- Medical Devices

- Electric Wheelchairs Market

Electric Wheelchairs Market Size, Share, and Growth Forecast, 2026-2033

Electric Wheelchairs Market by Product Type (Standard Electric Wheelchairs, Complex Rehab Power Wheelchairs, Standing Electric Wheelchairs, Heavy-Duty Electric Wheelchairs, Pediatric Electric Wheelchairs), Drive Configuration (Rear-Wheel Drive, Mid-Wheel Drive, Front-Wheel Drive, Hybrid Drive), End-User (Homecare, Hospitals, Rehabilitation Centers, Long-Term Care Facilities), and Regional Analysis for 2026-2033

Electric Wheelchairs Market Share and Trends Analysis

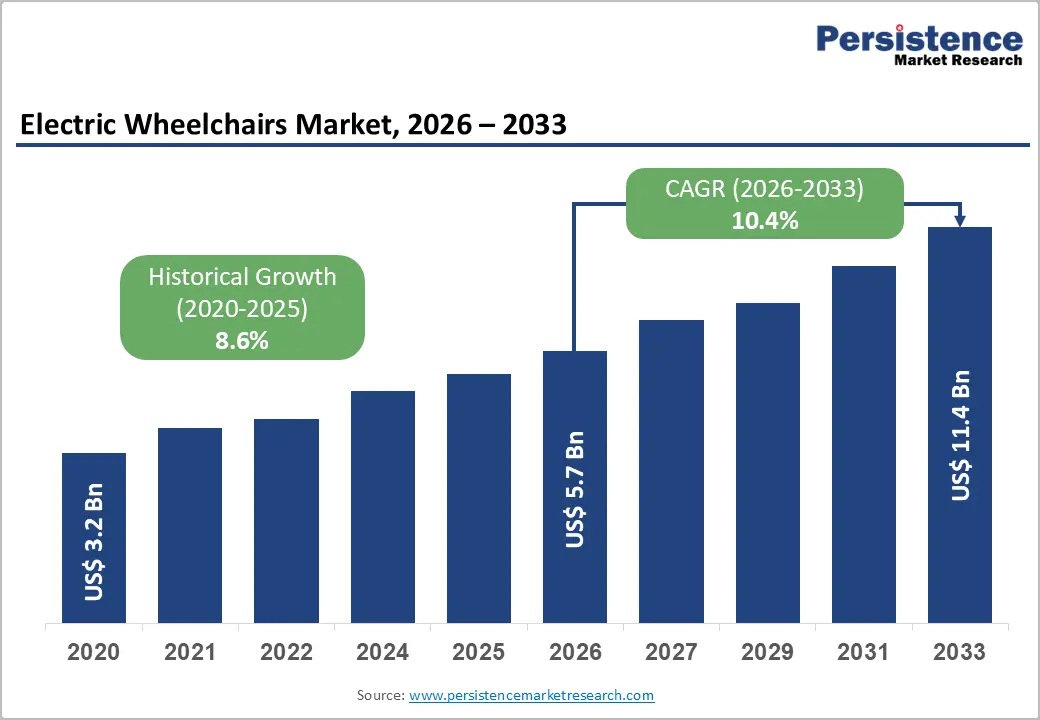

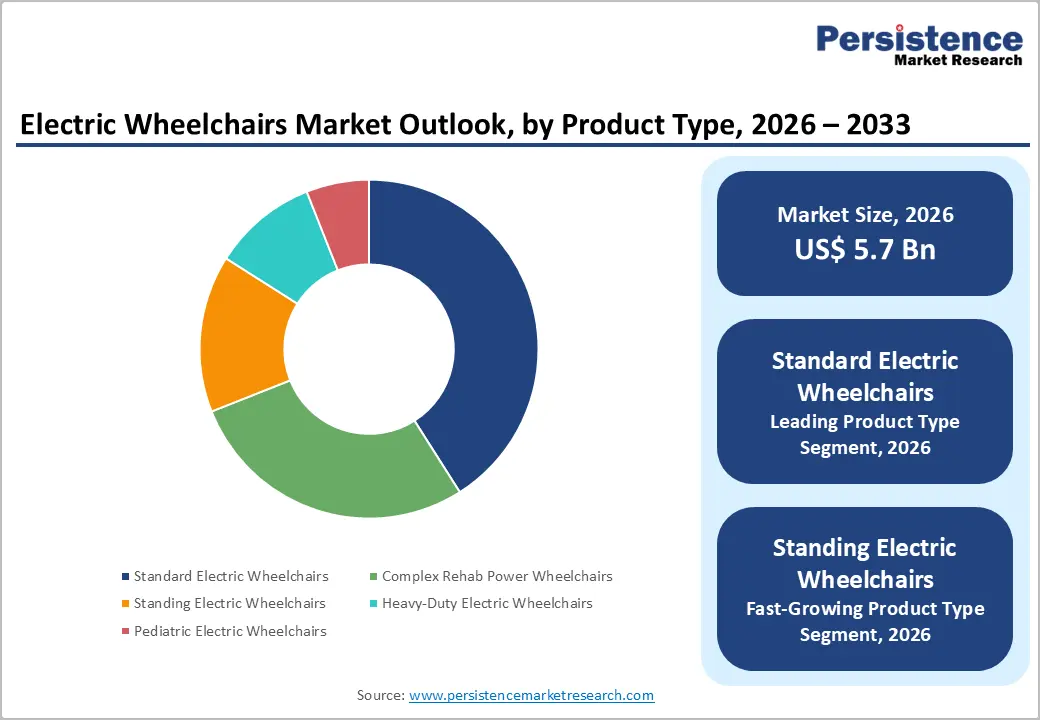

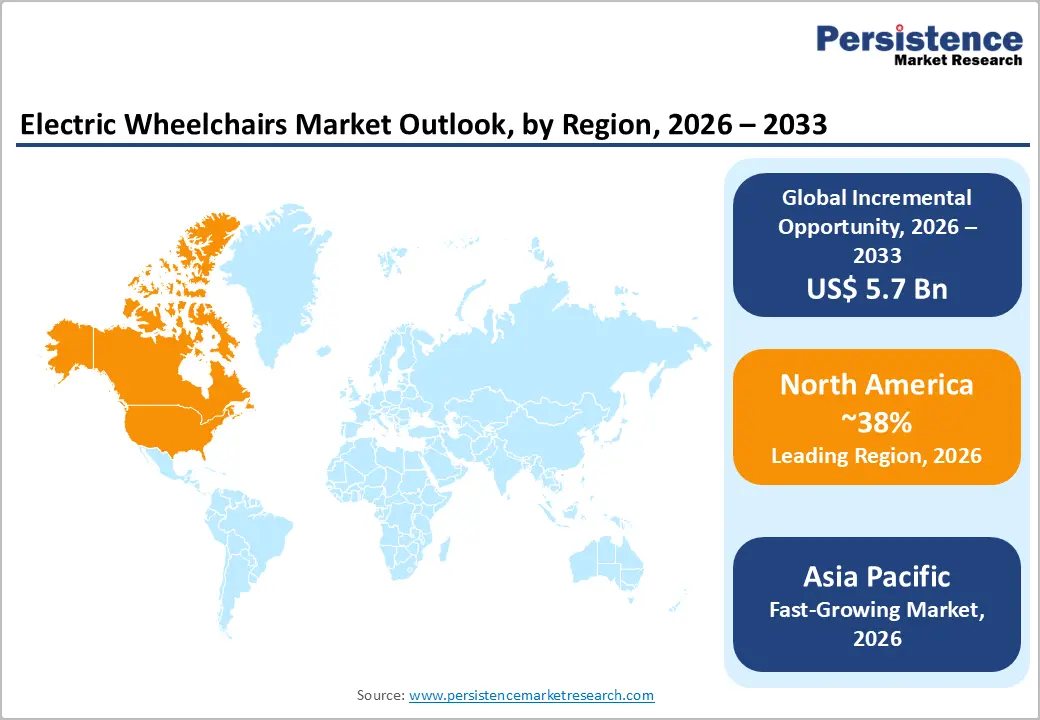

The global electric wheelchairs market size is likely to be valued at US$ 5.7 billion in 2026, and is projected to reach US$ 11.4 billion by 2033, growing at a CAGR of 10.4% during the forecast period 2026–2033.

The growth of this market is primarily driven by the rapidly aging global population, the rising prevalence of mobility impairments, and increasing adoption of assistive mobility technology. As life expectancy rises, healthcare systems are witnessing a growing number of individuals affected by conditions such as arthritis, spinal cord injuries, stroke, and neuromuscular disorders that require long-term mobility support. Governments and healthcare providers are also increasing investments in rehabilitation infrastructure and disability assistance programs, improving patient access to powered mobility devices.

The manufacturers are introducing advanced smart mobility devices featuring AI-assisted navigation, lightweight lithium-ion battery systems, improved seating ergonomics, and standing mobility capabilities. These innovations enhance safety and independence, which continues to accelerate adoption across homecare environments, hospitals, and rehabilitation centers worldwide.

Key Industry Highlights

- Dominant Product Type: Standard electric wheelchairs are set to command around 41% of the revenue share in 2026, while standing wheelchairs are likely to grow the fastest at about 12.1% CAGR through 2033, driven by proven rehabilitation benefits.

- Leading Drive Configuration: Mid-wheel drive is expected to lead with an estimated 38% share in 2026, while hybrid drive systems are projected to be the fastest-growing during 2026–2033, reflecting rising demand for versatile indoor-outdoor mobility performance.

- Dominant End-User: Homecare settings are anticipated to hold approximately 47% revenue share in 2026, while rehabilitation centers are likely to expand the fastest through 2033, supported by growing investments in post-acute mobility rehabilitation services.

- Regional Leadership: North America is poised to dominate with an estimated 38% share in 2026, while Asia Pacific is projected to register the fastest growth at about 12.8% CAGR through 2033, led by demographic aging and healthcare infrastructure expansion.

- Competitive Environment: Competitive dynamics increasingly revolve around innovation in smart mobility technologies, including AI-enabled navigation, connected wheelchair platforms, and high-efficiency battery systems.

- December 2025: India’s Artificial Limbs Manufacturing Corporation of India (ALIMCO) introduced a clip-on motorized device that converts a manual wheelchair into a battery-powered mobility aid.

| Key Insights | Details |

|---|---|

| Electric Wheelchairs Market Size (2026E) | US$ 5.7 Bn |

| Market Value Forecast (2033F) | US$ 11.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expanding Aging Populations and Increasing Mobility Disabilities Worldwide

The rapid expansion of the elderly population is a major factor driving the electric wheelchair market growth. According to the World Health Organization (WHO), the global population aged 60 years and older will reach 2.1 billion by 2050, nearly doubling from 1 billion in 2020. Aging populations experience higher incidences of arthritis, spinal cord injuries, Parkinson’s disease, and stroke-related mobility limitations, significantly increasing demand for powered mobility devices. The U.S. Centers for Disease Control and Prevention (CDC) further reports that nearly 12% of adults in the United States experience mobility limitations, creating sustained demand for advanced electric wheelchairs.

As healthcare systems prioritize long-term mobility support and independent living, demand for assistive mobility devices continues to rise globally. Older adults increasingly require mobility solutions that allow them to perform daily activities independently and safely. Electric wheelchairs provide improved maneuverability, comfort, and functional independence compared to manual mobility aids. The growing focus on aging-in-place strategies within healthcare systems further reinforces the adoption of electric mobility devices across homecare settings. This demographic trend will remain a critical demand driver for powered wheelchairs over the coming decade.

Technological Advancements and Expanding Healthcare Reimbursement Support

Continuous technological innovation has significantly improved the performance, usability, and accessibility of electric wheelchairs. Advances in lithium-ion battery technology, smart navigation systems, and joystick-controlled mobility platforms are enhancing operational efficiency and user independence. According to the International Energy Agency (IEA), lithium-ion battery costs have declined by over 85% since 2010, enabling manufacturers to produce lighter and longer-lasting powered wheelchairs. In addition, integration of IoT-enabled monitoring systems, AI-based obstacle detection, and posture management systems has improved safety and rehabilitation outcomes.

Government healthcare systems and disability support programs are also expanding access to electric mobility devices, particularly in developed economies. For example, the U.S. Centers for Medicare & Medicaid Services (CMS) provides reimbursement coverage for medically necessary power wheelchairs, improving affordability for elderly and disabled populations. Similarly, European countries offer disability mobility allowances under national healthcare programs. The European Commission (EC) reports that approximately 87 million people in the European Union (EU) live with disabilities, prompting governments to expand assistive technology funding. These reimbursement frameworks significantly improve accessibility to electric wheelchairs and strengthen long-term demand across healthcare systems.

High Cost of Advanced Electric Wheelchairs

Despite strong demand growth, the high cost of electric wheelchairs remains a major adoption barrier, particularly in developing economies. Advanced complex rehabilitation power wheelchairs can cost between US$ 5,000 and US$ 25,000, depending on customization, control systems, and seating configurations. According to the U.S. National Institute on Disability, Independent Living, and Rehabilitation Research (NIDILRR), high device costs remain one of the most significant barriers to mobility technology access. Limited insurance coverage and reimbursement in emerging markets restrict adoption among low-income populations, slowing overall powered wheelchair market penetration in several regions.

For many individuals requiring mobility assistance, upfront purchase costs remain difficult to manage without financial support. In several emerging healthcare systems, mobility devices are often categorized as non-essential medical equipment, limiting government funding or subsidy programs. As a result, patients frequently rely on personal financing or charitable support to obtain these devices. High maintenance expenses, replacement parts, and battery upgrades can further increase the total cost of ownership. These financial barriers continue to limit accessibility to advanced electric wheelchairs, particularly among elderly and disabled populations in lower-income regions.

Regulatory Compliance and Product Certification Challenges

Manufacturers operating in the electric wheelchair market must comply with strict medical device regulations, including safety, battery standards, and accessibility guidelines. Regulatory approvals such as Food and Drug Administration (FDA) medical device clearance in the United States and CE marking in Europe require extensive testing and certification procedures. These compliance requirements increase development costs and extend product launch timelines. Additionally, battery safety regulations and transportation restrictions for lithium batteries create logistical challenges, increasing supply chain complexity for manufacturers operating in the global mobility devices market.

Recent regulatory actions highlight the growing scrutiny surrounding mobility device safety and certification. In September 2025, the U.S. FDA issued a Class I recall for certain electric wheelchair joystick systems after a firmware issue caused unexpected movement, underscoring the importance of strict device testing and quality control. At the same time, aviation regulators and airlines have introduced additional safety measures for lithium-powered mobility devices due to fire risks. For example, Southwest Airlines implemented new policies in 2025 requiring removable lithium batteries to be taken out of powered wheelchairs before boarding and introduced a 300-watt-hour battery limit starting in 2026, following safety guidance from the Federal Aviation Administration (FAA). Such regulatory developments demonstrate how evolving safety requirements can increase compliance complexity and operational costs for electric wheelchair manufacturers.

Growing Uptake of Electric Wheelchairs in Developing Markets

Emerging economies represent a significant growth opportunity for the electric wheelchair market as healthcare accessibility improves across developing regions. According to the World Bank, more than 80% of people with disabilities live in developing countries, many of whom lack access to modern assistive mobility devices. Rapid healthcare infrastructure expansion in Asia Pacific, Latin America, and the Middle East is improving access to rehabilitation services and mobility technologies. Governments in countries such as India and China are introducing disability welfare schemes and healthcare reforms designed to increase accessibility to rehabilitation equipment and powered mobility solutions.

Policy initiatives and accessibility programs are further strengthening demand for electric mobility devices. The disability inclusion programs organized by India’s Department of Empowerment of Persons with Disabilities highlighted the importance of mobility aids and assistive technologies in improving independence and social inclusion for people with disabilities. At the same time, several countries are expanding healthcare reimbursement policies to improve wheelchair accessibility. For instance, France announced that standard wheelchairs would be fully reimbursed through public health insurance starting December 2025, reflecting growing government commitment to assistive mobility support. Global sporting events such as wheelchair divisions in the Boston Marathon and London Marathon also contribute to broader public awareness of mobility technologies and disability inclusion, indirectly supporting innovation in wheelchair design. These developments are expected to create substantial growth opportunities for manufacturers expanding into emerging healthcare markets.

Technological Innovation and the Shift toward Smart Homecare Mobility Solutions

The next phase of innovation in the electric wheelchair industry is being driven by the integration of AI, IoT connectivity, and autonomous navigation technologies. Smart wheelchairs equipped with sensor-based navigation, voice control, and smartphone connectivity are gaining traction in advanced healthcare systems. These technologies enable caregivers and healthcare professionals to monitor patient mobility remotely while improving safety and independence. Research initiatives from universities and technology developers are accelerating the development of next-generation smart mobility devices designed to enhance autonomy for individuals with severe mobility impairments.

In 2025, researchers from the Robotics and Intelligent Vehicles Research Laboratory at Northeastern University developed an AI powered autonomous wheelchair with an integrated robotic arm, designed to help users navigate complex environments and improve independence. Similarly, Indian researchers introduced an AI-enabled wheelchair with voice commands, cameras, and sensor-based obstacle detection, allowing users to navigate environments and store frequently visited locations through intelligent navigation systems. Alongside technological progress, healthcare systems are increasingly shifting toward home-based care models, encouraging manufacturers to develop compact, lightweight, and foldable powered wheelchairs suited for independent living environments. This convergence of smart technology and homecare demand is creating strong innovation-driven growth opportunities in the global electric wheelchair market.

Category-wise Analysis

Product Type Insights

Standard electric wheelchairs are estimated to hold the largest revenue share at around 41% in 2026, reflecting widespread adoption across hospitals, homecare, and rehabilitation centers due to affordability and ease of use. Their lower upfront and maintenance costs are projected to continue supporting accessibility among a broad user base, while reimbursement frameworks in North America and Europe are likely to sustain adoption. In 2025, U.S. public transit initiatives expanded funding for mobility-enhancement equipment, including powerchair accessibility improvements, which is expected to indirectly support broader visibility and use of standard electric wheelchairs in community and institutional settings. These factors indicate that standard electric wheelchairs are poised to maintain steady market dominance throughout the forecast period.

Standing electric wheelchairs are projected to be the fastest-growing product type with an estimated CAGR of 12.1% from 2026 to 2033, as users seek both mobility and therapeutic benefits. The ability to shift from seated to standing positions is anticipated to improve circulation, posture, and social engagement, driving adoption in rehabilitation programs and homecare. In 2026, pilot programs at U.S. rehabilitation hospitals integrating sensor-based stability and posture feedback systems demonstrated improved patient independence, signaling likely acceleration in adoption of standing models. These developments suggest continued strong growth potential as clinical and homecare environments increasingly favor multifunctional mobility solutions.

Drive Configuration Insights

Mid-wheel drive is anticipated to lead with approximately 38% of the electric wheelchair market revenue share in 2026, due to superior maneuverability, balance, and indoor navigation capabilities. Their tight turning radius and stable design are expected to sustain preference in healthcare facilities and residential care environments. In 2025, Canadian medical centers tested mid-wheel drive chairs equipped with advanced obstacle-avoidance sensors, which is projected to reinforce their safety and adoption in constrained indoor spaces. The combination of reliability, maneuverability, and enhanced safety features positions mid-wheel drive models to retain their leading status over the forecast period.

Hybrid drive electric wheelchairs are projected to record the highest 2026-2033 CAGR of roughly 11.6% from 2026 to 2033, due to their versatility across indoor and outdoor terrains. These models are expected to appeal to users transitioning between home, urban, and community environments. For instance, Australian pilot programs integrating adaptive suspension and terrain-sensor feedback in hybrid wheelchairs demonstrated improved usability on uneven surfaces, which is likely to enhance market acceptance. Such innovations indicate that hybrid drive models will continue gaining traction among users seeking flexible, multi-terrain mobility solutions.

Regional Insights

North America Electric Wheelchairs Market Trends

North America is projected to command about 38% of the electric wheelchair market share in 2026, driven primarily by the United States. The region benefits from well established healthcare infrastructure, expansive disability support programs, and high awareness of mobility needs. According to U.S. Census Bureau data, approximately 13.7% of U.S. adults live with a disability, supporting sustained demand for powered mobility devices. Programs such as Medicare and Medicaid reimbursement enhance affordability and access to advanced wheelchairs.

Leading manufacturers and technology developers continue to expand service offerings in conjunction with healthcare providers. A policy development in 2025, when the U.S. Department of Veterans Affairs expanded its mobility equipment benefit to include broader coverage for advanced power-wheelchairs, is expected to further encourage device adoption among eligible veterans.

In addition, North America has seen pilot implementations of smart health mobility systems in several major hospital networks, integrating electric wheelchairs with real time patient tracking and predictive analytics to improve rehabilitation outcomes and safety. These deployments demonstrate growing institutional commitment to assistive technology integration. Venture capital funding and partnerships between medical device firms and digital health companies are increasing, accelerating the regional innovation ecosystem. Thus, with strong clinical adoption and supportive reimbursement frameworks, these developments position North America for continued leadership through 2033.

Europe Electric Wheelchairs Market Trends

Europe represents a mature and steadily expanding market for electric wheelchairs, supported by robust public healthcare systems and disability support frameworks across major countries such as Germany, the United Kingdom, France, and Spain. The EU’s Medical Device Regulation (MDR) ensures high safety and quality standards while enabling innovation in assistive technologies. Public healthcare reimbursement programs improve access to mobility devices, significantly reducing cost barriers for patients.

Europe’s aging population, with about 21% of residents aged 65 or older, continues to drive demand for advanced mobility solutions. European manufacturers are responding with designs focused on lightweight materials, energy efficient batteries, and ergonomic comfort.

In 2025, several national health ministries introduced government subsidies for electric mobility devices to improve community care integration, with pilot programs in Spain and Italy providing direct funding to elderly and disabled individuals for power-wheelchair purchases. In 2026, a joint initiative between French rehabilitation hospitals and mobility tech firms deployed energy efficient wheelchairs with integrated health sensors for long term care patients, enhancing safety monitoring and user outcomes.

Such developments underscore Europe’s commitment to blending healthcare accessibility with technology innovation. Given these supportive policy and integration trends, Europe is expected to grow at an estimated 8.2% CAGR through 2033.

Asia Pacific Electric Wheelchairs Market Trends

Asia Pacific is forecast to be the fastest growing regional market for electric wheelchairs, slated to showcase an estimated CAGR of 11.3% between 2026 and 2033, propelled by rapid demographic shifts, increasing healthcare investment, and expanding rehabilitation infrastructure. Major markets include China, Japan, and India, where rising elderly populations and government support programs are broadening demand for powered wheelchairs. In Japan, more than 29% of the population is aged 65 or older, creating high demand for assistive devices.

China and India are also expanding healthcare infrastructure and introducing disability support schemes to improve device accessibility. Local manufacturing advantages and cost competitiveness are helping lower priced electric wheelchair adoption in emerging segments.

China’s Ministry of Civil Affairs launched regional smart rehabilitation hubs that standardize electric wheelchair accessibility in public care facilities, enabling patients to receive mobility support closer to home. India’s government also initiated inclusive mobility drives in multiple states in 2026, increasing subsidies for powered mobility devices and integrating them into community healthcare programs.

Meanwhile, in 2026, Japan’s Ministry of Health, Labour and Welfare supported pilot deployments of next generation assistive wheelchairs with integrated health monitoring apps to support aging in place strategies. These developments illustrate how policy, infrastructure investment, and technology integration are expanding electric wheelchair penetration across Asia Pacific, reinforcing its position as the fastestgrowing regional market.

Competitive Landscape

The global electric wheelchair market structure is moderately consolidated, with leading players such as Permobil, Sunrise Medical, Invacare, Pride Mobility, and Ottobock accounting for a large share of revenue. These companies leverage strong healthcare and homecare distribution networks and invest heavily in R&D, focusing on ergonomic designs, advanced battery systems, and digital integration. Their established brand presence and relationships with medical providers maintain their technological leadership. Strategic innovation in smart mobility devices continues to differentiate them in a competitive market.

Regional and niche competitors such as Drive DeVilbiss Healthcare, Karman Healthcare, and MEYRA focus on specialized segments, including pediatric, lightweight, and rehabilitation-specific wheelchairs. Regulatory compliance, certification requirements, and customization complexity limit new entrants. However, digitalization and AI-enabled solutions offer collaboration opportunities with traditional manufacturers. Market consolidation is expected to rise as global leaders pursue strategic acquisitions and partnerships, expanding reach and integrating advanced features across product portfolios.

Key Industry Developments

- In February 2026, WHILL unveiled the Model C Lite, a foldable, lightweight carbon electric wheelchair designed to combine portability with high performance and comfort. The mobility device integrates Japanese engineering and advanced materials to deliver easy folding, strong maneuverability, and reliable everyday mobility support.

- In December 2025, Sunrise Medical strengthened its Premium Standard Rehabilitation portfolio by acquiring Ergoflix, a German leader in foldable power wheelchairs for active lifestyles. The deal leverages Sunrise Medical’s global distribution network to scale Ergoflix’s dealer-focused model internationally, addressing rising demand for home-based care and user independence.

- In October 2025, at the 2025 Japan Mobility Show, Toyota unveiled the “Walk Me” wheelchair, featuring four foldable robotic legs capable of climbing stairs and navigating uneven terrain. This experimental, autonomous mobility device represents a breakthrough in assistive technology, expanding possibilities for user independence beyond traditional wheel-based designs.

Companies Covered in Electric Wheelchairs Market

- Permobil AB

- Sunrise Medical LLC

- Invacare Corporation

- Pride Mobility Products Corp.

- Ottobock SE & Co. KGaA

- Drive DeVilbiss Healthcare

- Karman Healthcare Inc.

- MEYRA GmbH

- GF Health Products Inc.

- Hoveround Corporation

- Merits Health Products

- Levo AG

- Falcon Mobility

- Karma Medical Products Co. Ltd.

Frequently Asked Questions

The global electric wheelchair market is projected to reach US$ 5.7 billion in 2026.

Rising aging populations, increased mobility disabilities, and adoption of advanced assistive mobility technologies are driving market growth.

The market is poised to witness a CAGR of 10.4% from 2026 to 2033.

Emerging healthcare markets, smart mobility integration, and expansion of homecare solutions are unlocking lucrative growth opportunities.

Permobil, Sunrise Medical, Invacare, Pride Mobility, and Ottobock are a few among the leading global players in the market.