- Power Generation, Transmission, & Distribution

- Gas-Insulated Transformer Market

Gas-Insulated Transformer Market Size, Share, and Growth Forecast, 2025 - 2032

Gas-Insulated Transformer Market by Configuration Type (Single-phase, Three-phase), Voltage (Low Voltage (Up to 72.5 kV), Medium Voltage (72.5 kV to 220 kV), High Voltage (Above 220 kV)), Application (Utilities, Industrial, Commercial), and Regional Analysis for 2025 - 2032

Gas-Insulated Transformer Market Share and Trends Analysis

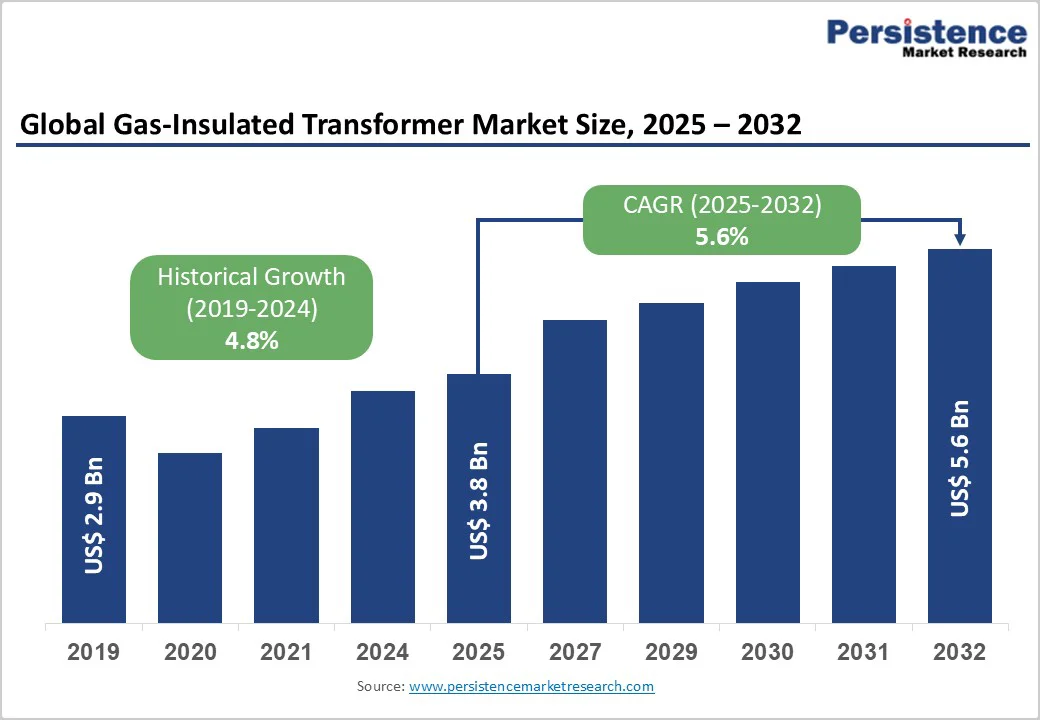

The global gas-insulated transformer market size is likely to be valued at US$ 3.8 billion in 2025, and is projected to reach US$ 5.6 billion by 2032, growing at a CAGR of 5.6% during the forecast period 2025 - 2032.

Accelerating urbanization requiring space-efficient power infrastructure, rising renewable energy integration, and increasing global electricity demand supporting grid modernization initiatives are the key drivers bolstering sales of insulated transformers.

Superior reliability and reduced maintenance requirements compared to conventional oil-filled transformers, combined with technological advancements in SF6-free insulation technologies and smart grid integration, sustain market growth through enhanced operational efficiency and environmental compliance.

Key Industry Highlights

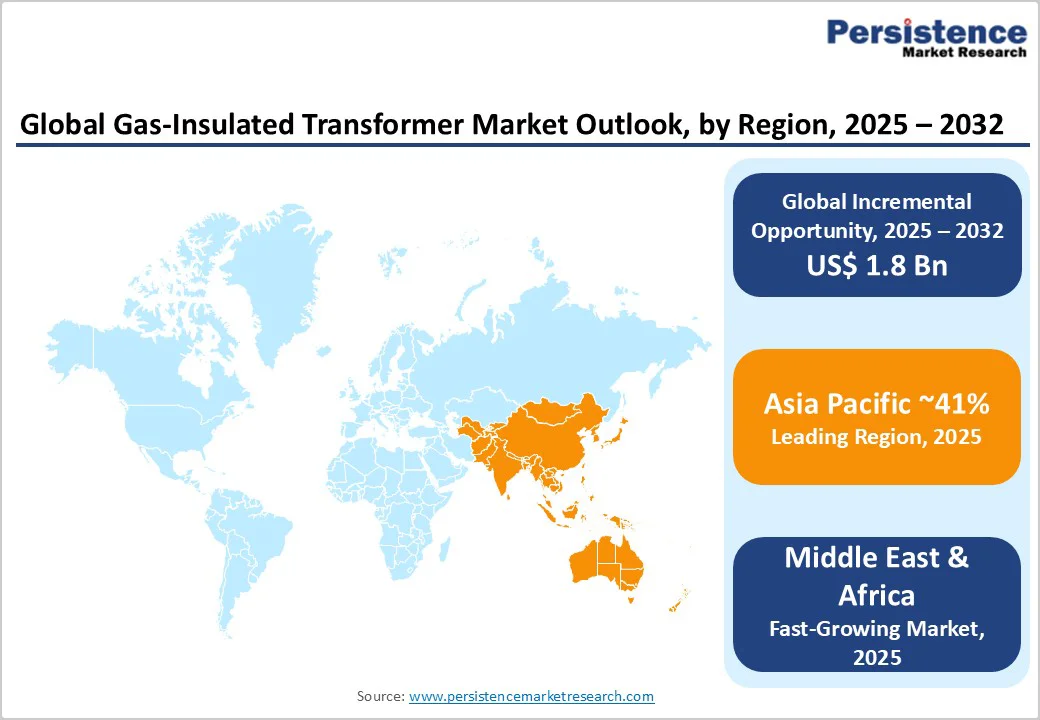

- Leading Region: Asia Pacific dominates with around 41.2% market share, driven by rapid industrialization, urbanization, and massive electricity demand.

- Fastest-growing Regional Market: Middle East & Africa is likely to grow the fastest at approximately 7.2% CAGR, propelled by infrastructure development, electrification initiatives, and renewable energy integration.

- Dominant Voltage Type: High voltage (72.5 kV to 220 kV) transformers lead with 63% market share, aided by utility transmission applications.

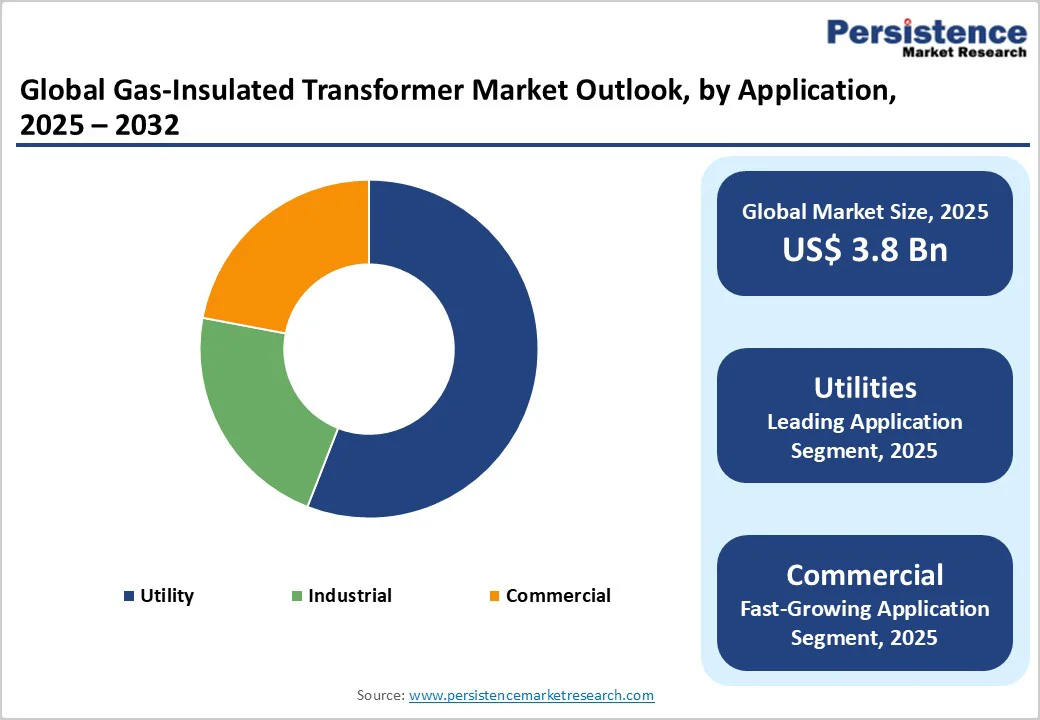

- Leading Application: The utilities sector leads with an estimated 58% market share in 2025, boosted by the growing need for reliable power distribution networks.

- Key Opportunity: SF6-free and digital transformer technology development targeting environmental compliance and smart grid integration can unlock premium pricing realization across developed markets.

| Key Insights | Details |

|---|---|

| Gas Insulated Transformer Market Size (2025E) | US$ 3.8 Bn |

| Market Value Forecast (2032F) | US$ 5.6 Bn |

| Projected Growth CAGR(2025 - 2032) | 5.6% |

| Historical Market Growth (2019 - 2024) | 4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

High-Speed Urban Infrastructure Development and Space-Efficient Power Solutions

Rapid urbanization has stoked the need for gas-insulated transformers, particularly in densely populated metropolitan areas facing space constraints. Global urban population is projected to reach 68% by 2050, requiring efficient power infrastructure to support escalating energy demand. Major metropolitan centers including Tokyo and New York City are increasingly deploying underground substations that necessitate compact transformer solutions.

Gas-insulated transformers offer 40-50% smaller carbon footprints compared to conventional oil-filled alternatives, enabling effective substation deployment in space-constrained urban environments.

Infrastructure expansion across Asia, Africa, and Latin America is further stimulating the demand for modern electrical equipment to support unprecedented population growth and industrialization, while government urban electrification programs and smart city initiatives further accelerate investment in modern substation infrastructure.

Global renewable energy expansion and grid modernization initiatives are driving substantial demand for gas-insulated transformers as essential components of upgraded transmission systems. Renewable energy capacity additions exceeding 500 GW annually worldwide require advanced interconnection infrastructure to transmit power from distributed generation sources to demand centers.

Wind and solar installations increasingly depend on medium and high-voltage transmission systems to integrate distributed generation effectively. Smart grid modernization programs are accelerating infrastructure upgrades and transformer procurement.

Grid reliability and resilience requirements are fueling the adoption of advanced transformer technologies capable of managing variable loads from renewable sources. Government renewable energy mandates and clean energy transition commitments are enabling substation modernization efforts, creating multi-year procurement programs that can sustain robust transformer demand growth across developed and emerging markets.

Environmental Concerns Regarding SF6 Gas and Regulatory Pressures

Sulfur hexafluoride (SF6) gas, with global warming potential (GWP) 23,500 times higher than carbon dioxide, has intensified environmental concerns and regulatory pressures. The European Union (EU) and other regulatory bodies are restricting SF6 emissions, limiting market expansion in environmentally-conscious jurisdictions.

Potential SF6 gas leaks during installation and maintenance requiring specialized handling and creating operational risks. The high cost of SF6 gas recovery and recycling systems are further inflating operational expenses, potentially disrupting existing market dynamics.

Gas-insulated transformer manufacturing requires significant capital investment and specialized technical expertise. Transformer installation timelines can extend several months, from order to commissioning, creating project financing challenges. Specialized shipping and handling requirements are spiking logistics costs, particularly for remote installations.

Furthermore, limited number of qualified manufacturers and installation contractors has restricted supply capacity in emerging economies, dampening market outlook.

SF6-Free and Low-GWP Insulation Technology Development

The development and commercialization of SF6-free and low GWP insulation technologies present an exceptional opportunity driven by tightening environmental regulations and growing sustainability requirements.

Major industry players are leading the transition to eco-friendly solutions, with Hitachi Energy unveiling the world's first SF6-free 550 kV gas-insulated switchgear for State Grid Corporation of China in 2024, demonstrating commercial viability at high voltage levels. Such efforts to develop alternative gas mixtures and solid insulation materials are enabling regulatory compliance without sacrificing technical capabilities.

Government incentives and mandates supporting eco-friendly technology adoption are accelerating market growth, with premium pricing for environmentally-certified transformers creating margin expansion opportunities for innovative manufacturers.

Smart grid technology advancement and digital transformation are creating significant market opportunities for advanced transformer solutions that enable predictive maintenance and operational optimization. Global smart grid investments require compatible transformer infrastructure equipped with digital capabilities.

The integration of Internet of Things (IoT) has enabled real-time condition monitoring and predictive maintenance, substantially reducing unplanned outages and operational costs while extending equipment lifespan. Digital twin technology can support virtual testing and design optimization, accelerating innovation and performance improvement.

Advanced sensors and data analytics can facilitate comprehensive transformer health monitoring, improving reliability and extending operational lifespans across utility networks. Regulatory support for smart grid initiatives is resulting multi-year infrastructure investment programs that can ensure stable demand for digitally-enabled transformer solutions across geographies.

Category-wise Analysis

Configuration Type Insights

Three-phase transformers dominate the gas insulated transformer market, commanding approximately 75% revenue share in 2025. This dominance is attributable to the widespread utility and industrial applications requiring three-phase power distribution. These configurations support high-capacity power transmission across regional transmission networks and industrial facilities.

Superior efficiency and reduced transmission losses justify the adoption of three-phase transformers in large-scale infrastructure projects. Established manufacturing processes and proven operational performance supporting cost competitiveness and supply chain maturity.

Single-phase transformers address specialized applications including lighting circuits and control systems, proving advantageous in rural electrification and distributed energy systems and aiding segmental growth.

Voltage Insights

The medium voltage (72.5 kV to 220 kV) segment represents the dominant voltage classification, capturing approximately 63% of the gas-insulated transformer market revenue share in 2025. Utility transmission and grid interconnection requirements are the primary forces fueling the adoption of medium-voltage transformers.

These transformers provide robust support for long-distance bulk power transmission, connecting generation facilities to demand centers. Utilities have demonstrated an unwavering preference for standardized high-voltage systems, allowing cost-effective procurement and supply chain integration.

Grid reliability requirements favor the deployment of proven high-voltage technology for mainstream adoption. Voltage classification selection driven by transmission distance and capacity requirements has been instrumental in facilitating market segmentation and diversifying supplier positioning.

Application Insights

The utility sector dominates applications, commanding approximately 58% of the total market demand through power generation, transmission, and distribution operations. Utility companies deploy gas-insulated transformers extensively for long-distance bulk power transmission, optimizing grid reliability and operational efficiency.

The integration of renewable energy sources necessitates continuous transformer upgrades to evacuate power from distributed generation facilities to demand centers. Ongoing grid modernization initiatives and substation infrastructure upgrades are driven by rising electricity demand, ensuring sustained procurement requirements across utility networks globally.

Industrial and commercial applications collectively account for approximately 42% of market demand, driven by manufacturing facilities, data centers, and commercial real estate expansion. Industrial operators prioritize reliable power supply systems to maintain operational continuity, justifying investment in premium transformer technologies that minimize downtime and enhance efficiency.

Commercial sector growth is spurring innovative substation placements in rooftops and basements to support urban real estate development while addressing space constraints. These diverse application segments have created differentiated demand patterns, with utilities focusing on transmission efficiency and industrial sectors emphasizing operational resilience, collectively propelling the gas-insulated transformer market growth.

Regional Insights

North America Gas-Insulated Transformer Market Trends

North America occupies a formidable market position, driven by systematic modernization of aging infrastructure and supportive regulatory frameworks. The U.S. electrical grid infrastructure, averaging over 30 years in age, requires substantial replacement and upgrade investments across transmission and distribution networks.

U.S. Environmental Protection Agency (EPA) standards and energy efficiency regulations are accelerating adoption of advanced transformer technologies across utility companies. Government-funded programs including the Smart Grid Investment Program (SGIP) and Energy Efficiency and Renewable Energy (EQIP) initiatives are channeling substantial funding into substation infrastructure upgrades, supporting long-term procurement commitments.

The integration of renewable energy from solar and wind resources is driving transmission infrastructure expansion requirements, particularly for connecting distributed generation facilities to demand centers.

Major metropolitan areas including New York City and Los Angeles are prioritizing substation modernization in space-constrained environments, creating demand for compact, efficient gas-insulated transformers. Regulatory emphasis on grid reliability and resilience, particularly in hurricane-prone and seismic regions, is further motivating utilities to invest in advanced equipment capable of withstanding extreme environmental conditions.

Europe Gas-Insulated Transformer Market Trends

Europe leads in advanced technology adoption on the back of stringent environmental regulations and ambitious renewable energy commitments. The environmental directives of the EU that restrict SF6 emissions are accelerating the transition toward SF6-free and low-GWP insulation technologies across member states.

Germany, the U.K., and France are pursuing aggressive renewable energy targets, particularly offshore and onshore wind integration, requiring substantial transmission infrastructure expansion to connect distributed generation to consumption centers.

Key economic hubs such as Berlin, London, and Paris are modernizing urban substations to accommodate growing energy demand while addressing space constraints through compact, efficient transformer solutions.

Regulatory harmonization across EU member states facilitates streamlined product certification and accelerated technology deployment, reducing barriers to market entry and supporting innovation. Europe's strategic emphasis on environmental sustainability and carbon reduction is creating premium market positioning for eco-friendly transformer technologies, enabling manufacturers to command higher margins for certified sustainable solutions.

Coordinated infrastructure investment programs are supporting comprehensive grid modernization and renewable energy integration initiatives across all member states, ensuring sustained, multi-year transformer procurement throughout the region.

Asia Pacific Gas-Insulated Transformer Market Trends

Asia Pacific commands a dominant 41.2% of the gas-insulated transformer market share in 2025, propelled by rapid industrialization and astronomical growth in electricity demand. China demonstrates technology leadership through pioneering deployments, including State Grid Corporation of China's SF6-free 550 kV gas-insulated switchgear, establishing standards for eco-friendly transformer solutions.

The country's extensive urbanization and industrial expansion are driving massive investments in power infrastructure development, creating sustained demand for advanced transformer technologies. India's electricity demand is projected to surge 65% by 2030, necessitating substantial transmission infrastructure expansion across the nation to support this growth trajectory.

Japan maintains strong technology leadership through advanced manufacturers including Toshiba and Mitsubishi Electric, contributing enormously to transformer innovation and development. Southeast Asian nations including Vietnam and Thailand are rapidly expanding power infrastructure to support accelerating industrial growth and economic development.

Government infrastructure investment programs and comprehensive electrification initiatives throughout the region are creating sustained, long-term market expansion opportunities. This combination of massive electricity demand growth, concentrated industrial development, technology innovation leadership, and coordinated government investment positions Asia Pacific as the critical growth engine for the market throughout the forecast period.

Competitive Landscape for the Insulated Transformer Market

The global gas-insulated transformer market structure is highly consolidated, with leading manufacturers such as General Electric, ABB Ltd., Siemens AG, and Mitsubishi Electric collectively holding approximately 50-55% of the revenues.

These giants are known to leverage their comprehensive portfolios, extensive manufacturing infrastructure, and strong relationships with utility companies to maintain dominant positions. Tier-two players such as Toshiba International and Hyosung have also captured sizable regional market segments by offering specialized solutions and capitalizing on emerging market expertise.

Strategic investments in research and development, capacity expansion, and partnerships with utilities serve as key competitive differentiators among market participants. Companies are prioritizing the development of SF6-free technologies, smart grid integration, manufacturing localization, and superior service to strengthen their competitive edge.

Chinese manufacturers such as Takaoka Toko and Tatung Co. are leveraging manufacturing scale and regional market advantages to support growth in emerging markets, contributing to a dynamic competitive landscape characterized by innovation and regional specialization.

Key Industry Developments

- In November 2025, Iljin Electric announced that it has secured new overseas orders worth US$ 69.86 million for supplying ultra-high-voltage transformers in California, expanding beyond its East Coast base. The company has also entered Europe with a 132-kilovolt transformer project for a U.K. data center and won a 132-kilovolt gas insulated switchgear order in Saudi Arabia, signaling success in market diversification and meeting stringent technological standards.

- In September 2025, Mehru Electrical signed a co-development agreement with Hyosung Heavy Industries to jointly develop GIS instrument transformers. This collaboration aims to leverage each company's expertise to enhance product innovation, improve performance, and meet increasing demand for advanced, reliable GIS components in power grid infrastructure modernization.

- In June 2025, Hitachi Energy introduced two innovations at CWIEME Berlin: GARIP® Eco, an SF6-free GIS transformer bushing designed for high-pressure, sustainable applications, and VUBB Compact, a space-saving on-load tap-changer that reduces transformer footprint and carbon footprint while enhancing flexibility. These advancements support the transition to sustainable, efficient, and compact transformer solutions for modern decentralized energy systems and renewable integration.

Companies Covered in Gas-Insulated Transformer Market

- General Electric

- ABB Ltd.

- Siemens AG - Trench Group

- Arteche

- Mitsubishi Electric Corporation

- Toshiba International Corporation

- NISSIN ELECTRIC Co., Ltd

- Takaoka Toko Co., Ltd.

- Tatung Co.

- Bharat Heavy Electricals Limited

- Hyosung Heavy Industries Corp.

- MEIDENSHA CORPORATION

- Fortune Electric Co., Ltd.

- Transpower Engineering Ltd.

- Hitachi Energy

- Schneider Electric

Frequently Asked Questions

The global gas-insulated transformer market is projected to reach US$ 3.8 billion in 2025.

Rapid urbanization requiring space-efficient power infrastructure, renewable energy capacity additions needing transmission infrastructure, smart grid modernization investments, and skyrocketing electricity demand are driving the market.

The market is poised to witness a CAGR of 5.6% from 2025 to 2032.

SF6-free and low-GWP transformer technology development targeting environmental compliance, regulatory requirements, and sustainability objectives are unlocking attractive market opportunities.

General Electric, ABB Ltd., and Siemens AG are some of the key players in the market.