- Food Ingredients & Additives

- Roasted Corn Market

Roasted Corn Market Size, Share, and Growth Forecast 2026 - 2033

Roasted Corn Market by Form (Whole, Splits, Flour), by Nature (Organic, Conventional), by End Use (Beverages, Bakery, Snacks & Convenience Food, Animal Feed, Others), by Regional Analysis, 2026-2033

Roasted Corn Market Size and Share Analysis

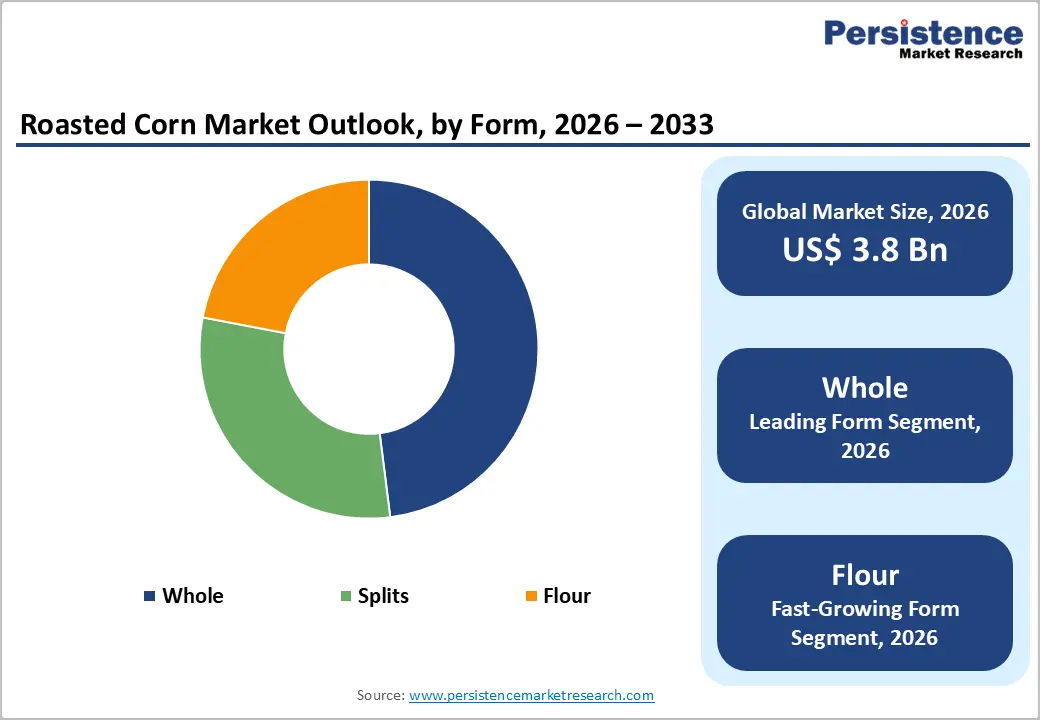

The global Roasted Corn market size is expected to be valued at US$ 3.8 billion in 2026 and projected to reach US$ 5.5 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033

The expansion of this market is fundamentally driven by a global shift toward plant-based, fiber-rich snacking and the increasing integration of roasted corn derivatives into industrial food processing. As consumers move away from deep-fried snacks toward better-for-you alternatives, the natural, nutrient-dense profile of roasted corn boasting high levels of vitamins and minerals has positioned it as a dominant player in the convenience food landscape. Furthermore, the rising demand for gluten-free ingredients in the bakery and beverage sectors, where roasted corn flour provides unique textural and flavor attributes, ensures sustained long-term growth across both mature and emerging markets.

Key Industry Highlights

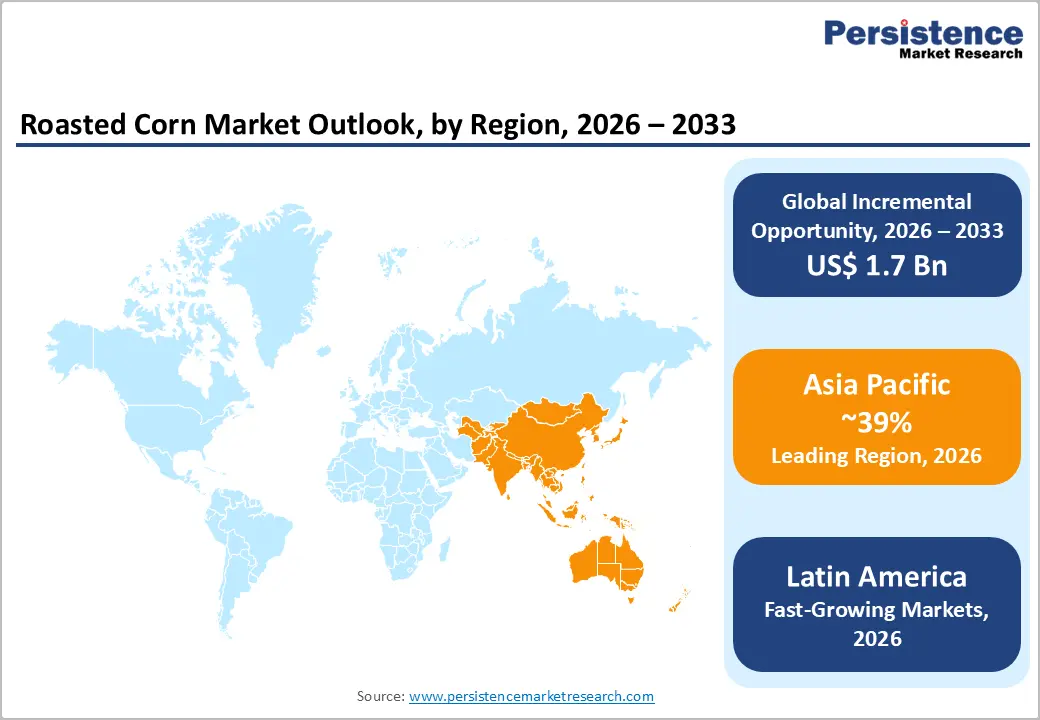

- Leading Regional Market: Asia Pacific holds the largest market share at 35%, driven by the high consumption of corn-based staples and a rapidly expanding middle class in China and India.

- Fastest Growing Region: Latin America is the fastest-growing region, fueled by rising disposable incomes and the increasing presence of multinational snack brands in countries like Brazil and Mexico.

- Dominant Product Form: Whole roasted corn accounts for 47% of the market share, preferred for its authentic street food appeal and perceived nutritional integrity.

- Fastest Growing Product Form: Flour is the fastest-growing segment, as its utility as a gluten-free and fiber-rich ingredient in the Bakery and Beverage industries expands globally.

- Primary Growth Opportunity: The shift toward Organic and Clean-Label snacks offers a high-value revenue pocket for brands targeting eco-conscious and health-oriented consumers.

| Key Insights | Details |

|---|---|

| Global Roasted Corn Market Size (2026E) | US$ 3.8 Bn |

| Market Value Forecast (2033F) | US$ 5.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Dynamics

Driver – Rising Demand for Gluten-Free and Non-GMO Flour Alternatives in Food Processing

The industrial application of roasted corn in the Bakery and Beverage sectors is witnessing a robust surge, primarily fueled by the accelerating diagnosis of celiac disease and gluten sensitivities. As indicated by research published in the Food Technology Magazine (IFT), manufacturers are increasingly replacing wheat-based fillers with roasted corn flour to achieve desirable crumb strength and moisture retention in baked goods. In the beverage industry, roasted corn derivatives are being explored as a base for traditional and innovative non-alcoholic drinks, leveraging their toasted flavor notes. The transition toward clean-label ingredients has made non-GMO roasted corn a preferred choice for companies aiming to meet stringent regulatory standards while satisfying consumer demand for transparency. This industrial utility provides a stable secondary demand pillar, insulating the market from seasonal fluctuations in retail snacking.

Restraints – Volatility in Raw Material Prices and Climate Impact on Corn Yields

The primary barrier to consistent growth in the market is the extreme sensitivity of corn production to global climatic conditions and supply chain disruptions. Corn is a staple crop whose yield is heavily influenced by weather patterns such as prolonged droughts or unseasonable rainfall in major producing regions like the United States, China, and Brazil. According to the International Grains Council (IGC), even minor fluctuations in annual harvest volumes can lead to significant price volatility in the commodities market. For manufacturers of roasted corn snacks and flours, these spikes in raw material costs can squeeze profit margins and force price hikes at the retail level. Furthermore, geopolitical tensions affecting the export of grains from regions like the Black Sea add layers of complexity to the supply chain, often resulting in localized shortages that hinder market expansion.

Opportunity – Expansion into the Organic and Clean-Label Retail Segments

The burgeoning demand for Organic food products represents one of the most significant revenue pockets for market participants. Consumers are increasingly willing to pay a premium for roasted corn that is certified free from synthetic pesticides and fertilizers. This trend is particularly strong in North America and Europe, where organic certification serves as a high-value trust signal. By pivoting toward organic farming partnerships and obtaining certifications like USDA Organic, companies can capture the high-margin health-retail segment. Furthermore, the Clean-Label movement offers opportunities to innovate with minimal seasoning and natural preservatives. High-growth segments like Flour the fastest-growing segment are well-positioned to benefit from this, as artisanal bakeries and health-food manufacturers seek out pure, high-quality roasted corn ingredients to differentiate their premium offerings in an increasingly competitive landscape.

Category-wise Analysis

Form Analysis

The Whole roasted corn segment currently leads the market, commanding a dominant share of 47% in 2025. This leadership is primarily attributed to the deep-rooted cultural affinity for whole-grain snacking and the popularity of roasted corn on the cob as a quintessential street food delicacy globally. Whole roasted corn is favored for its simplicity, authentic taste, and perceived naturalness, aligning with consumer preferences for minimally processed foods. In regions such as the United States and India, street vendors and festivals provide high-visibility sales channels that drive volume. However, the Flour segment is identified as the fastest-growing category through 2032. The justification for this rapid growth lies in the versatile industrial applications of roasted corn flour. From acting as a gluten-free binder in the Bakery sector to serving as a nutrient-dense thickening agent in the Beverage and baby-food industries, the utility of roasted corn in its powdered form is expanding far beyond traditional snacking.

End Use Analysis

The Snacks & Convenience Food segment is the leading end-use application for roasted corn, accounting for over 55% of the market share in 2025. This dominance is driven by the global snackification trend, where busy urban lifestyles have led to the replacement of traditional meals with frequent, portable snacking occasions. Roasted corn's high-fiber and gluten-free profile makes it a superior alternative to traditional salty snacks, sustaining its position as a household staple. Meanwhile, the Bakery and Beverage segments are witnessing significant growth, as roasted corn flour is increasingly utilized to enhance the texture and nutritional profile of cookies, pastries, and artisanal breads. The Animal Feed segment also represents a substantial portion of the market, as roasted corn is used in high-quality poultry and livestock feed to improve energy levels and digestibility. The justification for this broad utility is the high starch content and enhanced flavor developed during roasting, which makes corn a multi-functional ingredient across the entire food value chain.

Region-wise Insights

North America Roasted Corn Market Trends and Insights

North America remains a cornerstone of the global market, characterized by high-volume corn production and a deeply entrenched snacking culture. The United States leads the region, where the abundance of corn crops reaching record forecasts of over 423 million tons in the 2025/2026 marketing year as per the IGC provides a robust supply chain for the roasting industry. The market is bolstered by a highly sophisticated retail landscape and an innovation-centric ecosystem where companies like SunOpta Inc. and Del Monte Foods are pioneering organic and non-GMO product lines.

The regional dynamics are heavily influenced by the Vegan and Keto movements, which have increased the demand for whole-grain, plant-based proteins. Regulatory frameworks established by the Food and Drug Administration (FDA) regarding nutrient labeling have pushed manufacturers to highlight the fiber and mineral content of roasted corn snacks. Additionally, the rise of e-commerce has significantly boosted sales, with brands leveraging digital marketing to reach health-conscious Millennials. The U.S. market is also seeing a surge in artisanal and small-batch roasted corn products, catering to a growing consumer interest in provenance and traditional roasting techniques.

Asia Pacific Roasted Corn Market Trends and Insights

Asia Pacific is the leading regional market, holding a dominant 39% share in 2025. This leadership is the result of a massive consumer base in China and India, where corn has been a dietary staple for centuries. The region's growth is fueled by rapid urbanization, rising disposable incomes, and the world's largest middle class. In China, the healthification of the snack industry is a major driver, with consumers seeking high-quality, functional snacks that offer nutritional benefits beyond satiety.

The manufacturing advantages in Asia Pacific, combined with favorable government policies like India’s Make in India initiative, have encouraged the establishment of large-scale processing units by companies like Vaishnav Food Products and Nenimemi Foods. The regional market is also characterized by a high affinity for traditional street-food versions of roasted corn, which are being successfully transition into packaged, on-the-go formats. With population growth rates remaining steady such as India’s 0.89% annual increase as per Worldomete the volume of per-capita food consumption is set to escalate. The dominance of Supermarkets/Hypermarkets in the region provides high visibility for a variety of roasted corn forms, from whole snacks to flours and splits.

Market Competitive Landscape

The Roasted Corn Market exhibits a semi-consolidated structure, where a few global giants compete alongside a large number of regional and specialized players. Industry leaders such as Del Monte Food, Inc., SunOpta Inc., and H.J. Heinz maintain their dominance through vertical integration, ensuring a stable supply of high-quality corn and advanced processing capabilities. These companies focus on Consumer-Centric innovation, frequently launching new flavor profiles and packaging formats to stay ahead of shifting trends. Emerging business models are increasingly prioritizing Sustainability and Traceability, with brands like SunOpta releasing detailed sustainability reports to build consumer trust. The market is also seeing a rise in strategic alliances and acquisitions, such as Fresh Del Monte's recent successful bid to acquire select assets of Del Monte Foods Corporation in 2026, which aims to align fresh and shelf-stable strategies under a single integrated platform to enhance brand consistency and operational efficiency.

Companies Covered in Roasted Corn Market

- Del Monte Food, Inc.

- N. L. Food Industries

- Laxcorn

- Barberá Snacks SL

- Vaishnav Food Products

- Nenimemi Foods Pvt Ltd

- SunOpta Inc.

- H.J. Heinz Company Brands LLC

- AIM Biscuits

- Sergio

- Fresh Nuts GmbH

- Inka Crops, Inc.

- Brown Tree

- Vega Foods Corp. Private Limited

- Others

Frequently Asked Questions

The global market is expected to be valued at approximately US$ 3.8 billion in 2026, following a period of steady historical growth driven by health-conscious snacking trends.

Key growth drivers include the increasing consumer demand for Gluten-Free and fiber-rich snacks, the rising popularity of vegan diets, and the industrial utility of roasted corn in the bakery and beverage sectors.

Asia Pacific is the leading regional market, holding a dominant 39% share in 2025, primarily due to the large population bases and traditional affinity for corn in China and India.

The Organic segment is the fastest-growing nature category, as consumers prioritize pesticide-free and non-GMO ingredients in their nutritional intake.

Major companies include Del Monte Food, Inc., SunOpta Inc., H.J. Heinz Company, and specialized players like Barberá Snacks SL and Vaishnav Food Products.