- Hardware & Software IT Services

- Data Protection-as-a-Service (DPaaS) Market

Data Protection-as-a-Service (DPaaS) Market Size, Share, and Growth Forecast 2026 - 2033

Data Protection-as-a-Service (DPaaS) Market by Service Type (Disaster Recovery as a Service (DRaaS), Backup as a Service (BaaS), Storage as a Service (STaaS), Others), Deployment Model (Public Cloud DPaaS, Private Cloud DPaaS, Hybrid Cloud DPaaS), Industry (BFSI, Government, Healthcare, Retail & Ecommerce, IT & Telecommunication, Manufacturing, Others), Regional Analysis, 2026 - 2033

Data Protection-as-a-Service (DPaaS) Market Size and Trend Analysis

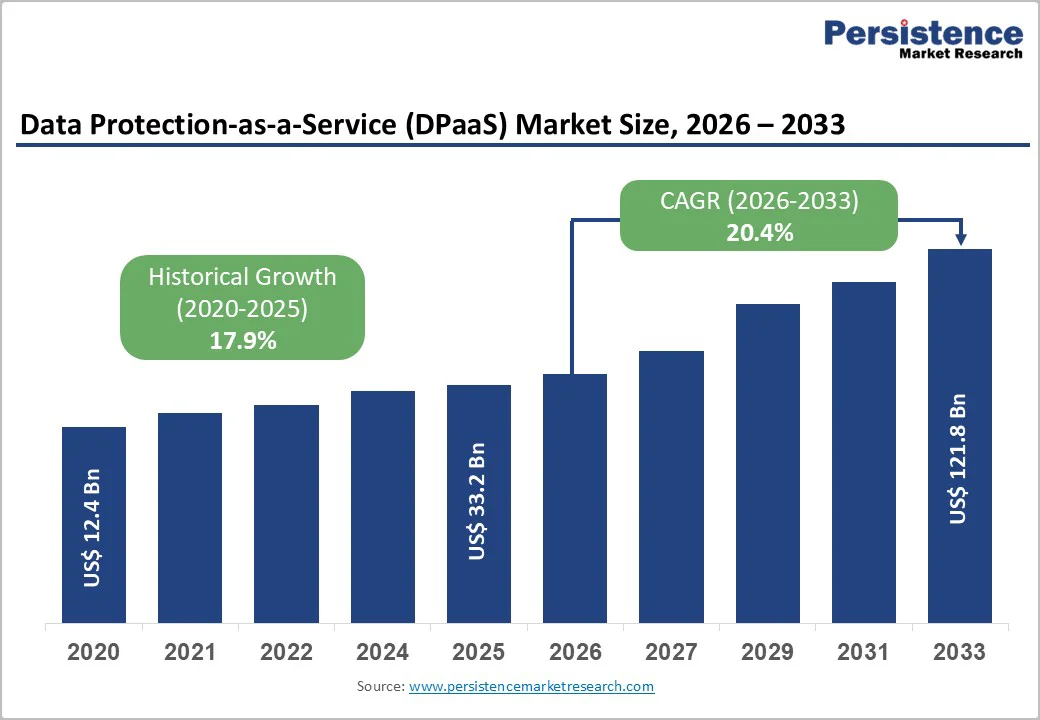

The global data protection-as-a-service (DPaaS) market is projected to be valued at US$ 33.2 billion in 2026 and is expected to reach US$ 121.8 billion by 2033, growing at a CAGR of 20.4% between 2026 and 2033. The market is experiencing strong growth fueled by a sharp rise in ransomware attacks, which increased by 34% globally in the first three quarters of 2025 compared to the same period in 2024, pushing organizations to adopt cloud-based data protection for better resilience.

At the same time, stricter regulatory requirements such as GDPR in Europe and India’s Digital Personal Data Protection Act (2023) are compelling financial institutions and healthcare providers to implement comprehensive data protection frameworks, accelerating the shift toward DPaaS solutions that offer scalable, automated, and cost-effective alternatives to traditional on-premises backup systems.

Key Industry Highlights:

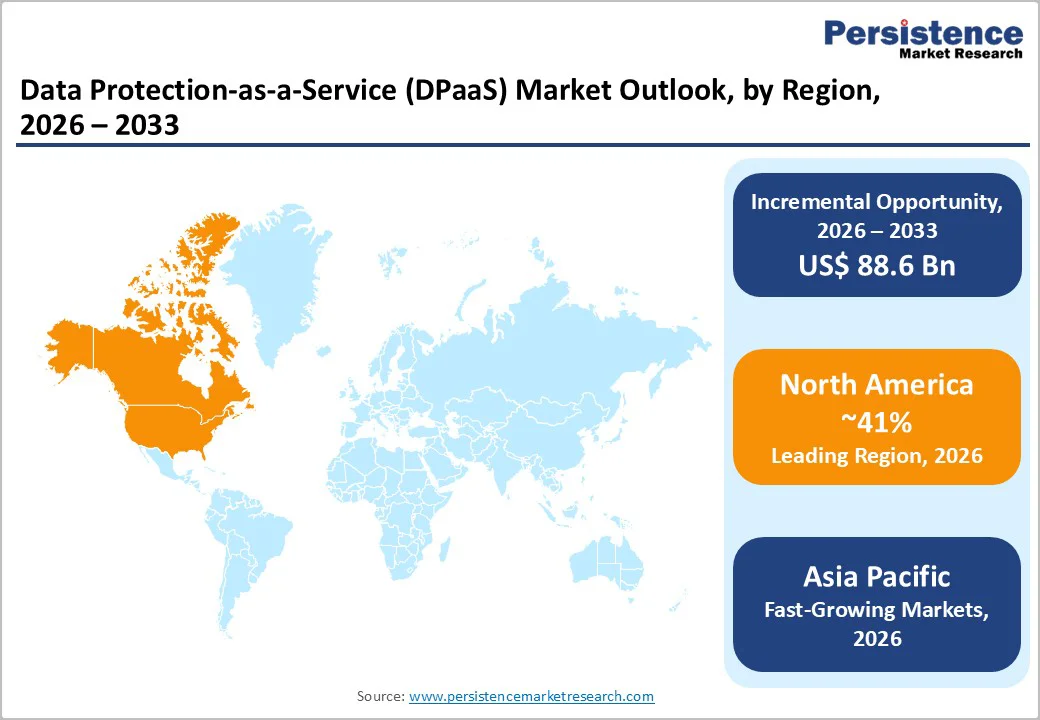

- Leading Region: North America leads the DPaaS market with 41% share in 2025, supported by its large data center base, high cybersecurity spending, and strong presence of major cloud and data protection providers.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a 31.4% CAGR, driven by rapid multi-cloud adoption, rising cybersecurity expenditure, large-scale data center investments, and government-led digital transformation initiatives.

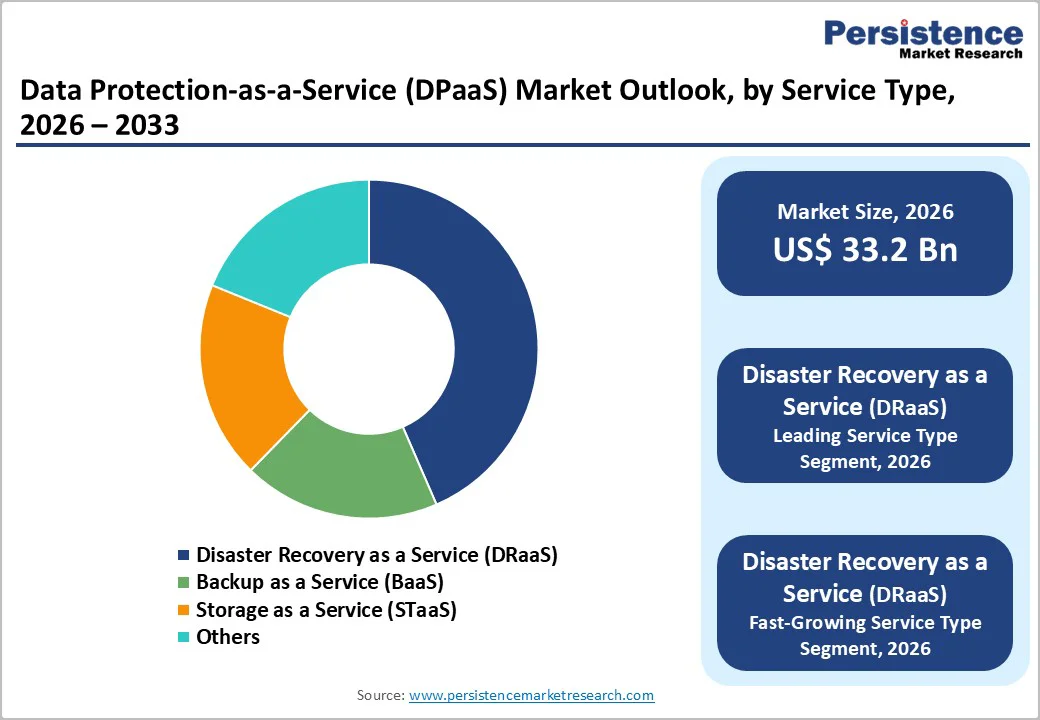

- Dominant Service Type Segment: DRaaS holds the dominant 38% service share in 2025, expanding rapidly due to rising ransomware threats and increasing enterprise adoption of automated, SIEM-integrated disaster recovery capabilities.

- Fastest Growing Deployment Model: Hybrid cloud DPaaS is the fastest-growing deployment model at 31.5% CAGR, propelled by regulatory mandates prioritizing localized data retention and compliant multi-cloud architectures, especially across Europe’s financial sector.

- Key Market Opportunity: AI-integrated DPaaS solutions offer the strongest market opportunity, as machine learning–driven automation, predictive analytics, and high-speed recovery capabilities significantly enhance enterprise resilience and reduce data restoration times.

| Key Insights | Details |

|---|---|

|

Data Protection-as-a-Service (DPaaS) Market Size (2026E) |

US$ 33.2 Bn |

|

Market Value Forecast (2033F) |

US$ 121.8 Bn |

|

Projected Growth CAGR (2026-2033) |

20.4% |

|

Historical Market Growth (2020-2025) |

17.9% |

Market Dynamics

Drivers - Rise in Cyber Threat Landscape Driving Enterprise Investment in Data Protection

The unprecedented rise in cyberattacks has emerged as a primary catalyst propelling DPaaS market expansion. According to industrial cyber intelligence reports, ransomware attacks on businesses surged from 1,195 incidents in the second quarter of 2025 to 1,325 in the third quarter, representing an 11% increase, with manufacturing industries bearing the brunt with 296 attacks in the third quarter alone. The average ransom demanded across all attacks reached $3 million, while the financial sector witnessed 65% of organizations experiencing ransomware attacks in 2024, compared to 34% in 2021.

These alarming statistics have compelled enterprises to adopt DPaaS solutions that offer immutable backups, air-gapped storage, and rapid recovery capabilities. Sophisticated threat actors are leveraging AI-enhanced attack vectors, making traditional backup systems inadequate, thereby pushing organizations toward cloud-native protection services that incorporate machine learning-based anomaly detection and automated threat response mechanisms. The global ransomware payment volume reached $800 million in 2024, with average ransom payments jumping from $400,000 in 2023 to $2 million in 2024, underscoring the critical need for resilient data protection strategies that DPaaS providers deliver through continuous data protection streams and policy-driven immutability1.

Stringent Regulatory Compliance Requirements Accelerating Cloud-Based Data Protection Adoption

The tightening global regulatory landscape surrounding data privacy and protection has become a fundamental driver for DPaaS market growth. The European Union’s GDPR enforcement has intensified significantly, with data protection authorities issuing 2,245 fines totaling €5.65 billion as of March 2025, with Spain leading enforcement actions with 932 published fines. In the banking and financial services sector, India’s Draft Digital Personal Data Protection Rules (2025) mandate that financial institutions implement robust data protection measures including encryption, pseudonymization, and masking, with data fiduciaries required to maintain consent records for a minimum of seven years.

The BFSI sector faces particularly stringent requirements, with the Reserve Bank of India’s Master Direction on Information Technology Governance (2023) making DPDP Act compliance mandatory for all regulated entities. Healthcare organizations are navigating evolving HIPAA regulations in 2025 that introduce multi-factor authentication requirements, reduce maximum access time for protected health information from 30 days to 15 days, and mandate enhanced cybersecurity protocols, including data encryption and regular penetration testing. These regulatory pressures are driving enterprises toward DPaaS solutions that offer built-in compliance frameworks, automated backup processes aligned with regulatory timelines, and comprehensive audit trails that simplify demonstrating adherence to legal requirements while reducing the operational burden on internal IT teams.

Restraints - Data Sovereignty Concerns and Cross-Border Transfer Restrictions Limiting Market Penetration

Data sovereignty requirements and cross-border transfer restrictions are increasingly limiting DPaaS market penetration, particularly in regions adopting strict localization mandates. Regulations such as India’s Digital Personal Data Protection Rules (2025), which restrict transfers to non-approved countries and require Significant Data Fiduciaries to store sensitive data within national borders, significantly increase compliance complexity. China’s Cybersecurity Law enforces similarly stringent data localization rules, while Saudi Arabia’s Data Protection and Cybersecurity Law mandates in-country storage and processing for critical and sensitive sectors. These policies force DPaaS providers to invest in sovereign cloud facilities, rising costs and fragmenting service models. The lack of global regulatory harmonization further complicates operations, leaving organizations uncertain about compliance obligations across jurisdictions and delaying DPaaS adoption decisions.

Integration Complexities and Legacy System Compatibility Challenges

Integration challenges with heterogeneous IT environments and legacy systems continue to restrain DPaaS adoption, as enterprises often operate hybrid infrastructures spanning physical servers, virtualized environments, and multiple cloud platforms. Ensuring seamless backup and recovery across complex workloads such as SAP HANA, Oracle databases, and Microsoft Exchange requires advanced application-consistent capabilities that many organizations struggle to implement. SMEs face even greater difficulties due to limited cloud expertise, with most reporting that their existing infrastructure is not adequately prepared for cloud-native applications. The shared responsibility model adds further ambiguity by requiring organizations to secure their own data despite using cloud-based protection. Integrating DPaaS with SIEM, IAM, and compliance monitoring tools demands specialized skills that many internal teams lack, resulting in deployment delays, misconfigurations, and reduced effectiveness of DPaaS solutions.

Opportunity - Artificial Intelligence and Machine Learning Integration Revolutionizing Data Protection Capabilities

The convergence of AI and machine learning technologies with DPaaS solutions presents transformative opportunities for market participants to deliver next-generation data protection capabilities. Cohesity’s introduction of Gaia, a generative AI enterprise search assistant leveraging large language models and retrieval augmented generation, demonstrates how AI can enable conversational interactions with backup data, allowing compliance and legal teams to ask intelligent questions such as whether patient confidential data has been sent outside healthcare organizations. The integration of predictive analytics enables DPaaS providers to identify anomalous backup patterns that may indicate ransomware encryption attempts, with 99.99% accuracy in identifying cyber threats and reducing recovery time by up to 80%. Organizations deploying AI-enhanced DPaaS solutions can benefit from automated policy recommendations, intelligent data classification, and proactive threat mitigation, positioning vendors who invest in AI capabilities to capture significant market share as enterprises prioritize automation and advanced threat detection in their data protection strategies.

Hybrid and Multi-Cloud Deployment Models Creating Expansive Growth Potential

The accelerating shift toward hybrid and multi-cloud architectures represents a substantial opportunity for DPaaS providers to deliver unified data protection across diverse IT environments. Market research indicates that 89% of organizations have embraced a multicloud model as of 2024, with 73% specifically utilizing hybrid cloud configurations that combine on-premises infrastructure with public cloud resources. Government initiatives including India’s Digital India program explicitly encourage multi-cloud and hybrid strategies, creating fertile ground for DPaaS adoption. Dell APEX Backup Services has expanded to include cloud-native capabilities for AWS and Azure virtual machines, providing snapshot orchestration for operational recovery and creating protected copies to defend against ransomware, while enabling cross-cloud backup redundancy by replicating data from Azure VMs to AWS cloud. The European Union’s implementation of the Digital Operational Resilience Act (DORA) mandates that financial institutions document contingency arrangements for third-party services, driving demand for hybrid DPaaS architectures that keep sensitive datasets on local private clouds while enabling burstable analytics in regulated public regions.

Category-wise Analysis

Service Type Insights

Disaster Recovery as a Service (DRaaS) leads the Service Type category with a 38% market share in 2025, driven by rising enterprise emphasis on resilience and business continuity amid escalating ransomware threats. The segment is projected to grow at a 29.5% CAGR through 2030 as organizations increasingly adopt automated failover and continuous data protection to meet stringent recovery requirements. More than 70% of enterprises plan to integrate DRaaS with SIEM systems by 2026 to enable automated, threat-aware failover that reduces recovery point objectives to seconds. Regulatory mandates such as Europe’s DORA, requiring annual disaster recovery testing for financial institutions, are accelerating DRaaS deployment across highly regulated industries where near-zero data loss and rapid restoration are critical.

Deployment Model Insights

Hybrid Cloud DPaaS is the fastest-growing deployment model with a projected 31.5% CAGR between 2025 and 2033, supported by enterprises seeking to balance regulatory compliance, data control, and cloud scalability. The hybrid model is gaining traction as organizations retain sensitive workloads on private clouds while leveraging public cloud environments for analytics and non-critical applications. This architecture aligns strongly with regulatory expectations, particularly for European institutions navigating DORA requirements and GDPR enforcement. With 73% of organizations already using hybrid cloud setups, demand is being further supported by growing multi-cloud adoption in markets such as India, where hybrid strategies are expanding under national digitalization programs. Vendors are enhancing hybrid DPaaS capabilities through cross-cloud replication and automated policy-driven data placement, making this model ideal for complex compliance-driven environments.

Industry Insights

The Banking, Financial Services, and Insurance (BFSI) sector holds a dominant 34% share of the DPaaS market in 2025, driven by stringent compliance requirements and heightened cybersecurity risks. Financial institutions face increasing regulatory pressures, including India’s DPDP Rules (2025), RBI’s IT Governance mandates, and GDPR enforcement across Europe, all of which require strong data protection, monitoring, encryption, and retention practices. With approximately 65% of financial organizations reporting ransomware attacks in 2024, the sector is accelerating adoption of DPaaS solutions that provide automated recovery, immutable storage, and comprehensive audit trails. BFSI’s complex data volumes, critical infrastructure dependencies, and high security expectations make advanced DPaaS platforms essential for maintaining operational continuity while meeting expanding regulatory obligations.

Regional Insights

North America Data Protection-as-a-Service (DPaaS) Market Trends

North America continues to dominate the global DPaaS landscape with an estimated 41% market share in 2025, driven by a highly developed cloud ecosystem and the presence of major service providers such as AWS, Microsoft, Google Cloud, IBM, Oracle, Dell Technologies, and Cisco. The United States hosts more than 2,600 data centers, accounting for about 40% of global capacity, supported by nearly USD 40 billion in data center construction spending recorded by June 2025.

Hyperscaler investment remains a core growth catalyst, with Microsoft’s USD 40 billion AI-focused data center outlay in 2024 and a planned USD 80 billion allocation for FY2025 reinforcing long-term cloud adoption. The region also faces the world’s highest data breach cost at USD 10.22 million in 2025, pushing enterprises toward DPaaS platforms that ensure rapid recovery, immutable backups, and ransomware-resilient storage. Compliance frameworks such as CCPA, GLBA, HIPAA, and FISMA further encourage adoption of secure, auditable, and automated cloud-based data protection systems.

Europe Data Protection-as-a-Service (DPaaS) Market Trends

Europe represents one of the most regulated and compliance-driven DPaaS markets, heavily shaped by GDPR, which has resulted in €5.65 billion in cumulative fines and 2,245 enforcement actions as of March 2025. Spain leads with 1,021 penalties totaling €120.75 million by September 2025, while Germany, France, Italy, and the U.K. maintain stringent enforcement through national-level data protection authorities. The region invested nearly €2 billion in new data center capacity in 2024, supporting ongoing digital transformation in BFSI, healthcare, manufacturing, and public sector operations.

The implementation of the EU Digital Operational Resilience Act (DORA) requires financial institutions to conduct rigorous ICT risk testing, including full-scale annual disaster recovery drills, accelerating demand for DRaaS platforms that support continuous monitoring and near-zero-loss failover. Organizations increasingly prefer DPaaS solutions with localized data storage, multi-region redundancy, strong encryption controls, and certification compliance such as GDPR, ISO 27001, PCI DSS, and SOC 2, reinforcing a trust-driven adoption environment across Europe.

Asia Pacific Data Protection-as-a-Service (DPaaS) Market Trends

Asia Pacific is the fastest-growing DPaaS market, expected to expand at a 31.4% CAGR from 2025 to 2033, supported by rapid cloud adoption, digitalization, and escalating cybersecurity risks. India’s cybersecurity expenditure is set to grow 16% to more than USD 3.0 billion in 2025, aligned with the Digital Personal Data Protection Act (2023) and MeitY’s USD 2 billion investment in national data center infrastructure during 2024. India’s multi-cloud market is forecast to reach USD 40 billion by 2033, reflecting a very high CAGR. China’s strict Cybersecurity Law (2017) enforces data localization, prompting global cloud providers to operate through sovereign, telecom-backed cloud zones.

Enterprises across APAC face an average of 1,636 cyberattacks per organization per week, a 30% year-over-year increase, pushing demand for ransomware-resilient DPaaS platforms. Adoption is further strengthened by digital initiatives across Japan, South Korea, Singapore, Australia, and ASEAN, where organizations seek scalable, compliant, and automated cloud-based data protection systems.

Competitive Landscape

The global data protection-as-a-service (DPaaS) market features a moderately consolidated structure, shaped by a mix of large cloud platform providers and specialized data-protection vendors. Competition is driven less by brand presence and more by platform breadth, integration depth, and cyber-resilience capabilities. Hyperscale cloud providers benefit from global infrastructure and embedded data-protection functions, strengthening their position through tightly unified cloud ecosystems. Specialist vendors compete by offering advanced ransomware defense, immutable storage, hybrid-cloud orchestration, and policy-based automation, enabling differentiation in complex enterprise environments.

The market is undergoing rapid convergence, with backup, disaster recovery, and storage services being integrated into unified, policy-driven architectures that deliver simplified management and auditability. Strategic activity remains high, supported by mergers, portfolio consolidation, and partnerships aimed at expanding service coverage and geographic scale. Across the landscape, vendors are prioritizing AI-driven threat detection, cross-cloud compatibility, and automation as core levers to enhance value propositions and secure long-term competitive advantage.

Key Market Developments:

- April, 2024: Dell Technologies expanded its data-protection portfolio with “Dell APEX Backup Services” and enhanced PowerProtect appliances, delivering faster backups and restores and integrated GenAI-based backup management.

- August, 2025: Hewlett Packard Enterprise launched its “HPE Alletra Storage MP X10000” backed by its data-protection stack and the “HPE Zerto” integration hub (with CrowdStrike Falcon), claiming up to 1.2 PB/hour backup throughput and real-time ransomware detection with instant recovery from seconds-prior clean points.

Companies Covered in Data Protection-as-a-Service (DPaaS) Market

- IBM Corporation

- Cisco Inc.

- Dell Inc.

- Amazon Web Services Inc.

- Veritas Technologies LLC

- HP Development Company

- Microsoft Corporation

- Oracle Corporation

- Quantum Corporation

- Asigra Inc.

- Hewlett Packard Enterprise Company

- Quest Software Inc.

- Huawei Technologies Co., Ltd.

- Hitachi Vantara LLC

- Cohesity Inc.

- Commvault Systems Inc.

- Veeam Software

- Druva Inc.

- Rubrik Inc.

- Acronis International GmbH

Frequently Asked Questions

The DPaaS market is projected to reach US$ 121.8 Bn by 2033, growing from US$ 33.2 Bn in 2026 at a 20.4% CAGR.

Demand is driven by rising ransomware attacks, stricter global data protection regulations, and rapid adoption of hybrid and multi-cloud environments.

DRaaS leads with a 38% market share in 2025, expanding fastest due to rising business continuity needs and ransomware-driven resilience investments.

North America leads with 41% share in 2025 owing to high data center concentration, strong cybersecurity spending, and stringent regulatory frameworks.

Key opportunities include AI-driven data protection, multicloud integration demand, and rapid APAC digitalization supported by data-localization initiatives.