- Inks, Coatings, Adhesives & Sealants (ICAS)

- Electronic Sealants Market

Electronic Sealants Market Size, Share, and Growth Forecast, 2026 - 2033

Electronic Sealants Market by Product Type (Silicone Sealants, RTV Silicones, Silicone Gel, Epoxy Sealants, PU Sealants, Acrylic Sealants), Application (Encapsulation, Underfilling, Potting, Others), End-use Industry, and Regional Analysis for 2026 - 2033

Electronic Sealants Market Size and Trends Analysis

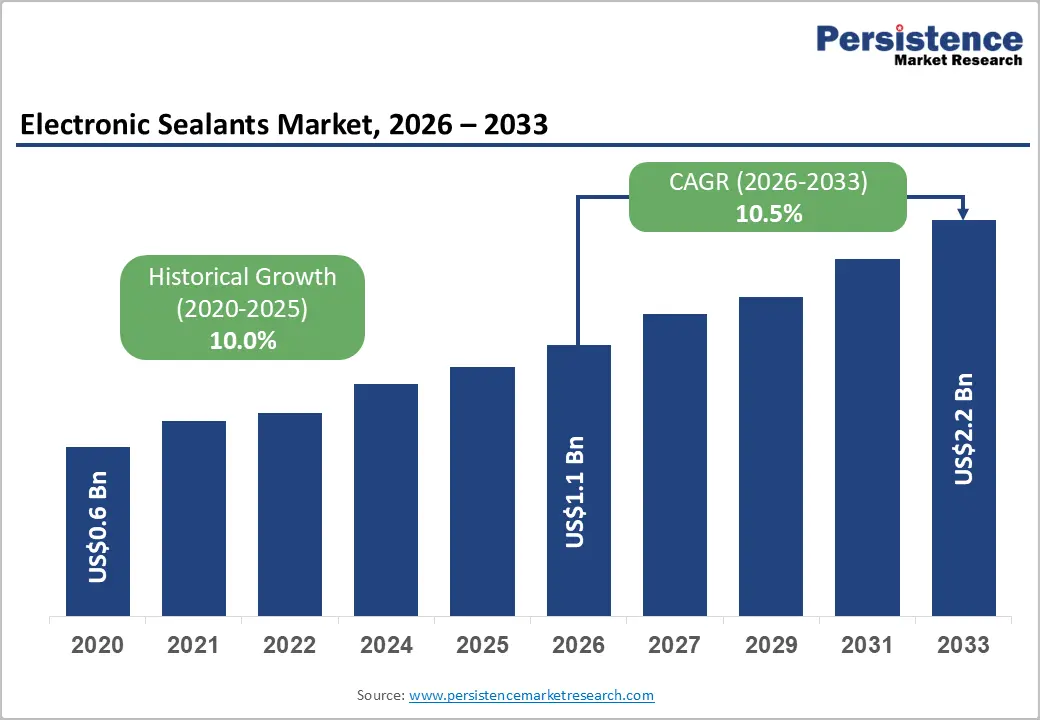

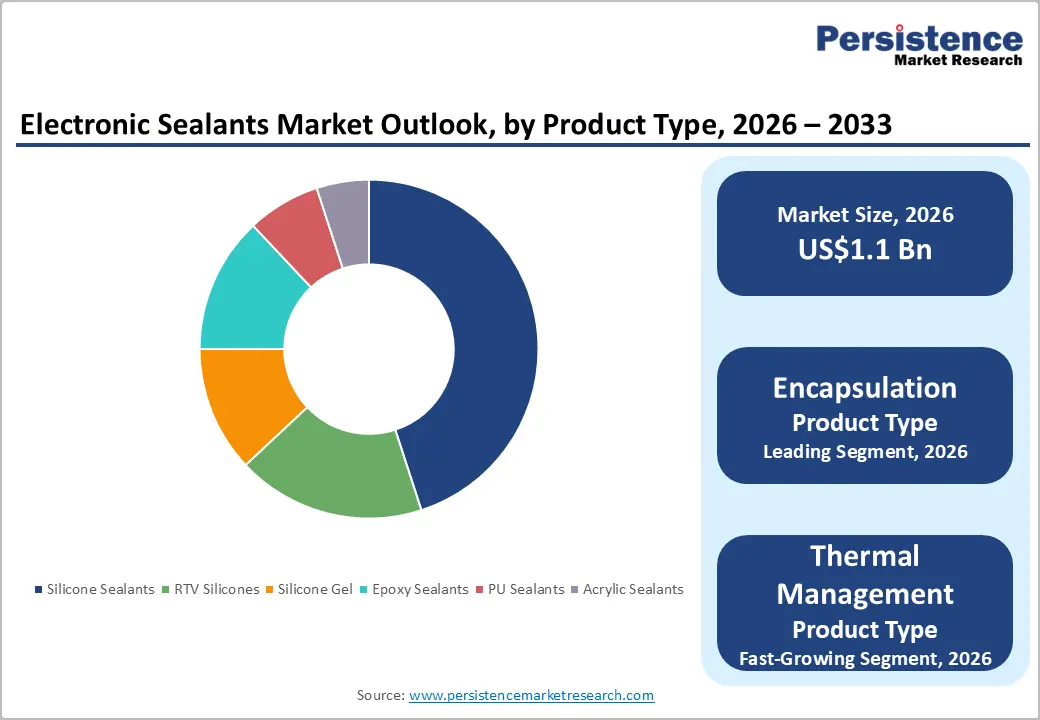

The global electronic sealants market size is likely to be valued at US$1.1 billion in 2026, and is expected to reach US$2.2 billion by 2033, growing at a CAGR of 10.5% during the forecast period from 2026 to 2033, driven by the increasing prevalence of miniaturization in consumer electronics, rising demand for high-performance protection against moisture, dust, vibration, and thermal cycling, and growing adoption of advanced sealing solutions in electric vehicles and 5G infrastructure.

Advances in low-VOC, thermally conductive, and flame-retardant formulations are further boosting uptake by offering better reliability and compliance with RoHS and REACH standards. Increasing recognition of electronic sealants as critical for extending product lifespan, preventing corrosion, and ensuring reliability in emerging 5G, EV, and IoT markets remains a major driver of market growth.

Key Industry Highlights:

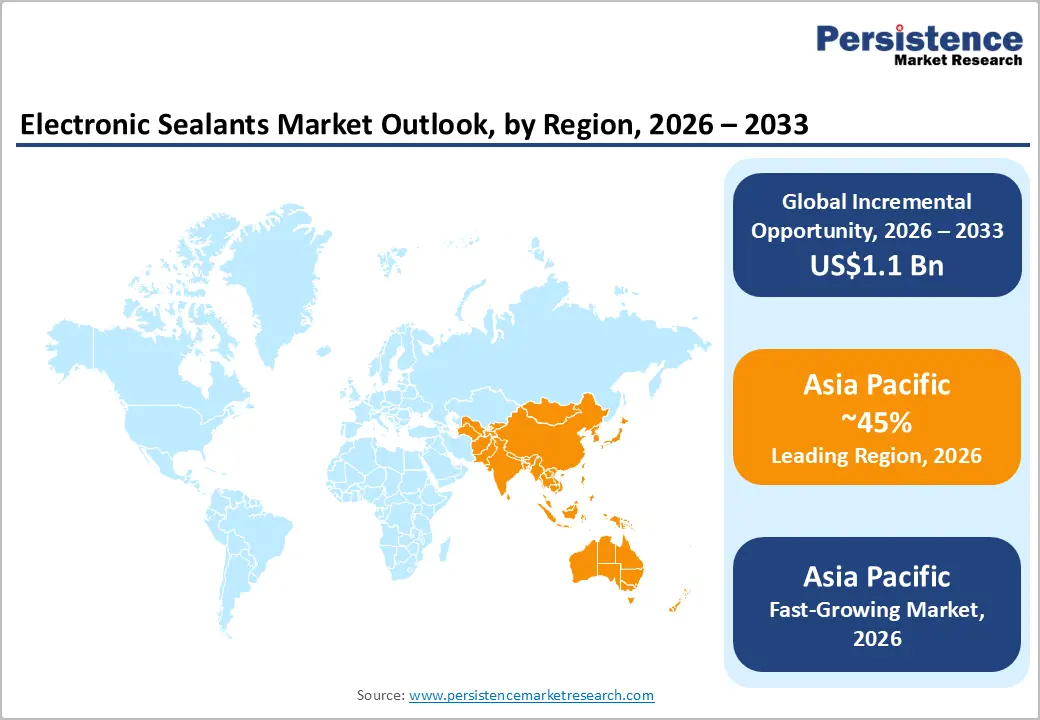

- Leading Region: Asia Pacific, anticipated to account for a 45% market share in 2026, driven by dominant electronics manufacturing, rapid EV adoption, and strong demand in China and Taiwan.

- Fastest-growing Region: Asia Pacific, fueled by expanding 5G rollout, increasing consumer electronics production, and growing automotive electrification in India and Southeast Asia.

- Dominant Product Type: Silicone sealants, to hold approximately 45% of the market share, as they remain the most versatile and widely used material.

- Leading Application: Encapsulation, contributing nearly 38% of the market revenue, due to the highest volume usage in component protection.

| Key Insights | Details |

|---|---|

|

Electronic Sealants Market Size (2026E) |

US$1.1 Bn |

|

Market Value Forecast (2033F) |

US$2.2 Bn |

|

Projected Growth CAGR (2026-2033) |

10.5% |

|

Historical Market Growth (2020-2025) |

10.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Miniaturization and 5G/EV Electronics Boom

The rapid shrinkage of electronic components, often called miniaturization, paired with surging demand for 5G connectivity and electric vehicle (EV) systems, is transforming electronics industries worldwide. Production of smaller, more efficient microchips is central to this shift, as governments are actively boosting domestic capabilities; for example, India’s semiconductor market was valued at about US$38 billion in 2023 and is projected to reach around US$109 billion by 2030 to support applications from smartphones to automotive systems. Compact semiconductors enable advanced 5G devices and high-performance controllers in EVs, enhancing connectivity and power management. 5G subscriber bases are expanding rapidly, too: India recorded 365 million 5G users with rising data use, demonstrating government-monitored uptake of next-generation networks.

Growth in EV and 5G electronics is reinforced by policy support and infrastructure expansion, requiring ever-smaller components to fit into space-constrained modules and vehicle platforms. As electric vehicles become more prevalent, electric powertrains and connectivity systems depend on dense power electronics and microcontrollers, which are increasingly sophisticated yet compact. Worldwide, cumulative EV sales and 5G base station deployments reflect this broader electronics boom affecting manufacturing strategies and supply chains.

Increasing Regulatory Push for Reliability and Safety

Governments and regulatory bodies worldwide have significantly increased mandates aimed at enhancing reliability and safety in electronic systems, compelling manufacturers to comply with defined standards and assessments to protect consumers and critical infrastructure. In the European Union, directives such as the Radio Equipment Directive (RED) require all radio and telecom hardware to meet essential performance and safety criteria before market entry, ensuring devices operate reliably and without harmful interference. The Low Voltage Directive (LVD) establishes common safety objectives for equipment within specific voltage ranges, with products needing conformity assessments such as CE marking to legally circulate across member states. International functional safety standards such as IEC 61508 set a lifecycle-based framework for safety-related electronic systems, mandating hazard and risk assessments throughout design and operation to reduce failure probabilities.

In India, the Bureau of Indian Standards (BIS) has published safety protocols for lithium-ion batteries used in EVs, prescribing test methodologies and performance requirements to minimize hazards and reinforce trust in electrified mobility. Regulatory emphasis extends to telecom and wireless sectors, where bodies enforce testing and certification procedures to verify equipment reliability and adherence to electromagnetic and cybersecurity norms before deployment. Telecom certification procedures, such as TEC 93009:2024 in India, lay out mandatory testing and conformity processes for telecommunications equipment, embedding reliability checks into the product approval system.

Barrier Analysis – Technical Barriers for Advanced Compliance

Meeting advanced compliance requirements creates technical barriers that slow adoption and raise execution risk across electronics and industrial equipment manufacturing. Modern safety, reliability, and cybersecurity regulations require design teams to embed fault tolerance, redundancy, secure boot, and real-time monitoring into hardware and firmware. Indian regulations for telecommunications equipment mandate conformity assessment and testing under MTCTE, covering electromagnetic compatibility, safety, and network security parameters.

Government data show that India has over 1.17 billion telecom subscribers as of 2024, raising the criticality of network reliability and equipment integrity on a national scale. EV and battery safety norms issued by the Bureau of Indian Standards require rigorous abuse testing, thermal stability validation, and traceability controls, expanding design complexity for power electronics and control units.

Limited Testing and Certification Infrastructure

Limited testing and certification infrastructure creates approval bottlenecks across regulated electronics and industrial equipment segments. India’s compulsory telecom equipment certification framework requires accredited laboratories for safety, electromagnetic compatibility, and network security testing. Government figures list 1,459 telecom equipment types under mandatory certification as of 2024, expanding demand for lab capacity beyond current availability. Limited slots extend waiting times for test bookings, pushing product validation milestones, and delaying commercial rollout across connected devices.

EV and battery safety compliance also depends on specialized facilities for abuse testing, thermal stability checks, and performance verification. Public listings of national quality infrastructure show a concentration of accredited labs in major cities, leaving emerging manufacturing clusters with access gaps. Travel, logistics, and queue times raise compliance costs and stretch development cycles.

Opportunity Analysis – Growth in Thermally Conductive and Low-Outgassing Sealants

Demand for thermally conductive and low-outgassing sealants is rising as electronics, automotive, and aerospace systems require materials that can effectively manage heat and maintain performance in confined environments. As electronic components become smaller and more powerful, efficient heat dissipation is critical to prevent overheating and failure. Thermally conductive sealants bridge gaps between heat-generating parts and heat sinks, improving thermal paths without introducing mechanical stress. Low-outgassing formulations are essential for sealed and vacuum-sensitive applications, such as aerospace electronics and advanced sensors, where volatile byproducts can contaminate optical surfaces, degrade insulation, and impair long-term reliability. Government technical standards and procurement documents for space and defense systems increasingly specify limits on volatile content and require certification of materials used in critical assemblies to avoid contamination at micro- and nano-scales.

In electric vehicles (EVs) and 5G communications equipment, thermal and environmental stresses are more severe due to higher power densities and extended duty cycles. Materials that conduct heat efficiently while resisting chemical breakdown under temperature cycling help enhance the lifetime of batteries, power modules, and RF front-ends. Recently published guidelines for electronics packaging outline acceptable outgassing rates and thermal performance metrics for adhesives and sealants used in high-reliability systems.

Data Centers and AI Hardware Cooling

Data centers and AI hardware cooling drive strong demand for thermally conductive and low-outgassing sealants as compute density rises inside compact enclosures. High-power GPUs, accelerators, and memory stacks generate intense localized heat that must be moved efficiently from chips to cold plates and heat sinks. Government figures show India’s data center capacity is expanding rapidly to support cloud and AI workloads; the Ministry of Electronics and Information Technology reported sustained growth in digital infrastructure investment and new data center projects to meet surging compute demand. Higher rack power densities increase thermal stress on interfaces and seals, pushing the adoption of gap fillers and sealants with stable conductivity across temperature cycling and vibration.

Low-outgassing performance matters in tightly sealed server modules and liquid-cooling loops where volatile residues can foul optics, sensors, and connectors over long duty cycles. In the U.S., the U.S. Department of Energy highlights data centers as major electricity consumers, with efficiency programs promoting advanced thermal management to curb heat losses and improve uptime. As operators shift toward direct-to-chip liquid cooling and rear-door heat exchangers, materials that transfer heat while staying chemically inert protect performance and reliability.

Category-wise Analysis

Product Type Insights

Silicone Sealants are anticipated to dominate the market, accounting for 45% of the market share in 2026. Their dominance is driven by their performance fit across high-reliability electronics, EV power modules, and data center cooling assemblies. These materials retain elasticity across wide temperature ranges, maintain stable thermal pathways between heat sources and sinks, and resist moisture, vibration, and UV exposure. Low-outgassing formulations protect sensitive optics, sensors, and connectors in sealed enclosures and liquid-cooling loops. Strong adhesion to metals, ceramics, and polymers supports compact packaging and miniaturized designs. Dow Silicones Corporation’s DOWSIL™ TC-6015 thermally conductive silicone encapsulant, designed to enhance heat dissipation in power electronics used in renewable energy systems, EV chargers, and 5G networking gear. The product integrates into power modules and high-power inverters to help manage thermal loads as these components shrink and operate at higher current densities.

Epoxy sealants are likely to be the fastest-growing product type, as they combine strong mechanical strength, excellent adhesion, and robust thermal performance, making them ideal for demanding electronics and industrial applications. In high-stress environments such as power modules, EV battery packs, and aerospace assemblies, epoxy formulations form rigid bonds that resist vibration, shock, and thermal cycling better than many flexible chemistries. 3M™ Thermally Conductive Epoxy Adhesive TC-2810 is a two-part epoxy sealant used in automotive, aerospace, and electronics applications to bond and thermally manage power modules and circuit assemblies. It offers good gap filling, high adhesive strength, and decent thermal conductivity (about 0.8–1.4 W/m·K) while maintaining low outgassing and electrical insulation features important for reliability under thermal stress.

Application Insights

The encapsulation segment is expected to dominate the market, contributing nearly 38% of revenue in 2026, fueled by rising use in EV power electronics, data center hardware, and telecom equipment. Encapsulation protects sensitive components from moisture, dust, vibration, and thermal shock while enabling efficient heat transfer away from hotspots. High-power modules, battery management systems, and RF units operate under dense packaging and continuous loads, raising the need for robust environmental sealing and thermal stability. Encapsulants extend service life, reduce failure rates, and support compact designs. For example, large electronics manufacturers routinely encapsulate components while also participating in thermal blend trials, ensuring devices receive specialized, protective solutions with high standards. Loctite Stycast 2651MM Epoxy Encapsulant is an epoxy-based encapsulant widely used to protect electronic assemblies in aerospace, automotive, and industrial applications. This material provides high mechanical strength, excellent thermal stability, and robust environmental sealing, ensuring sensitive components are safeguarded against moisture, vibration, and extreme temperatures during operation.

Thermal management represents the fastest-growing application, as power densities rise in EV electronics, data centers, and 5G infrastructure. High-performance processors, power modules, and battery systems generate concentrated heat that must be dissipated to protect reliability and efficiency. Compact packaging and higher rack loads intensify thermal stress at interfaces, driving adoption of conductive sealants, gap fillers, and encapsulants that move heat from hotspots to heat sinks or cold plates. For example, thermal brands such as Momentive provide walk-in lines for conductive sealants, making cooling solutions more accessible to global populations while reducing pressure on encapsulation-only alternatives. Thermally Conductive Compound (Dow TC 5622) is used by electronics OEMs to bridge heat-producing power modules and heat sinks in high-density applications such as data centers and EV inverters. This thermally conductive paste helps move heat away from components to cooling hardware, reducing junction temperatures and improving system reliability.

Regional Insights

North America Electronic Sealants Market Trends

North America's growth is supported by the region’s high electronics R&D, strong aerospace & defense demand, and high public awareness of reliability benefits. Distribution systems in the U.S. and Canada provide extensive support for electronic sealants programs, ensuring wide accessibility across silicone sealants, encapsulation, and consumer electronics populations. Increasing demand for high-reliability, convenient, and easy-to-apply forms is further accelerating adoption, as these formats improve device longevity and reduce barriers associated with harsh environments.

Innovation in electronic sealants technology, including stable thermally conductive, improved low-outgassing delivery, and targeted EV enhancement, is attracting significant investment from both public and private sectors. Government initiatives and IPC campaigns continue to promote use against failure risks, thermal concerns, and emerging reliability threats, creating sustained market demand. The growing focus on gap filler grades and specialty uses, particularly for consumer electronics and others, is expanding the target applications for electronic sealants.

Europe Electronic Sealants Market Trends

Europe is witnessing the steady growth powered by increasing awareness of electronic reliability benefits, strong regulatory systems, and government-led green electronics programs. Countries such as Germany, France, the U.K., and the Netherlands have well-established electronics frameworks that support routine electronic sealant use and encourage adoption of innovative low-VOC delivery methods. These high-compliance formulations are particularly appealing for encapsulation populations, regulation-conscious manufacturers, and automotive users, improving reliability and coverage rates.

Technological advancements in electronic sealants development, such as enhanced thermal conductivity, application-targeted delivery, and improved silicone gel grades, are further boosting market potential. European authorities are increasingly supporting research and trials for sealants against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, sustainable options is aligned with the region’s focus on preventive failure reduction and RoHS compliance. Public awareness campaigns and promotion drives are expanding reach in both consumer electronics and automotive segments, while suppliers are investing in advanced polymers and novel variants to increase efficacy.

Asia Pacific Electronic Sealants Market Trends

Asia Pacific is projected to dominate and be the fastest-growing, accounting for 45% revenue in 2026, propelled by rising electronics manufacturing awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, South Korea, Taiwan, and India are actively promoting sealant campaigns to address 5G and EV growth and emerging reliability needs. Electronic sealants are particularly attractive in these regions due to their cost-effective administration, ease of adoption, and suitability for large-scale consumer electronics and automotive drives in both urban and semi-urban populations.

Technological advancements are supporting the development of stable, effective, and easy-to-apply electronic sealants, which can withstand challenging production conditions and minimize failure dependence. These innovations are critical for reaching domestic OEMs and improving overall device reliability. Growing demand for silicone sealants, encapsulation, and consumer electronics applications is contributing to market expansion. Public-private partnerships, increased electronics expenditure, and rising investment in sealant research and production capacity are further accelerating growth. The convenience of sealant delivery, combined with improved protection and reduced risk of failure, positions it as a preferred choice.

Competitive Landscape

The global electronic sealants market shows intense competition between established chemical leaders and fast-moving specialty material providers. In North America and Europe, Dow Inc. and Henkel lead through sustained R&D investment, global manufacturing footprints, and deep OEM relationships, supported by advanced silicone and thermally conductive product lines. These capabilities enable rapid customization for EV power electronics, data centers, and telecom hardware, strengthening long-term supply agreements.

In Asia Pacific, regional manufacturers scale cost-competitive solutions that widen access for high-volume electronics assembly, accelerating adoption across consumer devices and industrial equipment. Improved silicone sealant delivery enhances reliability, lowers failure rates, and supports mass integration in compact designs. Strategic partnerships, technology collaborations, and targeted acquisitions combine formulation expertise with application engineering, shortening qualification cycles and speeding commercialization. Low-outgassing chemistries address contamination risks in sealed modules and vacuum-exposed systems, supporting deeper penetration into aerospace, optics, and high-reliability electronics segments.

Key Industry Developments:

- In November 2025, Henkel said it enabled the transition toward zero-emission mobility and launched Loctite SI 5643 and Loctite SI 5637 to strengthen its pioneering role in e-mobility solutions. The company developed these products in close partnership with OEMs, battery manufacturers, and automotive suppliers to address emerging challenges in thermal management for power conversion and eDrive systems.

- In September 2025, Dow Inc. launched DOWSIL™ EG-4175 Silicone Gel, a highly reliable protective solution for next-generation insulated gate bipolar transistor (IGBT) modules that operated at higher voltages. The company introduced this advanced material to withstand the higher temperatures associated with these IGBTs and to improve reliability, reduce power losses, and increase power efficiency in electric vehicle (EV) batteries and inverters used for photovoltaic (PV) panels and wind turbines.

Companies Covered in Electronic Sealants Market

- Dow Inc.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Momentive Performance Materials

- Shin-Etsu Chemical Co., Ltd.

- Wacker Chemie AG

- Parker Hannifin (Chomerics)

- Master Bond

- LORD Corporation (Parker)

- Elkem Silicones

Frequently Asked Questions

The global electronic sealants market is projected to reach US$1.1 billion in 2026.

Higher heat loads in compact electronics increase demand for thermally conductive, low-outgassing sealants to improve reliability and prevent thermal failures.

The electronic sealants market is poised to witness a CAGR of 10.5% from 2026 to 2033.

Expansion of advanced cooling architectures creates demand for sealants compatible with fluids, pressure cycling, and long-duty operation in AI servers and power modules.

Dow Inc., Henkel AG & Co. KGaA, Momentive Performance Materials, H.B. Fuller Company, and Shin-Etsu Chemical Co., Ltd. are the key players.