- Retail

- Electronic Equipment Repair Service Market

Electronic Equipment Repair Service Market Size, Share, and Growth Forecast, 2026 – 2033

Electronic Equipment Repair Service Market by Product Type (Consumer Electronics, Home Appliances, Industrial Equipment, IT & Telecom Equipment, Others), Service Type (Warranty Services, Out-of-Warranty Services, Preventive Maintenance, Others), End-User (Residential, Commercial, Industrial), and Regional Analysis for 2026-2033

Electronic Equipment Repair Service Market Share and Trends Analysis

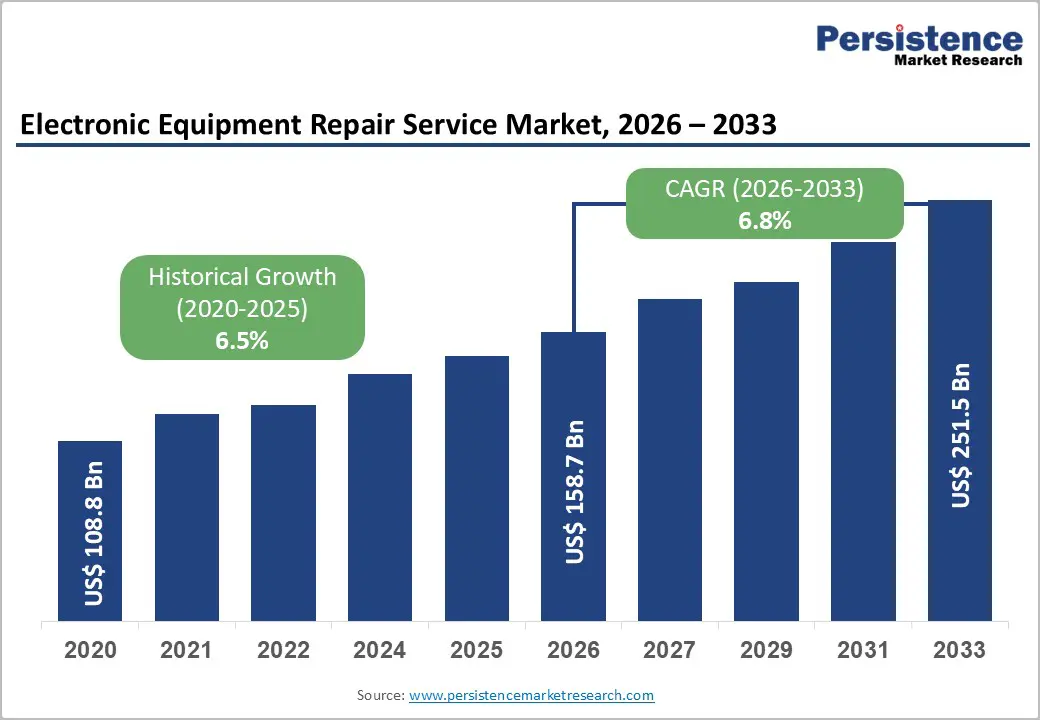

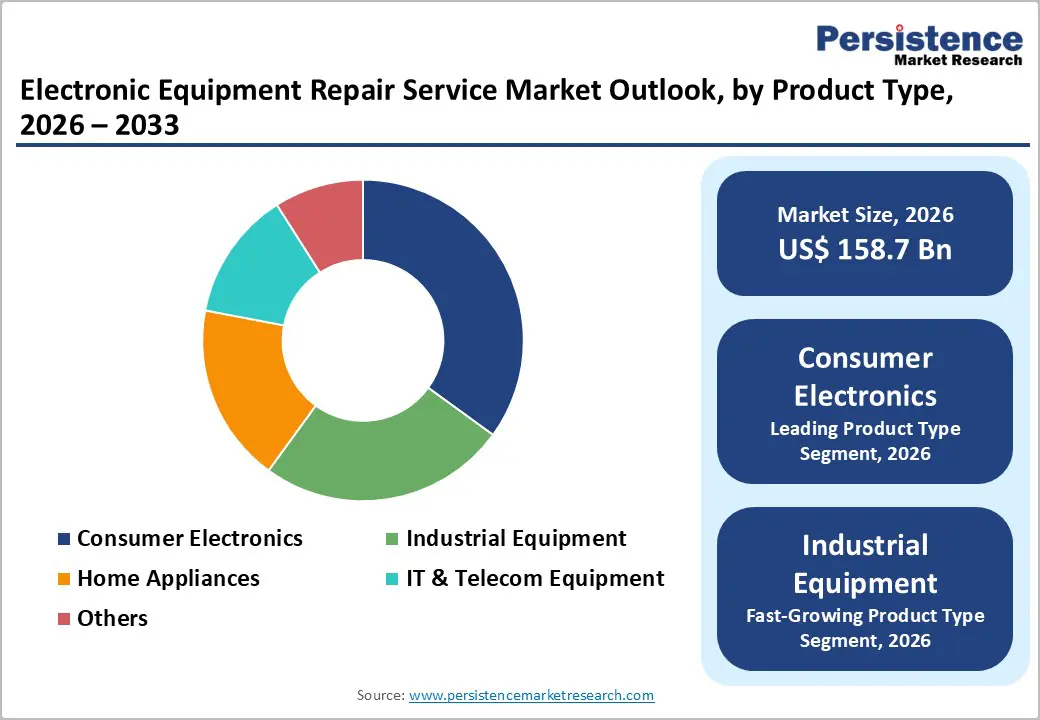

The global electronic equipment repair service market size is likely to be valued at US$ 158.7 billion in 2026, and is projected to reach US$ 251.5 billion by 2033, growing at a CAGR of 6.8% during the forecast period 2026−2033.

Growth in the market is primarily driven by increased reliance on electronic equipment across residential, commercial, and industrial sectors, which expands service demand. Rising adoption of advanced technologies such as Internet of Things (IoT)-enabled devices and smart home appliances increases the complexity and frequency of repair requirements.

Expansion of digital infrastructure and networked communication systems supports service accessibility, enabling faster diagnosis, remote troubleshooting, and predictive maintenance solutions. Demographic trends, including urbanization and a growing middle-class population in emerging economies, contribute to higher electronic consumption and subsequent service requirements. Investments in healthcare, education, and industrial automation indirectly fuel demand for repair services by increasing device utilization and critical uptime expectations. Regulatory frameworks mandating safety, performance standards, and warranty compliance further incentivize professional service engagement.

Key Industry Highlights

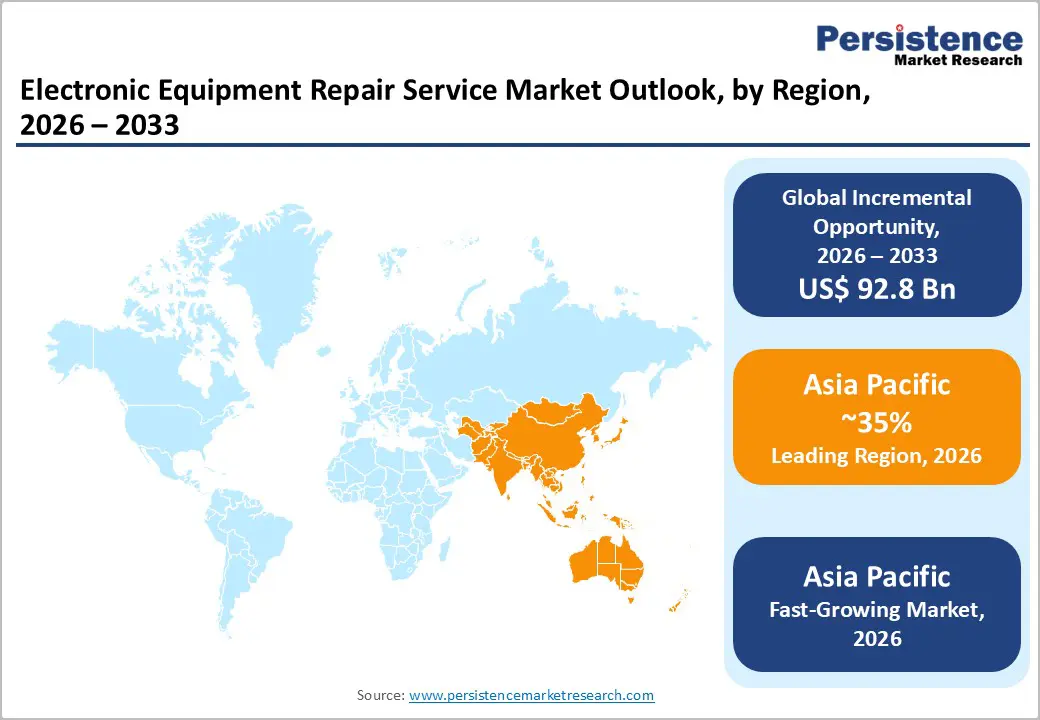

- Dominant Region: Asia Pacific is expected to dominate with an estimated 35% share in 2026, driven by high device adoption, dense production hubs, and widespread smart appliance use.

- Fastest-growing Market: Asia Pacific is poised to be the fastest-growing market through 2033, supported by rising device ownership and increasing adoption of digital service platforms.

- Leading Product Type: Consumer electronics is projected to hold a revenue share of about 35% in 2026, fueled by high usage frequency and intensifying demand for certified repair services.

- Fastest-growing Product Type: Industrial equipment is slated to register the fastest growth during 2026–2033, driven by automation adoption and IoT-enabled predictive maintenance.

- September 2025: Back Market launched a new repair platform in Europe, allowing customers and non-customers to access smartphone and tablet repairs with guarantees and potential trade-in vouchers.

| Key Insights | Details |

|---|---|

|

Electronic Equipment Repair Service Market Size (2026E) |

US$ 158.7 Bn |

|

Market Value Forecast (2033F) |

US$ 251.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Complexity and Proliferation of Electronic Devices

The sustained growth in demand for repair services is influenced by the expanding variety and sophistication of electronic products in use. Modern systems draw on interconnected technologies such as embedded sensors, complex hardware, firmware, and cloud communication layers, making fault diagnosis and restoration more intricate than in legacy devices. Devices such as smartphones, Internet-connected appliances and industrial controllers operate with miniaturized components and proprietary designs, necessitating highly skilled diagnostics and component-level repair routines rather than simple part replacement. This technical depth expands the range of service needs across residential, commercial and industrial sectors, increasing opportunities for professional service providers to meet detailed troubleshooting, software calibration and hardware restoration requests that general maintenance cannot address.

Voluminous electronic unit expansion amplifies this service need. The U.S. National Institute of Standards and Technology (NIST) notes projections of more than 75 billion Internet-connected devices in operation by 2025, indicating vast penetration of IoT technologies into everyday infrastructure and assets as per government research guidance. As the installed base of complex electronics expands, both end users and enterprises require access to professional repair functions to sustain performance, manage downtime risks and defer costly full replacements.

Growing Emphasis on Sustainability and Cost Efficiency

The demand for electronic equipment repair services is increasingly influenced by corporate and consumer priorities focused on environmental sustainability. Organizations face regulatory pressure and stakeholder expectations to reduce electronic waste, leading to extended product lifecycles through maintenance and repair. Companies adopt repair strategies to limit resource consumption and avoid premature disposal, aligning with circular economy practices. Consumers also show preference for refurbished or repaired electronics, driven by awareness of ecological impact and desire to reduce carbon footprint. This shift promotes steady growth in service providers offering advanced diagnostics, component-level repairs, and value-added maintenance contracts.

Cost efficiency drives adoption of repair services as businesses seek to optimize capital expenditure on electronic assets. Repair and maintenance offer financial advantages over full equipment replacement, enabling organizations to maximize return on investment while maintaining operational continuity. Supply chain disruptions and rising component costs further reinforce reliance on repair and refurbishment solutions. Service providers benefit from recurring revenue opportunities through preventive maintenance agreements and performance optimization programs, enhancing financial predictability. Operational efficiency gains achieved through timely repair interventions reduce downtime, support productivity, and strengthen overall asset management strategies.

Limited Access to Genuine Parts and Specialized Tools

Restricted availability of authentic parts and specialized diagnostic and repair tools significantly dampens operational efficiency in the electronic equipment repair industry because manufacturers commonly control distribution and usage rights for these inputs. Such control creates a bottleneck for independent service providers by forcing them to depend on original equipment manufacturer (OEM) supply chains, which often prioritise authorised service centres and limit third party access to parts, repair manuals and proprietary software. This increases turnaround times and input costs for repair businesses, shrinking their competitive edge against manufacturer repair networks and often compelling end users to replace devices rather than repair them. In the U.S., for example, widely adopted Digital Fair Repair Act provisions require OEMs to offer parts, tools and manuals to independent providers, signaling that, absent such mandates, restricted access is a prevalent issue in broader electronics maintenance ecosystems.

The underlying cause of these limitations is rooted in intellectual property protection and commercial strategy. OEMs assert that unrestricted distribution of spare parts and specialised tools could compromise trade secrets, device security and brand integrity, and therefore tightly regulate who can obtain and use these assets. This strategy can fragment repair markets into authorised and unauthorised segments, constraining smaller operators’ ability to procure critical inputs at fair prices and under fair conditions. Government initiatives such as India’s Right to Repair India portal aim to ease such barriers by expanding access to repair information and parts for consumer electronics and durables, indicating recognition of the issue at policy level.

Short Product Lifecycles and Rapid Obsolescence

Rapid product turnover and accelerated obsolescence stem from a combination of technology evolution, consumer expectations, and product design decisions that emphasize frequent upgrades over longevity. Moore’s Law and similar industry dynamics drive manufacturers to push new capabilities at regular intervals, reducing the commercial viability of older technologies within a few years of release. This engineering driven shortening of practical product lifespans is a principal cause of premature disposal and increasing waste globally, as highlighted in government linked research showing only about 22.3% of electronic waste generated worldwide was formally collected and recycled in 2022 indicating a large volume of equipment leaving the productive cycle early.

Policy frameworks in major economies increasingly reflect concern over such trends, mandating extended producer responsibility and transparency in lifecycle information to support reuse. European Union requirements for Digital Product Passports and ecodesign standards seek to record durability, maintenance, and end of life data to improve repair and reuse outcomes. Yet, many devices still reach end of service within a few years as software updates cease or parts become unavailable, creating gaps that complicate maintenance and repair efforts by third party technicians.

Integration of Digital and Predictive Maintenance Technologies

Digital diagnostics and predictive monitoring platforms are redefining maintenance economics by shifting service models from reactive breaks and fixes to real-time condition monitoring and failure anticipation. By embedding networked sensors and analytics engines that continuously assess operational signals such as vibration, temperature and electrical load, service providers can plan interventions before faults escalate to costly breakdowns, reducing unplanned downtime and improving equipment utilization. U.S. government research highlights the role of artificial intelligence driven predictive maintenance in helping small manufacturers avoid costly downtime by identifying failure precursors and scheduling service interventions before a breakdown occurs, illustrating the tangible operational value of these technologies in 2025.

Cloud enabled dashboards and machine learning models further enhance predictive capabilities by contextualizing historical and live performance data, enabling more accurate fault forecasting and continuous improvement of maintenance protocols. Integrating digital twins, virtual replicas of physical assets, with predictive models fosters remote diagnostics and guided repair workflows that limit field dispatches and reduce logistics costs. As more operators adopt these systems to benchmark performance and optimize service planning, predictive maintenance strengthens competitive positioning by lowering total cost of ownership and improving customer satisfaction.

Accelerating Device Penetration in Emerging Economies

Emerging economies are witnessing a rapid increase in ownership of digital devices across urban and rural populations as national infrastructure campaigns extend connectivity and affordability. Official information from an Indian government press release notes significant growth in wireless subscriptions and broader network coverage in 2025, illustrating a large installed base of mobile and connected hardware in markets previously underserved by formal service channels. With more consumers and enterprises relying on this hardware for communication, commerce and services, the incidence of functional issues and demand for timely support rises. Professional service channels that establish reliable repair capacity, transparent pricing and consistent quality stand to convert latent demand into sustainable revenue streams.

Policy emphasis on digital inclusion and incentives for local enterprise further stimulates addressable need for technical maintenance and service delivery. Government efforts to promote digital access, competition among service providers and consumer awareness contribute to a landscape where end users seek dependable support over the lifecycle of their products. Companies that align operational footprints with emerging demand corridors can achieve scale while mitigating logistical friction. Strategic partnerships with local stakeholders, investment in service hubs and responsive customer care models reinforce market presence and operational resilience.

Category-wise Analysis

Product Type Insights

Consumer electronics is anticipated to secure around 35% of the electronic equipment repair service market revenue share in 2026, reflecting widespread adoption of smartphones, laptops, tablets, and wearable devices. High usage frequency, rapid technological upgrades, and short device life cycles create recurring repair demand. Professional repair services gain traction due to warranty compliance, device sensitivity, and consumer preference for certified technicians. Retail penetration and urban concentration allow efficient service delivery, while digital diagnostic tools and remote troubleshooting enhance accessibility. Service providers leverage these factors to optimize operational efficiency, minimize turnaround time, and maintain quality standards. Increasing awareness of device performance preservation, supported by regulatory requirements and manufacturer-endorsed repair programs, further consolidates market leadership.

Industrial equipment is expected to be the fastest-growing segment during the 2026–2033 forecast period, propelled by adoption of automation, robotics, and manufacturing machinery. High capital expenditure and critical operational dependence incentivize companies to employ professional repair and preventive maintenance services. Integration of IoT-enabled sensors and predictive maintenance platforms improves monitoring of machinery health, reducing unplanned downtime and increasing repair service adoption. Growth is further supported by expanding industrialization in emerging markets and regulatory mandates for workplace safety and operational efficiency. Service providers are increasingly offering specialized solutions, including on-site diagnostics, remote monitoring, and performance optimization, enhancing the commercial scope.

Service Type Insights

Warranty services are poised to dominate with a forecasted market share of over 40% in 2026, powered by consumer trust in manufacturer-backed service solutions. Devices under warranty incentivize users to engage professional repair networks to maintain compliance and preserve functionality. Structured service protocols, trained technicians, and digital tracking systems ensure timely and standardized interventions, enhancing adoption across residential and commercial users. Regulatory frameworks mandating warranty obligations further reinforce demand for certified repair providers. High urban concentration and retail partnerships allow quick response times, reducing operational risk for both providers and consumers.

Preventive maintenance is estimated to be the fastest-growing segment from 2026 to 2033, fueled by increasing recognition of equipment longevity and operational continuity benefits. Businesses and consumers are prioritizing scheduled inspections, system calibration, and performance optimization to avoid costly downtime and service disruptions. Technological tools such as IoT-based monitoring and AI-driven diagnostics facilitate predictive maintenance, enhancing efficiency and service reliability. Expansion of subscription-based preventive service models allows providers to secure recurring revenue while improving customer engagement. Increasing adoption in industrial and commercial sectors, supported by regulatory compliance and operational risk reduction mandates, reinforces growth potential.

Regional Insights

North America Electronic Equipment Repair Service Market Trends

North America commands a substantial portion of the global demand for electronic equipment repair services, supported by high device penetration across consumer, commercial, and industrial segments. Widespread adoption of smartphones, laptops, smart home appliances, and connected industrial machinery generates continuous demand for maintenance, calibration, and post-warranty support. Advanced infrastructure and dense urbanization facilitate rapid service delivery, with established networks of authorized service centers and certified independent providers ensuring operational reliability. Consumers and businesses increasingly prioritize minimal downtime, driving demand for faster turnaround, on-site repair solutions, and preventive maintenance contracts. Strong integration of digital diagnostic tools and inventory management platforms allows service operators to optimize resource allocation, reduce parts shortages, and maintain consistent service quality across multiple service hubs.

Growth dynamics in the market are influenced by regulatory emphasis on electronics sustainability and product longevity, prompting manufacturers and service providers to align operations with repairability standards. High-value devices such as commercial servers, networking equipment, and industrial automation systems extend serviceable lifecycles, generating recurring revenue opportunities for skilled technicians and specialized repair firms. Shifts in consumer expectations toward eco-conscious consumption and reduced electronic waste encourage adoption of structured repair services over replacement. Strategic partnerships with equipment manufacturers, technology integrators, and logistics providers enable coordinated service solutions that meet rising demand for reliability and convenience.

Europe Electronic Equipment Repair Service Market Trends

Europe demonstrates a strong presence in the market for electronic equipment repair services, boosted by high technology adoption and regulatory emphasis on sustainability and product longevity. Advanced economies within this landscape maintain dense networks of service centers and authorized repair facilities, ensuring accessibility for both consumer electronics and industrial equipment. Government regulations promoting extended warranty, right-to-repair, and electronic waste reduction elevate demand for structured maintenance solutions. Consumers exhibit high expectations for service quality, turnaround time and compliance with environmental standards, pushing providers to adopt digital diagnostic tools, predictive maintenance, and multi-channel service models. Established industrial bases also contribute to steady demand for specialized maintenance, calibration and refurbishment of machinery, further reinforcing the service ecosystem.

Economic stability and high per capita income drive willingness among households and enterprises to invest in premium repair and maintenance services. Partnerships between service providers and manufacturers for certified repairs strengthen brand trust and foster repeat engagements, enhancing revenue predictability. Growing focus on circular economy initiatives encourages refurbishment and parts reuse, creating incremental business opportunities for professional service operators. Trends in remote diagnostics, app-based scheduling and doorstep repair support adoption among tech-savvy populations, extending service reach without substantial infrastructure expansion.

Asia Pacific Electronic Equipment Repair Service Market Trends

Asia Pacific is expected to dominate with an estimated 35% of the electronic equipment repair service market share in 2026, reflecting both scale and expansion momentum within this landscape. That performance is rooted in concentrated production and consumption of electronics across major economies, creating a dense installed base of devices requiring maintenance, recalibration and service interventions. Manufacturing hubs such as China and India generate significant volumes of consumer and industrial hardware, lowering costs and fostering an ecosystem of authorized centers and independent service operators that can operate at scale and price points attractive to a broad customer base. High utilization rates of personal electronics, widespread adoption of smart appliances and rapid deployment of connected industrial equipment elevate serviceable units per capita, amplifying workload intensity for service networks.

Asia Pacific is also forecasted to be the fastest-growing market for electronic equipment repair service through 2033, stimulated by a diverse mix of consumer segments with differing price sensitivities, strong brand engagement through authorized partnerships, and evolving regulatory focus on product lifecycle extension. Broad device ownership across smartphones, home appliances and business machinery ensures ongoing replacement cycles and post warranty service needs, while an expanding middle class shifts preferences toward cost-efficient maintenance rather than outright replacement. Strategic investments in technician training, digital service platforms and multi-channel repair models accelerate responsiveness and quality, enabling providers to scale operations rapidly in an environment where product complexity and service expectations are rising concurrently.

Competitive Landscape

The global electronic equipment repair service market structure exhibits moderate fragmentation, consisting of a combination of global service providers, regional operators, and independent technicians. Leading companies such as GE Appliances, Siemens, Honeywell International Inc, Panasonic Life Solutions India Pvt. Ltd., and SAMSUNG collectively account for roughly 45% of revenue, reflecting moderate concentration while leaving scope for strategic consolidation. Competitive dynamics are shaped by service quality, technological integration, and geographic coverage, with operators striving to maintain reliability across urban and semi-urban service corridors. Investment in certified technician programs, warranty-backed repairs, and standardized service protocols enables firms to build credibility and maintain customer trust.

Strategic partnerships with device manufacturers, distributors, and retailers further strengthen positioning by aligning service networks with product ecosystems and expanding access to high-value client segments. Subscription-based maintenance plans, preventive service programs, and specialized repair solutions contribute to recurring revenue streams and long-term customer retention. Companies that integrate advanced diagnostic tools, maintain localized spare parts inventories, and optimize workforce deployment capture a competitive edge while ensuring consistent service delivery. Market positioning relies on a combination of reliability, technological adoption, network reach, and operational efficiency, allowing leading players to balance scale with responsiveness.

Key Industry Developments

- In February 2026, Oppo India announced plans to open 110 new premium Service Center 3.0 Pro facilities across the country in 2026 to enhance after-sales experience through digital check-in, real-time queue updates, and dedicated product and gaming zones.

- In June 2025, Samsung Electronics Canada launched an Independent Service Provider program to expand nationwide access to authorized parts and certified technicians, improving out-of-warranty repair convenience for Galaxy device users.

- In June 2025, Apple awarded Tata Group the mandate to handle iPhone and MacBook repairs in India, expanding supply-chain collaboration and shifting service operations from Wistron’s local unit.

Companies Covered in Electronic Equipment Repair Service Market

- GE Appliances

- Siemens

- Honeywell International Inc

- Panasonic Life Solutions India Pvt. Ltd.

- SAMSUNG

- LG Electronics India Limited.

- BSH Home Appliances Group

- Electrolux

- Apple Inc.

- Canon.

Frequently Asked Questions

The global electronic equipment repair service market is projected to reach US$ 158.7 billion in 2026.

Rising device adoption, increasing product complexity, and growing demand for reliable post-purchase support are driving the market.

The market is poised to witness a CAGR of 6.8% from 2026 to 2033.

Widening device adoption in emerging economies and proliferation of digital service platforms presents key market opportunities.

Some of the key market players include GE Appliances, Siemens, Honeywell International, Panasonic Life Solutions India Pvt. Ltd., and SAMSUNG.