- Sporting Goods & Equipment

- Home Fitness Equipment Market

Home Fitness Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Home Fitness Equipment Market by Product Type (Punching Bags, Treadmills, Dumbbells, Cycles, Weightlifting Benches, Resistance Bands, Others), End User (Male, Female), Application (Cardiovascular Training, Strength Training, Others), Sales Channel (Online, Offline), and Regional Analysis for 2026 - 2033

Home Fitness Equipment Market Size and Trend Analysis

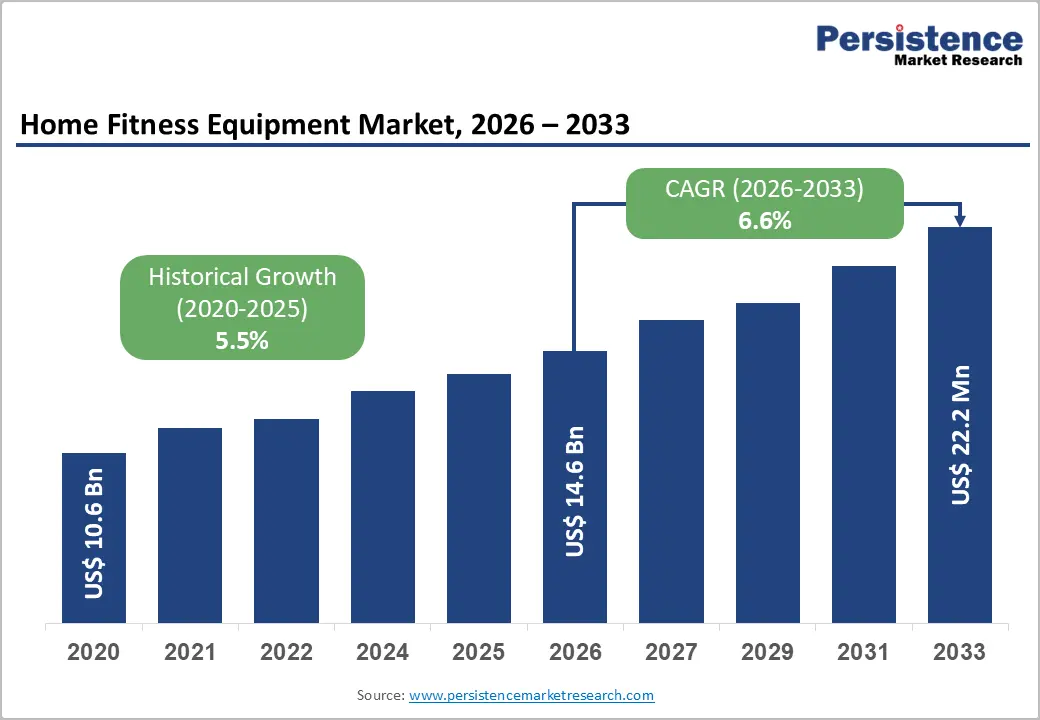

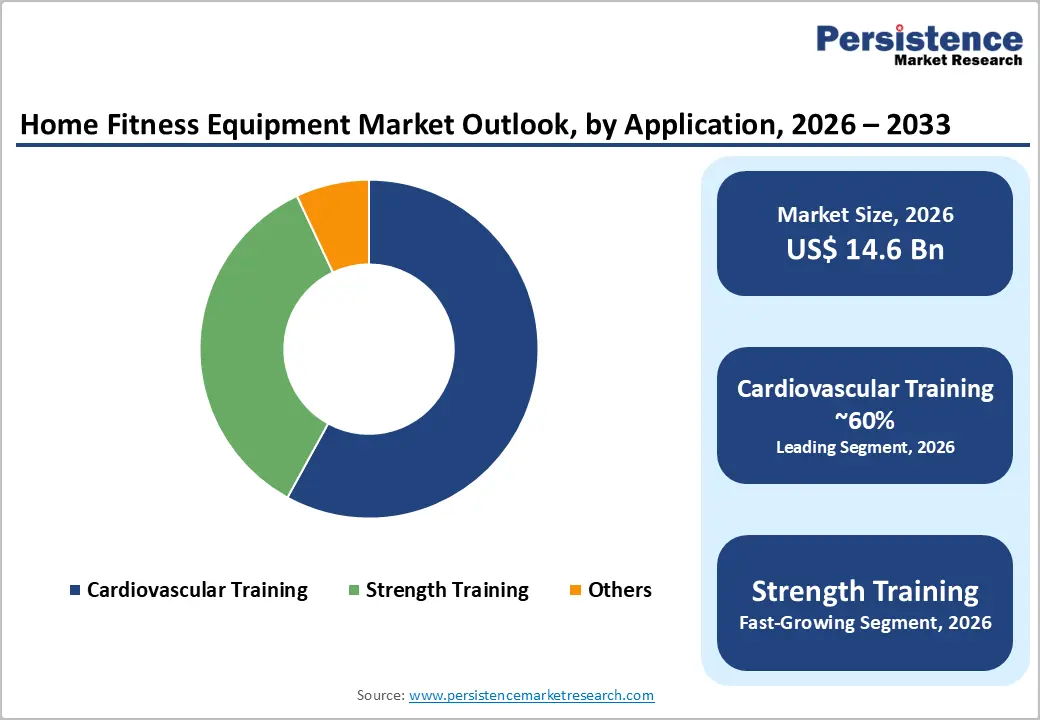

The global home fitness equipment market size is expected to be valued at approximately US$ 14.6 Bn in 2026 and is projected to reach US$ 22.2 Bn by 2033, growing at a CAGR of 6.2% between 2026 and 2033. This sustained growth is driven by the structural shift in consumer fitness behavior toward home-based exercise routines, the rising global prevalence of lifestyle diseases reinforcing preventive health investment, and the proliferation of digital fitness platforms that are increasing home gym equipment utilization rates and purchase intent.

Key Market Highlights

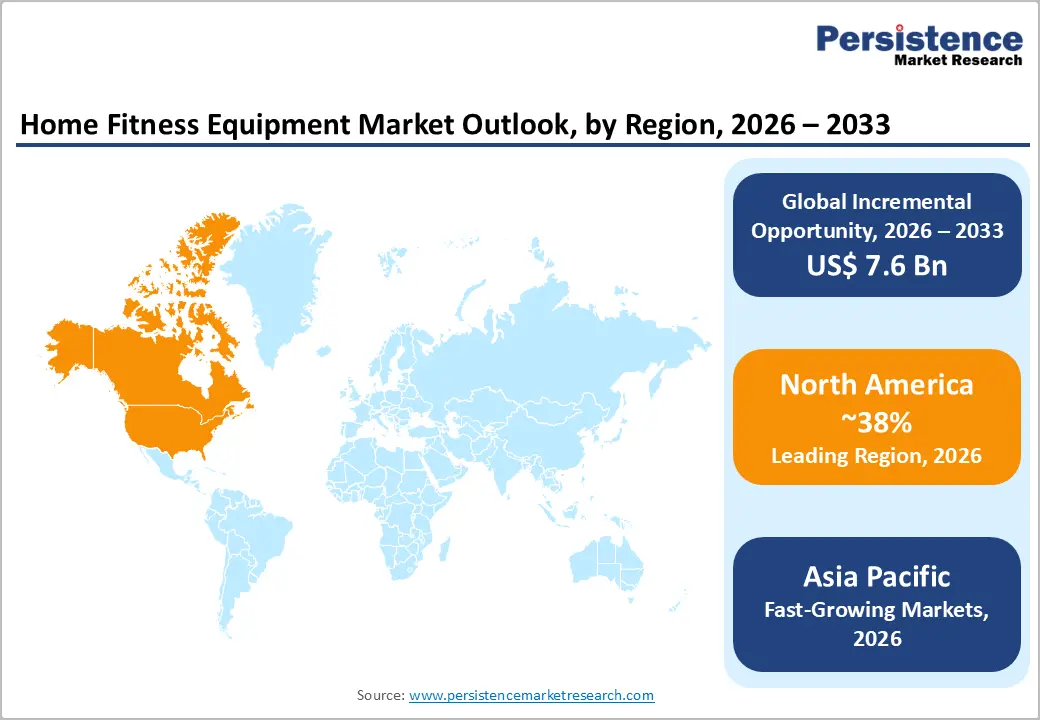

- Leading Region – North America leads the global home fitness equipment market with approximately 38% revenue share in 2025, anchored by U.S. consumers' high disposable income, established home gym culture, and the concentrated presence of leading connected fitness brands including Peloton and NordicTrack.

- Fastest Growing Region – Asia Pacific is projected to register the highest CAGR through 2033, driven by India's first-time buyer surge at 8.1% CAGR, China's Healthy China 2030 fitness investment, and explosive e-commerce channel growth enabling fitness equipment purchases across markets with limited specialty retail access.

- Dominant Segment – Treadmills lead the product type segment with approximately 28% market share in 2025, entrenched as the most universally recognized home fitness product globally, with connected models from NordicTrack and Peloton elevating average selling prices from USD 500–1,000 to USD 1,500–4,000.

- Fastest Growing Segment – Strength training equipment is the fastest-growing application segment, driven by ACSM's consistent top-trends ranking, social media fitness culture normalizing home weightlifting, and resistance bands and dumbbells' compact footprint making them the highest-penetration home fitness category in urban apartments.

- Key Market Opportunity: Asia Pacific's 3.5 billion-strong middle class by 2030 (ADB projection) largely first-time home fitness equipment buyers combined with Tmall, JD.com, Flipkart, and Lazada's expanding fitness category investment, creates the largest underpenetrated consumer acquisition opportunity in the global home fitness equipment market.

DRO Analysis

Market Growth Drivers

Rising Global Prevalence of Lifestyle Diseases Is Creating Structural, Health-Driven Demand for Home Fitness Equipment

The escalating global burden of non-communicable diseases directly linked to physical inactivity including cardiovascular disease, type 2 diabetes, obesity, and hypertension is generating sustained health-driven consumer investment in home fitness equipment as a preventive healthcare tool.

The WHO's Global Action Plan on Physical Activity 2018–2030 documents that physical inactivity is the fourth leading risk factor for global mortality, responsible for approximately 3.2 million deaths annually, and calls for a 15% relative reduction in physical inactivity by 2030 a public health imperative that is driving national physical activity promotion campaigns across high- and middle-income countries.

Digital Fitness Integration and Connected Equipment Are Elevating Average Transaction Values and Driving Upgrade Cycles

The integration of interactive digital content, live instructor-led sessions, and AI-powered performance coaching into home fitness equipment is creating a premium product category connected fitness equipment that commands significantly higher purchase prices and generates recurring subscription revenue streams that sustain consumer engagement and drive equipment upgrade cycles.

The International Health, Racquet and Sportsclub Association (IHRSA) reports that digital fitness content consumers demonstrate significantly higher frequency of home equipment use than non-connected equipment owners validating the commercial logic of digital integration as both a revenue uplift and a brand loyalty mechanism that sustains repeat purchase intent among the growing connected fitness consumer cohort.

Market Restraints

Post-Pandemic Demand Normalization and Gym Reopening Are Creating Cyclical Headwinds for Home Equipment Adoption

The home fitness equipment market experienced an extraordinary demand surge in 2020–2021 driven by global gym closures with Allied Market Research noting that some categories saw 170% year-over-year revenue growth at peak pandemic demand followed by significant demand normalization as commercial gyms reopened and consumers partially returned to shared fitness facilities.

This post-pandemic inventory correction cycle, which particularly affected large cardiovascular equipment categories including treadmills and stationary cycles, is suppressing replacement purchase demand among the large cohort of consumers who purchased equipment during the pandemic surge and have not yet reached their natural replacement horizon.

Space Constraints and High Cost of Premium Equipment Limit Addressable Market Penetration in Urban Emerging Markets

The structural space constraint of urban apartment living particularly prevalent across Asia Pacific's rapidly growing megacities where average apartment sizes in cities including Shanghai, Mumbai, and Jakarta frequently fall below 60 square meters limits the feasibility of full home gym configurations that require floor space for treadmills, cycles, and weightlifting equipment.

Premium connected fitness equipment with Peloton's bike starting above USD 1,200 also exceeds the discretionary consumer electronics budget of the large middle-class cohort in income-constrained emerging markets, constraining the total addressable market for premium home fitness products below the levels suggested by total population statistics.

Market Opportunities

Strength Training Equipment Is the Fastest-Growing Application Segment, Driven by Evidence-Based Fitness Science and Social Media Influence

Strength training has experienced a profound consumer popularity resurgence driven by a convergence of clinical evidence, social media fitness culture, and aging demographics that is making dumbbells, resistance bands, and weightlifting benches among the fastest-growing individual product categories within the home fitness equipment market.

The American College of Sports Medicine (ACSM) ranks strength training as one of its top fitness trends for five consecutive years in its annual worldwide survey, and peer-reviewed research including studies published in the British Journal of Sports Medicine has documented strength training's benefits for metabolic health, bone density, and longevity that resonate with both younger athletes and older adults seeking functional fitness maintenance.

For manufacturers, strength training's home fitness appeal is amplified by its compact equipment footprint dumbbells and resistance bands require minimal space making it the highest-penetration fitness category in urban apartment contexts that constrain large cardiovascular equipment adoption.

Asia Pacific's Rising Middle Class and Online Channel Growth Create the Market's Largest Underpenetrated Demand Opportunity

Asia Pacific is the fastest-growing regional home fitness equipment market, with the convergence of a rapidly expanding health-conscious middle class, improving digital infrastructure enabling online fitness content consumption, and the e-commerce channel's growing dominance in fitness equipment retail creating a high-growth opportunity for international and domestic equipment brands that invest in the region now.

The Asian Development Bank (ADB) projects that Asia's middle class will reach 3.5 billion people by 2030 many of whom are first-time fitness equipment buyers and Google Trends data consistently shows rising search volume for home fitness equipment terms across India, Vietnam, Indonesia, and the Philippines.

Category-wise Analysis

Product Type Insights

Treadmills lead the product type segment with approximately 28% market share in 2026, a position sustained by their status as the most universally understood, broadly marketed, and category-defining home fitness product globally representing the entry-point purchase for millions of first-time home gym buyers who equate cardiovascular training primarily with walking and running. Treadmills serve the full fitness spectrum from rehabilitation-pace walking to high-intensity interval running, making them the broadest-demographic-appeal home fitness product in the market. The Physical Activity Council's (PAC) annual participation report consistently identifies walking and running as the most widely practiced fitness activities among U.S. adults validating treadmill ownership as the logical home fitness equipment entry point for the largest consumer fitness cohort.

End User Insights

Male users lead the end user segment with approximately 55% market share in 2026, historically anchored by male consumers' higher engagement with strength training and resistance equipment categories that dominate home gym equipment purchase decisions a pattern consistently documented in consumer fitness behavior surveys.

The Sports & Fitness Industry Association (SFIA) Sports, Fitness and Leisure Activities Topline Participation Report documents that males maintain higher participation rates in weightlifting and resistance training activities, which correlate directly with purchasing intent for dumbbells, weightlifting benches, and resistance training equipment that represent significant categories within the home fitness equipment market.

Application Insights

Cardiovascular Training leads the application segment with approximately 58% market share in 2025, reflecting treadmills' and stationary cycles' collective dominance of the home fitness equipment installed base globally and the universal recognition of cardio exercise's health benefits among the broadest consumer demographic. The American Heart Association (AHA) recommends a minimum of 150 minutes of moderate-intensity or 75 minutes of vigorous-intensity aerobic activity per week exercise guidance that most consumers interpret as cardio training and that directly motivates cardiovascular fitness equipment purchases.

Connected cycling has demonstrated exceptional consumer engagement: Peloton has publicly reported average weekly usage rates significantly above traditional home fitness equipment industry norms, validating the subscription model's ability to convert cardiovascular equipment from low-utilization hardware into highly engaged fitness platforms.

Sales Channel Insights

Online channels lead the sales channel segment with approximately 62% market share in 2025, reflecting the home fitness equipment category's natural alignment with e-commerce purchasing behavior consumers research specifications, read peer reviews, compare prices, and value home delivery for large, heavy items that would be difficult to transport from retail stores.

The pandemic-era shift to online fitness equipment purchasing permanently accelerated the channel's dominance, as consumers who had never previously purchased fitness equipment online experienced the convenience of home delivery and are unlikely to revert to predominantly retail purchasing. Amazon is the world's largest individual channel for home fitness accessories including resistance bands, dumbbells, and yoga equipment, and Peloton's direct-to-consumer online model achieved USD 4 billion in annual revenue at peak validating the scale achievable through digital-first distribution strategies.

Regional Analysis

North America Home Fitness Equipment Market Trends & Analysis

North America is the world's largest home fitness equipment market by revenue, anchored by U.S. consumers' high disposable income, well-established home gym culture, and the concentrated market presence of leading connected fitness brands including Peloton, NordicTrack (iFIT), and Nautilus (Bowflex). The North American market's evolution toward premium connected fitness platforms where hardware serves as a subscription gateway is creating above-average revenue per unit growth even as unit volumes normalize.

U.S. Home Fitness Equipment Market Size

The United States commands approximately 83% of the North American home fitness equipment market, representing the world's most developed home gym culture with the SFIA reporting that approximately 62 million Americans participate in home exercise on fitness equipment. The U.S. segment grows at approximately 5.8% CAGR through 2033, with growth driven by the connected fitness subscription model expanding across cycling, rowing, and strength training product categories and by the growing 45+ demographic's investment in home-based functional fitness equipment aligned with longevity and mobility health goals.

Europe Home Fitness Equipment Market Trends, Drivers, & Insights

Europe is a mature and quality-driven home fitness equipment market, characterized by strong consumer preference for premium, durably built equipment from established brands including Technogym, Life Fitness, and Kettler.

Europe's progressive health policy environment with the EU Physical Activity Guidelines recommending 150 minutes of moderate physical activity weekly and national government active living campaigns in Germany, France, and the Nordics is sustaining health-motivated consumer fitness investment.

Germany Home Fitness Equipment Market Size

Germany holds approximately 22% of the European home fitness equipment market, driven by Germans' historically strong fitness culture the German Olympic Sports Confederation (DOSB) reports over 27 million active sports club members and a growing home fitness consumer segment that supplements club-based training with home equipment. Germany's market grows at approximately 5.9% CAGR through 2033, with premium strength training equipment from Kettler and international brands benefiting from Germany's high per-capita fitness spending.

U.K. Home Fitness Equipment Market Size

The United Kingdom accounts for approximately 17% of the European market. The UK Sport and Recreation Alliance and Sport England's Active Lives Survey documents consistent home exercise participation growth, and the UK market is among Europe's most digitally engaged with high adoption rates for connected fitness applications including Peloton UK and Apple Fitness+. UK consumers show strong preference for premium, compact fitness solutions compatible with smaller home footprints.

France Home Fitness Equipment Market Size

France represents approximately 13% of the European home fitness equipment market. France's Programme National Nutrition Santé (PNNS) promotes physical activity as a public health priority, and the government's active health investment agenda sustains consumer motivation for home fitness equipment purchases. French consumers show growing adoption of compact strength training equipment and connected cycling platforms, with Decathlon one of Europe's largest sporting goods retailers serving as the dominant volume distribution channel for entry-to-mid-tier home fitness products across France.

Asia Pacific Home Fitness Equipment Market Drivers & Analysis

Asia Pacific is the fastest-growing regional home fitness equipment market, propelled by a rapidly expanding health-conscious middle class, increasing urbanization driving demand for home-based fitness solutions, and the explosive growth of e-commerce channels enabling first-time equipment purchases across markets with limited specialty retail infrastructure.

India and Southeast Asia represent the region's highest-growth emerging markets, where first-time home fitness equipment buyers motivated by post-pandemic health awareness and social media fitness culture are entering the market at an accelerating pace. The Ministry of Youth Affairs and Sports (India) and Sport SG (Singapore) active living programs are further stimulating fitness investment awareness across government-backed health promotion channels.

China Home Fitness Equipment Market Size

China holds approximately 38% of the Asia Pacific home fitness equipment market, with demand driven by its rapidly growing urban middle class and the world's largest e-commerce fitness equipment retail ecosystem. China's segment grows at approximately 7.2% CAGR through 2033, driven by Alibaba's and JD.com's expanding fitness equipment category investment, growing strength training equipment adoption among China's young urban population, and the domestic health policy emphasis on physical activity under China's Healthy China 2030 initiative.

India Home Fitness Equipment Market Size

India accounts for approximately 14% of the Asia Pacific market and is among the region's fastest-growing country markets at approximately 8.1% CAGR through 2033. India's post-pandemic fitness awareness surge documented by Google Trends showing sustained high search volume for home gym equipment combined with rising disposable income in urban tier-1 and tier-2 cities, and the rapid growth of Flipkart and Amazon India fitness equipment categories, is creating the region's most dynamic first-time home equipment buyer market.

Japan Home Fitness Equipment Market Size

Japan represents approximately 16% of the Asia Pacific home fitness equipment market. Japan's aging population with 28% of the population over 65 per the Ministry of Internal Affairs and Communications is driving demand for functional fitness and rehabilitation equipment suited to elderly users, including low-impact cycling equipment and resistance band systems. Japan's high health consciousness and premium product preference sustain above-average selling prices.

Competitive Landscape

The global home fitness equipment market is moderately fragmented, with established hardware brands competing alongside connected fitness platform operators and emerging value-tier manufacturers from Asia. Peloton Interactive, iFIT Health & Fitness (NordicTrack), Nautilus (Bowflex), Technogym, and Life Fitness hold premium segment leadership through brand recognition, connected platform ecosystems, and retail channel control collectively accounting for an estimated 35% of premium segment revenue.

Strategic themes include direct-to-consumer digital channel investment, subscription revenue diversification through premium content tiers, and product line premiumization through AI coaching integration. Emerging Chinese OEM manufacturers are intensifying entry-to-mid-tier price competition, compelling Western brands to accelerate platform differentiation.

Key Market Developments

- In April 2025, Strong way Gym Supplies launched the Smith Machine Home Gym in the UK, offering an all-in-one strength training solution featuring a Smith machine barbell, dual cable pulley system with a 144kg weight stack, pull-up bar, adjustable dip station, and a wide array of attachments for comprehensive workouts.

- In April 2025, Sunny Health and Fitness expanded its connected equipment portfolio with the launch of new Wi-Fi-enabled treadmills, designed to deliver an immersive and engaging at-home fitness experience.

Companies Covered in Home Fitness Equipment Market

- Peloton Interactive Inc.

- iFIT Health & Fitness Inc. (NordicTrack / ProForm)

- Technogym S.p.A.

- Nautilus Inc. (Bowflex / Schwinn)

- Life Fitness

- Johnson Health Tech

- Rogue Fitness

- Inspire Fitness

- ICON Health & Fitness

- Precor

- Lululemon Athletica (Mirror)

- Decathlon S.A.

- UFI Filters

Frequently Asked Questions

The global home fitness equipment market is estimated at approximately US$ 14.6 billion in 2026. The market is projected to reach US$ 22.2 billion by 2033, expanding at a CAGR of 6.2%, driven by health-motivated consumer investment, connected fitness platform growth, and Asia Pacific's rapidly expanding first-time buyer cohort fueled by e-commerce accessibility.

The primary demand drivers are the rising global burden of physical inactivity-linked diseases with the WHO estimating 3.2 million deaths annually attributable to inactivity creating health-motivated consumer investment, combined with the connected fitness platform model pioneered by Peloton and iFIT that elevates average equipment revenue by integrating subscription content.

Treadmills lead the product type segment with approximately 28% market share in 2025. Their dominance reflects treadmills' status as the most universally recognized and broadly purchased home fitness product globally validated by the Physical Activity Council's (PAC) consistent documentation of walking and running as the most popular U.S. fitness activities.

North America leads the global home fitness equipment market with approximately 38% revenue share in 2025. The region's leadership is anchored by U.S. consumers' high disposable income and established home gym culture with the SFIA reporting approximately 62 million Americans participating in home exercise equipment use combined with the concentrated market presence of the world's leading connected fitness brands including Peloton Interactive and iFIT Health & Fitness.

The leading companies in the global home fitness equipment market include Peloton Interactive, iFIT Health & Fitness (NordicTrack), Technogym S.p.A., Nautilus (Bowflex), Life Fitness, Johnson Health Tech (Horizon/Matrix), Rogue Fitness, Decathlon S.A., and Lululemon Athletica (Mirror).