- Hardware & Software IT Services

- Data Mining Tools Market

Data Mining Tools Market Size, Share, and Growth Forecast 2026 - 2033

Data Mining Tools Market by Component (Software, Services), by Deployment (Cloud, On-Premise), by Industry (BFSI, Healthcare, Retail, IT & Telecom, Manufacturing, Government, Miscellaneous), by Enterprise Size (Large Enterprises, SMEs), and Regional Analysis, 2026 - 2033

Global Data Mining Tools Market Size and Trend Analysis

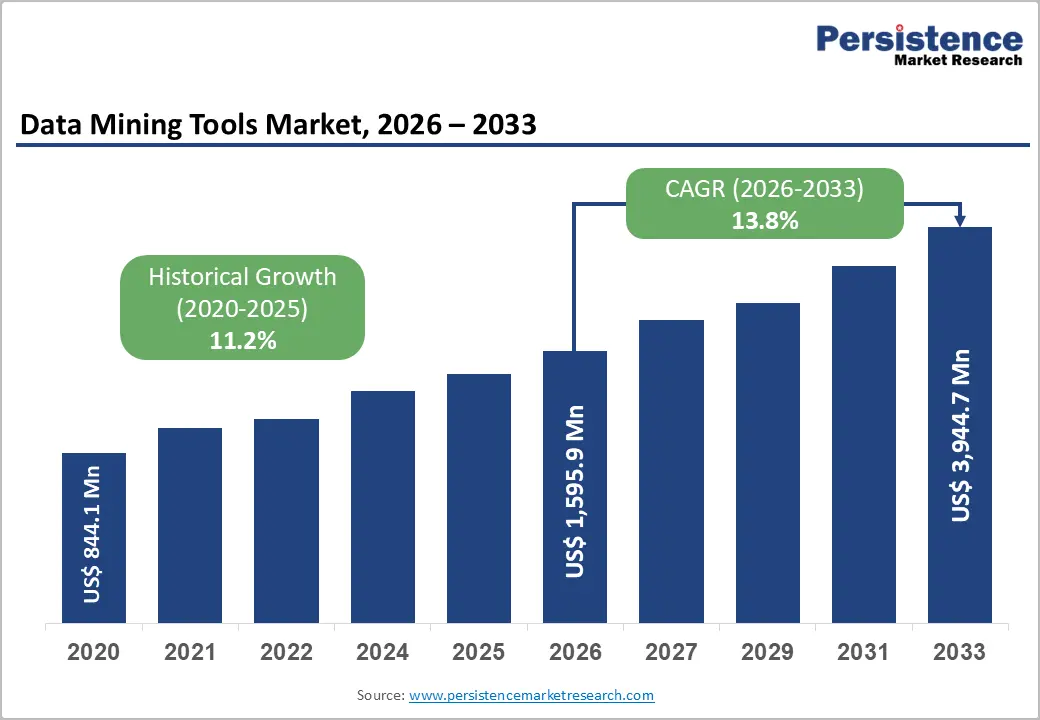

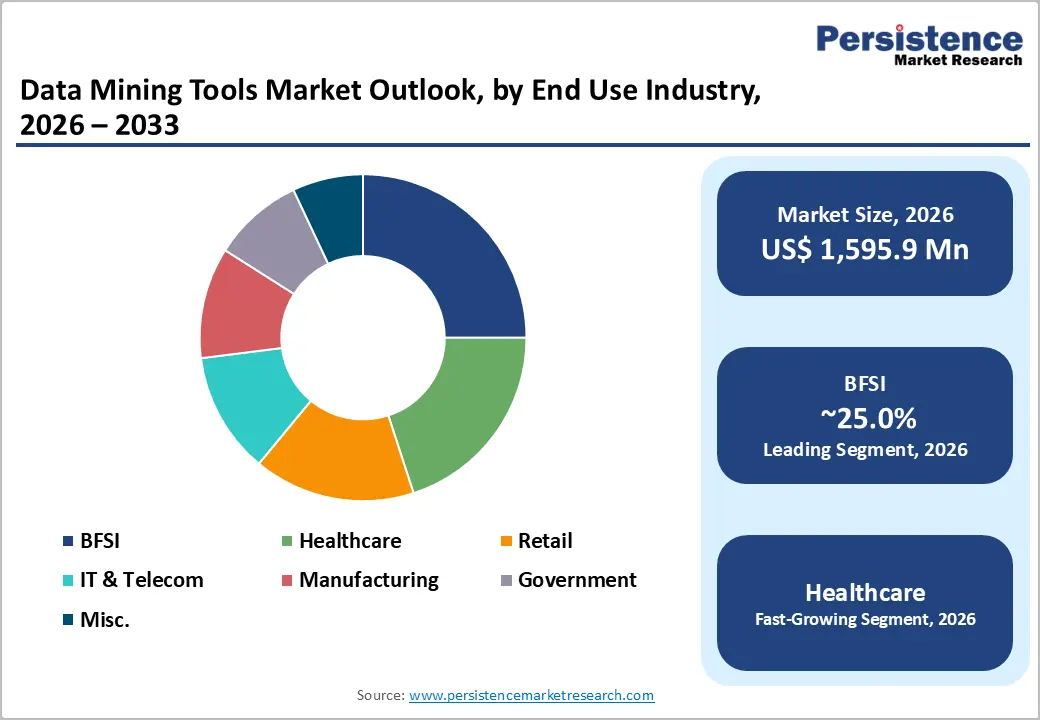

The global Data Mining Tools market size is expected to be valued at US$ 1,595.9 million in 2026 and projected to reach US$ 3,944.7 million by 2033, growing at a CAGR of 13.8% between 2026 and 2033. This robust growth trajectory is anchored in the exponential proliferation of enterprise data across sectors and the urgent need for organisations to extract actionable intelligence from increasingly complex datasets.

The accelerating adoption of artificial intelligence (AI) and machine learning (ML) frameworks within data mining platforms, combined with regulatory mandates for data governance and evidence-based decision-making in industries such as BFSI and healthcare, is compelling organisations of all sizes to invest in advanced data mining capabilities. The parallel shift toward cloud-native architectures is further reducing deployment barriers, enabling even small and medium enterprises (SMEs) to access sophisticated analytical tooling at scale.

Key Industry Highlights:

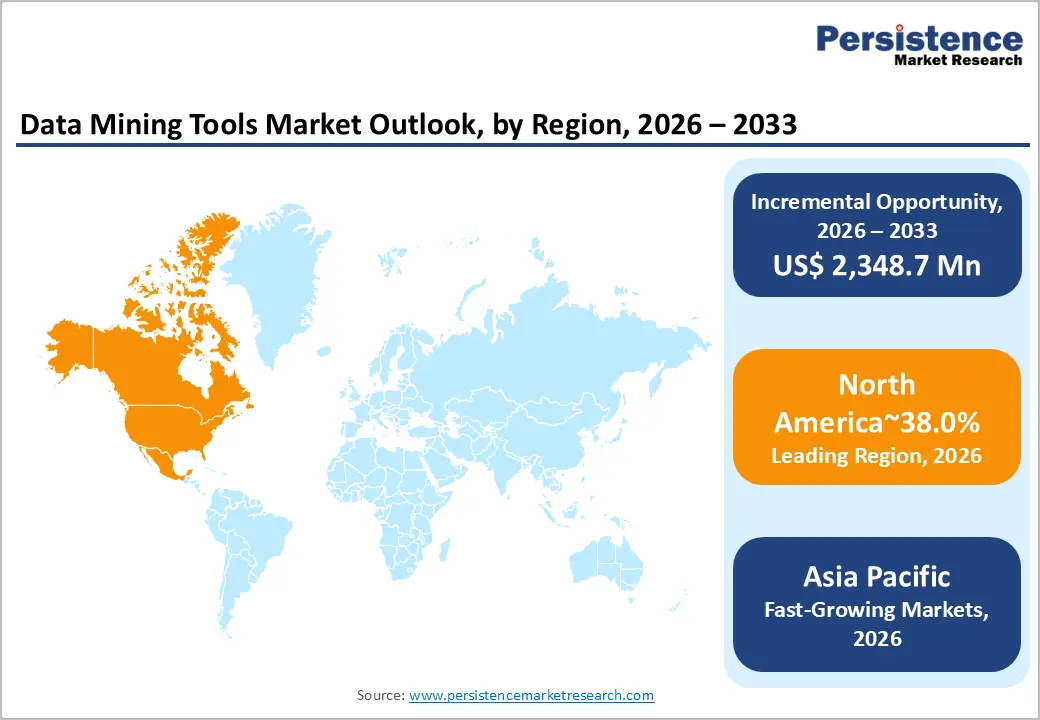

- North America leads the global data mining tools market with approximately 38% revenue share in 2025, driven by the highest concentration of enterprise software adoption, hyperscale cloud infrastructure, and data-intensive BFSI and healthcare sectors mandating advanced analytical compliance.

- Asia Pacific is the fast-growing market with a positive CAGR, fueled by China's data economy policies, India's simultaneous digitisation of BFSI and telecom at a billion-user scale, and Southeast Asia's accelerating financial inclusion and e-commerce data intensity.

- The software segment dominates with approximately 60% share in 2025, reflecting enterprise prioritisation of purpose-built mining platforms, AI/ML-integrated analytical suites, and SaaS-based mining tools that deliver scalable, governance-compliant pattern recognition across complex datasets.

- Services is the fast-growing category with a projected CAGR of ~12% through 2033, driven by surging enterprise demand for implementation consulting, managed analytics services, and model maintenance support as organisations scale data mining programs beyond initial deployments.

- The most compelling near-term market opportunity lies in healthcare sector digitisation, with the EU facing a shortfall of 1.2 million health professionals and one-third of its population projected to be over 65 by 2050, creating structurally durable demand for clinical data mining tools supporting precision medicine, resource optimisation, and population health management.

DRO Analysis

Drivers - Surge in Structured and Unstructured Enterprise Data Across Industries

The sheer volume, velocity, and variety of data generated across modern enterprises have reached unprecedented levels, creating a structural imperative for advanced data mining capabilities. According to IDC, the global datasphere is projected to surpass 175 zettabytes by 2025, with a significant proportion of this data remaining unanalyzed or underutilised without purpose-built mining tools. Industries such as BFSI, retail, and manufacturing are at the epicentre of this data deluge, generating transactional, behavioural, and operational data streams that demand real-time analytics.

The ability to mine structured databases alongside unstructured data sources, including logs, emails, and social media feeds, has elevated data mining tools from optional business intelligence add-ons to mission-critical infrastructure. Organisations that deploy mature data mining pipelines consistently demonstrate measurable improvements in customer retention, fraud detection accuracy, and supply chain optimisation, reinforcing capital allocation to these platforms.

Integration of Artificial Intelligence and Machine Learning Within Data Mining Platforms

The convergence of data mining with AI and ML has fundamentally altered the value proposition of analytical tools, enabling predictive and prescriptive capabilities that extend well beyond traditional descriptive analytics. According to the National Institute of Standards and Technology (NIST), AI integration within data processing workflows improves pattern recognition accuracy by orders of magnitude compared to rule-based systems, particularly in anomaly detection and predictive classification tasks.

In the BFSI sector alone, AI-enhanced data mining supports credit risk modelling, anti-money laundering (AML) pattern detection, and real-time fraud prevention capabilities that directly impact regulatory compliance and profitability. India's banking sector, which expanded 50 times in market capitalisation to reach US$ 1 trillion by 2025 while reducing gross NPAs from 5.8% in FY22 to 2.2% in FY25, exemplifies how data-driven decision-making powered by mining tools translates into measurable financial system resilience. Vendors are embedding AutoML, natural language processing (NLP), and deep learning modules directly within mining platforms, compressing the time from raw data ingestion to actionable insight.

Restraints - Data Privacy Regulations and Compliance Complexity

Stringent and evolving data privacy regulations present a tangible constraint on data mining tool deployment, particularly for cross-border and multi-cloud use cases. The European Union's General Data Protection Regulation (GDPR), the California Consumer Privacy Act (CCPA), and sector-specific mandates such as HIPAA in healthcare collectively impose strict limitations on how personal and sensitive data may be collected, stored, and processed.

Non-compliance penalties under GDPR can reach €20 million or 4% of global annual turnover, whichever is higher, creating significant legal and financial risk for organisations with immature data governance frameworks. These regulatory pressures slow procurement cycles and require vendors to invest heavily in compliance-ready architectures, audit trails, and data anonymisation capabilities, which are ultimately reflected in the total cost of ownership (TCO) for enterprise buyers.

Opportunities - Cloud-Native Deployment Models Unlocking SME and Emerging Market Demand

The transition to cloud-native data mining platforms represents one of the most significant demand-generation catalysts for market participants, particularly in reaching the previously underserved SME segment and high-growth emerging markets. Cloud deployment eliminates the prohibitive upfront capital expenditure associated with on-premise infrastructure, replacing it with subscription-based consumption models that align cost with measurable business value. Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP) have each embedded proprietary data mining and ML workbench capabilities within their platforms, accelerating enterprise cloud migration and tool adoption simultaneously.

Latin America's banking sector, where over 50% of adults remain unbanked, and institutions are deploying API-first core modernisation strategies, illustrates the transformative potential: as financial infrastructure digitises, data mining tools are among the first analytical layers deployed to support customer segmentation, credit scoring for thin-file borrowers, and real-time fraud detection. Cloud-native mining platforms with low-code interfaces are positioned to capture this democratization wave across Southeast Asia, the Middle East, and Sub-Saharan Africa.

Healthcare Sector Digitisation and Precision Medicine Adoption

Healthcare's accelerating digital transformation is creating substantial and structurally durable demand for data mining tools, driven by the imperative to derive clinical and operational insights from exponentially expanding patient datasets. The European Commission's report Health at a Glance: Europe 2024 underscores a structural crisis: the EU faces an estimated shortfall of 1.2 million doctors, nurses, and midwives, while nearly one-third of the EU's population will be over 65 by 2050, driving chronic disease burden and long-term care complexity to unprecedented levels.

Data mining tools capable of integrating electronic health records (EHRs), genomic datasets, imaging archives, and claims data are essential for enabling predictive diagnostics, hospital resource optimisation, and population health management. In India, the government's Ayushman Bharat program and the Tele-MANAS mental health initiative are generating large-scale patient data ecosystems that require sophisticated mining infrastructure. Brazil's healthcare market, representing 9.7% of GDP at approximately US$ 135 billion, with regulatory oversight by ANVISA and a dual public-private structure serving 72% of the population through the Unified Healthcare System (SUS), presents a high-value opportunity for vendors offering compliance-ready, interoperable data mining solutions.

Category-wise Analysis

Component Insights

The Software segment dominates the global data mining tools market, holding approximately 60% of the total market share in 2025. This leadership reflects the central role that purpose-built mining platforms, analytical suites, and embedded AI/ML toolkits play in enterprise data strategy. Software solutions spanning specialised tools such as IBM SPSS Modeler, SAS Enterprise Miner, RapidMiner, and open-source frameworks like Python-based scikit-learn provide the core algorithmic and visualization capabilities that drive data extraction, transformation, and pattern recognition workflows.

Enterprises across BFSI, retail, and IT & Telecom preferentially invest in software licenses and SaaS subscriptions as foundational analytical infrastructure. The growing embedding of AutoML and NLP capabilities within mining software platforms further reinforces this segment's dominance by expanding the addressable user base beyond specialized data scientists to business analysts and domain experts.

Deployment Insights

The cloud deployment is the leading segment and accounted for 58% share in 2025, reflecting the broad enterprise transition toward scalable, infrastructure-light analytical architectures. Cloud-hosted data mining platforms offer critical advantages, including elastic compute capacity for large-scale batch and real-time processing, built-in integration with enterprise data lakes and warehouses, and consumption-based pricing that aligns tool costs with analytical output.

The EU information and communication services sector, employing nearly 7.2 million people and contributing €667 billion in value added in 2022, increasingly deploys cloud-based analytical tooling to support software-driven service delivery. The On-Premises segment retains meaningful share among regulated industries such as government, defence, and financial services, where data residency and sovereignty requirements constrain cloud migration timelines.

Industry Insights

The BFSI sector is the dominant end-use segment for data mining tools, commanding approximately 28% of global market share in 2025. Financial institutions rely on data mining for a uniquely broad range of mission-critical applications: credit risk scoring, fraud pattern detection, customer lifetime value modelling, regulatory stress testing, and AML compliance. The sector's data intensity and regulatory accountability invest in mining tools a strategic necessity rather than a discretionary spend.

In Europe, the banking sector held total assets of €43.6 trillion in 2023 with over 2 million employees, while China's banking and insurance sectors reported total banking assets of RMB 467.3 trillion, up 7.9% year-on-year as of Q2 2025, with inclusive loans to micro and small enterprises rising 12.3% to RMB 36 trillion all generating vast transactional datasets requiring continuous mining for risk and performance management. India's BFSI sector, now contributing 27% of GDP, further exemplifies data-mining-intensive growth at scale.

Regional Insights

North America Data Mining Tools Market Trends and Insights

North America holds the leading regional position in the global Data Mining Tools market, capturing approximately 38% of the total revenue share in 2025. The region benefits from a concentration of technology innovation hubs, a deep enterprise IT investment culture, and a regulatory environment that actively incentivises data-driven decision-making across regulated industries.

The mature presence of global software vendors, hyperscale cloud providers, and a high density of data-intensive sectors, including financial services, healthcare, and e-commerce, sustains consistent demand for advanced mining platforms. North American enterprises were early adopters of AI-integrated analytics, and this technology maturity translates directly into premium tool procurement and high per-seat licensing revenues.

U.S. Data Mining Tools Market Size

The U.S. Data Mining Tools market is valued at approximately US$ 469.0 million in 2025, driven by the structural convergence of three mutually reinforcing forces: the world's largest enterprise software ecosystem, regulatory mandates in BFSI and healthcare compelling evidence-based analytics, and aggressive AI investment by hyperscale platforms.

The U.S. Federal Reserve's supervisory stress testing framework and SEC reporting obligations generate persistent demand for financial data mining tools, while the Health Information Technology for Economic and Clinical Health (HITECH) Act has catalyzed EHR data standardisation, creating mining-ready clinical datasets across thousands of health networks. North America's B2B eCommerce GMV, part of a global market projected at US$ 36,163 billion by 2026, further drives retail and supply chain data mining investment.

Europe Data Mining Tools Market Trends and Insights

Europe accounts for approximately 24% of the global Data Mining Tools market revenue in 2025, underpinned by the region's stringent data governance culture, advanced IT services sector, and the structural digitisation momentum driven by the EU's Data Strategy and the European Health Data Space (EHDS) initiative.

The GDPR framework, while imposing compliance costs, has simultaneously elevated the strategic value of privacy-compliant data mining tools that can deliver analytical depth within defined processing boundaries. Germany and the U.K. serve as the primary demand centres, anchored by their large financial services industries, export-oriented manufacturing intelligence requirements, and mature enterprise software adoption. The EU's information and communication services sector generated €667 billion in value added in 2022 with 7.2 million employees, reflecting the institutional scale of European data infrastructure investment.

Germany Data Mining Tools Market Size

Germany's Data Mining Tools market is valued at approximately US$ 74.0 million in 2025, reflecting the country's position as the EU's largest economy and its industrial data analytics imperative. Germany's manufacturing sector, home to global automotive and industrial machinery leaders, is deeply invested in predictive maintenance, quality control analytics, and supply chain intelligence powered by data mining platforms.

Eurostat confirms Germany contributes over 22% of EU-wide IT sector value added, providing an institutional foundation for enterprise-grade mining tool deployment. The country's Industrie 4.0 national strategy has explicitly prioritised data analytics as a core competency for manufacturing competitiveness, embedding mining tools into factory floor digital transformation programs.

U.K. Data Mining Tools Market Size

The U.K. Data Mining Tools market is valued at approximately US$ 67.3 million in 2025, sustained by London's position as Europe's leading financial center and the country's advanced financial services regulatory infrastructure.

The Financial Conduct Authority (FCA) and Prudential Regulation Authority (PRA) mandate sophisticated risk data aggregation and reporting capabilities that directly require enterprise data mining solutions. The U.K.'s post-Brexit independent data regulation trajectory, including the Data Protection and Digital Information (DPDI) Act, is creating opportunities for vendors offering compliant, domestically hosted analytical platforms tailored to U.K.-specific financial and healthcare reporting requirements.

Asia Pacific Data Mining Tools Market Drivers and Analysis

Asia Pacific holds approximately 26.0% of the global Data Mining Tools market revenue in 2025 and is the fastest-growing region, projected to expand at a CAGR exceeding 16% through 2033. China anchors the region's market with the largest absolute revenue base, while India, Japan, and Southeast Asia collectively represent the most dynamic growth frontiers.

The region's growth is structurally supported by government-led digital transformation programs, rapid cloud infrastructure buildout, and the emergence of large-scale digital data ecosystems in BFSI, healthcare, and e-commerce. APAC's dominance in B2B eCommerce, accounting for approximately 80% of global B2B eCommerce GMV by 2026, underscores the region's data intensity and corresponding analytical infrastructure investment imperative. According to ITU, approximately 74% of the global population was online in 2025, with Asia Pacific markets accounting for the largest share of the 1.3 billion new internet users added between 2020 and 2025, generating unprecedented volumes of mineable behavioural and transactional data.

China Data Mining Tools Market Size

China's Data Mining Tools market is valued at approximately US$ 116.7 million in 2025, propelled by the country's state-directed data economy ambitions and the immense scale of its digital financial and industrial ecosystems. China's banking sector alone reported total assets of RMB 467.3 trillion (up 7.9% YoY) and insurance assets of RMB 39.2 trillion (up 9.2%) as of Q2 2025, generating transaction and risk data at a scale requiring industrial-grade mining infrastructure.

The Ministry of Industry and Information Technology (MIIT)'s data element market policies and the 14th Five-Year Plan's emphasis on digital economy development have institutionalised data mining tool investment across government-linked enterprises and state-owned banks, ensuring sustained public sector demand alongside rapidly growing private sector adoption.

India Data Mining Tools Market Size

India's Data Mining Tools market is valued at approximately US$ 65.6 million in 2025 and is among the fastest-growing country-level markets globally, underpinned by the simultaneous digitization of its banking, telecom, and healthcare sectors at an unparalleled scale. India's telecom sector now serves 1.21 billion subscribers with gross revenues rising from US$ 39.22 billion in FY24 to US$ 43.42 billion in FY25, and total wireless data usage rising 17.46% YoY, is generating behavioural and network data streams that require sophisticated mining for churn prediction, network optimisation, and personalised service delivery.

Concurrently, India's BFSI sector's market capitalisation expansion to US$ 1 trillion by 2025, with NPAs falling to 2.2%, has elevated the sophistication of risk analytics and fraud detection systems, directly driving data mining tool procurement across both public sector banks and fast-growing NBFCs and fintechs.

Competitive Landscape

The global data mining tools market exhibits a moderately fragmented competitive structure, with a handful of established technology conglomerates, including IBM, SAS Institute, Microsoft, Oracle, and SAP, maintaining dominant positions through deep enterprise relationships, broad product portfolios, and continuous R&D investment. However, the proliferation of open-source frameworks and cloud-native analytical platforms has meaningfully lowered barriers to entry, enabling specialised vendors and emerging AI-native startups to compete effectively in specific verticals and use cases.

Market leaders differentiate through ecosystem integration depth, regulatory compliance certifications, and the quality of embedded AI/ML capabilities. A notable strategic trend is the shift from standalone tool licensing toward unified data intelligence platforms offered as SaaS subscriptions, blurring the boundary between data mining, business intelligence, and AI platforms. Emerging vendors are gaining traction through vertical-specific solutions in BFSI, healthcare, and retail that deliver pre-built mining models and industry-specific compliance frameworks, challenging incumbents on time-to-value.

Key Market Developments

- March 2025: IBM announced an expansion of its watsonx platform with enhanced automated data mining and pattern discovery capabilities, integrating generative AI-powered data cataloging that reduces manual feature engineering time by up to 60% for enterprise analytics teams.

- November 2024: Microsoft launched advanced data mining and anomaly detection modules within Azure Synapse Analytics, enabling real-time mining across petabyte-scale data warehouses with native integration into Microsoft Fabric, accelerating enterprise adoption of unified analytical architectures.

- July 2024: SAS Institute unveiled SAS Viya 4.0 upgrades featuring AI-driven automated model building and explainability enhancements, specifically targeting regulated industries including banking and pharmaceuticals, reinforcing its position in compliance-sensitive data mining deployments.

Global Data Mining Tools Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 844.1 Million |

|

Current Market Value (2026) |

US$ 1,595.9 Million |

|

Projected Market Value (2033) |

US$ 3,944.7 Million |

|

CAGR (2026–2033) |

13.8% |

|

Leading Region |

North America, ~38% market share (2025) |

|

Dominant Category-1 (Component) |

Software, ~60% market share (2025) |

|

Top-ranking Category-2 (Deployment) |

Cloud, ~58% market share (2025) |

|

Incremental Opportunity (2026–2033) |

~US$ 2,348.8 Million |

Companies Covered in Data Mining Tools Market

- IBM Corporation

- SAS Institute Inc.

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Teradata Corporation

- Alteryx Inc.

- RapidMiner Inc.

- TIBCO Software Inc.

- MicroStrategy Incorporated

- Qlik Technologies Inc.

- Databricks Inc.

- Palantir Technologies Inc.

- H2O.ai

- DataRobot Inc.

- Knime AG

- Sisense Inc.

Frequently Asked Questions

The global Data Mining Tools market is valued at US$ 1,595.9 million in 2026, up from US$ 844.1 million in 2020, reflecting a historical CAGR of 11.2% between 2020 and 2025. The market is projected to reach US$ 3,944.7 million by 2033 at a CAGR of 13.8%, driven by AI integration, cloud adoption, and expanding data volumes across industries.

Explosive growth in enterprise data and the integration of AI/ML are driving strong demand for advanced data mining tools with predictive capabilities. Cloud adoption and regulatory compliance requirements are further accelerating enterprise-wide deployment across key industries.

North America leads the global Data Mining Tools market with approximately 38% revenue share in 2025, anchored by the United States, whose market is valued at approximately US$ 469.0 million.

The biggest opportunity lies in healthcare digitisation and ageing populations, driving massive clinical data generation. This is creating strong demand for advanced data mining tools to enable predictive diagnostics, population health management, and resource optimisation through 2033.

The global Data Mining Tools market is led by IBM Corporation (WatsonX Platform), SAS Institute Inc. (SAS Viya), Microsoft Corporation (Azure Synapse Analytics), Oracle Corporation, and SAP SE.