- Hardware & Software IT Services

- Data Center Market

Data Center Market Size, Share, and Growth Forecast, 2026 - 2033

Data Center Market by Component (Hardware, DCIM Software, Services), Data Center Type (Hyperscale, Colocation, Enterprise, Cloud, Edge), by Data Center Tier (Tier-1, Tier-2, Tier-3, Tier-4), End User (Cloud Service Provider, IT & Telecom, Healthcare, BFSI, Government, Manufacturing, Others), and Regional Analysis, 2026 - 2033

Data Center Market Size and Trends

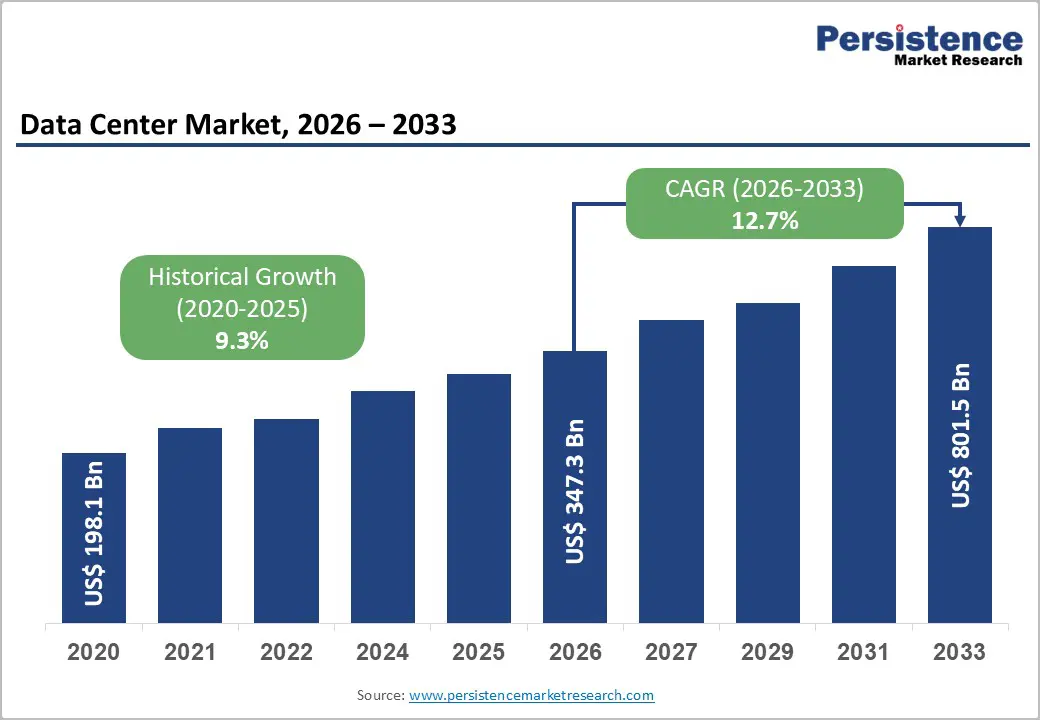

The global data center market size is projected to rise from US$347.3 billion in 2026 to US$801.5 billion by 2033, growing at a CAGR of 12.7% during the forecast period from 2026 to 2033, driven by the explosive surge in artificial intelligence workloads, cloud computing adoption, and digital infrastructure modernization across enterprises globally.

Rising demand for high-performance computing infrastructure to support generative AI, machine learning, and large language model training has become the primary market catalyst, alongside increasing enterprise cloud migration and hybrid IT environment deployments. The convergence of 5G network expansion, Internet of Things proliferation, and edge computing adoption is creating sustained demand for distributed data center infrastructure across multiple geographic regions and use cases.

Key Industry Highlights:

- Leading Component: Hardware dominates with over 56% market share in 2026, valued at over US$ 194.5 Bn, driven by AI, cloud, and big data workload expansion requiring continuous server, GPU, storage, and network upgrades. DCIM is expanding at 16.7% CAGR, as operators require real-time monitoring of power, cooling, asset performance, and sustainability metrics across hybrid environments.

- Leading Data Center Type: Colocation holds more than 28% market share in 2026, valued at over US$ 97.3 Bn, driven by enterprises seeking capital-light expansion, multi-cloud connectivity, and energy-efficient infrastructure. Edge is expected to grow at 17.3% CAGR, driven by low-latency requirements, IoT proliferation, and data sovereignty needs.

- Leading Data Center Tier: Tier-3 holds over 40% share in 2026, valued at over US$ 138.9 Bn, due to its optimal balance of uptime ~99.98% and cost. Tier-4 is expected to grow at 17.8% CAGR, as enterprises demand zero-downtime infrastructure for mission-critical AI, finance, and healthcare workloads.

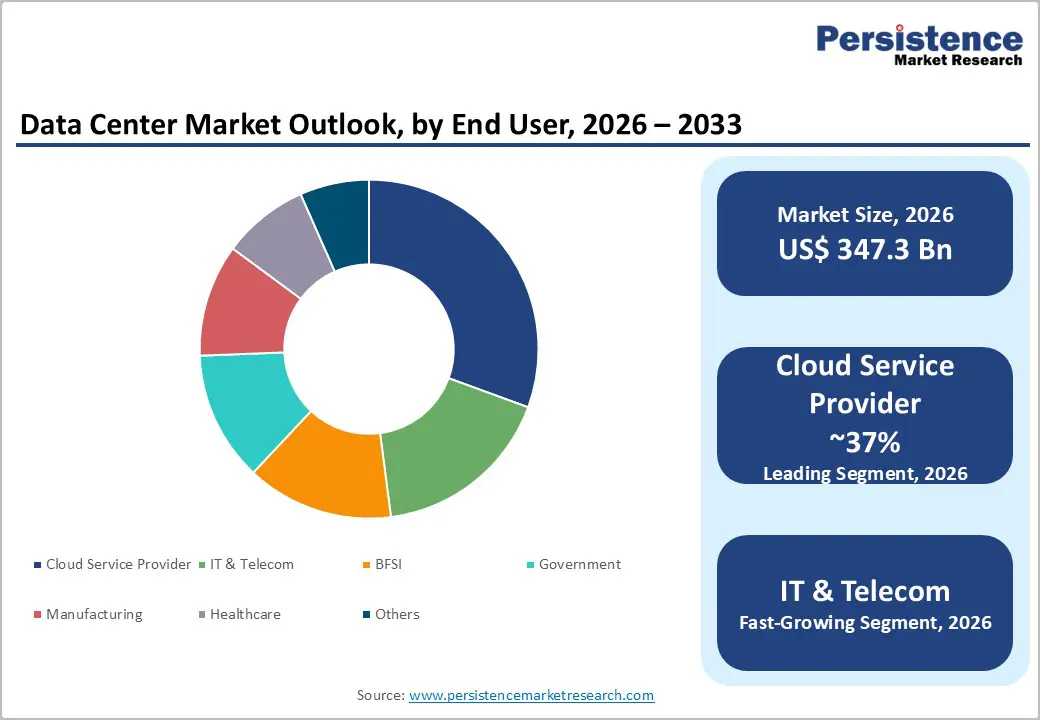

- Leading End-user: Cloud service providers dominate with more than 37% share in 2026, valued at over US$ 128.5 Bn, due to scalability, global reach, and AI-driven demand. IT & Telecom are growing at 16.9% CAGR, driven by 5G expansion, streaming, and edge compute requirements.

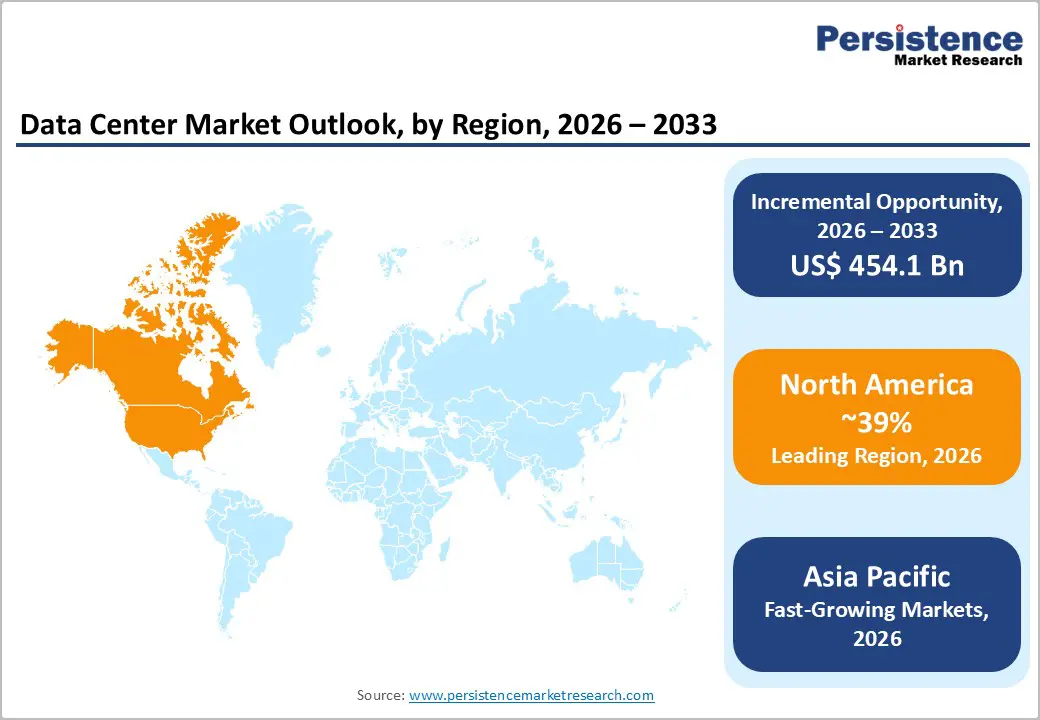

- Leading Region: North America holds more than 39% share in 2026, valued at US$ 135.5 Bn, driven by mature infrastructure, hyperscale deployments, and renewable energy commitments. Asia Pacific is expected to grow at 18.5% CAGR, supported by rapid digitalization, 5G rollout, and strong investment inflows.

| Key Insights | Details |

|---|---|

|

Data Center Market Size (2026E) |

US$347.3 Bn |

|

Market Value Forecast (2033F) |

US$801.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

12.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

9.3% |

Market Dynamics

Driver - Artificial Intelligence and High-Performance Computing Workload Demand

The exponential growth in artificial intelligence applications is fundamentally reshaping global data center infrastructure requirements. According to a Study, AI-driven power demand from data centers is projected to increase by over 160% by 2030, with an approximately 50% surge expected by 2027. Organizations are deploying GPU-intensive workloads, neural network training, and generative AI applications that require significantly higher power densities and specialized cooling capabilities. Cloud service providers, including Amazon Web Services, Microsoft Azure, and Google Cloud, are investing billions to build AI-ready facilities with rack densities exceeding 100 kW to 250 kW per rack. This technological shift creates substantial demand for next-generation data center infrastructure incorporating advanced liquid cooling systems, immersion cooling technologies, and optimized power distribution architectures.

Cloud Computing Expansion and Multi-Cloud Strategy Adoption

Global enterprises are accelerating their cloud migration strategies to achieve digital transformation objectives and operational agility. The worldwide cloud infrastructure services market reached US$ 99 billion in Q2 2025, representing a 25% year-over-year growth rate. AWS, Microsoft Azure, and Google Cloud collectively control 63% of the global cloud market share, with cloud service providers accounting for over 60% of enterprise workload distribution. The shift toward hybrid and multi-cloud deployments necessitates distributed data center capacity across geographies, driving investment in colocation and hyperscale facilities. Organizations increasingly adopt edge data centers to support low-latency applications, IoT device connectivity, and real-time analytics requirements across diverse geographic regions and industry verticals.

Restraint - Energy Supply Constraints and Power Grid Infrastructure Limitations

Data centers face unprecedented energy availability challenges as power demand dramatically outpaces grid infrastructure expansion capabilities. In North America alone, data center construction has increased by 70% over the past six months, with states including Texas, California, Arizona, Oklahoma, Kansas, and Illinois emerging as critical markets. Traditional utilities experience significant bottlenecks, with grid connection wait times extending by 24 to 72 months in key markets like Northern Virginia, Santa Clara, and Phoenix. The International Energy Agency reports that data centers currently account for approximately 1% of global electricity consumption, creating acute pressure on power distribution infrastructure. Permitting delays, substation capacity limitations, and delayed grid interconnections directly constrain facility deployment timelines and operational expansion strategies across competitive markets.

High Capital Expenditure Requirements and Infrastructure Investment Barriers

Establishing state-of-the-art data center facilities demands substantial capital investment exceeding US$ 150-300 million per megawatt of capacity, creating formidable barriers for smaller operators and emerging market participants. The Uptime Institute's Global Data Center Survey 2025 indicates that infrastructure procurement bottlenecks for critical equipment, including transformers, switchgears, and gas turbines, continue to disrupt construction schedules. Organizations must simultaneously address cybersecurity infrastructure upgrades, compliance certifications including ISO 27001 and LEED standards, advanced cooling system implementations, and renewable energy integration requirements that escalate total project costs. These barriers limit market participation to capital-rich providers and restrict competitive landscape diversification across emerging geographic markets and regional economies.

Opportunity - Edge Data Center Deployment for Low-Latency Applications and Real-Time Processing

Industries including autonomous vehicles, smart manufacturing, telemedicine, augmented reality applications, and real-time financial trading require ultra-low latency and localized data processing capabilities that edge infrastructure uniquely provides. The proliferation of IoT devices exceeding billions of connected endpoints generates data at the edge that benefits from proximity-based processing rather than centralized transmission. Governments worldwide are incentivizing regional edge data center development through infrastructure grants and tax incentives, particularly across Asia Pacific, where digital transformation initiatives accelerate rapid urbanization. This expansion creates substantial revenue opportunities for operators capable of deploying modular, containerized facilities rapidly in tier-2 and tier-3 cities while maintaining interconnection with hyperscale backbones.

Green Data Center and Sustainability-Driven Infrastructure Investments

Environmental sustainability initiatives are increasingly driving capital allocation toward green data center solutions incorporating renewable energy sources, advanced cooling technologies, and carbon-neutral operations. Major cloud service providers including Google, operating on 100% renewable energy, and Microsoft, pursuing carbon-negative commitments by 2030, establish market precedents motivating enterprise clients to prioritize sustainable colocation providers. The data center liquid cooling market is projected to expand from US$ 5.6 billion in 2026 to US$ 27.3 billion by 2033, representing a remarkable 25.1% CAGR as immersion cooling and direct-to-chip technologies enable 45% reduction in carbon emissions compared to traditional air cooling. Regulatory frameworks, including European Union energy efficiency directives and corporate ESG commitments, mandate demonstrable sustainability progress, creating competitive differentiation for operators deploying green infrastructure. This expansion opportunity attracts private equity investment and infrastructure funds seeking long-term revenue stability, combined with environmental impact alignment and regulatory compliance advantages.

Category-wise Analysis

Component Insights

Hardware dominates the global market, capturing more than 56% share in 2026 with a value exceeding US$ 194.5 Bn, due to it addresses the core physical needs of data processing and storage. The rapid growth of AI, cloud computing, and big data workloads requires massive investments in servers, GPUs, storage systems, and high-performance networking equipment. Rising demand for low latency, high reliability, and energy efficiency is also pushing upgrades of power, cooling, and rack infrastructure. Hardware must be continuously expanded and refreshed to handle higher compute density and performance requirements.

DCIM Software demonstrates a significant rate at 16.7% CAGR due to operators increasingly need real-time visibility into power, cooling, and asset performance to prevent downtime and reduce energy costs. As data centers scale rapidly, manual tracking becomes impossible, so DCIM helps automate inventory, capacity planning, and change management. With rising energy prices and stricter sustainability goals, DCIM enables better monitoring of PUE and carbon emissions. Hybrid and multi-cloud environments drive demand for centralized control and optimization across both on-prem and colocation facilities.

Data Center Type Insights

Colocation holds over 28% market share in 2026, with a value exceeding US$ 97.3 Bn, as enterprises need fast, scalable, and capital-light infrastructure without building their own facilities. It meets the growing need for hybrid IT setups, allowing companies to combine on-premise control with cloud connectivity. Rising demand for low-latency performance, secure interconnection, and access to multiple cloud providers in one location makes colocation highly attractive. Businesses facing power, cooling, and sustainability constraints rely on colocation providers that can deliver energy-efficient and compliant infrastructure at scale.

Edge is expected to grow at the highest rate, with a CAGR of 17.3%, due to businesses' need for real-time processing with ultra-low latency for use cases like AI inference, IoT, autonomous systems, gaming, and AR/VR. The explosion of connected devices is pushing data generation closer to users, making the centralized cloud alone inefficient and costly. Enterprises also need localized data processing to meet data sovereignty, security, and compliance requirements. Edge infrastructure reduces bandwidth strain and cloud dependency, enabling faster decisions and more resilient digital operations.

Data Center Tier Insights

Tier-3 commands the largest market share at over 40% in 2026, with a value exceeding US$ 138.9 Bn, as they strike the best balance between availability, cost, and scalability, which matches the core needs of most enterprises. With ~99.98% uptime, they meet business-critical reliability requirements without the high capex and operating costs of Tier-4 facilities. Growing demand from cloud service providers, BFSI, e-commerce, and SaaS players favors Tier-3 designs that support redundancy, compliance, and hybrid cloud integration. Rapid digitalization and edge deployments require flexible, modular infrastructure, an area where Tier-3 centers are the most practical choice.

Tier-4 is expected to grow at a CAGR of 17.8% as enterprises increasingly need zero-downtime environments to support always-on digital services, real-time analytics, and mission-critical workloads. The rise of AI training, cloud-native financial platforms, healthcare systems, and national digital infrastructure demands fault tolerance, full redundancy, and continuous operations even during maintenance or failures. Growing data sovereignty and regulatory pressure also push organizations to invest in highly resilient infrastructure within their own regions. As downtime costs escalate and service reliability becomes a competitive differentiator, demand naturally shifts toward Tier-4 facilities despite their higher upfront costs.

End-user Insights

Cloud service providers command the largest market share at over 37% in 2026, with a value exceeding US$ 128.5 Bn, due to enterprises increasingly needing on-demand scalability without heavy upfront capital investment. Businesses prioritize speed, flexibility, and global reach, which hyperscale cloud platforms deliver faster than traditional enterprise-owned data centers. The growing need for AI, analytics, and high-performance workloads favors cloud providers that can rapidly deploy advanced infrastructure. Organizations prefer cloud data centers to simplify operations, reduce IT complexity, and shift costs from CapEx to OpEx, aligning better with uncertain economic conditions.

IT & Telecom are expected to grow at a CAGR of 16.9% due to their core operations increasingly depending on always-on, low-latency digital infrastructure. Explosive growth in 5G, cloud services, streaming, and real-time communication is driving massive demand for scalable computing, storage, and interconnection capacity. Telecom operators need data centers to support edge computing for faster data processing closer to users. IT companies require highly secure, energy-efficient facilities to manage growing workloads from AI, SaaS platforms, and enterprise digital transformation.

Regional Insights

North America Data Center Market Trends

North America holds over 39% share in 2026, reaching US$ 135.5 Bn value, due to strong technology sector concentration, mature infrastructure ecosystems, and advanced regulatory frameworks. The United States drives regional growth, with Northern Virginia recording over 1,668 MW of net absorption in early 2025, about 43% year-over-year growth.

Major operators are locating facilities near renewable energy sources and committing to 100% renewable power to meet sustainability mandates and regulatory pressures. Innovation in the region focuses on hybrid interconnection models that combine colocation flexibility with cloud scalability, enabling multi-cloud deployments with vendor neutrality and lower operational costs. North America’s strong financial infrastructure, advanced real estate development capabilities, and access to top technical talent sustain its leadership and growth outlook through 2033.

Asia Pacific Data Center Market Trends

Asia Pacific is expected to achieve the highest CAGR of 18.5% in the forecast period, driven by rapid digital transformation, 5G rollout, and rising digital economies. The region attracted US$15.5 billion in cross-border investments in 2024, accounting for 70% of global data center investment flows, reflecting strong investor confidence.

Operational capacity reached about 12.7 GW in H1 2025, with 3.2 GW under construction and 13.3 GW in planning, supporting 4,174 MW of new capacity through 2027 backed by US$58.7 billion in infrastructure investments. India is the fastest-growing market, with capacity rising from 1,110 MW in 2024 to 2,070 MW by end-2025, driven by cloud expansion, digital payments, and BFSI digitalization. Southeast Asia is accelerating deployment, notably in Johor, Malaysia, where Equinix has launched new facilities to support ASEAN’s digital transformation.

Europe Data Center Market Trends

Europe is expected to achieve a robust share by 2026, with capacity concentrated in the FLAPD hubs Frankfurt, London, Amsterdam, Paris, and Dublin. Frankfurt supports about 750 MW of operational capacity and serves as a key connectivity hub for Central Europe and global financial networks. London is the largest market with 1.5 GW of capacity and has attracted over US$47 billion in investments between 2016 and 2024.

European data centers are increasingly adopting sustainability measures such as LEED and BREEAM certifications, renewable energy sourcing, and carbon neutrality goals to comply with strict regulations. Secondary markets in Spain, Portugal, and Italy are growing as operators seek expansion in regions with abundant renewable energy and lower costs compared to saturated primary markets.

Competitive Landscape

The global data center market demonstrates a hybrid competitive structure. Leading providers invest heavily in AI-powered data center operations, predictive maintenance capabilities, and autonomous resource orchestration platforms, reducing operational complexity and enabling remote management across geographically distributed facility networks. They focus on customization and modular designs to meet hyperscale and enterprise requirements while accelerating deployment. Competitive advantage is also driven by energy-efficient innovations, compliance with sustainability standards, and strong partnerships with cloud providers and telecom operators.

Key Industry Developments:

- In August 2025, ADB and GSA Data Center 01 signed a THB900 million (about $26.8 million) local currency green loan to fund the development and operation of a 25.6 MW colocation green data center in Samut Prakan, Thailand. The facility will be highly energy-efficient with a PUE of 1.4, Tier III certification for 99.982% uptime, and is expected to achieve LEED Gold certification.

- In June 2025, Ecolab Inc. launched its 3D TRASAR Technology for Direct-to-Chip Liquid Cooling, an AI-driven solution that monitors coolant health in real time to enhance data center cooling performance and protect servers. The technology expands Ecolab’s cooling portfolio across the entire data center landscape, helping operators optimize water and energy use as AI-driven demand increases.

Companies Covered in Data Center Market

- NTT Communications

- Schneider Electric

- ABB Ltd.

- Huawei Technologies Co., Ltd.

- Microsoft Corporation

- Equinix, Inc.

- Digital Realty

- Hitachi

- Microsoft

- EdgeConneX

- Google LLC

- IBM Corporation

- Cisco Systems, Inc.

- Dell Technologies

- Fujitsu Limited

- KDDI Corporation

- Comarch SA

- Others

Frequently Asked Questions

The global data center market is projected to be valued at US$347.3 Bn in 2026.

Exponential data growth from AI, cloud, and IoT demand scalable computing and storage infrastructure, are key drivers of the market.

The data center market is expected to witness a CAGR of 12.7% from 2026 to 2033.

Rising focus on sustainability and energy efficiency opens opportunities for green data centers, renewable energy integration, and advanced cooling solutions is creating strong growth opportunities.

NTT Communications, Schneider Electric, ABB Ltd., Huawei Technologies Co., Ltd., Microsoft Corporation, Equinix, Inc. are among the leading key players.