- Animal Feed & Additives

- Corn Germ Meal Market

Corn Germ Meal Market Size, Share, and Growth Forecast, 2026 - 2033

Corn Germ Meal Market by Animal (Ruminants, Poultry, Swine, Catfish), Application (Fertilizers, Animal Feed, Others), Nature (Conventional, Natural), and Regional Analysis for 2026 - 2033

Corn Germ Meal Market Share and Trends Analysis

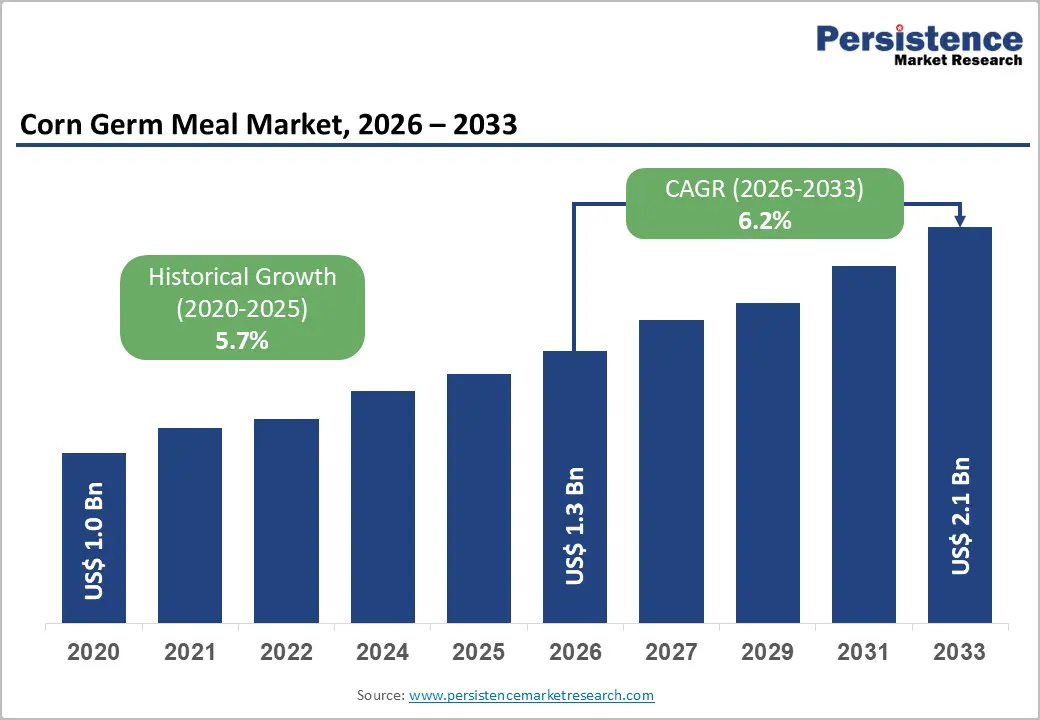

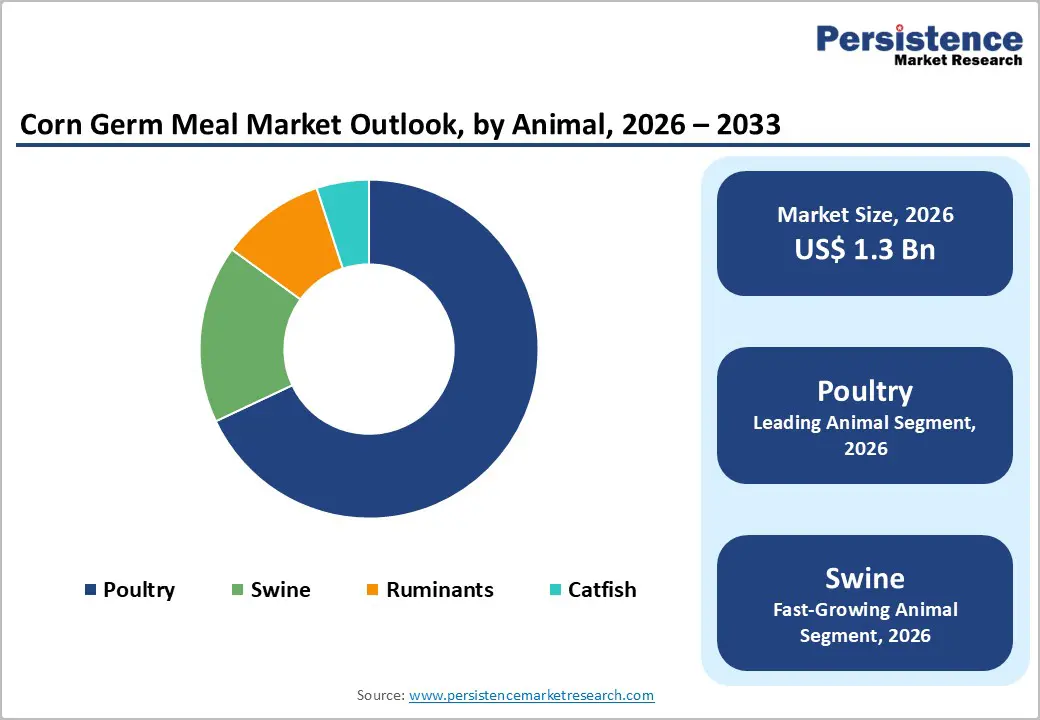

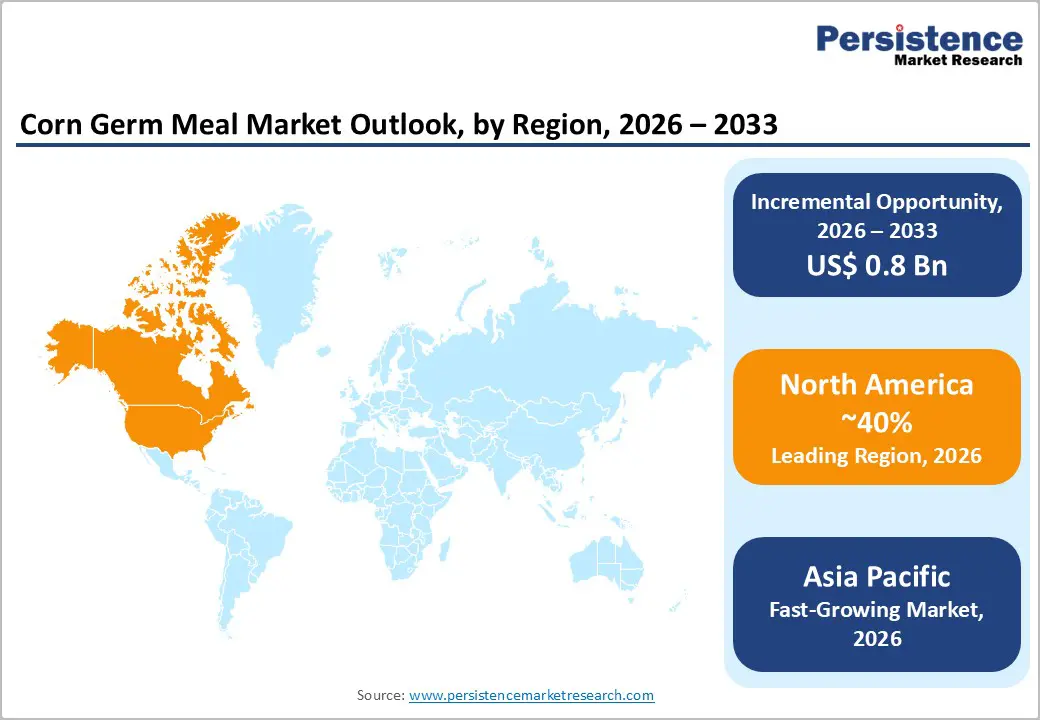

The global corn germ meal market size is likely to be valued at US$ 1.3 billion in 2026, and is projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 6.2% during the forecast period 2026 - 2033.

Heightened recognition of superior nutritional profiles in livestock feeds has propelled this trajectory, complemented by regulatory endorsements for natural additives and surging uptake of non-genetically modified organism (non-GMO) and organic feed components. Escalating raw material costs have prompted producers to adopt protein-dense, cost-effective supplements, particularly in poultry, swine, and ruminant operations across developing economies. The livestock sector's expansion in these economies has further amplified demand for sustainable protein sources, positioning corn germ meal as a versatile solution amid global supply pressures. The ingredient is being increasingly valued in the feed industry for its balanced amino acid content and digestibility, which enhance animal performance without compromising cost structures. Companies to develop blending strategies with legumes or by-products to optimize rations, while investing in traceability for premium certifications that command higher margins in export-oriented markets.

Key Industry Highlights

- Dominant Region: North America is expected to command about 40% market share in 2026, owing to substantial livestock populations and advanced feed manufacturing capabilities.

- Fastest-growing Market: Asia Pacific is poised to be the fastest-growing market through 2033 due to the rapid expansion of poultry, swine, cattle, and aquaculture industries across China, India, and Southeast Asia.

- Fastest-growing Animal: Swine is likely to be the fastest-growing segment during the 2026 - 2033 forecast period, as China deepens its focus on restoring domestic pork supply.

- Leading & Fastest-growing Applications: Animal feed is set to hold an estimated 68% revenue share in 2026, while fertilizers are expected to be the fastest-growing segment during the 2026 - 2033 forecast period.

- November 2025: IFF introduced OPTIMASH® BOOST, a next-generation cellulase, to maximize distillers’ corn oil recovery at ethanol plants by releasing oil from fiber and minimizing wet cake losses.

| Key Insights | Details |

|---|---|

| Corn Germ Meal Market Size (2026E) | US$ 1.3 Bn |

| Market Value Forecast (2033F) | US$ 2.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Consumer Preference for Natural and Organic Animal Products

Consumer preference for organic and naturally raised animal products is reshaping how producers think about feed formulation and sourcing strategies. In response, many livestock operators now prioritize certified organic and non-GMO inputs to align with retailer requirements and brand promises. Corn germ meal, when derived from identity-preserved corn and processed under audited systems, fits well into this evolving procurement strategy. It contributes meaningful nutritional value while also supporting marketing claims around animal welfare, sustainability, and transparency. This alignment strengthens the value proposition for brands that position their products on premium retail shelves or in export-oriented channels.

Regulatory frameworks such as the United States Department of Agriculture (USDA) National Organic Program (NOP) and the European Union (EU) Organic Regulation 2018/848 provide the structure that enables this shift in feed ingredients to translate into defensible market differentiation. Livestock producers and feed manufacturers that systemically embed these standards into their sourcing, documentation, and quality assurance gain access to higher-value customer segments and long-term supply contracts. For corn germ meal suppliers, investing in certification, traceability, and segregated logistics supports entry into these premium tiers and can improve margin resilience. From a strategic perspective, early movers that build credible organic and non-GMO portfolios are better positioned as retailers and food companies tighten specification requirements across their animal protein supply chains.

Price Volatility and Competition from Alternative Protein Sources

Corn germ meal operates in a highly competitive environment in which established protein sources already hold strong technical and commercial positions. Soybean meal remains the benchmark ingredient in many formulations because nutritionists and integrators are familiar with its performance profile, pricing behavior, and global availability. Its higher protein content and well-developed international logistics networks make it a natural first choice when formulating for consistency and least-cost optimization. Corn germ meal must be positioned carefully, with a clear understanding of where it adds value in specific diets rather than as a direct, one-for-one replacement. Feed manufacturers that treat corn germ meal as a complementary component within broader ration strategies are better able to manage this competitive dynamic.

Increasingly affecting this feed ingredient are the broader structural changes in the feed protein landscape. Its economics remain sensitive to movements in grain markets, so procurement teams need to manage this exposure through diversified sourcing, flexible formulation approaches, and regular scenario planning. The emergence of newer protein sources such as insect meal, single-cell proteins, and algae-based ingredients introduces another strategic consideration, particularly as large feed groups and integrators evaluate these options for sustainability and brand positioning benefits. Suppliers of corn germ meal benefit from refining their value proposition around reliability, nutritional consistency, and compatibility with existing milling systems, while also tracking how customer preferences and corporate sustainability commitments influence inclusion decisions over time.

Development of Specialty and Functional Feed Ingredients

Advanced processing technologies are reshaping how corn germ meal fits into the evolving market for specialty and functional feed ingredients. By using approaches such as fermentation, enzymatic treatment, and protein concentration, producers can shift corn germ meal from a conventional byproduct to a more differentiated, higher-value component in feed formulations. These methods can enhance nutrient density, improve amino acid availability, and support better digestibility, which are key priorities for nutritionists who need to deliver measurable performance outcomes in livestock and companion animals. From a strategic perspective, this shift creates an opportunity to move away from purely cost-based competition and toward solutions that reinforce narratives around productivity, animal health, and sustainability.

The broader market for specialty feed ingredients increasingly values functionality, traceability, and alignment with brand positioning in segments such as organic poultry feed, natural pet nutrition, and high-performance livestock diets. Companies that invest in upgrading corn germ meal through dedicated processing lines, robust quality assurance systems, and application-focused product development can create a differentiated portfolio that appeals to integrators and premium feed manufacturers. This approach strengthens their ability to meet more demanding specifications and supports stronger commercial relations.

Category-wise Analysis

Animal Insights

Poultry is slated to maintain a dominant position in 2026, with an estimated 48% of the corn germ meal market revenue share. This dominance reflects the scale and integration of the global poultry industry, where corn germ meal has become a familiar and trusted component in many feeding programs. Poultry nutritionists have validated its use in both broiler and layer diets, confirming that it can support energy and protein requirements while maintaining growth, feed efficiency, and egg production performance. When used within well-designed formulation limits, it helps reduce overall ration cost and enables more flexible ingredient strategies. As producers face margin pressure and look for resilient feed options, corn germ meal provides a practical way to optimize diets without undermining productive outcomes.

Swine is likely to be the fastest-growing segment over the 2026 - 2033 forecast period. This acceleration reflects the rebound of swine industries across Asia as producers rebuild herds and bring production back toward pre-disruption levels. China in particular has focused on restoring domestic pork supply, which has increased demand for flexible and cost-effective feed ingredients in commercial operations. In this context, corn germ meal benefits from a favorable combination of palatability, digestibility, and price competitiveness that aligns well with modern nutrition programs. When nutritionists incorporate it at appropriate levels in grower and finisher diets, it supports efficient weight gain, consistent feed conversion, and stronger overall profitability for integrated production systems.

Application Insights

Animal feed is predicted to hold the highest revenue share, estimated to reach 68% in 2026. This segment’s leadership position reflects corn germ meal’s established role as a cost-effective protein and energy source across a broad range of livestock species, including poultry, swine, cattle, and aquaculture. Its nutritional profile, which combines meaningful protein levels, useful crude fiber content, and a balanced amino acid pattern, makes it well suited to modern compound feed formulations. Nutritionists typically position it as a complementary ingredient alongside primary proteins such as soybean meal, using it to fine-tune energy density, enhance ration economics, and increase flexibility in ingredient sourcing without compromising core performance objectives.

Fertilizers are expected to be the fastest-growing segment from 2026 to 2033 due to the increasing focus on organic farming systems, soil health regeneration, and more sustainable nutrient management practices across the agriculture sector. Corn germ meal is now widely viewed as a useful organic fertilizer and soil amendment that aligns well with these priorities. It offers a gradual nutrient release pattern that supports steady plant development rather than sharp fluctuations, while also contributing meaningful amounts of phosphorus, potassium, and other beneficial constituents. In addition, its organic matter helps improve soil structure, stimulates microbial activity, and supports better moisture-holding capacity, which are critical for resilient, high-performing cropping systems.

Nature Insights

The conventional segment is projected to capture approximately 82% market share in 2026, supported by widespread livestock systems and mature supply networks spanning crop farming, milling, and delivery. Conventional corn germ meal has leveraged extensive corn planting, robust processing infrastructure, and competitive pricing that matches commercial feed economics. Major producers in the Americas and Asia have chosen it for superior affordability, steady quality, and constant supply. Integrated farms have adopted it as the standard choice, reserving premium options for programs demanding specific eco-credentials or approvals.

The organic segment is expected to achieve the fastest growth between 2026 and 2033, propelled by rigorous oversight across production stages that elevates premiums. Certification protocols, segregated handling, and exclusive facilities have constrained supply while justifying higher returns. European buyers have driven this surge through stringent farming regulations and robust demand from retailers for verified feeds in organic meats, dairy, and eggs. Forward-thinking suppliers should invest in traceability tech and regional alliances to scale organic output, capturing value in wellness-aligned channels where differentiation commands loyalty.

Regional Insights

North America Corn Germ Meal Market Trends

North America is set to command a significant portion of the corn germ meal market share at approximately 40% in 2026, underpinned by a highly developed corn processing base, substantial livestock populations, and advanced feed manufacturing capabilities. The United States anchors this ecosystem through extensive wet-milling and dry-milling industries that generate consistent germ streams, which feed manufacturers convert into standardized meal inputs for commercial diets. Strong integration between processors and feed companies supports stable offtake, predictable product specifications, and reliable logistics into key poultry, swine, and cattle production areas. This alignment enables corn germ meal to operate as a mainstream ingredient in many commercial rations rather than remaining a marginal byproduct.

Growth in the region is increasingly driven by strategic shifts rather than simple volume expansion. Producers and feed manufacturers are placing greater emphasis on sustainability, byproduct valorization, and supply chain resilience, which strengthens the strategic rationale for incorporating corn germ meal into broader nutrient utilization strategies. Regulatory oversight by institutions such as the Food and Drug Administration (FDA) and the Association of American Feed Control Officials (AAFCO) reinforces market confidence by providing clear definitions, safety standards, and labeling requirements.

Europe Corn Germ Meal Market Trends

Europe plays a pivotal role in the corn germ meal market, supported by mature livestock sectors and a strong policy and consumer focus on sustainable feed ingredients. Demand concentrates in countries such as Germany, France, Spain, and the United Kingdom, where intensive poultry, swine, and ruminant production systems require reliable, traceable protein and energy sources. Germany’s advanced animal nutrition industry and Spain’s intensive livestock clusters use corn germ meal in compound feeds to balance cost, nutritional performance, and sustainability requirements. The region’s strong preference for organic and non-GMO products, combined with strict standards on animal welfare and feed safety, further shapes how corn germ meal is specified and sourced.

Europe provides a supportive yet demanding environment for corn germ meal suppliers. Frameworks such as the European Commission (EC)’s Farm to Fork Strategy and the Green Deal promote greater use of byproduct-derived feed ingredients that help reduce waste and enhance resource efficiency. Instruments including the EU Feed Materials Register and strict traceability requirements drive robust quality management systems across the supply chain, which can serve as a key differentiator for well-organized processors. For market participants, the priority is to invest in non-GMO and organic lines, enhance processing technologies to raise nutritional value, and position offerings to align with retailer and processor sustainability commitments.

Asia Pacific Corn Germ Meal Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for corn germ meal through 2033. Regional market growth is underpinned by rapid expansion of poultry, swine, cattle, and aquaculture industries across China, India, and Southeast Asia. Rising incomes and urbanization are reshaping dietary patterns, with a clear shift toward higher animal protein consumption that, in turn, drives structural demand for formulated feeds and reliable protein-energy ingredients. Policy priorities in key markets increasingly emphasize domestic feed manufacturing capacity, upgraded on-farm nutrition practices, and reduced reliance on imported inputs, creating a favorable environment for wider inclusion of corn germ meal in commercial rations. Programs that focus on agricultural modernization and animal husbandry development are also pushing producers toward more consistent and performance-oriented feeding systems where byproduct-based ingredients can be systematically integrated.

The region’s competitive manufacturing advantages strengthen the strategic case for corn germ meal adoption. Expanding corn processing capacity, relatively competitive operating costs, and geographic proximity between milling assets and livestock clusters support efficient supply and attractive delivered economics for feed manufacturers. At the same time, the market still contends with fragmented distribution channels, variable quality assurance capabilities, and uneven technical knowledge among smaller producers, which can limit optimal utilization without targeted support. This combination of capacity build-out, education, and localization positions both regional and multinational players to capture long-term growth in a market that is steadily moving toward higher feed sophistication.

Competitive Landscape

The global corn germ meal market structure exhibits moderate fragmentation, where leading companies such as Cargill Incorporated, Archer Daniels Midland Company, Ingredion Incorporated, and Tate & Lyle plc have secured dominant positions through superior operational strengths. Competitive advantages have hinged on expansive processing capacities, unwavering product standards, and comprehensive certifications including organic, non-GMO, kosher, and halal designations, alongside extensive distribution reach. Vertically integrated firms controlling corn milling and feed production have captured extra margins while directing pricing strategies, recipe choices, and client ties more effectively.

Cost leadership has proven vital, as corn germ meal has vied against entrenched protein sources in a price-sensitive arena. Efficient plants and optimized transport have underpinned profitability amid commodity pressures. Supply chain architects should pursue integration and certification expansions to fortify resilience, blending scale with premium credentials to outpace rivals and align with rising demands for verified, sustainable feeds in evolving livestock sectors.

Key Industry Developments

- In August 2025, Regreen-Excel EPC India Limited commissioned a corn oil extraction unit at Seas Biotech's ethanol plant in Assam, recovering oil from thin stillage to boost revenue, improve distillers’ dried grains with solubles (DDGS) feed quality, and support biodiesel production. This enhances plant efficiency and sustainability, building on prior EPC successes in grain ethanol and biomass power.

- In May 2025, Canadian Food Inspection Agency (CFIA) approved wet corn germ as a new single ingredient feed (SIF) under class 2.2 (energy feeds), a high-moisture (50-55%) wet milling by-product for livestock energy, requiring timely use within 1 week and guarantees for fat, protein, fiber, and moisture.

- In March 2025, Cargill inaugurated a new corn milling plant in Gwalior, Madhya Pradesh, in partnership with Saatvik Agro Processors, to produce starch derivatives for India’s fast-growing confectionery, dairy, and infant formula sectors, which together are worth about US$ 15 billion and growing at 6-11% annually.

Companies Covered in Corn Germ Meal Market

- Cargill, Incorporated

- Archer Daniels Midland Company (ADM)

- Ingredion Incorporated

- Tate & Lyle PLC

- Bunge Limited

- Roquette Frères

- Grain Processing Corporation

- AGRANA Beteiligungs-AG

- Global Bio-chem Technology Group

- China Corn Oil Company

- Tereos Group

- Gulshan Polyols Ltd

- Sayaji Industries Limited

- Wilmar International Limited

- Associated British Foods PLC

Frequently Asked Questions

The global corn germ meal market is projected to reach US$1.3 billion in 2026.

Rising global demand for cost-effective, protein-rich animal feed and sustainable use of corn processing byproducts drives the market.

The market is poised to witness a CAGR of 6.2% from 2026 to 2033.

Key opportunities lie in the expanding use of corn germ meal in aquaculture and livestock feed in emerging markets, plus new applications in biofuels and functional foods.

Cargill, Incorporated, Archer Daniels Midland Company, Ingredion Incorporated, and Tate & Lyle PLC are some of the key players in the market.