurement windows for ballistic glazing suppliers. These initiatives align with geopolitical imperatives and force modernization requirements, generating consistent revenue streams for established BRG manufacturers and attracting new entrants to the defense supply chain ecosystem.

Banking and Cash-In-Transit Security Infrastructure Modernization

The resilience of India's banking sector, with net profits rising from INR1.05 lakh crore in FY 2022-23 to INR1.78 lakh crore in FY 2024-25, demonstrates robust institutional capital deployment toward infrastructure modernization. Reserve Bank of India (RBI) regulatory mandates requiring specialized cash vans with separate passenger and cash compartments, reinforced doors, and ballistic glazing systems represent standardized procurement requirements across authorized cash management service providers.

The current fleet of at least 300 specially fabricated cash vans per service provider, coupled with ongoing fleet expansion and replacement cycles, creates sustained demand for BR-classified security glazing. Emerging security threats and the proliferation of organized financial crimes necessitate continuous upgrades to protective glazing standards, particularly for BR4-BR6 classification levels in high-value cash transit operations across metropolitan centers and tier-1 cities with dense financial infrastructure.

Category-wise Analysis

Product Type Insights

Laminated bullet-proof glass emerges as the dominant product segment, commanding approximately 38% of the market share, driven by its versatility across institutional, commercial, and defense applications. This leadership position reflects the material's superior ballistic performance across all threat levels (BR1 through BR7 classifications), optical clarity enabling unobstructed visibility in critical applications, and established manufacturing infrastructure among established Indian glass processors. Laminated Bullet-Proof Glass comprises multiple bonded layers with Poly-vinyl Butyral (PVB) interlayers manufactured according to EN 1063 and IS 2553 specifications, providing superior impact absorption and fragmentation containment compared to monolithic alternatives.

The dominance of this segment is substantiated by widespread adoption across RBI-regulated cash transit vehicles, defense and VIP security installations, and government administrative complexes nationwide. Manufacturers including Saint-Gobain India Pvt. Ltd., FG Glass Industries, and Duratuf Glass Industries maintain substantial production capacities for laminated variants, with Saint-Gobain India operating advanced lamination facilities at its Sriperumbudur complex (featuring multiple lamination and insulated glass unit production lines capable of handling jumbo glass sizes).

BRG Class Analysis

BR4 Classification dominates market demand, representing approximately 34% market share, reflecting its optimal positioning between comprehensive threat coverage and cost-effectiveness. This classification level, tested in accordance with EN 1063 standards using rifle ammunition (7.62 mm NATO rounds) at an impact velocity of 950 meters per second, provides robust protection suitable for armored VIP vehicles, high-security government installations, and premium commercial applications. The BR4 segment benefits from institutional procurement preferences that balance security requirements with economic constraints; it effectively protects against conventional small-arms fire common in security threats across India while maintaining reasonable transparency and structural integrity for architectural integration.

The adoption rate of BR4-classified systems accelerated significantly following 2024-2025 security incidents, heightened terrorism threat assessments, and government directives mandating upgraded protective standards for vulnerable institutions. Lower classifications (BR1-BR3) serve specialized applications in basic security infrastructure and residential installations with limited threat exposure, while higher classifications (BR5-BR7) remain concentrated in elite defense installations and ultra-high-security government facilities requiring maximum ballistic resistance against military-grade weaponry.

Application Insights

Defense and VIP Vehicles command the largest application segment, accounting for approximately 42% of total market value, driven by India's escalating geopolitical security imperatives and the government's institutional commitment to protecting strategic personnel. This segment encompasses specialized glazing systems integrated into armored personnel carriers, ministerial vehicles under SPG or CRPF protection, and military tactical vehicles engaged in border security operations and counter-insurgency missions.

The segment's dominance reflects sustained demand from defense procurement agencies, government motor pool modernization programs, and continuous fleet replacement cycles driven by vehicle lifecycle depreciation and capability enhancement requirements. Cash-in-Transit Vehicles represent the second-largest application domain, capturing approximately 28% of market share, encompassing RBI-compliant security vans operated by authorized cash management service providers and financial institutions' internal transportation fleets.

Regional Insights

North India Bullet-Resistant Glass Trends

North India is estimated to account for approximately 38% of the India bullet-resistant glass market in 2026, driven by its strategic importance in national defense, internal security, and governance. The region hosts a high concentration of army bases, paramilitary forces, border security installations, and central government institutions, resulting in sustained demand for ballistic glazing across armored vehicles, fortified check posts, surveillance towers, and administrative buildings.

States such as Delhi NCR, Uttar Pradesh, Punjab, Haryana, and Jammu & Kashmir are focal points for security-related procurement, supported by frequent upgrades to military and police infrastructure. In addition, North India’s dense urban population and concentration of VIP movement sustain demand for armored civilian vehicles and protected transport solutions. The region also benefits from proximity to defense public sector units, system integrators, and testing facilities, enabling faster procurement cycles and greater customization. Strong policy support for indigenous manufacturing further reinforces regional leadership.

West India Bullet-Resistant Glass Trends

West India exhibits relatively stagnant growth in the bullet-resistant glass market, reflecting a mature demand profile and limited exposure to large-scale defense procurement compared to other regions. Maharashtra and Gujarat account for the bulk of regional demand, primarily driven by urban security applications, financial institutions, commercial buildings, ports, and premium automotive armoring. While metropolitan centers such as Mumbai generate consistent demand for armored cash-in-transit vehicles, bank security, and VIP transport, much of this consumption is replacement-driven rather than expansionary. Industrial and commercial projects in the region often prioritize cost efficiency, limiting widespread adoption of high-spec ballistic glazing outside critical installations.

Additionally, defense and paramilitary deployments are comparatively lower than in border-focused northern and eastern regions, reducing the frequency of large government tenders. Although Gujarat’s industrial corridors, ports, and energy assets create episodic demand for protective glazing, procurement cycles tend to be conservative and supplier-consolidated. Consequently, West India maintains a steady but low-growth trajectory, contributing stable volumes to the national market without significantly increasing its overall share.

East India Bullet-Resistant Glass Trends

East India is emerging as the fastest-growing region, with projected CAGR of approximately 13.5% through 2033, supported by rising defense infrastructure investments, internal security modernization, and a lower base of historical adoption. States such as West Bengal, Odisha, Bihar, Jharkhand, and the northeastern region are witnessing increased spending on border roads, surveillance outposts, police mobility, and fortified government facilities.

Strategic emphasis on strengthening eastern borders and improving connectivity has accelerated deployment of armored vehicles and protected installations, directly increasing demand for ballistic glazing. Growing urbanization and industrial development in cities such as Kolkata, Bhubaneswar, and Guwahati are driving incremental adoption of bullet-resistant glass in public infrastructure and law enforcement facilities. As procurement intensity increases from a relatively small base, growth rates remain structurally higher than the national average.

Competitive Landscape

The India Bullet-Resistant Glass market exhibits a moderately consolidated competitive structure with established market leaders controlling a significant share through integrated manufacturing capabilities, comprehensive product portfolios, and established distribution networks. Market concentration reflects substantial capital requirements for modern manufacturing facilities, skilled technical workforce development, and rigorous quality certification infrastructure. Saint-Gobain India Pvt. Ltd. maintains market leadership with a comprehensive glass solutions portfolio, including specialized ballistic protection systems, supported by advanced research facilities and established institutional customer relationships.

Emerging manufacturers, including Duratuf Glass Industries, FG Glass Industries, and Chandra Lakshmi Safety Glass, pursue focused specialization strategies targeting specific application niches, including armored vehicle supply contracts and regional government security infrastructure projects. Market participants differentiate through technology capabilities (including advanced interlayer formulations and multi-layer bonding innovations), certification portfolio breadth (covering EN 1063, NIJ, UL 752, and BIS standards), and customer service specialization.

Key Market Developments:

- In March 2025, Saint-Gobain India Pvt. Ltd. announced an ambitious tripling of organizational revenue to INR36,000 crore by 2032 through INR 6,000-8,000 crore capital expenditure program encompassing greenfield manufacturing expansion in glass wool, stone wool, and advanced laminated glass production facilities in Tamil Nadu, supported by strategic acquisition portfolio development in ceramics and infrastructure-aligned materials sectors.

- In January 2024, VNL-MIDHANI Partnership for Armored Vehicle Development Vehicle Factory Jabalpur established collaborative manufacturing partnership between AVNL (Armoured Vehicles Nirvana Ltd) and MIDHANI (Mishra Dhatu Nigam Limited) for advanced armored vehicle production, creating substantial integrated supply chain demand for ballistic-classified glazing systems across commercial and defense applications.

Companies Covered in India Bullet-Resistant Glass Market

- Saint-Gobain India Pvt. Ltd.

- Asahi India Glass Limited

- Gujarat Guardian Ltd.

- Duratuf Glass Industries (P) Ltd.

- Jeet & Jeet Glass and Chemicals Pvt. Ltd.

- Gold Plus Glass Industry Limited

- FG Glass Industries Pvt. Ltd.

- Chandra Lakshmi Safety Glass Ltd.

- Fuso Glass India Pvt. Ltd.

- Art-n-Glass Inc.

- Gurind India Pvt. Ltd.

- Nippon Sheet Glass Co. Ltd.

- Smartglass International

- Varna Group

Frequently Asked Questions

India Bullet-Resistant Glass market is projected to reach US$ 302.9 billion by 2033, growing from US$ 132.8 billion in 2026 at a compound annual growth rate of 12.5%.

Key demand drivers include escalating defense expenditures, comprehensive VIP security infrastructure modernization, ash-in-transit vehicle fleet modernization complying with RBI security mandates, and government Make in India procurement policies emphasizing 75% domestic supplier allocation.

BR4 Classification dominates market demand, representing approximately 34% market share, reflecting an optimal balance between comprehensive threat protection against conventional small arms ammunition and cost-effectiveness enabling broad institutional adoption across government facilities, armored vehicles, and commercial security applications nationwide.

North India to dominate India BRG market, driven by its high concentration of defense installations, paramilitary forces, border security infrastructure, and central government institutions.

Armored Vehicle Manufacturing Expansion driven by government defense contracts including Mahindra Defence Systems LSV order and AVNL-MIDHANI collaborative manufacturing partnerships creates sustained multi-year procurement pipelines for integrated ballistic glazing systems across military, paramilitary, and internal security vehicle fleets with escalating threat level specifications.

Leading market participants include Saint-Gobain India Pvt. Ltd. Asahi India Glass Limited, Gujarat Guardian Ltd., Duratuf Glass Industries, FG Glass Industries, and Chandra Lakshmi Safety Glass, among others.