- Healthcare Services

- Electronic Health Records Market

Electronic Health Records Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Electronic Health Records Market by Product (Web-based, On-premise), Form (Acute, Post-Acute, Ambulatory), Application (Cardiology, Neurology, Radiology, Oncology, Others), End-user (Hospital, Ambulatory Surgical Centers, Others), and Regional Analysis from 2026 to 2033

Electronic Health Records Market Share and Trends Analysis

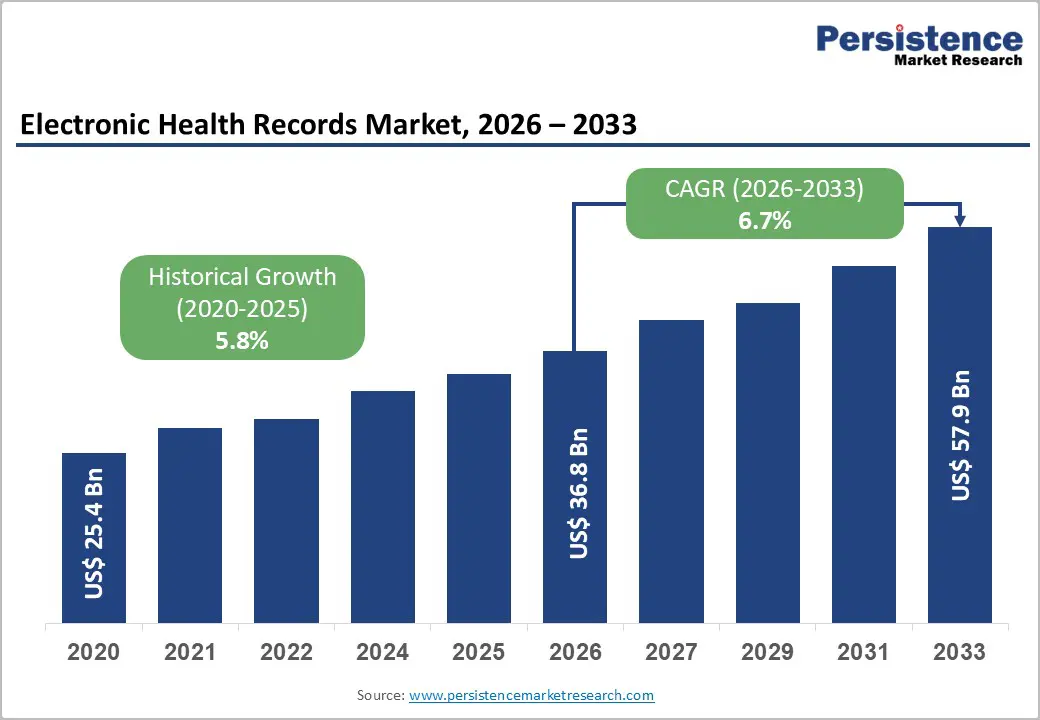

The global electronic health records market size is estimated to grow from US$ 36.8 billion in 2026 to US$ 57.9 billion by 2033. The market is projected to record a CAGR of 6.7% during the forecast period from 2026 to 2033. The global electronic health records market is growing steadily, driven by expanding telehealth, mHealth, healthcare analytics adoption, and digital care workflows. North America dominates due to advanced infrastructure and regulations, while Asia Pacific is the fastest-growing region, supported by healthcare expansion, government digital initiatives, rising patient awareness, and increasing investments in software, services, and interoperable remote monitoring solutions.

Key Industry Highlights:

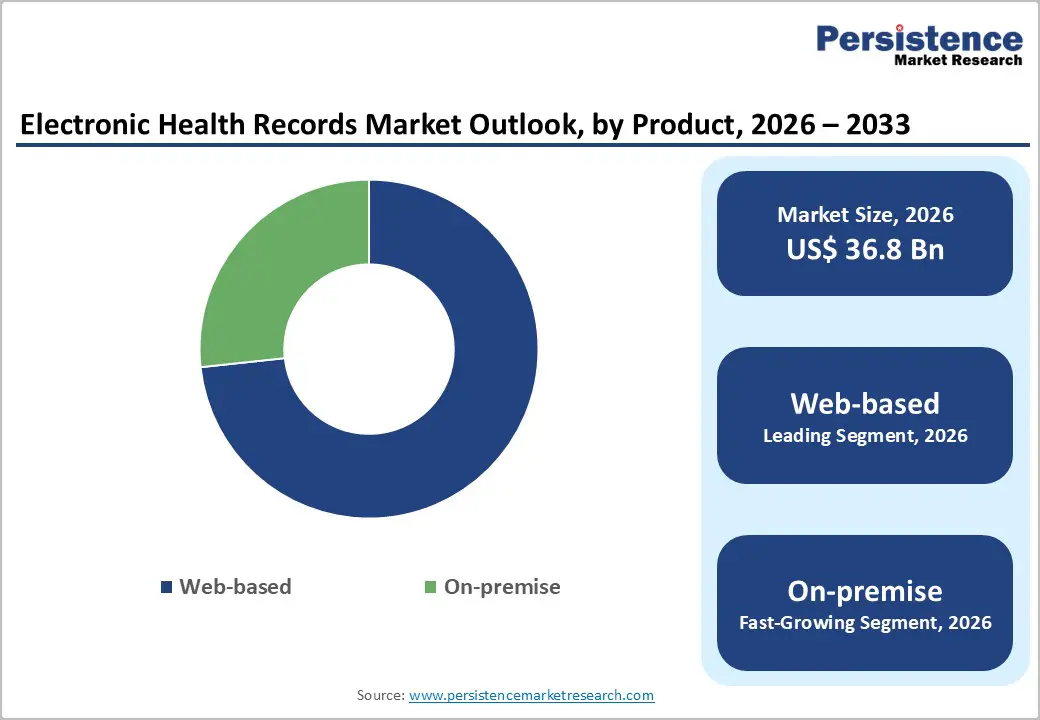

- Dominant Segment: Web-based solutions account for a dominant share as 73.3% of the Electronic Health Records (EHR) market in 2025, driven by growing preference for cloud-hosted platforms offering scalability, flexibility, and lower upfront costs. Hospitals, clinics, and ambulatory providers are increasingly adopting web-based EHRs to enable remote access, real-time data sharing, interoperability, and faster updates, supporting telehealth, analytics, and integrated care delivery.

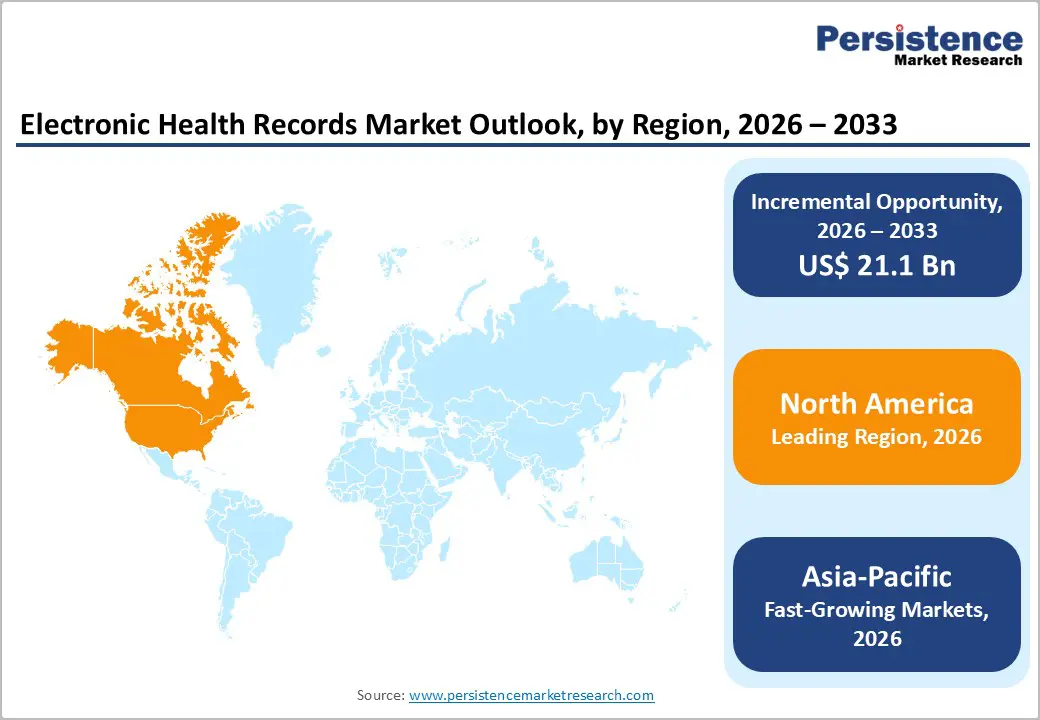

- Dominant Region: North America leads with a 50.7% share, supported by mature healthcare IT infrastructure, high EHR penetration, regulatory mandates, and favorable reimbursement frameworks. Asia Pacific is the fastest-growing region, fueled by expanding healthcare infrastructure, government digital health initiatives, rising patient awareness, and rapid adoption of cloud and mobile health solutions.

- Market Drivers: Growth is driven by rising chronic disease prevalence, increasing adoption of telehealth and value-based care, demand for efficient clinical workflows, regulatory support for digital records, and advancements in AI, cloud computing, interoperability standards, and mobile health technologies.

- Market Opportunity: Key opportunities include AI-enabled clinical decision support, cloud-native EHR platforms, interoperability and data exchange solutions, predictive analytics, population health management, remote patient monitoring integration, and rapid expansion across emerging economies with improving healthcare access and digitization efforts.

| Report Attribute | Details |

|---|---|

|

Global Electronic Health Records Market Size (2026E) |

US$ 36.8 Bn |

|

Market Value Forecast (2033F) |

US$ 57.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.8% |

Market Dynamics

Driver: Growing Adoption Rate of EHR Solutions

The accelerating adoption of EHR solutions drives significant expansion in the healthcare market. EHR systems are transforming patient care by improving data management, reducing errors, and streamlining administrative tasks.

As healthcare providers increasingly recognize the advantages of EHRs, including enhanced patient outcomes, regulatory compliance, and operational efficiency, the adoption rates are surging. Government initiatives and incentives, such as the Meaningful Use program, have been pivotal in this growth. These initiatives promote the widespread use of EHRs by offering financial support and setting performance benchmarks, encouraging healthcare facilities to transition from paper-based records to digital systems.

Additionally, technological advancements, such as cloud computing and artificial intelligence, further enhance EHR functionalities and integration capabilities. The shift towards value-based care models also supports EHR adoption. These models rely on accurate data and analytics for personalized treatment plans and effective patient health management.

As healthcare organizations strive to meet these new standards, the demand for sophisticated EHR solutions continues to rise. Consequently, the EHR market is expanding rapidly, driven by technological advancements and a growing emphasis on efficient, data-driven healthcare solutions.

Restraints: High Costs Associated with Implementing and Maintaining EHR Systems

The high costs associated with implementing and maintaining EHR systems limit their growth. Initial setup expenses, including hardware, software, and training, can be substantial for healthcare providers, particularly smaller practices with limited budgets.

Additionally, ongoing maintenance costs, such as system updates, technical support, and cybersecurity measures, add to the financial burden. These costs can be a barrier for some healthcare organizations, potentially slowing the rate of EHR adoption. Small and rural practices may need help to justify the investment despite the long-term benefits of improved data management and patient care.

Consequently, while EHR systems offer significant advantages, the high financial outlay required for implementation and maintenance remains a challenge, potentially impacting the healthcare sector's overall growth and adoption rates.

Opportunity: Cloud-Based HER Systems Gaining Traction for Improved Scalability, Flexibility, and Cost Savings

Cloud-based electronic health records present a valuable opportunity for healthcare providers, offering scalability, flexibility, and cost savings. Unlike traditional on-premises systems, cloud-based EHR solutions provide a scalable infrastructure that can easily adjust to healthcare organizations' growing needs.

As patient volumes and data requirements increase, these systems can expand without significant additional investment in hardware.

Another key advantage is flexibility. Cloud-based EHRs enable healthcare providers to access patient information from any location, facilitating remote work and telemedicine services. This accessibility enhances collaboration and ensures continuity of care regardless of physical location.

Moreover, cloud-based solutions are a cost-effective choice, reducing the need for extensive on-site IT support and infrastructure. This leads to significant cost savings, with providers benefiting from lower upfront costs, predictable subscription fees, and reduced maintenance expenses.

Such financial advantages make cloud-based EHRs an attractive option, driving their adoption and transforming healthcare delivery.

Category-wise Analysis

By Product Insights

Web-based EHR occupies 73.3% share of the global market in 2025, because digitization of health information has become nearly universal and demand for cloud-accessible tools has surged. In the United States, 95% of office-based physicians and nearly all hospitals have adopted certified EHR systems that increasingly support patient access through online portals and app-based interfaces, which are typically delivered via web/cloud platforms rather than traditional on-site servers. Patient engagement capabilities such as viewing and downloading records electronically are present in over 96% of hospitals, and the use of APIs and online access tools continues to grow as providers support remote care and interoperability. These trends underscore a shift toward flexible, accessible, and interoperable web-based EHR deployments driven by real-world clinical and policy requirements.

By Form Insights

Acute care EHRs dominate the Electronic Health Records market because adoption among acute care hospitals is nearly universal, reflecting the critical need for digital records in inpatient settings. In the United States, approximately 96% of non-federal acute care hospitals have adopted certified EHR systems, indicating widespread integration into core clinical workflows, and 86% of general acute care hospitals use certified EHR technology as of recent federal health IT surveys. This high penetration stems from regulatory incentives, quality reporting, and operational demands such as computerized clinician documentation, order entry, and real-time information access. In contrast, slower adoption persists in post-acute and specialty settings, underscoring the relative dominance of acute care deployments in overall EHR utilization.

Regional Insights

North America Electronic Health Records Market Trends

North America dominates the Electronic Health Records Market with 50.7% share in 2025, because EHR adoption in the United States and Canada is among the highest globally, supported by longstanding government programs and infrastructure maturity. In the U.S., 95.0% of office?based physicians have adopted EHR systems, and certified EHRs are used by nearly all acute care hospitals, reflecting deep digitization of clinical workflows. Federal initiatives such as the HITECH Act provided billions in incentives to accelerate EHR implementation nationwide, significantly reducing barriers to digital record systems. In Canada, over 85% of hospitals and about 91% of primary care physicians use EHRs, underpinned by national efforts like Canada Health Infoway to standardize and expand digital health solutions. These high adoption rates drive North America’s market leadership.

Europe Electronic Health Records Market Trends

Europe is an important region for the Electronic Health Records market because digital health adoption and government initiatives are driving widespread EHR implementation and interoperability across multiple countries. Nearly all EU Member States now provide some form of online access to health data, and 96% of general practitioners in the EU use electronic health records in routine practice, indicating deep clinical integration. The European Health Data Space (EHDS) regulation is being implemented to standardize EHR formats and enable secure cross?border data exchange, enhancing quality of care and research utility. National rollouts such as Germany’s ePA and digital portals in Scandinavia and the UK further reinforce EHR utilization. These efforts position Europe as a strategic market with strong regulatory support and expanding digital health infrastructure.

Asia Pacific Electronic Health Records Market Trends

Asia?Pacific is the fastest?growing region for the Electronic Health Records market because healthcare digitization is expanding rapidly amid rising internet and smartphone penetration enabling broader remote care access. Internet penetration in the region exceeded 70% by 2024, facilitating digital health adoption including EHRs tied to telehealth and mobile solutions. Governments are actively promoting national digital health infrastructures, such as India’s Ayushman Bharat Digital Mission and cloud?based record systems like Australia’s My Health Record, boosting standardized record?keeping and interoperability. Additionally, the rising burden of chronic diseases and the need for coordinated care across large populations further accelerate demand for EHR systems that support continuity, data sharing, and scalable healthcare delivery.

Market Competitive Landscape

Leading Electronic Health Records market companies focus on software, services, and connected devices, prioritizing interoperability, security, and usability. Investments target AI-driven analytics, telehealth, and patient engagement tools. R&D emphasizes efficiency, data accuracy, and care continuity, while partnerships with healthcare providers and regulators accelerate adoption, innovation, and global integration of digital health technologies.

Key Industry Developments:

- In December 2025, Philips unveiled new advances in its AI-driven imaging systems and expanded its radiation-free, light-based navigation technologies. The company highlighted enhancements that improve imaging accuracy, workflow efficiency, and patient safety, emphasizing the integration of artificial intelligence to support clinical decision-making.

- In December 2025, GE Healthcare launched its next-generation Signa MRI technology to enhance the patient experience. The new system featured advanced imaging capabilities, faster scan times, and improved comfort for patients during procedures.

Companies Covered in Electronic Health Records Market

- Veradigm LLC (Allscripts Healthcare, LLC)

- Cerner Corporation (Oracle)

- GE Healthcare

- eClinicalWorks

- Epic Systems Corporation

- Greenway Health, LLC

- NextGen Healthcare, Inc.

- Health Information Management Systems

- AdvancedMD, Inc.

- CPSI

- Medical Information Technology, Inc. (Meditech)

- CureMD Healthcare

- McKesson Corporation

- Others

Frequently Asked Questions

The global Electronic Health Records Market is projected to be valued at US$ 36.8 Bn in 2026.

Rising telehealth adoption, regulatory support, chronic disease prevalence, digitalization, AI, cloud, and mobile health technologies.

The global Electronic Health Records Market is poised to witness a CAGR of 6.7% between 2026 and 2033.

AI-enabled diagnostics, cloud-based platforms, wearable devices, predictive analytics, personalized care, remote monitoring, emerging markets expansion.

Veradigm LLC (Allscripts Healthcare, LLC)m Cerner Corporation (Oracle), GE Healthcare, eClinicalWorks, Epic Systems Corporation, Greenway Health, LLC.