- Advanced Materials

- Europe Textile Recycling Market

Europe Textile Recycling Market Size, Share, and Growth Forecast 2026 - 2033

Europe Textile Recycling Market by Material Type (Cotton, Polyester & Polyester Fibers, Wool, Nylon Fibers, Acrylic, Others), End-user, Source (Post-Consumer Waste, Pre-Consumer Waste), Recycling Process (Chemical, Mechanical), and Regional Analysis, 2026 - 2033

Europe Textile Recycling Market Size and Trend Analysis

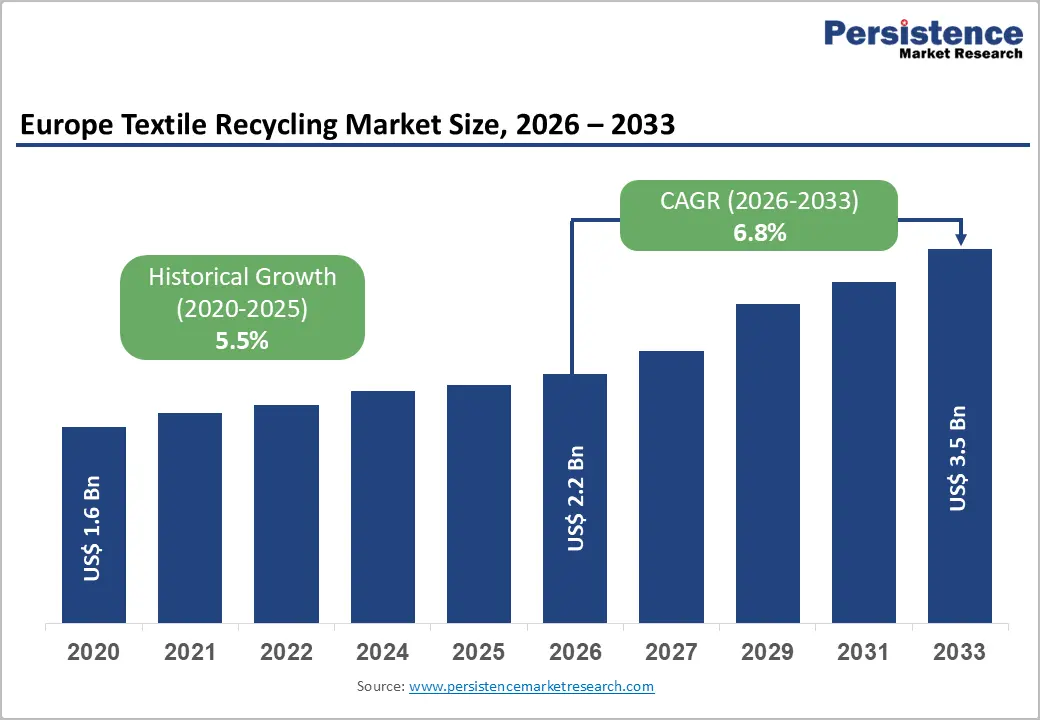

The Europe textile recycling market size is expected to be valued at US$ 2.2 billion in 2026 and projected to reach US$ 3.5 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033. This robust expansion is fundamentally driven by the convergence of stringent EU regulatory mandates on textile waste diversion and accelerating brand-level commitments to circular fiber sourcing.

The European Environment Agency (EEA) estimates that Europeans discard an average of 11 kg of textiles per person annually, of which less than 1% is currently recycled back into fiber, signaling a structural supply-demand gap that advanced mechanical and chemical recycling technologies are uniquely positioned to address. Mandatory separate collection requirements taking effect across EU member states from 2025 onward are catalyzing investment in sortation infrastructure, recycling capacity, and fiber-to-fiber process development.

Key Industry Highlights:

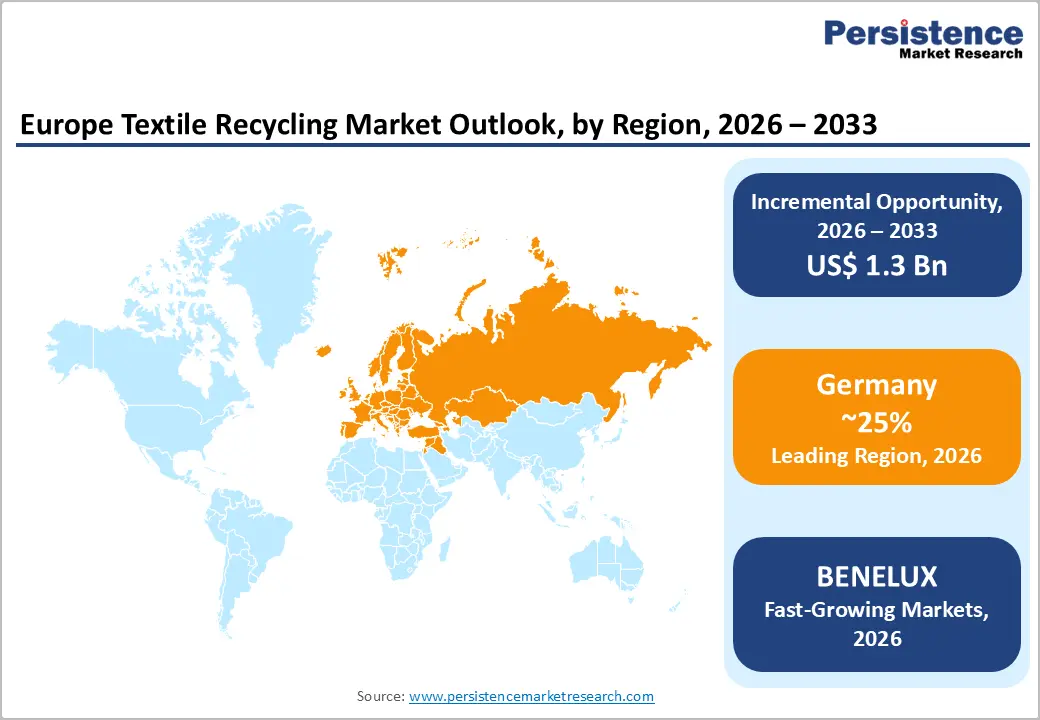

- Leading Region: Germany leads Europe textile recycling market with a 25% share in 2026, supported by advanced waste management infrastructure, industrial mechanical recycling capacity, and accelerating investment in chemical fiber-to-fiber processing technologies.

- Fastest Growing Region: BENELUX is the fastest-growing European sub-region, driven by Belgium's automated sorting hub status, the Netherlands' circular economy policy leadership, and cross-border textile waste logistics capabilities supporting pan-European recycling network development.

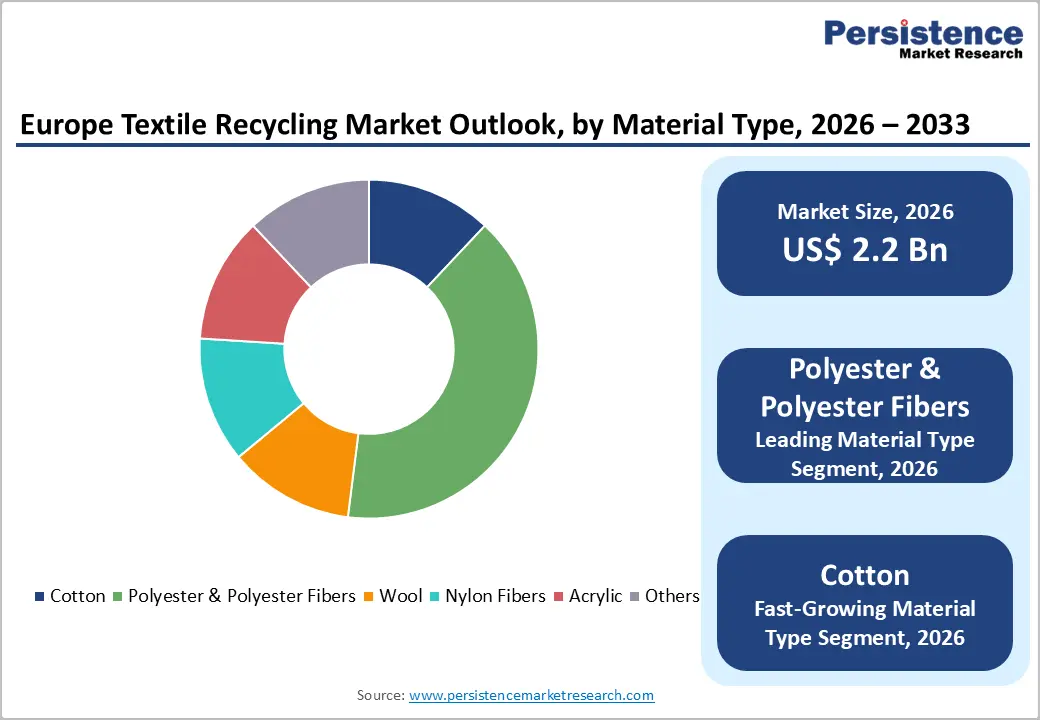

- Dominant Material Type: Polyester and polyester fibers dominate with a 44% share in 2026, reflecting synthetic fabric prevalence in post-consumer textile waste and mature rPET mechanical recycling capacity among key European recyclers and fiber producers.

- Fast-Growing Material Type: Cotton recycling is the fastest-growing material type segment at a 7% CAGR (2026 - 2033), propelled by chemical recycling innovations enabling cotton fiber-to-fiber recovery and growing brand demand for recycled cotton content in premium apparel.

- Key Opportunity: Chemical fiber-to-fiber recycling targeting fashion and apparel applications represents the highest-value opportunity, enabled by EU Digital Product Passport mandates, brand circularity commitments, and technology scale-up by Renewcell, Worn Again, and Lenzing.

DRO Analysis

Drivers - EU Mandatory Textile Separate Collection and Extended Producer Responsibility Frameworks

Regulations and mandates are dominant for Europe textile recycling market. The EU Waste Framework Directive (2008/98/EC) mandated all EU member states to establish separate textile waste collection systems by January 1, 2025. Complementing this, the EU Strategy for Sustainable and Circular Textiles (2022) set a target that by 2030, all textile products placed on the EU market must be durable, repairable, and recyclable.

Extended Producer Responsibility (EPR) schemes, already operational in France since 2007 under Refashion (formerly Eco TLC), are progressively being adopted across Germany, Italy, and the Netherlands, creating fee-based funding mechanisms that directly channel capital into post-consumer textile collection, sorting, and recycling infrastructure at scale.

Brand-Level Circularity Commitments and Recycled Fiber Offtake Agreements

Major European fashion groups are making binding recycled content commitments that are translating into long-term demand for recycled textile fibers. H&M Group has committed to using 100% recycled or sustainably sourced materials by 2030, while Inditex targets 40% sustainable fabrics in its garments by 2030. These commitments create predictable demand pipelines for recyclers and fiber producers.

Renewcell's Circulose®, a dissolving pulp made from 100% recycled cotton textiles, has secured offtake agreements with brands including Levi's and H&M, demonstrating that brand procurement strategies are actively de-risking investment in fiber-to-fiber recycling technology. The feedback loop between brand sustainability targets and recycler commercial viability is a defining structural growth dynamic for the European market through 2033.

Restraints - Technological and Quality Barriers in Fiber-to-Fiber Chemical Recycling

Despite technological promise, chemical textile recycling remains constrained by persistent challenges in processing blended fabrics, which constitute the majority of post-consumer textile waste. A 2023 report by the Ellen MacArthur Foundation noted that less than 1% of fibres used to make clothing are currently recycled into new clothing.

The incompatibility of cotton-polyester blends with existing solvent-based recycling processes forces costly pre-sorting investments and results in significant material yield losses. Output fiber quality frequently falls below virgin fiber standards, limiting substitutability and requiring blending at low ratios in premium product lines, thereby restricting recycler revenue realization.

Fragmented Collection Infrastructure and Contamination in Post-Consumer Streams

The economic viability of textile recycling is fundamentally dependent on the quality and consistency of input feedstock, a dimension where Europe's collection infrastructure remains structurally inadequate. The European Environment Agency has highlighted that, despite mandatory separate collection, a significant share of collected textiles contains high contamination levels, soiling, mixed-material garments, and non-textile items, that reduces yields and raises preprocessing costs.

Logistics costs for low-density, bulky textile waste are disproportionately high relative to material recovery values, particularly for smaller collection operators in rural regions, compressing unit economics and deterring private investment in network expansion.

Opportunities - High-Value Chemical Recycling for Fashion and Apparel Applications

The transition from mechanical downcycling to chemical fiber-to-fiber recycling represents the highest-value commercial opportunity in the European textile recycling market. Chemical recycling technologies, including solvent-based processes such as Worn Again Technologies' polymer and cellulose separation platform, and Renewcell's cellulosic dissolution technology, can produce virgin-equivalent output fibers suitable for premium fashion applications.

The EU Ecodesign for Sustainable Products Regulation (ESPR), approved in 2024, introduces mandatory Digital Product Passports for textiles that will require traceability of recycled content, structurally advancing chemical recyclers who can certify fiber provenance. With fashion and apparel commanding significantly higher fiber price realization than industrial uses, scaling chemical recycling output into this channel represents a multi-year revenue maximization opportunity for technology developers and licensed operators across Europe.

AI-Enabled Sorting and Automation as a Scalability Unlock

Advanced automated sorting, powered by near-infrared (NIR) spectroscopy, hyperspectral imaging, and AI-based material classification, is emerging as a critical enabler of large-scale textile recycling economics. Manual sorting, which currently dominates European textile waste processing, is labor-intensive, inaccurate across blended materials, and unscalable relative to the volumes that mandatory collection will generate post-2025.

ANDRITZ and Valvan Baling Systems have deployed industrial-scale automated fiber sorting lines across Belgium and Germany. The RESYNTEX and SORT4CIRCLE EU Horizon-funded projects have validated AI-assisted sorting accuracy exceeding 90% for single-material fractions. As throughput scales, unit sorting costs are projected to decline significantly, improving the feedstock economics for both chemical and mechanical recyclers and unlocking the volume throughput necessary to justify fiber-to-fiber recycling plant construction at a commercial scale across the region.

Category-wise Analysis

Material Type Insights

Polyester & polyester fibers dominate the European textile recycling market with an estimated 44% share in 2026. Polyester's leadership reflects both its overwhelming prevalence in the European waste textile stream, driven by decades of fast fashion's reliance on synthetic fabrics, and the relative maturity of mechanical recycling processes for PET-based textiles. HYOSUNG TNC's regen™ and Aquafil's ECONYL® nylon regeneration process demonstrate the commercial viability of closed-loop synthetic fiber recycling.

The Textile Exchange's Preferred Fiber & Materials Report confirms that recycled polyester (rPET) accounts for the largest share of preferred synthetic fiber adoption across European brands. Continued investment in bottle-to-fiber and fiber-to-fiber PET recycling capacities, particularly by Veolia and Ecotex Group, reinforces polyester's structural dominance within the material type segment.

Source Insights

Post-consumer waste is the leading source segment, accounting for an estimated 62% of the European textile recycling market in 2026. The sheer volume of discarded garments, household textiles, and accessories from European consumers, an estimated 5.8 million tons generated annually across the EU, dwarfs pre-consumer industrial offcuts and overstock. The EU's mandatory separate collection mandate, effective January 2025, significantly expands the formalized post-consumer collection stream.

Pre-consumer waste, while lower in contamination and therefore easier to process, is structurally limited by brands' improving production efficiency and on-demand manufacturing models, which are reducing fabric waste at source. Post-consumer dominance is expected to deepen through the forecast period as collection systems scale and urban recovery infrastructure matures.

Recycling Process Insights

Mechanical recycling remains the dominant process in the European textile recycling market with an estimated 72% share in 2026, underpinned by its established industrial infrastructure, lower capital costs, and ability to process large volumes of mixed textile waste without chemical inputs. Mechanical processes, shredding, carding, and re-spinning, are well-suited to producing industrial-grade fibers for insulation, padding, and nonwoven. Industry bodies such as the European Recycling Industries' Confederation (EuRIC) represent a well-developed mechanical processing sector across Germany, Italy, and the Netherlands.

Chemical recycling is the fastest-growing process segment, as European policy mandates and brand circularity targets increasingly require fiber-to-fiber quality outputs that mechanical processes cannot deliver, driving investment in solvent-based and hydrothermal chemical recycling platforms across the region.

End-user Insights

Low-value products such as insulation materials and industrial cleaning clothes represent the current leading end-use segment, with an estimated 58% share in 2026, a reflection of the fact that most of the mechanically recycled textile fiber is of insufficient quality for high-value apparel re-entry. Recycled textile insulation, particularly for the construction sector, benefits from growing European demand for sustainable building materials under the EU Energy Performance of Buildings Directive (EPBD).

The fastest-growing segment is High Value Products (specifically Fashion and Apparel), as chemical recycling technology matures, and brand circularity mandates create premium offtake channels. Companies such as Renewcell and Worn Again Technologies are enabling high-value re-entry, structurally shifting segment revenue mix toward apparel applications through 2033.

Regional Analysis

Germany Textile Recycling Market Trends and Insights

Germany leads the European textile recycling market with a 25% share in 2026, underpinned by its combination of advanced waste management infrastructure, strong industrial-scale mechanical recycling capacity, and progressive regulatory implementation. Germany's Kreislaufwirtschaftsgesetz (Circular Economy Act) and municipal waste management framework have supported one of Europe's most comprehensive textile collection networks, with charities and commercial collectors operating parallel systems that feed into industrial recyclers.

German mechanical recyclers, serving automotive, construction, and industrial sectors, benefit from a consistent feedstock supply. Germany is also home to significant sortation technology players, and investment in chemical recycling pilots is accelerating, with ANDRITZ and pilot facilities by Worn Again Technologies positioning the country as a future hub for advanced fiber-to-fiber processing in Western Europe.

France Textile Recycling Market Trends and Insights

France holds a structurally distinctive position in Europe textile recycling as the continent's most mature EPR market. It is characterized by a higher share of fashion apparel reuse and high-value recycling relative to its neighboring countries reflecting both the country's cultural fashion heritage and refashions incentive structure for quality-upgrading. Brands such as Inditex (Zara France) and domestic labels are active in EPR fee contributions, channeling investment into sorting and recycling innovation across the national value chain.

Italy Textile Recycling Market Trends and Insights

Italy occupies a unique position in the European textile recycling market as the home of Prato, one of the world's oldest and most productive textile recycling districts, with over 3,000 companies engaged in the collection, sorting, and mechanical recycling of pre- and post-consumer woolen textiles into regenerated fiber. The Prato model has demonstrated the economic viability of large-scale textile recycling long before regulatory compulsion and represents a significantly embedded industrial capacity for the Europe market.

Italy's luxury fashion sector is increasingly engaging with recycled fiber sourcing to meet sustainability commitments, creating a premium demand channel for Italian recyclers. The country is also investing in chemical recycling R&D to extend its heritage mechanical capacity into higher-value output streams, supported by national innovation funds and EU Horizon grants. Italy's market trajectory is shaped by both artisanal heritage and the modernization imperative of the EU textile strategy.

U.K. Textile Recycling Market Trends and Insights

The U.K. textile recycling market operates in a post-Brexit regulatory environment that is progressively realigning with EU sustainability standards through domestic policy frameworks. The UK Environment Act 2021 provides the legislative foundation for EPR scheme development, and the UK government's Textiles 2030 voluntary commitment programme, administered by WRAP (Waste & Resources Action Programme), has engaged over 100 signatories including major fashion retailers.

Approximately 350,000 tons of clothing and household textiles are collected annually in the UK, per WRAP estimates. TEXAID's UK operations and domestic players such as Nathans Wastesavers form a growing commercial recycling base. The U.K. is a key market for chemical recycling technology firms given its combination of large post-consumer textile volumes, brand-sustainability commitments, and government innovation funding through Innovate UK.

BENELUX Textile Recycling Market Trends and Insights

BENELUX is the fastest-growing sub-region in the European textile recycling market, driven by Belgium's role as a hub for pan-European automated sorting infrastructure and the Netherlands' leadership in circular economy policy implementation. Valvan Baling Systems (Belgium) and Wieland Textiles (Netherlands) are significant industrial actors in the regional value chain. The Netherlands' National Agreement on Sustainable Garments and Textiles has mobilized over 70 signatories from across the Dutch fashion industry.

Belgium serves as a critical logistics node for cross-border textile waste flows within the EU single market. The iinouiio platform and similar B2B textile waste trading innovations are gaining traction in the BENELUX market. Investment in high-throughput automated sorting, capable of processing 30,000+ tons per year, is positioning BENELUX as the operational backbone of the emerging European textile recycling infrastructure network.

Competitive Landscape

Europe textile recycling market is moderately fragmented, with a mix of established industrial waste processors (Veolia, ANDRITZ), specialist textile recyclers (Renewcell, Aquafil, Worn Again Technologies), and fiber-integrated players (Lenzing AG, HYOSUNG TNC). Key differentiators include chemical recycling IP, brand offtake partnerships, and sortation automation capability.

Emerging business models include waste-as-feedstock platforms (iinouiio), technology licensing, and brand-recycler joint ventures. Competitive intensity is increasing as brand sustainability mandates convert into procurement requirements, drawing new entrants and venture-backed startups into the fiber-to-fiber segment.

Key Developments:

- In 2025, Renewcell completed a restructuring and new investor financing arrangement to secure its Circulose® production facility in Sweden, re-establishing commercial supply of chemically recycled cotton pulp to European fashion brands under long-term offtake contracts.

- In 2024, Lenzing AG announced expanded sourcing of recycled cotton feedstock for its TENCEL™ Lyocell fiber production, deepening its integration into the post-consumer textile recycling supply chain and supporting circular apparel brand commitments across Europe.

- In 2023, Worn Again Technologies secured funding to scale its PET and cellulose chemical separation technology, with pilot operations in collaboration with Sulzer, targeting commercial-scale fiber-to-fiber recycling output for European brand customers by 2025.

Europe Textile Recycling Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 1.6 Billion |

| Current Market Value (2026) | US$ 2.2 Billion |

| Projected Market Value (2033) | US$ 3.5 Billion |

| CAGR (2026 - 2033) | 6.8% |

| Leading Region | Germany, 25% market share (2026) |

| Dominant Category-1 (Material Type) | Polyester & Polyester Fibers, 44% share (2026) |

| Top-ranking Category-2 (End-user) | Low Value Products, 58% share (2026) |

| Incremental Opportunity (2026 - 2033) | US$ 1.3 Billion |

Companies Covered in Europe Textile Recycling Market

- Lenzing AG

- Inditex

- H&M Group

- ANDRITZ

- Recover Textile Systems, S.L.

- Worn Again Technologies

- Veolia

- Renewcell

- TEXAID

- iinouiio

- Ecotex Group

- Nathans Wastesavers

- HYOSUNG TNC

- Renewcell

- Aquafil S.p.A.

Frequently Asked Questions

Europe textile recycling market size is expected to be valued at US$ 2.2 billion in 2026 and is projected to reach US$ 3.5 billion by 2033, expanding at a CAGR of 6.8% during the forecast period (2026 - 2033), driven by regulatory mandates and advancing recycling technology.

The primary demand drivers are the EU's mandatory separate textile collection requirement effective January 2025 under the Waste Framework Directive, and brand-level circularity commitments from major fashion groups such as H&M Group and Inditex.

Germany leads the European textile recycling market with approximately 25% market share in 2026. Its leadership is built on advanced waste management infrastructure, industrial mechanical recycling capacity serving automotive and construction sectors, and accelerating investment in chemical fiber-to-fiber recycling technologies, supported by progressive circular economy legislation.

The key opportunity lies in scaling chemical fiber-to-fiber recycling for high-value fashion and apparel applications. The EU Ecodesign for Sustainable Products Regulation (ESPR) and Digital Product Passport requirements for textiles will create traceable recycled fiber demand from brands, rewarding chemical recyclers with premium pricing and long-term offtake security through 2033.

Leading companies in the European textile recycling market include Lenzing AG, Renewcell, Worn Again Technologies, Aquafil S.p.A., Veolia, ANDRITZ, Recover Textile Systems S.L., HYOSUNG TNC, TEXAID, Ecotex Group, iinouiio, Nathans Wastesavers, H&M Group (as a major recycled fiber buyer), Inditex, and Valvan Baling Systems, among others.