- Off-Road Equipment & Machinery

- Earthmoving Equipment Market

Earthmoving Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Earthmoving Equipment Market by Equipment Type (Excavators (Mini Excavator, Crawler Excavator, Wheeled Excavator, Others), Loaders (Skid Steer, Rigid Trucks, Backhoe, Crawler/ Track, Mini Loaders, Dump Trucks)), Engine Capacity (Up to 250 HP, 250-500 HP, More than 500 HP), by Engine Type (ICE, Electric), Application (Construction, Mining, Agriculture & Forestry, Landscaping & Utility Work, Others), and Regional Analysis 2026 - 2033

Earthmoving Equipment Market Size and Share Analysis

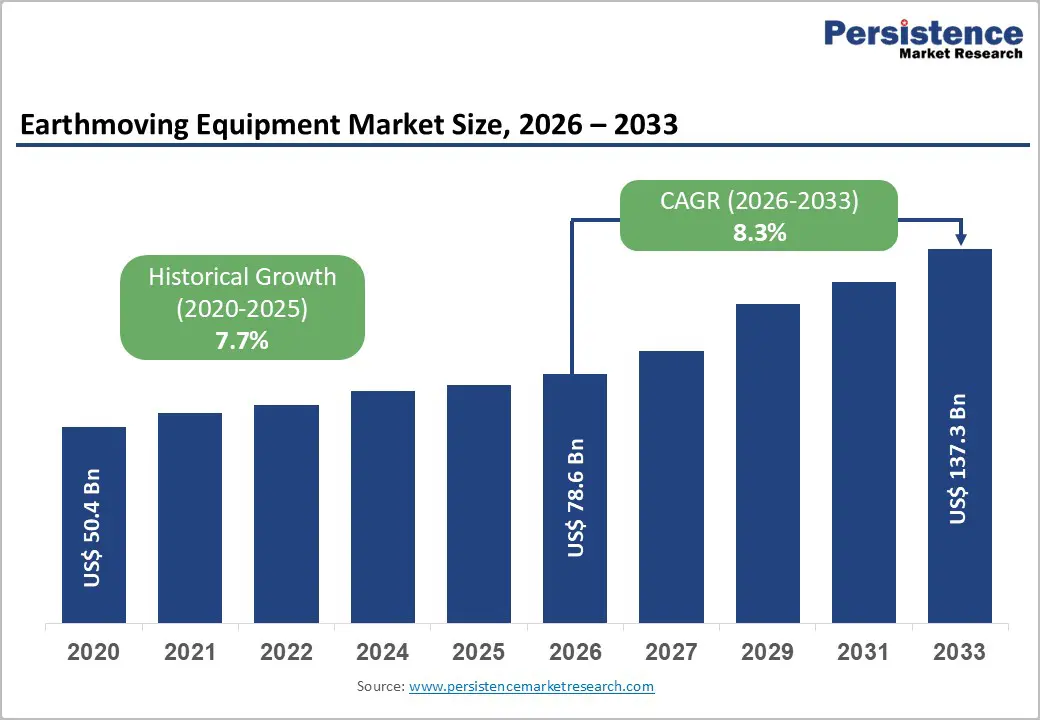

The global earthmoving equipment market size is expected to be valued at US$ 78.6 billion in 2026 and projected to reach US$ 137.3 billion by 2033, growing at a CAGR of 8.3% between 2026 and 2033. This growth is driven by rapid urbanization, large-scale infrastructure development, and rising construction and mining activities worldwide. Major government programs such as the US Infrastructure Investment and Jobs Act (IIJA), with over $500 billion in new funding, are accelerating demand for advanced machinery in road, bridge, and resilience projects. Emerging economies like China and India further strengthen market expansion, with the Asia Pacific leading overall.

Key Industry Highlight:

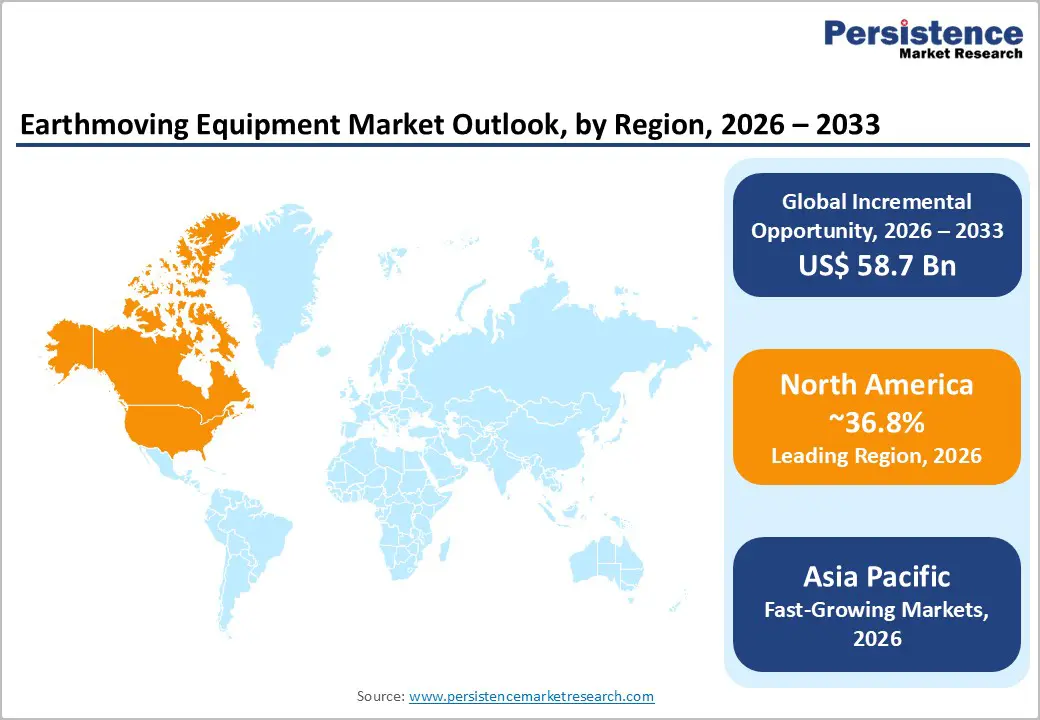

- Leading Region: North America leads with 36.8% share in 2025, fueled by massive infrastructure investments under initiatives like the IIJA and high replacement demand for advanced machinery.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by rapid urbanization, large-scale infrastructure projects in China and India, and rising equipment adoption across emerging markets.

- Leading Equipment Category: Excavators dominate the equipment type with 51.2% share in 2025, crucial for digging, trenching, and site preparation in construction and mining projects.

- Fastest-Growing Equipment Category: Electric machinery is the fastest-growing type, driven by emission regulations, urban low-noise requirements, and sustainability initiatives.

- Key Market Opportunity: Electrification of urban loaders presents a major opportunity, enabling contractors to meet zero-emission policies while reducing fuel and maintenance costs.

| Key Insights | Details |

|---|---|

|

Earthmoving Equipment Size (2026E) |

US$ 78.6 billion |

|

Market Value Forecast (2033F) |

US$ 137.3 billion |

|

Projected Growth CAGR(2026-2033) |

8.3% |

|

Historical Market Growth (2020-2025) |

7.7% |

Market Dynamics

Drivers - Rising Infrastructure and Urban Construction Investments

Global infrastructure expansion is significantly increasing demand for earthmoving equipment, as governments prioritize highways, bridges, smart cities, and large-scale urban development. The United Nations projects that 68% of the world’s population will live in urban areas by 2050, driving major construction activity in fast-growing economies such as India and China. In India, construction equipment sales rose strongly in FY24, with earthmoving machinery forming the largest share of total volumes.

This surge is improving productivity in site preparation, excavation, and material handling, making advanced equipment essential for megaprojects such as expressways, industrial corridors, and metro rail networks. Contractors increasingly rely on efficient earthmoving solutions to meet tight project timelines and rising infrastructure needs.

Growing Adoption of Automation and Smart Equipment Technologies

Technological advancements such as telematics, GPS guidance, and automated machine controls are transforming the earthmoving equipment industry by enhancing efficiency, precision, and operational safety. Industry associations highlight that these digital solutions reduce downtime, improve fleet management, and enable contractors to optimize fuel use and machine performance. Semi-autonomous systems are becoming increasingly common across excavation and grading operations.

Smart earthmoving equipment is now viewed as indispensable for handling complex infrastructure and mining projects, where accuracy and cost control are critical. As automation continues to expand, contractors worldwide are investing in connected machinery to improve productivity, reduce labor dependency, and support sustainable construction practices.

Restraints - High Capital Investment and Ongoing Maintenance Burden

The high upfront cost of earthmoving equipment remains a major restraint, particularly for small and medium-sized contractors with limited capital resources. Heavy machinery such as excavators, bulldozers, and loaders requires substantial investment, making ownership difficult for firms operating under tight budgets. In addition, regular servicing, spare parts replacement, and fuel expenses create long-term financial pressure, especially during periods of economic uncertainty.

As a result, many companies in cost-sensitive regions rely on refurbished or mid-tier equipment instead of purchasing advanced models. This limits fleet modernization and slows the adoption of newer, more efficient machines, ultimately restraining broader market expansion across developing and price-driven markets.

Increasing Regulatory Pressure from Emission and Sustainability Standards

Stringent environmental regulations are placing significant constraints on the earthmoving equipment market, as manufacturers must comply with evolving emission reduction targets and sustainability requirements. Policies across Europe and other regulated regions are pushing the industry toward cleaner engines, alternative fuels, and low-emission machinery, which increases production complexity and overall equipment costs.

Meeting these standards requires heavy investment in research, redesign, and certification processes, creating challenges for both global and regional manufacturers. Higher prices linked to compliance can reduce affordability for contractors, particularly in emerging markets, slowing adoption rates and limiting market growth in highly regulated environments.

Opportunities - Expanding Potential Through Electrification of Earthmoving Equipment

The shift toward electric and low-emission earthmoving machinery presents a strong growth opportunity, especially as construction firms seek cleaner alternatives for urban and regulated environments. Electric loaders and compact excavators are gaining traction due to their suitability for indoor, noise-sensitive, and zero-emission job sites. Advances in battery technology, charging infrastructure, and energy efficiency are further improving the feasibility of electric heavy equipment.

Government incentives and sustainability policies across North America and Europe are accelerating adoption, while contractors benefit from reduced fuel consumption and lower maintenance requirements. Manufacturers investing early in electrified product portfolios are well positioned to capture demand as the industry transitions toward greener construction practices.

Infrastructure Expansion in Emerging Economies Driving New Demand

Rapid infrastructure development across emerging markets, particularly in Asia Pacific, offers significant opportunities for earthmoving equipment manufacturers. Large-scale investments in highways, metro systems, industrial corridors, and smart city initiatives in China, India, and Southeast Asia are creating sustained demand for excavation, grading, and material-handling machinery. Urban growth and rising construction activity continue to expand equipment requirements across both public and private projects.

To capitalize on this momentum, global players are increasingly focusing on localized production, affordable models, and strong dealer networks. Companies that deliver versatile and cost-efficient machines can secure long-term growth in these high-volume developing markets.

Category-wise Analysis

Equipment Type Insights

Excavators lead the earthmoving equipment category with approximately 51.2% market share in 2025, supported by their wide applicability in trenching, digging, lifting, and loading across construction and mining sites. Sub-types such as crawler excavators and mini excavators remain the most deployed machines globally, forming a major portion of earthmoving volumes in high-growth markets. Their durability, multi-functionality, and efficiency in both large infrastructure and urban projects continue to reinforce their dominance.

Looking ahead, compact and electric excavator variants are expected to be the fastest-growing sub-segment, driven by increasing demand for machines suited to confined construction sites, smart city projects, and low-emission urban development requirements.

Engine Capacity Insights

The 250–500 HP segment commands nearly 45.3% market share in 2025, as it offers an optimal balance between performance and fuel efficiency for medium-duty construction and mining operations. Equipment in this power range is widely preferred for excavators, loaders, and dozers that require strong torque without excessive operating costs. Its dominance is supported by rising infrastructure activity, where versatility and reliability are critical for handling diverse project workloads.

The fastest-growing segment is expected to be lower-capacity and compact power classes, as contractors increasingly adopt smaller, agile equipment for urban construction, rental fleets, and applications requiring flexibility rather than extreme horsepower.

Engine Type Insights

Internal Combustion Engine (ICE) equipment holds roughly 85.9% market share in 2025, driven by its proven reliability, high-duty cycle capability, and widespread fueling infrastructure. ICE-powered machines remain the preferred choice in demanding environments such as mining, large-scale earthworks, and remote infrastructure projects, where uninterrupted performance and strong residual value are essential. Established service networks further strengthen their continued dominance across global markets.

The fastest-growing category is expected to be electric and hybrid earthmoving equipment, as sustainability regulations, urban emission restrictions, and advances in battery systems push manufacturers and contractors toward cleaner alternatives.

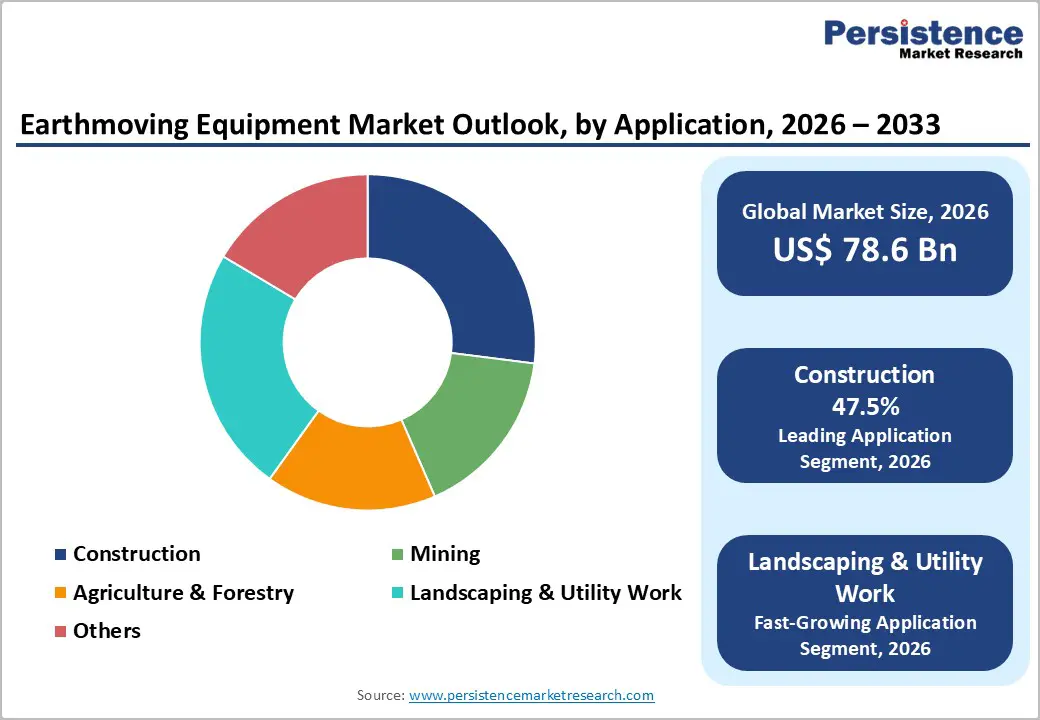

Application Insights

Construction dominates the application landscape with over 47.5% market share in 2025, fueled by strong activity in residential, commercial, and infrastructure development worldwide. Earthmoving equipment plays a critical role in site preparation, excavation, grading, and material handling, making it indispensable for highways, bridges, industrial zones, and urban expansion projects. Rapid urbanization across the Asia Pacific and other developing regions continues to reinforce construction as the primary demand driver.

The fastest-growing application is expected to be infrastructure modernization and utility development, as governments prioritize transport upgrades, renewable energy projects, and resilient urban systems requiring extensive excavation and groundwork support.

Regional Insights

North America Earthmoving Equipment Market Trends

North America remains a leading region in the earthmoving equipment market, supported by strong infrastructure spending and modernization programs. The United States continues to drive demand through initiatives such as the Infrastructure Investment and Jobs Act (IIJA), funding thousands of resilience and transportation projects nationwide. In 2025, North America accounted for around 36.8% of the market share, reflecting its mature construction ecosystem and high replacement demand for advanced machinery.

The region is also witnessing rapid adoption of telematics, automation, and semi-autonomous systems, with manufacturers like Caterpillar advancing smart equipment platforms. Electrification is gaining momentum amid regulatory pressure, positioning North America as a key hub for next-generation earthmoving solutions.

Europe Earthmoving Equipment Market Trends

Europe demonstrates steady market expansion, led by construction and industrial activity across Germany, France, and the UK. The region’s growth is shaped by strict EU emission regulations targeting long-term carbon reductions, pushing manufacturers toward cleaner engine technologies and sustainable equipment portfolios. Europe is expected to grow at a CAGR of 8.7%, supported by ongoing infrastructure renewal and investment in energy transition projects.

Countries such as Spain are increasing spending on renewable energy and utility infrastructure, boosting demand for specialized earthmoving machinery. Equipment makers are also upgrading product lines with low-emission haulers and digitalized systems, making Europe a critical market for regulatory-driven innovation.

Asia Pacific Earthmoving Equipment Market Trends

Asia Pacific represents the fastest-expanding regional market, fueled by rapid urbanization and massive infrastructure development across China, India, and ASEAN economies. In 2025, Asia Pacific holds approximately 34.5% market share, driven by large-scale investments in rail networks, expressways, industrial corridors, and smart city construction. Strong equipment demand is also supported by rising contractor activity and government-backed development programs.

The region is increasingly adopting compact and versatile machinery suited for dense urban environments, with Japan leading advancements in mini equipment technology. Growing manufacturing capabilities in ASEAN further strengthen Asia Pacific’s position as both a high-consumption and high-production hub.

Competitive Landscape

The earthmoving equipment market is relatively consolidated, with leading manufacturers maintaining strong positions through extensive product portfolios, global distribution networks, and continuous innovation. Competition is shaped by advancements in automation, with semi-autonomous systems becoming increasingly common across construction and mining operations.

Key differentiators include the integration of telematics, GPS-enabled monitoring, and predictive maintenance solutions that improve uptime and fleet efficiency. Manufacturers are also focusing on electrified and hybrid machinery to meet sustainability goals and evolving emission regulations. Digital fleet management and eco-friendly equipment designs are emerging as critical factors influencing competitive advantage.

Key Developments:

- In January 2025, Volvo Construction Equipment introduced its redesigned articulated haulers range (A25–A60), marking the company’s largest portfolio renewal and improving performance, productivity, and hauling efficiency across demanding construction and mining applications.

- In January 2025, Hyundai Construction Equipment received an order for 122 medium excavators from the Philippines Department of Public Works and Highways (DPWH), strengthening its presence in Southeast Asia’s growing infrastructure and earthmoving equipment demand.

- In August 2025, Caterpillar partnered with Luminar to integrate advanced LiDAR technology into its Cat Command autonomy platform, enhancing safety and precision in mining operations through improved obstacle detection and autonomous equipment performance.

Companies Covered in Earthmoving Equipment Market

- ABB Limited

- Endress+Hauser Management AG

- Siemens AG

- Krohne

- Pepperl+Fuchs GmbH

- Continental AG

- VEGA Grieshaber KG

- ;Hans TURCK GmbH & Co. KG

- Gems Sensors, Inc.

- Omega Engineering Inc.

- KEYENCE CORPORATION

- Texas Instruments Incorporated

- MIGATRON CORPORATION

- Honeywell International Inc.

- AMETEK.Inc.

Frequently Asked Questions

The global earthmoving equipment market is expected to reach US$ 78.6 billion in 2026.

Key drivers include urbanization and infrastructure growth, with North America leading investments via IIJA and Asia Pacific driving rapid equipment adoption.

North America leads with 36.8% share in 2025, supported by large-scale infrastructure programs and replacement demand.

Electrification presents a major opportunity, with electric machinery as the fastest-growing type for urban and low-emission projects.

Leaders include ABB Limited, Endress+Hauser Management AG, Siemens AG, Krohne, and Pepperl+Fuchs GmbH.