- Specialty & Fine Chemicals

- Sustainable Construction Market

Sustainable Construction Market Size, Share, and Growth Forecast, 2026 - 2033

Sustainable Construction Market by Product Type (Interior, Exterior), Material (Green Building, Energy Efficient, Recycled, Others), End-User (Residential, Commercial, Infrastructure), and Regional Analysis for 2026-2033.

Sustainable Construction Market Share and Trends Analysis

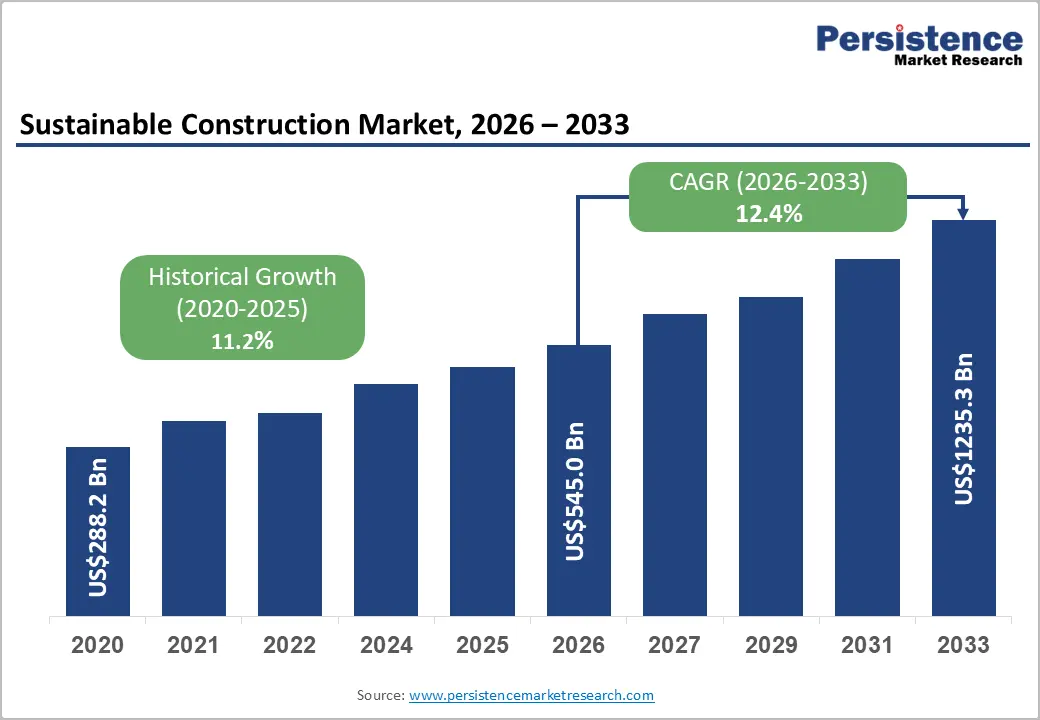

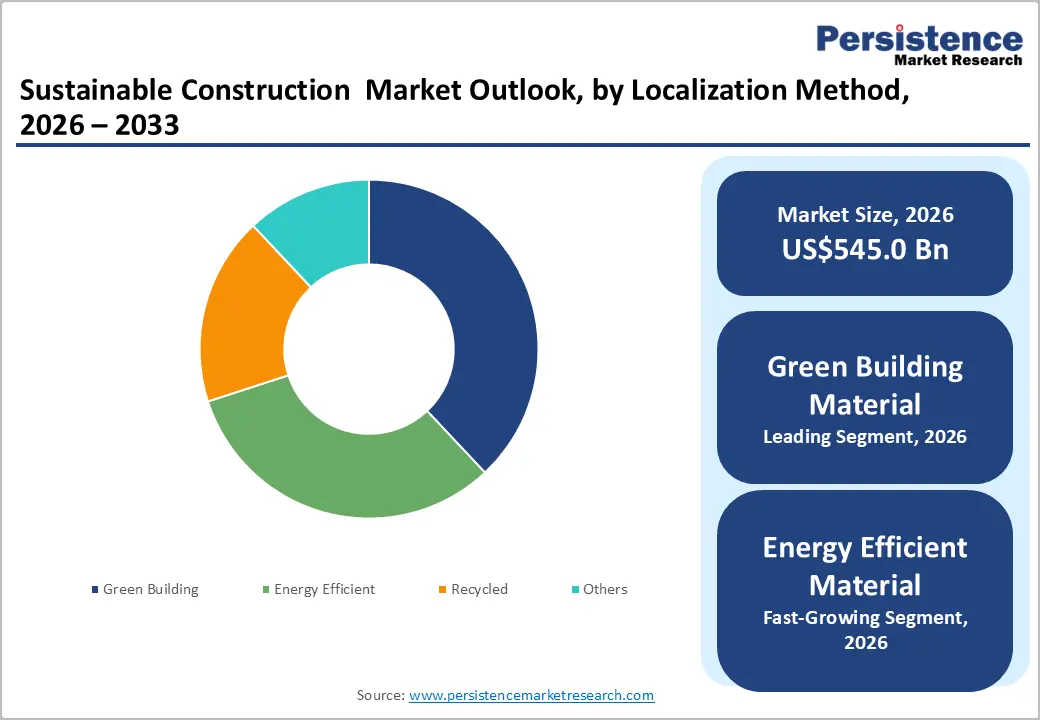

The global sustainable construction market size is likely to be valued at US$ 545.0 billion in 2026, and is projected to reach US$ 1,235.5 billion by 2033, growing at a CAGR of 12.4% during the forecast period 2026−2033. Market expansion is being driven by the construction sector’s accelerating transition toward environmentally responsible building practices, as governments are enforcing stricter carbon reduction targets and continuously updating building codes.

Large-scale public infrastructure programs are increasingly prioritizing energy efficiency, low-emission materials, and resource optimization, which is strengthening demand for sustainable construction solutions across both new-build and retrofit projects. Corporate sustainability commitments are also playing a central role, as developers and asset owners are increasingly requiring green building certifications to meet environmental, social, & governance (ESG) objectives. Rising awareness of lifecycle cost benefits, including lower operating expenses and improved asset resilience, is influencing procurement decisions across residential, commercial, and infrastructure segments. At the same time, ongoing technological innovation in sustainable materials, digital design tools, and construction methods is reshaping project delivery models.

Key Industry Highlights

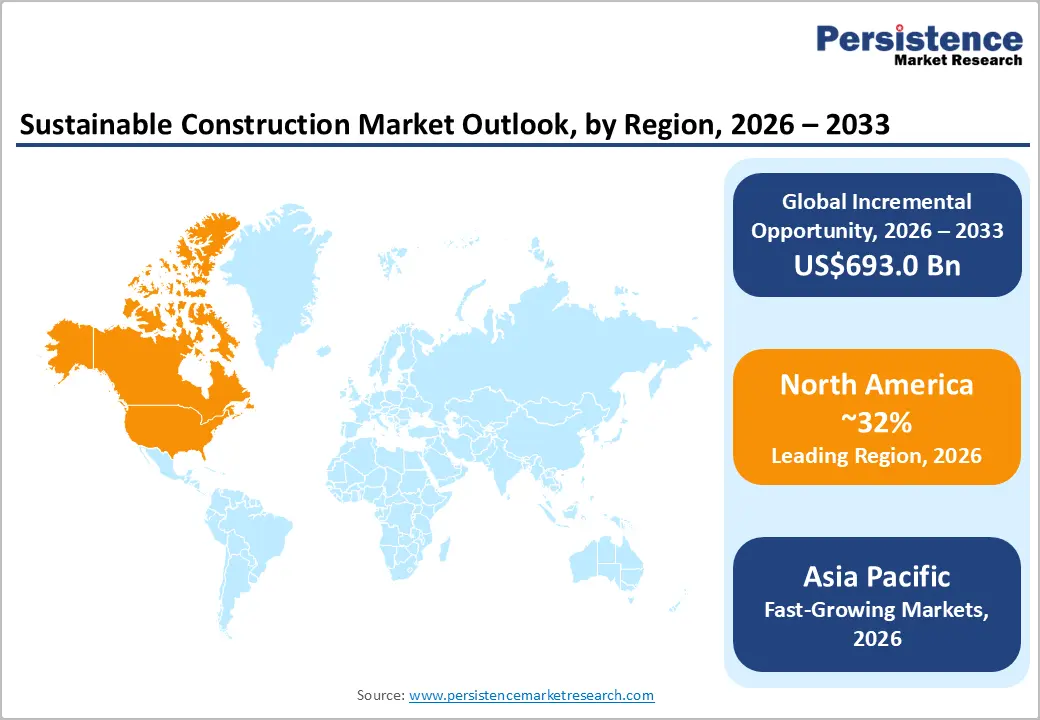

- Dominant Region: North America is set to command approximately 32% market share in 2026, driven by infrastructure modernization programs that promote sustainable construction.

- Fastest-growing Market: The Asia Pacific market is likely to be the fastest-growing due to advanced technologies with disaster-resilience features and extensive seismic retrofitting expertise.

- Dominant Material: Green building materials are expected to account for an estimated 55% of revenue in 2026, encompassing recycled-content products, rapidly renewable materials, and locally sourced components.

- Fastest-growing Material: Energy-efficient materials are projected to be the fastest-growing segment over the 2026-2033 forecast period, driven by building code evolution prioritizing operational energy performance and net-zero energy.

- September 2025: Henkel's UniBond brand launched a next-generation cardboard-based cartridge for construction adhesives and sealants, reducing plastic content by at least 51% while cutting non-recyclable waste by 73%.

| Key Insights | Details |

|---|---|

| Sustainable Construction Market Size (2026E) | US$ 545.0 Bn |

| Market Value Forecast (2033F) | US$ 1,235.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 12.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 11.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Regulatory Mandates and Carbon Neutrality Commitments

Regulatory authorities worldwide enforce increasingly stringent requirements that elevate sustainable practices from optional enhancements to mandatory obligations. For example, the European Union (EU) implements its Energy Performance of Buildings Directive (EPBD), which mandates near-zero energy performance for all new buildings by 2030, compelling developers to integrate advanced energy-efficient designs from project inception. In parallel, the United States directs substantial funding through the Infrastructure Investment and Jobs Act, embedding comprehensive sustainability provisions across transportation, energy, and public works initiatives to accelerate green infrastructure deployment. Buildings are a primary source of global energy-related carbon emissions, prompting governments to progressively strengthen building codes.

China advances its 14th Five-Year Plan with explicit mandates for green building standards across the majority of new urban construction projects, reshaping urban development patterns nationwide. These coordinated regulatory frameworks generate powerful compliance-driven demand that fundamentally reshapes market dynamics. The World Green Building Council (WGBC) confirms that such policies now govern markets encompassing the majority of global construction expenditure. Sustainable construction is the emerging baseline standard rather than a premium alternative, positioning early adopters to secure competitive advantages through streamlined compliance processes and preferential access to regulated markets.

Skilled Labor Shortages and Technical Complexity

The construction industry confronts significant shortages of workers skilled in sustainable building methods. Firms struggle to recruit personnel with expertise in specialized green construction techniques. The Associated General Contractors of America (AGC) highlights persistent challenges in filling roles that demand advanced capabilities. Installation of sophisticated building envelope systems requires precise technical knowledge beyond conventional practices. Similarly, renewable energy systems and high-performance heating, ventilation, & air conditioning (HVAC) units demand elevated competencies that traditional training programs rarely address. These gaps necessitate substantial investments in workforce development to bridge critical skill deficiencies.

Quality assurance issues compound workforce challenges as technological complexity increases. Improper installation of advanced systems undermines expected energy efficiency gains and compromises long-term building performance. Geographic variations in training access exacerbate regional disparities, especially in areas distant from urban centers where expertise concentrates. Construction leaders must prioritize strategic workforce planning through comprehensive training academies and certification programs tailored to sustainable practices. Executives recognize that proactive skill development creates sustainable competitive advantages, enabling companies to meet escalating project demands while maintaining superior quality standards across diverse market geographies.

Growing Trend of Corporate Sustainability Initiatives

Corporations increasingly establish ambitious sustainability targets to minimize their environmental impact across operations. These commitments drive substantial demand for sustainable construction materials in corporate offices, manufacturing facilities, and retail environments. Business leaders prioritize building solutions that demonstrate measurable progress toward net-zero goals and enhance corporate social responsibility profiles. Developers and material suppliers gain strategic positioning by delivering innovative, high-performance products that precisely align with these corporate sustainability priorities.

This corporate momentum creates significant market opportunities for sustainable construction providers. Companies offering advanced materials, such as low-carbon concrete alternatives, recycled steel components, and energy-efficient insulation systems, capture premium pricing while securing long-term client relationships. Suppliers differentiate through comprehensive lifecycle assessments that quantify carbon reductions and energy savings, providing corporate clients with verifiable data for sustainability reporting. The growing recognition of green buildings' social benefits, including improved employee wellness and enhanced brand reputation, is accelerating business investments in sustainable projects.

Category-wise Analysis

Product Type Insights

Interior products are poised to dominate by capturing approximately 60% of the sustainable construction market revenue share in 2026, on account of their direct impact on indoor environmental quality and occupant health, alongside their relative ease of implementation compared to structural modifications. This segment encompasses sustainable flooring systems, low-VOC paints and coatings, energy-efficient lighting and controls, high-performance windows and glazing, and environmentally responsible interior finishes.

Commercial office renovations and residential remodeling projects prioritize interior product upgrades as cost-effective ways to achieve green building certifications, with Leadership in Energy and Environmental Design (LEED) and WELL Building Standard credits heavily weighted toward indoor environmental quality.

Exterior products are likely to be the fastest-growing segment over the 2026-2033 forecast period, reflecting heightened focus on building envelope performance as the primary determinant of energy efficiency and operational carbon emissions. Advanced exterior cladding systems, high-performance insulation materials, cool roofing technologies, and integrated photovoltaic systems are experiencing accelerating adoption as building energy codes become progressively stringent.

Technological innovations, including dynamic facades with automated shading, thermochromic glazing that responds to ambient conditions, and prefabricated envelope systems that enable rapid installation, are expanding market opportunities while improving performance and cost-competitiveness relative to conventional building envelope solutions.

Material Insights

Green building materials are expected to hold the largest revenue share, reaching 55% in 2026, encompassing recycled-content products, rapidly renewable materials, locally sourced components, and materials with environmental product declarations documenting lifecycle impacts. This segment includes bamboo flooring and structural products, recycled steel and aluminum, reclaimed wood, recycled plastic lumber, and cork materials. The market benefits from established supply chains, broad product availability across multiple categories, and widespread familiarity among architects and contractors, reducing specification barriers.

Major manufacturers have introduced sustainable product lines across portfolios, with companies including Interface, Armstrong, and Mohawk achieving substantial market share through comprehensive green building materials offerings supported by technical documentation facilitating project certification processes.

Energy-efficient materials are projected to be the fastest-growing segment over the 2026-2033 forecast period, driven by building code evolution that prioritizes operational energy performance and net-zero energy targets that require superior insulating values and thermal mass characteristics. Residential construction increasingly specifies continuous insulation and air-sealing systems, while commercial projects integrate dynamic glazing systems that optimize daylight while minimizing solar heat gain.

Technological advancements in aerogel insulation and vacuum-insulated panels are enabling retrofit applications in space-constrained existing buildings where conventional insulation thicknesses prove impractical, substantially expanding addressable market opportunities.

End-User Insights

Residential is anticipated to lead with an approximate 45% of the sustainable construction market share in 2026, aided by residential renovations incorporating sustainable construction practices and materials. Growing consumer awareness of the health impacts of building materials and indoor air quality drives demand for low-VOC products and formaldehyde-free materials. Government incentive programs, including tax credits, rebates, and preferential mortgage rates for energy-efficient homes, stimulate market growth.

Homebuilders, including KB Home, Lennar, and national equivalents in international markets, have established net-zero energy home programs, with sustainable features transitioning from premium options to standard specifications in response to buyer preferences and regulatory requirements.

Infrastructure is expected to be the fastest-growing segment over the 2026-2033 forecast period. Governments and municipalities increasingly prioritize sustainable materials within infrastructure projects, including roads, bridges, and public utilities. These initiatives target reductions in carbon emissions, enhanced climate resilience, and long-term sustainable development objectives. Recycled aggregates, permeable paving systems, and low-carbon concrete are gaining widespread adoption due to their environmental advantages and lifecycle cost efficiencies.

Public-sector investments in green infrastructure are accelerating demand for verified performance materials that meet stringent environmental standards. Project owners favor solutions that demonstrate measurable sustainability metrics and proven durability under heavy-load conditions.

Regional Insights

North America Sustainable Construction Market Trends

North America is set to command a significant portion of the sustainable construction market share at approximately 32% in 2026. The United States drives regional dominance, while Canada and Mexico play supporting roles. The U.S. Green Building Council (USGBC) establishes thought leadership through its LEED certification program, which influences standards worldwide. Governments channel substantial climate investments through mechanisms such as the Inflation Reduction Act (IRA), offering tax incentives, rebates, and grants that accelerate both new developments and existing building upgrades.

Technology hubs, including Silicon Valley, Boston, and Toronto, foster advanced research in materials science and construction technologies.

Progressive state regulations create compliance imperatives that exceed federal baselines, positioning early adopters for competitive advantages. California enforces its Title 24 Building Energy Efficiency Standards, mandating solar readiness for new residential projects. New York City implements Local Law 97, establishing emissions limits for large buildings with significant penalties for noncompliance. Investment capital flows toward efficiency retrofits and decarbonization solutions, targeting the vast existing building inventory facing performance mandates.

Commercial properties encounter tenant-driven pressures, while residential markets embrace net-zero homes and Passive House standards.

Europe Sustainable Construction Market Trends

Europe demonstrates global leadership in sustainable construction through stringent regulatory frameworks and comprehensive market transformation initiatives. The EU has been aggressively advancing its European Green Deal and Fit for 55 package, establishing binding emissions-reduction targets and climate-neutrality objectives. Germany leads national markets, followed by the United Kingdom, France, and Spain, while Nordic countries achieve the highest per-capita performance through ambitious climate commitments.

The EPBD has set minimum energy standards for both new developments and existing buildings, compelling member states to progressively strengthen their national building codes. France implements its RE2020 environmental regulation, introducing carbon intensity limits that encompass operational and embodied emissions across building lifecycles.

National programs accelerate market adoption through targeted financial incentives and performance mandates. Germany deploys KfW Efficiency House programs that offer preferential financing for structures that exceed minimum code requirements. The United Kingdom enforces its Future Homes Standard, mandating substantial carbon reductions for new residential construction alongside gas boiler phase-outs that promote heat pump systems and enhanced building envelopes.

Regulatory harmonization across EU member states streamlines operations for manufacturers and contractors serving multiple jurisdictions. Europe excels in Passive House construction methodologies and circular-economy practices, including building-materials passports that facilitate future deconstruction and recycling.

Asia Pacific Sustainable Construction Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for sustainable construction through 2033, driven by rapid urbanization, massive infrastructure programs, and evolving environmental policies. China commands regional dominance, followed by Japan, India, Australia, and ASEAN countries. National strategies accelerate the transformation of the building sector through mandatory green standards and carbon-reduction targets outlined in comprehensive five-year plans.

Provincial authorities enforce progressively stringent building codes, requiring technologies such as building information modeling (BIM), renewable energy systems, and vegetative roofing in major urban centers. Governments prioritize sustainable development practices that balance economic expansion with environmental stewardship.

Japan integrates advanced technologies with disaster resilience features, leveraging extensive seismic retrofitting expertise. India advances through its Smart Cities Mission, mandating green building certification for public projects while residential demand accelerates market adoption. Singapore leads ASEAN nations with its Green Mark certification scheme, aiming to achieve widespread green building penetration. Manufacturing advantages, including cost-competitive labor and proximity to raw materials, establish the region as the global hub for sustainable materials production and export. Foreign investment flows toward production facilities, project developments, and technology collaborations.

Competitive Landscape

The global sustainable construction market structure is moderately fragmented, with leading companies such as LafargeHolcim, CRH plc, Saint-Gobain, Kingspan Group, and Interface controlling approximately 30–35% of the total market share. The competitive environment is continuing to intensify as large, established building materials manufacturers are competing alongside innovative startups that are focusing on specialized low-carbon and high-performance solutions. Market leaders are consistently allocating substantial resources to research and development to advance next-generation materials that are meeting increasingly stringent regulatory requirements while also addressing higher expectations around durability, energy efficiency, and environmental performance.

Strategic consolidation is increasingly shaping the competitive landscape, as companies pursue mergers and acquisitions to broaden product portfolios, secure access to raw materials, and accelerate entry into high-growth regional markets. Collaborative partnerships with technology providers and materials science innovators are enabling faster commercialization of advanced sustainable solutions across residential, commercial, and infrastructure applications. As sustainability requirements are becoming more embedded in procurement frameworks, competitive advantage is increasingly shifting toward firms that can scale innovation efficiently while delivering verified environmental benefits, regulatory compliance, and long-term economic value for project stakeholders.

Key Industry Developments

- In January 2026, the American Concrete Institute (ACI) and Global Consensus on Sustainability in the Built Environment (GLOBE) signed a MoU to advance sustainable concrete construction through shared technical expertise, publications, conferences, and collaborative initiatives.

- In December 2025, Egypt's New Urban Communities Authority (NUCA) approved an incentive package to promote green construction in new cities, covering new developments, projects under 20% complete, and large-scale initiatives over 50 feddans, with a dedicated task force ensuring compliance via inspections and certifications.

- In June 2025, CREDAI, representing over 13,000 Indian real estate developers, partnered with Adani Cement to promote sustainable construction using GRIHA-certified green concrete products, additives, and technical support, while launching a Green India Council for reforestation and green standards, and a Skilling Council to train 15,000+ workers across 25 cities.

Companies Covered in Sustainable Construction Market

• Clark Group

• Gilbane Building company

• Alumasc Group Plc

• The Turner Corp.

• Florbo International SA

• Bauder ltd.

• The Whiting- Turner Contracting Company

• Hensel Phelps

• Alumasc Group Plc,

• Forbo International SA

Frequently Asked Questions

The global sustainable construction market is projected to reach US$545.0 billion in 2026.

Stringent net-zero regulations, corporate sustainability mandates, and infrastructure modernization programs are propelling market growth.

The market is poised to witness a CAGR of 12.4% from 2026 to 2033.

Corporate facility transformations, public infrastructure projects, and existing building retrofit programs create substantial market expansion potential.

LafargeHolcim, CRH plc, Saint-Gobain, Kingspan Group, and Interface, Inc. are some of the key players in the market.