- Food Ingredients & Additives

- Cornmeal Market

Cornmeal Market Size, Share, and Growth Forecast, 2026 - 2033

Cornmeal Market by Product Type (White Cornmeal, Yellow Cornmeal, Red and Blue Cornmeal), Category (Organic, Conventional), Applications (Food & Beverage, Animal Feed, Industrial Ethanol, Bio-based Plastics), and Regional Analysis 2026 - 2033

Cornmeal Market Size and Trends Analysis

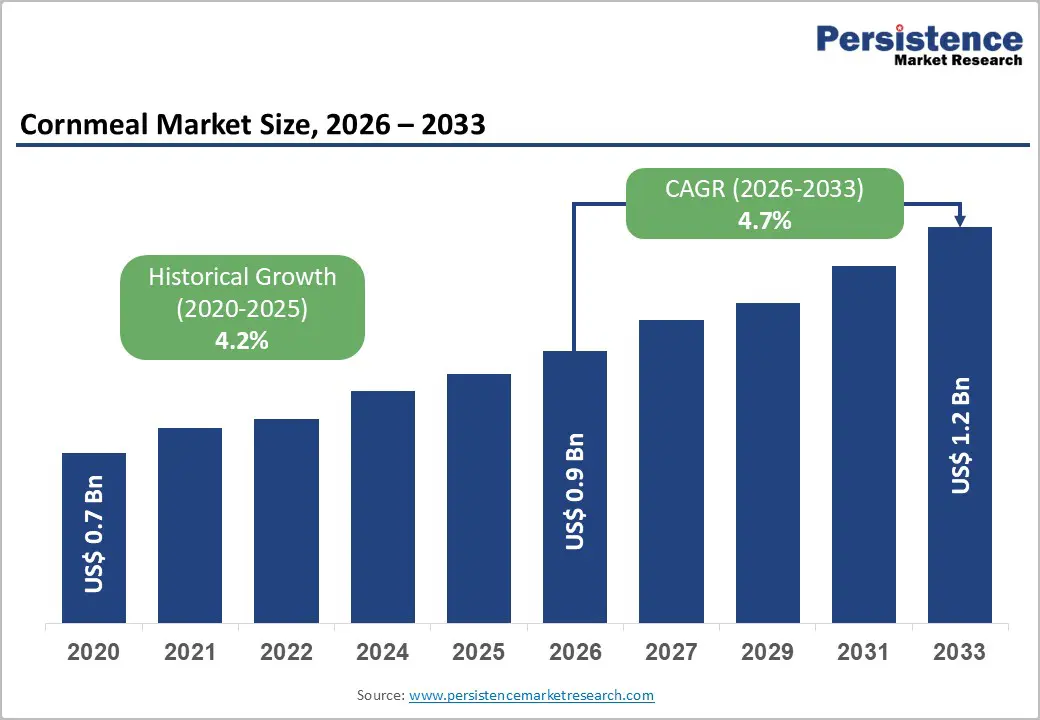

The global cornmeal market size is likely to be valued at US$0.9 billion in 2026 and is expected to reach US$1.2 billion by 2033, growing at a CAGR of 4.7% during the forecast period from 2026 to 2033, driven by increasing consumer awareness of gluten-free dietary needs, which continues to drive demand across various food processing sectors.

Rising demand for versatile, grain-based ingredients is further contributing to market expansion across both food and industrial applications. Advancements in milling technologies are also improving processing efficiency and enabling higher yields from a wide range of corn varieties. Innovations in dry milling processes are also expected to enhance the nutritional value of specialty grain products. Shifting procurement trends toward nutrient-rich specialty grains reflect evolving consumer preferences, reinforcing market growth. Overall, the cornmeal market is well-positioned to benefit from the continued expansion of the global snack food industry.

Key Industry Highlights:

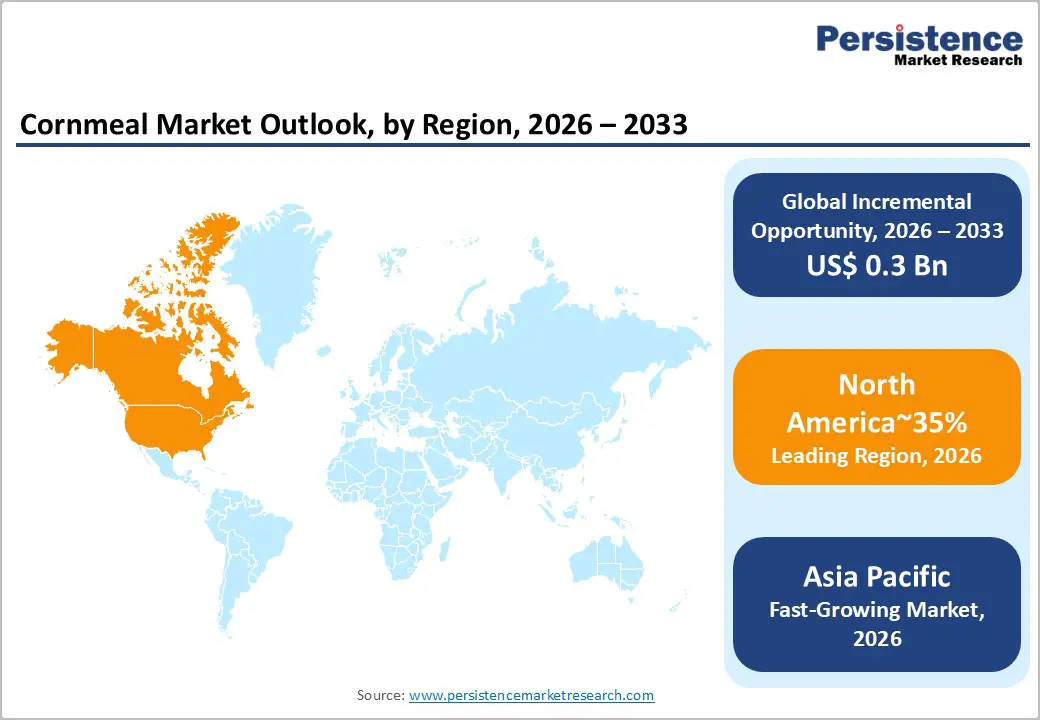

- Leading Region: North America is projected to lead, accounting for approximately 35% share in 2026, supported by high snack consumption and established milling infrastructure.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest, driven by rapid urbanization and increasing demand for processed foods in India and China.

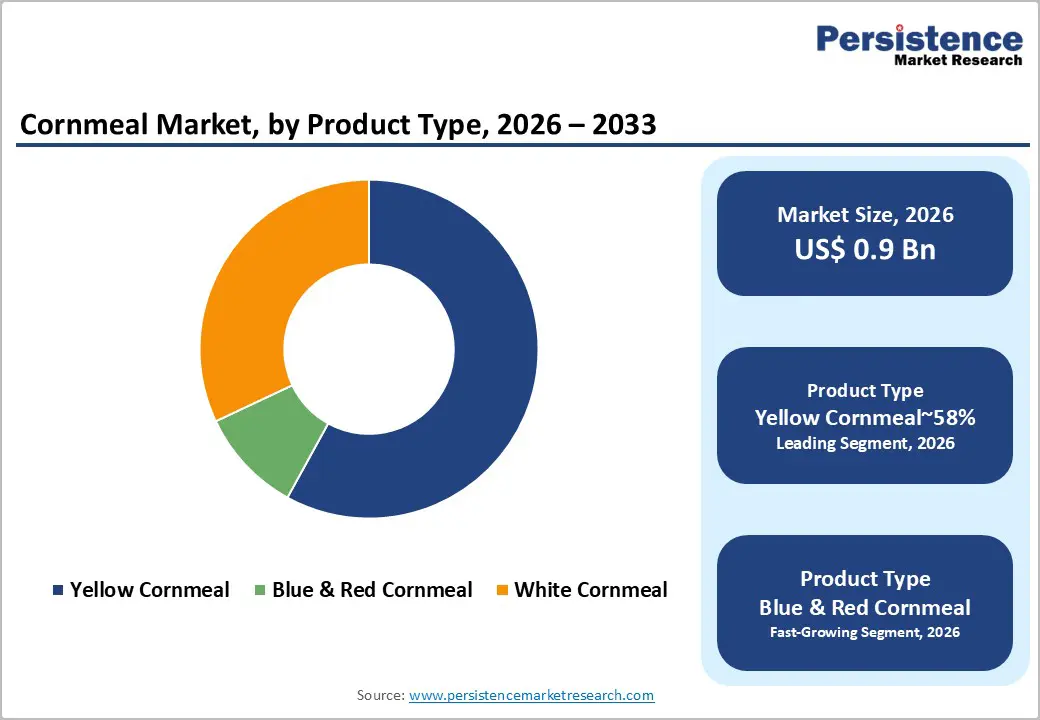

- Leading Product Type: Yellow cornmeal is expected to lead, accounting for approximately 58% share in 2026, anchored by its widespread application in the bakery and snack segments.

- Leading Applications: The food & beverage segment is projected to dominate, holding approximately 47% share in 2026, driven by rising demand for corn-based staples and convenience foods.

| Key Insights | Details |

|---|---|

| Cornmeal Market Size (2026E) | US$0.9 Bn |

| Market Value Forecast (2033F) | US$1.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

DRO Analysis

Driver Analysis - Escalating Demand for Gluten-Free Staple Alternatives

The structural transition toward gluten-free nutrition drives integration of corn-based ingredients across mainstream food manufacturing portfolios. Rising celiac awareness and broader health consciousness expand demand for non-wheat flour alternatives globally. Industrial baking and confectionery segments increase procurement volumes to meet evolving dietary requirements and labeling standards. Manufacturers adapt processing lines to eliminate cross-contamination risks within gluten-free production environments. Regulatory emphasis on clean-label certification influences sourcing strategies and supplier selection criteria. Cost structures adjust toward segregated production, traceability systems, and quality assurance investments. These dynamics collectively sustain long-term demand growth for corn-derived staple ingredients within global food systems.

Bob's Red Mill’s Medium Grind Cornmeal aligns with clean-label expectations through minimally processed, stone-ground product formulations. Nutritional retention of natural fiber components strengthens product appeal among health-conscious consumer segments. Distribution strategies emphasize transparency and ingredient integrity within competitive retail environments. Manufacturers integrate such inputs to meet strict gluten-free certification and labeling requirements. Product positioning supports consistent demand across both household and industrial consumption channels. These factors reinforce sustained adoption of corn-based alternatives within evolving gluten-free dietary ecosystems.

Rising Utilization in Industrial Bio-based Applications

Technological advancements are expanding applications of corn-derived materials across ethanol and bioplastic manufacturing ecosystems. Regulatory mandates for renewable fuel blending sustain demand for industrial-grade corn inputs within energy markets. This industrial uptake diversifies revenue streams for milling operators beyond conventional food-oriented applications. The development of biodegradable packaging introduces new demand cycles for corn-based starch derivatives across industries. Sustainability regulations accelerate the substitution of petroleum-based polymers with renewable, plant-derived material alternatives. Cost structures evolve toward specialized processing infrastructure supporting multi-application output streams. These dynamics collectively strengthen the structural resilience of corn-based inputs within industrial and energy value chains.

Cargill’s Soluble Corn Fiber highlights multifunctional applications spanning both industrial material science and nutritional ingredient domains. Material versatility enables manufacturers to reduce reliance on petroleum-derived polymers in packaging systems. Processing innovation supports scalability and consistency across diverse industrial use cases requiring performance reliability. Enterprises increasingly prioritize such inputs to align procurement with sustainability and regulatory compliance objectives. Investment flows target advanced corn processing capabilities to support diversified end-use demand. These interdependencies reinforce long-term expansion of bio-based industrial applications within global markets.

Restraint Analysis - Volatility in Global Grain Procurement Costs

Fluctuating raw corn prices create structural instability for downstream cornmeal processing and distribution networks globally. Climate variability and geopolitical disruptions frequently destabilize agricultural supply chains, impacting consistent grain availability. These external pressures complicate long-term pricing strategies for millers operating within competitive, margin-constrained environments. Elevated input costs translate into higher retail pricing, affecting demand elasticity across food and industrial segments. Procurement uncertainty increases reliance on dynamic sourcing strategies and short-term contracting mechanisms. Regulatory scrutiny on food pricing further limits cost pass-through flexibility within consumer markets. These factors collectively constrain profitability and operational predictability within the cornmeal value chain.

Bunge’s blockchain-enabled traceability initiatives improve supply chain transparency by integrating digital tracking systems across sourcing networks. This enhances procurement reliability and helps minimize inefficiencies associated with fragmented supplier bases. However, the high cost of implementation poses challenges for smaller regional processors with limited financial resources. As a result, technological gaps are widening, favoring larger players with stronger digital capabilities and capital backing. Ongoing investments in traceability also support compliance with evolving regulatory and sustainability standards, contributing to gradual consolidation within the corn processing industry.

Processing Cost Pressures in Cornmeal Production

Energy-intensive grinding operations significantly elevate production expenses under volatile electricity and fuel pricing conditions globally. Smaller milling units lack scale efficiencies, limiting their ability to absorb cost fluctuations effectively. Equipment maintenance requirements further increase operational overheads, impacting long-term cost stability across facilities. These combined pressures compress profit margins within conventional cornmeal production environments. Procurement strategies become increasingly constrained as input and processing costs rise simultaneously. Regulatory compliance related to energy usage adds further complexity to operational cost management frameworks. These dynamics collectively restrict scalability and profitability across fragmented milling industry structures.

Manufacturers respond by passing increased expenses to end-users, which dampens overall demand elasticity. Operational strategies prioritize efficiency upgrades and process optimization to mitigate margin erosion. Capital allocation shifts toward modernizing equipment and reducing energy consumption intensity. Competitive positioning increasingly depends on the ability to manage cost structures effectively. These constraints limit broad-based production expansion across conventional cornmeal processing segments.

Opportunity Analysis - Expansion of Organic and Premium Specialty Grains

Rising consumer willingness to pay premiums for organic grains drives demand across specialty cornmeal segments globally. Distinct variants such as blue and red cornmeal gain traction through differentiated nutritional and visual attributes. This premiumization supports higher margin realization for millers focusing on niche agricultural varieties. Organic farming integration attracts environmentally conscious consumers concentrated within developed urban retail ecosystems. Regulatory emphasis on clean-label and non-GMO certifications strengthens demand for traceable grain sourcing practices. Cost structures evolve toward segregated processing and certified supply chain management systems. These dynamics collectively sustain the growth of high-value specialty grain markets.

Bob's Red Mill’s Organic Cornmeal aligns with demand for pesticide-free, minimally processed pantry staples within health-focused retail channels. Dedicated organic processing facilities enable compliance with certification standards and maintain product integrity. Brand positioning emphasizes transparency and nutritional quality, reinforcing consumer trust and repeat purchasing behavior. Specialty grain portfolios support innovation across artisanal bakery and gourmet food applications. Distribution networks increasingly prioritize premium shelf placements, reflecting higher value perception. These interdependencies reinforce sustained demand for organic and specialty cornmeal products across evolving consumer segments.

Functional Food Formulations in Cornmeal Applications

Fortification trends integrate cornmeal into nutrient-enhanced ready meals and snack formulations across urban consumption markets. Precision milling technologies enable the incorporation of vitamins and micronutrients without compromising texture or product consistency. This capability supports the development of functional foods aligned with convenience-driven dietary preferences among working populations. Regulatory frameworks governing nutritional claims reinforce the adoption of fortified ingredients within packaged food categories. Cost structures evolve toward advanced milling processes and controlled nutrient blending systems within production lines. Product innovation expands across meal kits, bakery mixes, and ready-to-eat formats, leveraging fortified grain bases. These dynamics collectively broaden application scope and sustain demand for functional cornmeal formulations.

King Arthur Baking Company’s Fortified Cornmeal Blend demonstrates formulation stability supporting consistent nutrient integration within baking and prepared food applications. Manufacturers collaborate with meal kit platforms to deliver co-branded, nutrition-focused product offerings. Blended formulations enhance the value proposition through improved dietary profiles without altering sensory characteristics. Processing capabilities ensure uniform nutrient dispersion across large-scale production batches. Retail and digital channels increasingly promote fortified grain products targeting health-conscious consumer segments. These interdependencies reinforce accelerated uptake of functional cornmeal across diversified food ecosystems.

Category-wise Analysis

Product Type Insights

Yellow cornmeal is expected to lead, accounting for approximately 58% share in 2026, underpinned by its extensive utilization in the global bakery and snack industries. High carotenoid content and a distinct flavor profile make this variant the preferred choice for producing traditional cornbreads and extruded snacks. Adoption remains anchored in the availability of large-scale milling infrastructure dedicated to yellow maize processing. Enterprises prioritize this product type to ensure consistency in color and texture across high-volume food production lines. Gruma with Maseca remains a dominant force in this segment by providing high-quality yellow corn flour to international retail markets. Ongoing enhancements in dry-milling technology further strengthen the yield and quality of yellow cornmeal for industrial applications. This convergence of functional versatility and established consumer preference sustains the segment's leadership within the global starch market.

Blue & red specialty grains are anticipated to be the fastest-growing segment, driven by increasing consumer demand for nutritionally dense and visually distinct food ingredients. Rising awareness regarding the antioxidant properties of anthocyanins found in colored corn is accelerating procurement within the premium health food sector. Bob's Red Mill’s Medium Grind Cornmeal variants in specialty colors address the emerging need for artisanal baking components. This transition toward specialty grains reflects a broader shift in consumer behavior toward functional and experiential nutrition. Integration of unique corn varieties into gourmet culinary applications is expected to expand the segment's reach across high-end food service channels. As manufacturers prioritize product differentiation and nutritional enhancement, specialty cornmeal is gaining traction across diverse regional ecosystems. This trend reinforces the expansion of the addressable market for non-traditional corn varieties globally.

Applications Insights

The food & beverage segment is expected to lead, accounting for approximately 47% share in 2026, supported by the rising consumption of corn-based staples and convenience foods globally. The segment's dominance is anchored in the versatility of cornmeal as a thickening agent, coating, and primary ingredient in traditional dishes. Gruma with Maseca exemplifies the industrial scale required to meet the high demand for tortilla and snack production. Enterprises prioritize cornmeal for its gluten-free properties, which align with contemporary health and wellness trends. Ongoing innovation in ready-to-eat meal formats and breakfast cereals further reinforces the utilization intensity of cornmeal in this sector. This convergence of cultural significance, nutritional value, and industrial functionality sustains the leadership of the food and beverage application segment.

Bio-based plastics are forecast to be the fastest-growing segment, driven by global initiatives to reduce carbon emissions and plastic waste. Cornmeal serves as a vital feedstock for fermentation processes in the production of renewable biofuels and biodegradable polymers. Bunge with Justoken supports this transition by ensuring that corn-based feedstocks are sourced through transparent and sustainable supply chains. This shift toward bio-based alternatives is projected to benefit from government mandates for higher ethanol blending in transportation fuels. Integration of corn-derived starch into the manufacturing of compostable packaging is expected to address the growing demand for eco-friendly consumer goods. As industries prioritize decarbonization and circular economy principles, the demand for industrial-grade cornmeal is gaining significant momentum. This trend is likely to expand the application scope of corn-based products beyond the traditional food value chain.

Regional Insights

North America Cornmeal Market Trends

North America is expected to remain the leading regional market, accounting for approximately 35% share in 2026, supported by an advanced food manufacturing ecosystem and a strong cultural affinity for corn-based products. The region's market structure is anchored in large-scale industrial milling operations that supply diverse sectors, including snacks, bakery, and animal feed. Adoption remains driven by the high penetration of gluten-free dietary trends and the expansion of the ready-to-eat meal category. Furthermore, the presence of major agribusiness leaders ensures a consistent supply of both conventional and organic cornmeal variants.

The U.S. is expected to anchor regional momentum through sustained investments in automated milling technologies and a robust demand for clean-label food products. Government policies supporting the production of corn-based ethanol continue to drive significant volumes in the industrial application segment. ADM’s Hubbard Feeds is expected to benefit from the growing concentration of professional livestock management operations across the Midwest. Regulatory focus on food safety and traceability is projected to increase the adoption of digital supply chain solutions among major vendors.

Asia Pacific Cornmeal Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as rapid urbanization and shifting consumer dietary patterns accelerate market expansion across diverse demographics. The region is experiencing a structural transition toward processed and convenient food formats, significantly increasing the demand for corn-derived ingredients. This momentum is supported by the expansion of organized retail and the growing popularity of corn-based snacks among younger populations. Policy initiatives aimed at improving food security and local manufacturing capacity are further reinforcing the market's growth potential.

India is expected to serve as a primary growth engine due to the increasing demand for healthy, gluten-free breakfast alternatives and snack options. The rising domestic production of maize is anticipated to provide a stable raw material base for local milling enterprises. Cargill’s Soluble Corn Fiber is set to capitalize on the country's expanding functional food sector as consumers prioritize gut health and wellness. Investments in cold chain logistics and modern processing facilities are projected to enhance the distribution of premium cornmeal products.

Europe Cornmeal Market Trends

Europe is expected to remain a mature and structurally stable regional market, with demand primarily anchored in premiumization and strict regulatory compliance. The market is characterized by a high demand for non-GMO and organic cornmeal variants, reflecting a deeply ingrained consumer preference for natural food products. Adoption remains focused on high-quality bakery applications and specialized industrial uses, such as gluten-free beer production. The region's focus on sustainability is also driving the utilization of cornmeal in bio-based packaging solutions.

The Netherlands is anticipated to act as a critical hub for European cornmeal trade and processing, supported by its strategic port infrastructure and advanced food science sector. Cargill, with EverSweet, demonstrates the region's focus on integrating innovative sweeteners and fibers into corn-based product formulations. Strict EU labeling regulations regarding genetically modified grains are expected to sustain the demand for verified non-GMO supply chains. Regional manufacturers are likely to prioritize the procurement of specialty grains to meet the needs of the artisanal food market.

Competitive Landscape

The global cornmeal market is moderately consolidated, with leadership concentrated among agribusiness firms such as Archer Daniels Midland and Cargill alongside regional millers. These entities exert influence through integrated milling operations, global sourcing networks, and established relationships with food processors. Their capabilities set benchmarks for yield efficiency, safety compliance, and large-scale supply reliability across applications. Strong procurement linkages and logistics infrastructure reinforce their dominance in commodity-sensitive value chains. This structure balances global standardization with localized specialization in niche and organic product segments.

Competitive positioning reflects vertical integration for high-volume production alongside horizontal differentiation in specialty and organic cornmeal offerings. Premium participants emphasize stone-ground processing, certification standards, and fortified variants targeting health-conscious consumers. Companies such as Bob's Red Mill and Gruma advance differentiated portfolios addressing premium and regional demand patterns. Value-oriented players focus on operational efficiency and bulk supply for industrial and food manufacturing applications. Platform evolution increasingly integrates digital traceability and bio-based applications aligned with sustainability and industrial demand trends.

Key Industry Developments:

- In March 2026, Cargill was awarded the BIG Artificial Intelligence Excellence Award for its predictive supply chain analytics. The use of AI to predict crop yields and optimize milling schedules allows Cargill to maintain more stable pricing and inventory levels compared to competitors relying on traditional forecasting.

- In March 2026, Mittal Cornezza integrated blockchain technology for end-to-end traceability in its corn grits supply chain. This move allows international B2B buyers to verify non-GMO and organic status in real-time, reducing fraud risks by 30-40% and setting a new transparency standard for Indian corn exports.

- In September 2025, ADM and Alltech announced an agreement to form a North American animal feed joint venture. By contributing 28 combined mills, the partners aim to align their nutrition science expertise and manufacturing scale, specifically strengthening the animal nutrition segment of the corn-processing value chain.

Companies Covered in Cornmeal Market

- Archer-Daniels-Midland (ADM)

- Cargill

- Bunge

- Ingredion

- Gruma (Maseca)

- Associated British Foods

- General Mills

- COFCO Corporation

- POET LLC

- LifeLine Foods

- Semo Milling

- Bob's Red Mill Natural Foods

- The Hain Celestial Group

- Nature's Path

- King Arthur Baking Company

- Arrowhead Mills

Frequently Asked Questions

The global cornmeal market is projected to be valued at US$0.9 billion in 2026 and is expected to reach US$1.2 billion by 2033, driven by rising demand for gluten-free food ingredients and expanding applications across food processing and industrial sectors.

The increasing prevalence of celiac disease and broader health-conscious consumption patterns are accelerating the shift toward gluten-free alternatives, positioning cornmeal as a critical substitute for wheat-based ingredients across bakery, snack, and processed food manufacturing ecosystems.

The cornmeal market is forecast to grow at a CAGR of 4.7% from 2026 to 2033, reflecting stable demand expansion across food, feed, and emerging bio-based industrial applications.

North America is the leading regional market, accounting for approximately 35% share, supported by high consumption of corn-based foods, advanced milling infrastructure, and strong presence of integrated agribusiness supply chains.

The cornmeal market is moderately consolidated, with key players including Cargill, Archer Daniels Midland, Bunge, Ingredion, and Gruma, competing through global sourcing networks, processing scale, and product diversification.