- Construction & Engineering

- Construction Equipment Market

Construction Equipment Market Size, Trends, Share, and Growth Forecast for 2025 - 2032

Construction Equipment Market By Equipment Type (Earthmoving Equipment, Material Handling Equipment, Concrete and Road Construction Equipment, Other Construction Equipment), Propulsion Type (Diesel, Electric, Hybrid, CNG/LNG), End-user (Residential Construction, Commercial & Industrial Construction, Infrastructure, Misc.), and Regional Analysis for 2025 - 2032

Construction Equipment Market Size and Trends Analysis

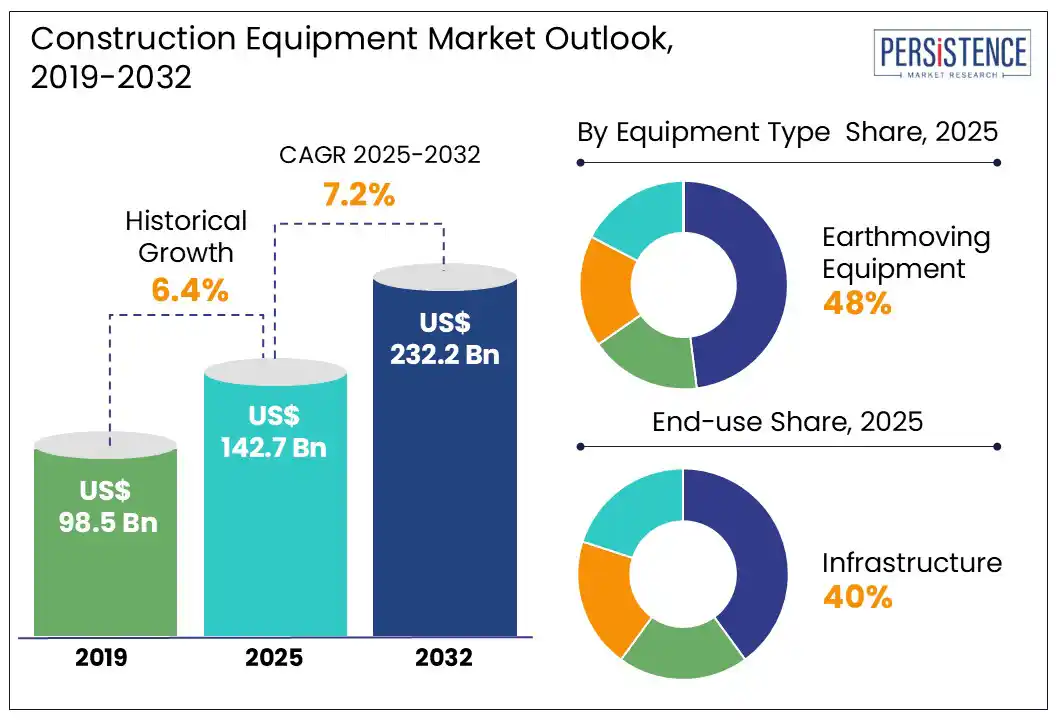

The global construction equipment market size is likely to be valued at US$ 142.7 Bn in 2025 and is expected to reach US$ 232.2 Bn at a CAGR of 7.2% during the forecast period from 2025 to 2032.

Manufacturers are focusing on electrification, automation, and operator-assist technologies to enhance efficiency and reduce emissions. Sustainability goals are also accelerating demand for hybrid and electric-powered machinery in prominent regions. The market is witnessing strong growth driven by rising infrastructure investments and rapid urbanization across emerging economies.

Key Industry Highlights:

- Strong infrastructure and urbanization efforts in Asia Pacific and Latin America are fueling significant equipment demand.

- Rising regulatory pressure and sustainability mandates are prompting a shift toward electric and hybrid machinery in the global construction industry.

- Asia Pacific dominates with 44% of market share, led by China and India’s massive infrastructure investments and development strategies.

- North America is experiencing significant growth in improving its infrastructure over the next eight years, aided by federal infrastructure legislation such as the IIJA.

- Rental and leasing models are gaining traction as cost-efficient alternatives to equipment ownership, transforming market dynamics.

- The surge in automation and telematics integration is driving the shift toward smarter, safer, and more efficient construction equipment solutions.

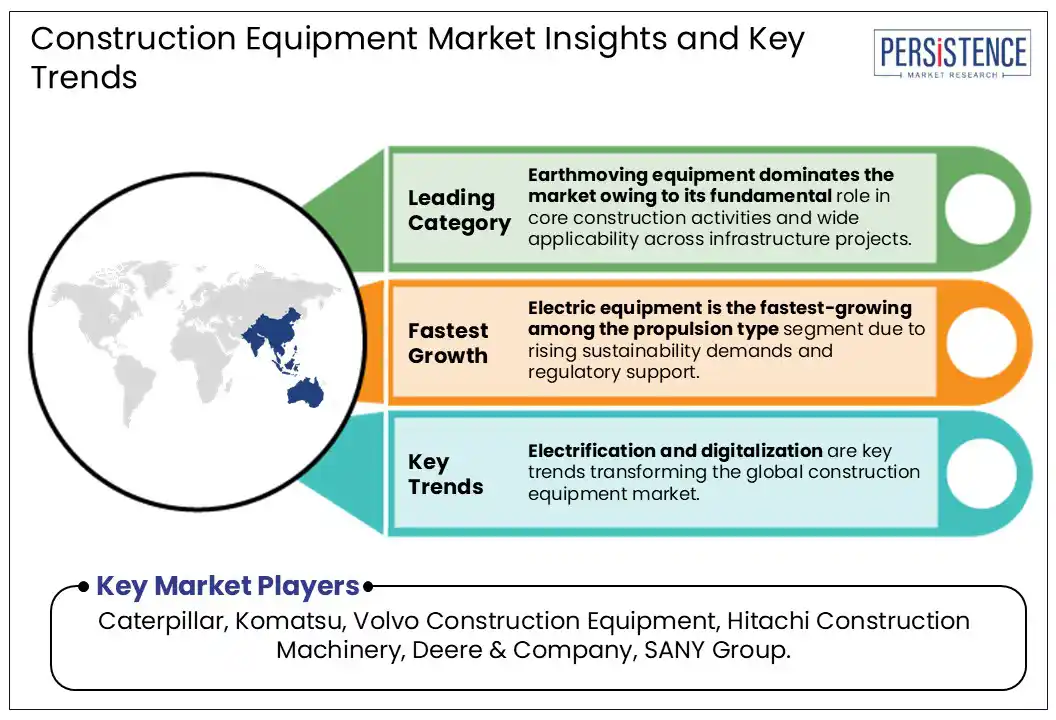

- Earthmoving equipment, mainly excavators, dozers, and high-horsepower loaders, leads the market due to its importance in infrastructure and large-scale construction.

- Infrastructure dominates end use, supported by global mega projects and sustained public investments.

|

Global Market Attribute |

Key Insights |

|

Construction Equipment Market Size (2025E) |

US$ 142.7 Bn |

|

Market Value Forecast (2032F) |

US$ 232.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.3% |

Market Dynamics

Driver - Massive Infrastructure Push Accelerates Demand for Advanced Construction Equipment Globally

The market is primarily driven by unprecedented infrastructure investment, with governments worldwide allocating ambitious budgets to build roads, bridges, airports, railways, and smart cities. Asia Pacific, notably China and India, continues to be the epicenter of this demand, accounting for more than around 56 % of global infrastructure investment. This surge fuels demand for earthmoving equipment like excavators, dump trucks, and motor graders, enhancing fleet expansion across commercial and industrial construction segments. Manufacturers are expanding production of wheeled loaders and concrete mixers to meet the demand from large-scale residential and infrastructure projects.

Rapid technological adoption, including telematics, GPS, automation, and electrification, is transforming equipment fleets into smarter, greener assets. Electric and hybrid propulsion advancements not only help meet tightening environmental regulations but also lower the total cost of ownership over diesel counterparts. Tech-forward equipment types such as skid steer loaders and telescopic handlers are leading automation efforts, enabling enhanced productivity and remote operation.

In January 2023, the PIB press release emphasized that India is rapidly adopting electric and hybrid construction and transportation equipment, supported by government incentives, charging infrastructure subsidies, and Production Linked Incentive (PLI) schemes, aligning with the global shift towards greener fleets and increased production of EV-powered machinery.

Restraint - Component Shortages and Regulatory Barriers Challenge Growth

The market is experiencing setbacks due to ongoing component shortages and logistics delays, particularly in semiconductors and raw materials. Manufacturers such as Caterpillar have reported production delays and rising used-equipment prices, as demand for smart machinery grows. Additionally, fluctuating steel and copper prices, driven by geopolitical tensions and regulations, are increasing production costs, which may hinder the adoption of electric and hybrid machinery.

Stringent environmental and trade regulations are increasingly impacting manufacturers and operators, leading to costly compliance efforts. New mandates, such as the EU’s emissions reporting and U.S. export controls, complicate global supply chains. A shortage of skilled operators for advanced machinery, such as excavators and telescopic handlers, is causing inefficiencies and project delays. A CERAWeek report highlights how permitting and labor gaps in the U.S. are stalling key infrastructure projects, showing the impact of regulatory and workforce challenges on market growth. In April 2025, Caterpillar disclosed that global chip scarcity has extended new machine lead times by up to 20 weeks, inflating secondary-market pricing and disrupting fleet renewal schedules.

Opportunity - Electrification and Green Mandates Unlock High-Growth Potential

The construction equipment market is undergoing a significant transformation as electrification emerges as a major growth opportunity. Increasingly stringent emissions standards and breakthroughs in battery technology are driving the rapid adoption of zero-emission equipment such as electric excavators, loaders, and cranes. Public incentives and municipal procurement policies, including zero-emission mandates and green funding initiatives in regions such as Europe and cities such as Oslo, are encouraging original equipment manufacturers (OEMs) to scale up production of electric machinery. As battery costs continue to decline, the total cost of ownership for electric equipment becomes more competitive, prompting widespread fleet upgrades across residential, infrastructure, and industrial construction sectors.

Manufacturers are integrating battery-electric powertrains with advanced telematics, autonomous systems, and on-site renewable charging infrastructure to support smarter, greener next-generation fleets. Asia Pacific leads this development, driven by rapid urbanization, massive infrastructure investments, and supportive government policies. This region is expected to dominate electric equipment spending, particularly in segments such as electric excavators, loaders, dump trucks, and concrete machinery, positioning these technologies as key drivers of future market growth.

In April 2025, Hitachi Construction Machinery Europe launched its largest-ever lineup of zero-emission excavators, including hydrogen-powered and fully autonomous electric models, alongside digital fleet management solutions to enhance operational efficiency.

Category-wise Analysis

Equipment Type Insights

Earthmoving Equipment Dominates Market Share as Foundational Backbone of Global Construction Activity

Earthmoving Equipment represents the largest and most essential segmentaccounting for around 48% of the total market share. This category includes high-demand machinery such as excavators, loaders, dump trucks, dozers, and motor graders, which form the operational backbone of infrastructure, mining, and real estate construction projects worldwide. Governments across Asia Pacific, the Middle East, and North America continue to invest heavily in transportation networks, urban renewal, and energy infrastructure, driving consistent demand for heavy-duty equipment.

Diesel-powered variants, especially those in the 101 to 400 Hp range, are widely adopted due to their balance between fuel efficiency and performance. The segment is also witnessing a transition toward hybrid and electric models, led by environmental compliance and OEM innovation. Earthmoving Equipment dominates the market due to its multi-functional use and irreplaceable value across all construction verticals.

End-use Insights

Infrastructure Remains the Prime End-use with Long-Term Public Investments

Infrastructure accounts for a significant market share among end-use groups and continues to drive growth. The need for large-scale development, such as highways, railways, bridges, airports, and energy corridors, has pushed demand for high-performance machines like crawler excavators, rigid dump trucks, and concrete pavers. Public-private partnerships (PPPs), smart city initiatives, and multi-year infrastructure pipelines in countries like India (NIP), USA (IIJA), and China (Belt & Road) are driving long-term equipment leasing and procurement.

Earthmoving and concrete & road construction machinery hold prominent demand in this segment due to the heavy-duty nature of applications. Infrastructure projects often require fleets with higher power output (above 400 Hp), making this segment lucrative for OEMs offering technically advanced machinery. The durability, load capacity, and automation potential in this end-use scenario make infrastructure construction the primary driver of equipment modernization and investment.

Regional Insights

Asia Pacific Construction Equipment Market Trends

Asia Pacific Dominates Global Market with Infrastructure-led Earthmoving Equipment Demand Across China and India

Asia Pacific holds the largest share contributing nearly 44% of total revenue in 2024. The region’s dominance is anchored in massive government spending, rapid industrialization, and a growing urban population. Countries like China, India, Japan, and Southeast Asian nations are engaged in multi-billion-dollar public infrastructure projects, significantly increasing demand for earthmoving equipment such as excavators, wheeled loaders, and dump trucks. China, the region’s largest contributor, has announced a USD 173 billion investment in transportation infrastructure in 2024, covering high-speed rail, airports, and highways, as part of its 14th Five-Year Plan. In response, major OEMs like SANY and XCMG are expanding production to serve both domestic and export markets.

India continues to experience accelerated growth, driven by the National Infrastructure Pipeline (NIP) and PM Gati Shakti initiatives, pushing demand for motor graders, backhoe loaders, and concrete machinery. Rising mechanization in rural and Tier-2/Tier-3 areas is creating new demand. OEMs are localizing production and forming partnerships to lower lead times and stay competitive. As a result, Asia Pacific is set to remain the leading region in equipment volume and growth rate.

North America Construction Equipment Market Trends

North America Advances with Federal Infrastructure Spending and Rapid Adoption of Smart & Electric Equipment

North America is poised to witness fast-growth in the global construction equipment market, primarily driven by the Infrastructure Investment and Jobs Act (IIJA) in the United States. This landmark legislation allocates substantial funding for transportation, broadband, and clean energy infrastructure, significantly boosting demand for rigid dump trucks, wheeled excavators, and concrete pumps. The surge in large-scale infrastructure and industrial construction projects has intensified the need for these machines. The U.S. dominates the region’s demand, accounting for around 90% of North America’s construction equipment consumption. Additionally, there is a rising emphasis on next-generation technologies such as telematics, automation, and electric propulsion. Leading OEMs like Caterpillar, John Deere, and CASE are actively driving innovation by developing smart and energy-efficient machinery to meet evolving market needs.

Canada is investing in public transit, green building, and inter-provincial transport through its Infrastructure Bank, boosting the use of material handling equipment like cranes and forklifts. Environmental policies and ESG frameworks are pushing contractors toward low-emission and hybrid machines, while trials of autonomous construction equipment position North America as a testing ground for future solutions. This focus on infrastructure and technology adoption enhances the region's role in global equipment market growth.

Europe Construction Equipment Market Trends

Europe Transforms Equipment Demand with Emission Regulations, EU Funding, and Public-Sector Electrification Mandates

Europe is a strategically evolving region for construction equipment, driven by sustainability policies, infrastructure renewal, and rapid technology adoption. The region is actively transitioning from conventional diesel-powered machines to electric, hybrid, and low-emission equipment, propelled by regulatory frameworks such as the EU Green Deal, carbon neutrality targets, and stringent emissions standards. Earthmoving equipment, including wheeled excavators, backhoe loaders, and compact dump trucks, remains the most in-demand category, while material handling equipment like cranes and forklifts is gaining traction in logistics and public utility projects. Leading European countries such as Germany, France, and Italy are modernizing their machinery fleets to support rail, highway, and smart city projects, while countries in Eastern Europe benefit from EU Cohesion Funds to develop infrastructure.

Scandinavian nations, particularly Norway and Sweden, are at the forefront of zero-emission public procurement policies, with cities like Oslo mandating the exclusive use of zero-emission equipment in public construction projects, significantly boosting demand for electric pavers, mini excavators, and road reclaimers. This shift is complemented by a growing preference for autonomous and connected machines, positioning Europe as a model region for sustainable construction equipment deployment and innovation.

Construction Equipment Market Competitive Landscape

The global construction equipment market is witnessing intensified competition as manufacturers adopt sustainability trends, smart technologies, and modular equipment platforms. Investments in electrification, autonomous operation, and telematics are prevalent in core segments such as excavators and loaders. Strategic partnerships with infrastructure developers and leasing firms are helping secure long-term contracts and expand brand reach. This innovation-driven environment fosters R&D, regional diversification, and future-ready product development.

On the supply side, manufacturers are enhancing networks through local assembly units and responsive aftermarket services, which reduce lead times and improve service efficiency. These strategies support scalability and reinforce competitive agility in both developed and emerging markets.

Key Industry Developments

- In April 2025, Kubota enters an OEM supply agreement with Sumitomo Construction Machinery to procure 14-ton hydraulic excavators for the European market.

- In April 2025, Hitachi Construction Machinery unveils its new LANDCROS concept at bauma?2025, including fleet management systems, zero-emission excavators, and autonomous machinery.

Companies Covered in Construction Equipment Market

- Bobcat Company

- CNH Industrial

- Caterpillar Inc.

- Deere & Company

- Hitachi Construction Machinery

- Hyundai Construction Equipment

- JCB

- Kobelco Construction Machinery

- Komatsu Ltd.

- Kubota Corporation

- Liebherr Group

- SANY Group

- Sumitomo Construction Machinery

- Volvo Construction Equipment

- XCMG

Frequently Asked Questions

The construction equipment market is set to reach US$ 142.7 Bn in 2025.

The construction equipment sector is driven by large-scale infrastructure investments, rapid urbanization, technological advancements, and growing demand for sustainable and efficient machinery.

The construction equipment market is estimated to rise at a CAGR of 7.2% from 2025 to 2032.

The key market opportunities lie in the rising adoption of electric and autonomous equipment, expanding infrastructure projects in emerging economies, and growing demand for rental and smart construction solutions.

The major players are Caterpillar, Komatsu, Volvo Construction Equipment, Hitachi Construction Machinery, Deere & Company, and SANY Group.