- Specialty & Fine Chemicals

- Electronic Chemicals Market

Electronic Chemicals Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Electronic Chemicals Market by Product Type (Solid, Gas, and Liquid), by End-user (Semiconductor & IC, PCB (Printed Circuit Boards), and Photovoltaic (PV)), by Application (Silicon Wafers, PCB Laminates, Specialty gases, Wet chemicals and solvents, Photoresists, and Others), and Regional Analysis for 2025 - 2032

Electronic Chemicals Market Size and Trends Analysis

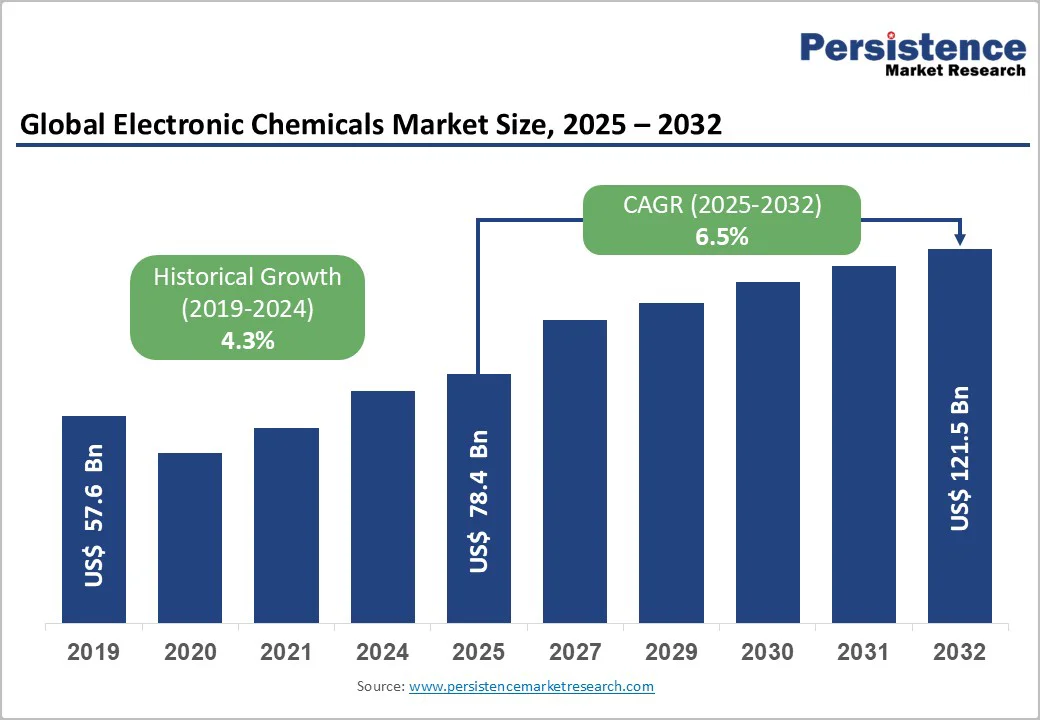

The global electronic chemicals market size is valued at US$ 78.4 Billion in 2025 and is projected to reach US$ 121.5 Billion by 2032, growing at a CAGR of 6.5% between 2025 and 2032. According to WSTS, the semiconductor industry is positioned for broad-based acceleration in 2025, with overall market revenues expected to rise by 11.2% and approach US$ 697 billion.

A significant share of this momentum will stem from the Logic and Memory segments, which together are projected to surpass US$ 400 billion. This rapid scaling of chip production directly amplifies the demand for electronic chemicals, which remain indispensable across every stage of semiconductor fabrication.

Key Industry Highlights:

- Product Type Leadership: Solid product type dominates with above 55% revenue share, while Gas segment represents fastest growing category at 7.4% CAGR, driven by specialty gases critical for deposition and etching in advanced semiconductor fabrication processes.

- End-user Segment Dynamics: Semiconductor & IC end-user commands above 65% revenue share reflecting US$ 200+ billion in fabrication facility investments 2020-2022, while PCB segment fastest growing at 4.1% CAGR through 2033 propelled by IoT device proliferation and automotive electronics expansion.

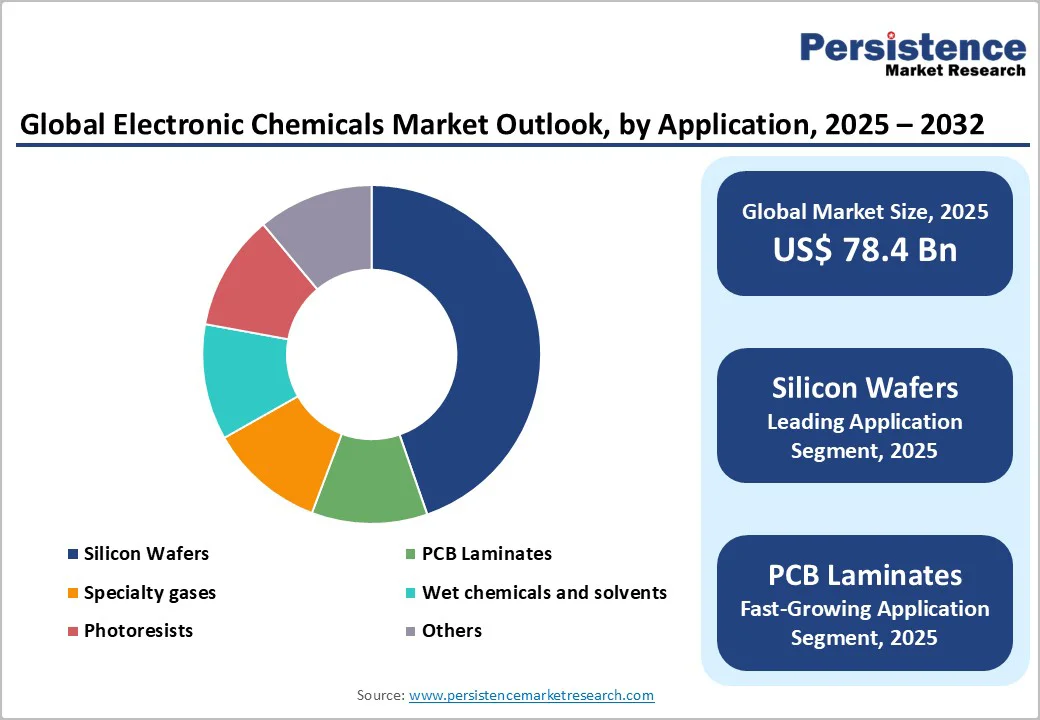

- Application Dominance: Silicon wafers application leads with above 42% revenue share driven by wafer fabrication capacity expansions globally, while PCB laminates represent fastest growing application at 6.8% CAGR through 2030 supported by 5G infrastructure and consumer electronics demand.

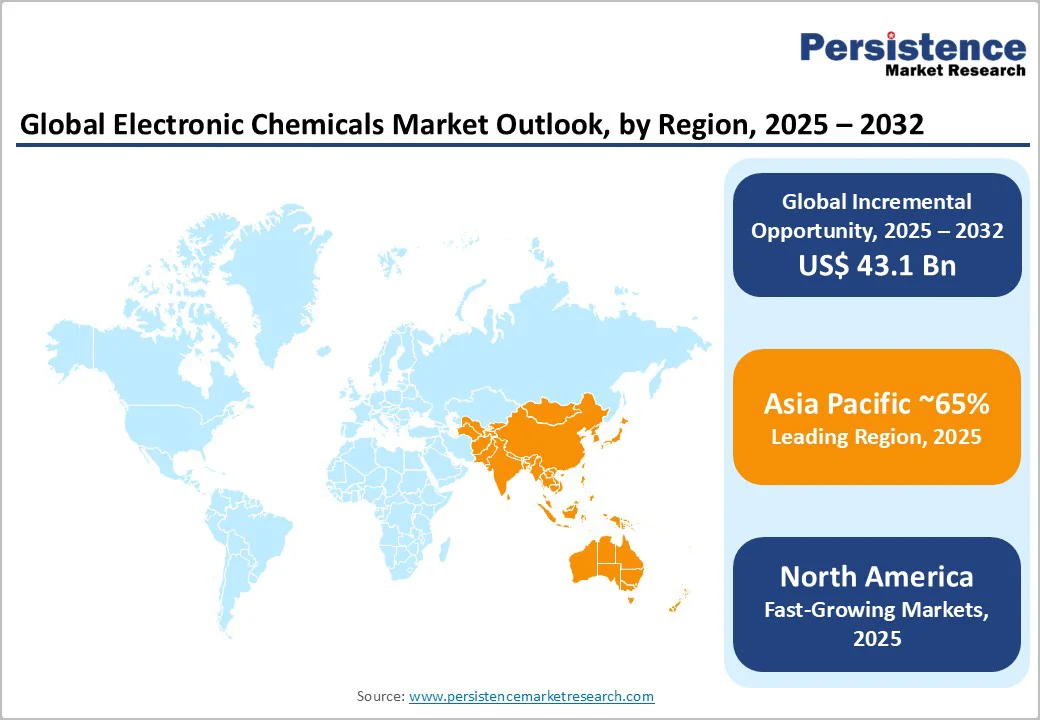

- Regional Distribution: Asia Pacific dominates with above 65% revenue; Europe represents fastest fastest-growing developed market driven by the EU Chips Act implementation.

- Strategic Developments: DuPont doubled photoresist capacity in Japan (October 2024), launched first PFAS-free commercial photoresist DuPont™ UV™ 26GNF (February 2025); Merck KGaA investing €3+ billion in capacity expansions through 2025 including 150,000 m² Taiwan facility producing specialty gases from 2025.

- Sustainability Transformation: Industry-wide shift toward eco-friendly formulations addressing PFAS regulations, with REACH compliance requiring €2 million potential fines, RoHS violations reaching €100,000 penalties, driving green chemistry innovations and bio-based photoresist development creating multi-billion dollar sustainable materials opportunity.

| Key Insights | Details |

|---|---|

|

Electronic Chemicals Market Size (2025E) |

US$ 78.4 Bn |

|

Market Value Forecast (2032F) |

US$ 121.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.3% |

Market Dynamics

Driver - Surging Semiconductor Manufacturing Fueling Intensive Demand for High-Purity Electronic Chemicals

A major growth driver for the electronic chemicals market is the accelerating expansion of global semiconductor manufacturing. Updated WSTS projections indicate that the semiconductor industry will grow 11.2% in 2025, reaching an estimated $697 billion, with the logic and memory segments alone expected to exceed US$400 billion in combined value. Logic is forecast to rise by more than 17% year over year, while memory is set for 13% growth, highlighting the robust scaling of advanced chip production. This sustained rise directly strengthens the need for high-purity chemicals, as producing a single semiconductor chip requires at least 500 specialized chemical formulations, according to the American Chemistry Council.

Technological progress, particularly the adoption of extreme ultraviolet (EUV) lithography, is generating substantial demand for new photoresists and auxiliary materials offering superior resolution, line-edge precision, and sensitivity. Meanwhile, recent global chip shortages have prompted governments to accelerate semiconductor self-sufficiency initiatives, such as the U.S. CHIPS Act and the EU Chips Act, driving fresh investments into domestic semiconductor materials and chemical production ecosystems.

Collectively, these factors surging semiconductor output, rapid technological advancements, massive fabrication investments, and supportive government policies, are significantly boosting demand for high-performance electronic chemicals, making semiconductor manufacturing one of the most powerful and sustained drivers of market growth.

Restraint - Environmental and Regulatory Challenges Associated with PFAS and Hazardous Substances

Per- and polyfluoroalkyl substances (PFAS) are essential in semiconductor manufacturing, playing crucial roles in up to 1,000 nanometric-level processes including photolithography and plasma processing due to their exceptional resistance to degradation and chemical stability. However, these same characteristics present significant challenges in managing and eliminating PFAS from wastewater, creating environmental compliance burdens for manufacturers.

The semiconductor and electronic chemicals industries face increasingly stringent regulatory frameworks, particularly the European Union's RoHS (Restriction of Hazardous Substances) Directive 2015/863 and REACH (Registration, Evaluation, Authorization, and Restriction of Chemicals) regulations. RoHS specifies maximum concentration limits for ten restricted substances including heavy metals and phthalates in electrical and electronic equipment, with penalties for non-compliance reaching up to €100,000 per violation in some EU member states. REACH compliance requires comprehensive product audits against the European Chemicals Agency's Candidate List of Substances of Very High Concern (SVHCs), with fines potentially reaching €2 million or 4% of annual turnover for violations. These regulatory pressures necessitate substantial investments in research and development for sustainable, eco-friendly chemical alternatives.

Opportunities - Development of Sustainable and Eco-Friendly Chemical Formulations

Growing environmental awareness worldwide creates substantial opportunities for developing sustainable, environmentally friendly electronic chemicals, with leading manufacturers increasingly investing in research and development for eco-friendly materials. Companies including BASF, Dow, Merck KGaA, and DuPont are actively developing biodegradable and non-toxic chemical formulations to reduce environmental impact, with a specific focus on sustainable photoresists and etching solutions complying with evolving environmental regulations.

DuPont's recent launch of DuPont™ UV™ 26GNF photoresist represents a significant advancement, the company's first commercial photoresist, substituting traditional fluorine-containing photoacid generators (PAGs) with non-fluorinated alternatives to address environmental and regulatory challenges associated with PFAS substances. This market shift toward green chemistry and bio-based photoresists is gaining traction as manufacturers seek to reduce hazardous waste generation and improve eco-compliance. The emerging trend toward sustainable electronics creates demand for specialty chemicals supporting green semiconductor manufacturing, representing a multi-billion dollar opportunity for companies pioneering environmentally responsible chemical solutions while maintaining performance standards required for advanced fabrication processes.

Category-wise Analysis

Product Type Insights

The electronic chemicals market exhibits a clear product-type hierarchy, with the solid segment maintaining dominance, accounting for over 55% of total revenue, driven by its essential role in semiconductor wafer production and substrate manufacturing. Solid electronic chemicals, including photoresist polymers, CMP pads, substrate materials, and solid-phase dopants, are fundamental to providing the structural integrity and functional performance required in integrated circuits, memory chips, and microprocessors. These materials support critical processes such as deposition, patterning, and surface modification, reinforcing their indispensable position in semiconductor fabrication.

In parallel, the gas segment is emerging as the fastest-growing category, with specialty gases projected to expand at a 7.4% CAGR, fueled by escalating demand in deposition, etching, doping, and wafer-cleaning applications. The rapid advancement of semiconductor nodes, along with the expansion of ALD and CVD thin-film techniques and increasing adoption of advanced packaging technologies, is significantly boosting the need for ultra-high-purity process gases such as NF3, WF6, SiH4, and various dopant gases. Together, these dynamics reflect a market where solid chemicals maintain structural dominance while gaseous chemicals lead the next wave of growth aligned with global semiconductor capacity expansion.

Application Insights

The application landscape of the electronic chemicals market is led by the silicon wafers segment, which holds over 42% revenue share in 2025. Silicon wafers form the essential substrate for semiconductor device fabrication, and the growing need for device miniaturization, performance enhancement, and tighter feature geometry continues to drive demand for ultra-high-purity wafers. Their extensive use across consumer electronics, automotive systems, data centers, and industrial equipment underscores the segment’s long-standing dominance. This leadership is further reinforced by global investments in wafer fabrication capacity as major regions pursue semiconductor self-sufficiency. Technological advancements, including the transition to larger wafer diameters (300mm mainstream, 450mm under development), superior crystalline quality, reduced defect density, and enhanced flatness, are increasing the consumption of specialized chemicals required for wafer cleaning, polishing, etching, and surface preparation.

In parallel, PCB laminates represent the fastest-growing application, projected to expand at a 6.9% CAGR between 2025 and 2030. Their growth is driven by rising demand for electronics such as amplifiers, LEDs, smartphones, computers, and laptops, as well as the rapid expansion of 5G telecommunications infrastructure requiring high-frequency laminates. Additionally, the automotive electronics boom spanning ADAS, EVs, and power-control systems is fueling demand for high-reliability laminate materials capable of operating under harsh conditions. As advanced laminates increasingly incorporate specialized resins, reinforcement fabrics, and high-performance copper foils, they require sophisticated chemical formulations, thereby contributing to sustained and growing demand for specialty electronic chemicals across the PCB laminates segment.

End-user Insights

The electronic chemicals market is heavily shaped by end-user dynamics, with the Semiconductor & IC segment maintaining clear dominance at over 65% revenue share, driven by its position as the largest consumer of high-purity chemicals across all fabrication stages. The segment’s strength is reinforced by the semiconductor industry’s US$ 627 billion global sales in 2024 and the continued shift toward smaller process nodes (5nm, 3nm, and beyond), larger wafer formats (300mm and future 450mm), and advanced packaging technologies such as 3D integration and chiplet architectures all of which demand increasingly sophisticated photoresists, wet chemicals, specialty gases, and CMP slurries.

Asia Pacific, led by China, continues to dominate global PCB production due to its large-scale electronics manufacturing base, while evolving PCB requirements such as miniaturization, flexible printed circuits (FPCs) for IoT devices, and high-reliability automotive-grade PCBs for electric and autonomous vehicles further accelerate the need for specialized electroplating chemicals, copper treatment solutions, photoresists, and precision etching formulations. Together, the dominance of semiconductor applications and the rapid expansion of the PCB industry form a powerful foundation for sustained growth in the electronic chemicals market.

Regional Insights

Asia Pacific Leads the Electronic Chemicals Market with Over 65% Revenue Share, Driven by Dominant Semiconductor Manufacturing Strength

Asia Pacific continues to dominate the global electronic chemicals market with over 65% revenue share. This dominance is reinforced by the region’s status as the global hub for semiconductor production, electronics assembly, and advanced manufacturing, with China, Taiwan, South Korea, Japan, India, and major ASEAN economies hosting the highest concentration of fabs and electronics OEM operations.

China remains the principal growth driver, supported by strong industrial performance value-added output of major firms rose 11.1% year over year, sector revenues increased 9.4% to 6.49 trillion yuan (USD 907 billion), and profits grew 11.9% while semiconductor sales increased 18.3% annually. Japan, despite a slight 0.4% decline in semiconductor sales, maintains demand for high-purity chemicals through its advanced robotics, automotive electronics, and precision manufacturing industries.

Taiwan’s IC sector generated NT$4,342.8 billion (USD 139.2 billion) in 2023, reflecting a 10.2% contraction due to global inventory resets, with declines across design (–11%), manufacturing (–8.8%), packaging (–15.6%), and testing (–12.8%); however, foundry operations, valued at USD 79.9 billion, remain essential to global chip supply chains.

India is the fastest-growing market, achieving electronics output of Rs 11.3 lakh crore in 2024–25 nearly six times the level a decade earlier, driven by strong policies, expanding semiconductor-related initiatives, and rising exports. Meanwhile, ASEAN economies such as Vietnam, Thailand, and Singapore are rapidly scaling their consumer electronics, automotive electronics, PCB manufacturing, and semiconductor back-end industries.

Asia Pacific’s dominance is reinforced by strong semiconductor ecosystems, cost-efficient manufacturing, government support, skilled talent, rising electronics demand, and continued investments in chemical production near major chip clusters.

North America Electronic Chemicals Market Trends

The North America electronic chemicals market remains a strategic global hub supported by accelerating semiconductor manufacturing investments under the CHIPS and Science Act, which allocates USD 52 billion to expand domestic chip production. According to the Semiconductor Industry Association, yearly semiconductor sales in the Americas surged 44.8%, reflecting strong momentum across advanced electronics and next-generation computing technologies. With global semiconductor demand rising, the United States is projected to triple its domestic chip manufacturing capacity by 2032, significantly strengthening supply chain resilience and national competitiveness. Policymakers continue to emphasize initiatives that expand semiconductor innovation, enhance the high-tech workforce, and reinforce U.S. trade leadership to maintain technological superiority.

The region’s growth is driven by the reshoring of semiconductor capacity to reduce dependency on Asian supply chains, soaring demand from AI, high-performance computing, and cloud data centers, rising electric vehicle adoption, increasing requirements for automotive chips, nationwide expansion of 5G and IoT infrastructure, and defense and aerospace applications requiring high-reliability electronic components. U.S. manufacturers focusing on advanced process nodes (5nm and below) are increasing demand for ultra-high-purity wet chemicals, EUV-grade photoresists, advanced CMP slurries, and specialty gases.

Competitive dynamics are led by established suppliers, including DuPont, Dow, Air Products, and CMC Materials, which maintain close R&D partnerships with regional fabs. Investment activity is expanding across photoresist, CMP slurry, and specialty gas manufacturing to support major semiconductor facility developments in Arizona, Texas, Ohio, and New York. In Canada, automation is also rising rapidly, with robot installations increasing 37% to 4,311 units, driven primarily by the automotive industry, which accounted for 58% of demand in 2023.

Competitive Landscape

The global electronic chemicals market exhibits a moderately consolidated structure with several multinational corporations commanding significant market shares alongside numerous regional and specialized suppliers. Leading players including BASF SE, Dow Inc., Merck KGaA, DuPont, Air Products and Chemicals Inc., Linde plc, Cabot Microelectronics (CMC Materials), Tokyo Ohka Kogyo (TOK), JSR Corporation, Fujifilm Electronic Materials, Shin-Etsu Chemical, and Sumitomo Chemical collectively hold approximately 45-50% of the global market share. The competitive landscape is characterized by high barriers to entry due to substantial capital requirements, stringent quality certifications, and established customer relationships with semiconductor manufacturers requiring multi-year qualification processes for chemical suppliers. Market positioning emphasizes technological differentiation through advanced formulations, supply chain reliability, technical support capabilities, and geographic proximity to major semiconductor fabrication clusters in Asia Pacific, North America, and Europe.

Key Industry Developments:

- In 2025, Solvay doubled its production capacity for electronic-grade hydrogen peroxide in China, responding to rapidly rising demand for high-purity chemicals used in semiconductor manufacturing and reinforcing its position as a key supplier for advanced chip production.

- In July 2025, Tata Electronics and Bosch signed a Memorandum of Understanding (MoU) to collaborate in semiconductor manufacturing and technology. Under this partnership, the two companies plan to work together on chip packaging and manufacturing activities at Tata Electronics’ upcoming assembly and test facility in Assam and its planned semiconductor foundry in Gujarat.

- In September 2024, AGC established a new technical service center in Taiwan to strengthen regional support for its chemical materials portfolio, particularly those used in semiconductor and electronic manufacturing.

- In July 2024, Suven Pharmaceuticals Limited received approvals from both NSE and BSE for its proposed merger with Cohance Lifesciences, marking a major strategic step toward expanding its specialty chemicals and pharmaceutical operations.

- In 2024, Mitsubishi Gas Chemical (MGC) expanded its North American operations, announcing a major capacity increase at the Texas site of MGC Pure Chemicals America. The expansion boosts output of ultra-high-purity hydrogen peroxide and ammonium hydroxide used in semiconductor cleaning and etching, strengthening MGC’s leadership in the electronic chemicals market.

- In October 2023, FUJIFILM Corporation completed the USD 700 million acquisition of Entegris’ electronic chemicals business (formerly CMC Materials KMG Corporation), rebranding it as FUJIFILM Electronic Materials Process Chemicals. This strategic development strengthens Fujifilm’s position in the global semiconductor materials sector and aligns with its long-term growth strategy to expand capabilities in high-purity electronic chemicals and advanced manufacturing solutions.

- In October 2023, Noctiluca made significant progress in OLED materials development, introducing a new electron-injection material, NCEIL-4, designed to improve blue pixel longevity through collaborative R&D under its Chemical CRO/CDMO model.

- In April 2023, Resonac Corporation announced a 60% capacity expansion for its “Dicing Die Bonding Film” at the Goi Plant in Kamisu City, Japan, to meet increasing global demand for dual-function semiconductor packaging adhesives. Operations are expected to begin in 2026.

Companies Covered in Electronic Chemicals Market

- Bayer AG

- Albemarle Corporation

- Ashland

- BASF SE

- Air Liquide Electronics

- Merck KGaA

- Honeywell International Inc.

- Cabot Corporation.

- Linde PLC

- Dow

- Hitachi, Ltd.

- Sumitomo Chemical Co., Ltd.

- Monsanto Electronic Materials Co.

- EKC Technology

- FUJIFILM Holdings America Corporation

- HD Microsystems. Ltd.

- High Purity Products

- JSR Micro

- KANTO KAGAKU.

- Moses Lake Industries, Inc.

- Other Market Players

Frequently Asked Questions

The Electronic Chemicals market is estimated to be valued at US$ 78.4 Bn in 2025.

The key demand driver for the Electronic Chemicals market is the rapid expansion of the global semiconductor industry, which increasingly requires high-purity chemicals for wafer fabrication, cleaning, etching, photolithography, and packaging processes.

In 2025, the Asia Pacific region will dominate the market with an exceeding 65% revenue share in the global Electronic Chemicals market.

Among application, Silicon Wafers has the highest preference, capturing beyond 42% of the market revenue share in 2025, surpassing other applications.

Cabot Corporation, Bayer AG, Drex-Chem Technologies, EKC Technology, EMD Performance Materials Corp., Fujifilm Electronic Materials, and Sumika Electronic Materials are a few leading players in the Electronic Chemicals market.