- Specialty & Fine Chemicals

- Bangladesh Construction Chemicals Market

Bangladesh Construction Chemicals Market Size, Share, and Growth Forecast 2026 - 2033

Bangladesh Construction Chemicals Market by Product Type (Concrete Admixture, Adhesives & Sealants, Water Proofing Chemicals, Concrete Repair Mortar, Flooring Compounds, Protective Coating, Plaster, Asphalt Additives, and Others), Application (Infrastructure, Residential, Commercial, and Industrial), and Regional Analysis for 2026 - 2033

Bangladesh Construction Chemicals Market Size and Share Analysis

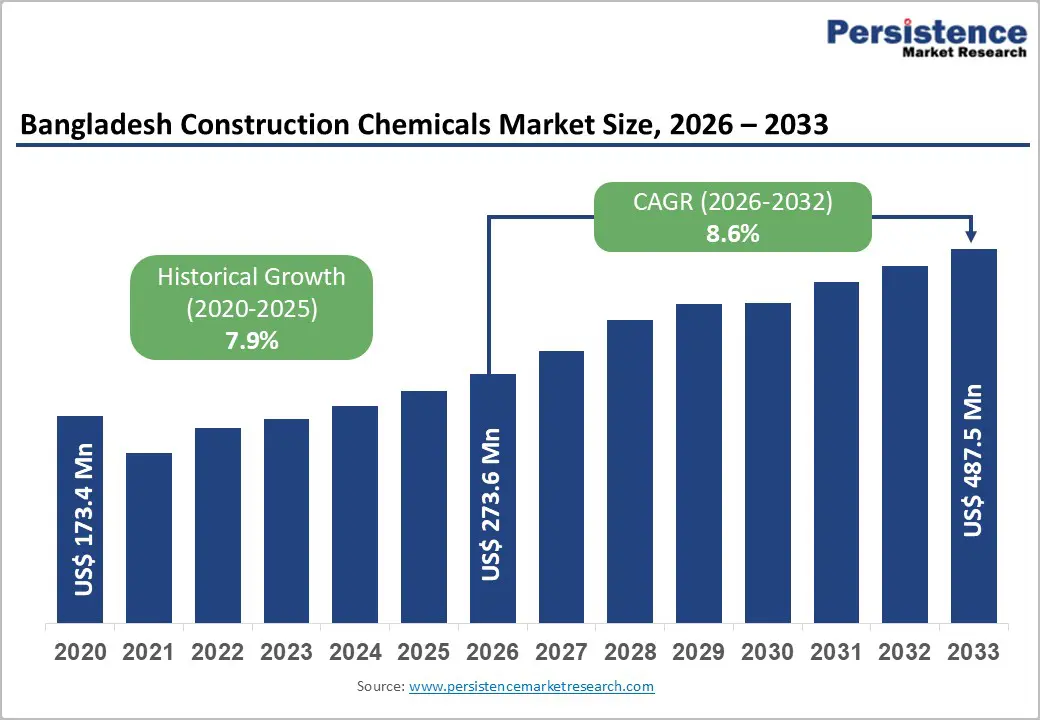

The Bangladesh Construction Chemicals market size is likely to be valued at US$ 273.6 million in 2026 and is projected to reach US$ 487.5 million by 2033, growing at a CAGR of 8.6% between 2026 and 2033.

The market's robust expansion is primarily fueled by the Government of Bangladesh's ambitious public infrastructure investment program and accelerating urbanization, with the country's urban population expanding at approximately 3.5% annually according to the Bangladesh Bureau of Statistics (BBS). The Eighth Five Year Plan (2021–2025) allocated over BDT 7.97 trillion for infrastructure and public development, directly stimulating demand for high-performance construction chemicals across all product categories.

Key Industry Highlights:

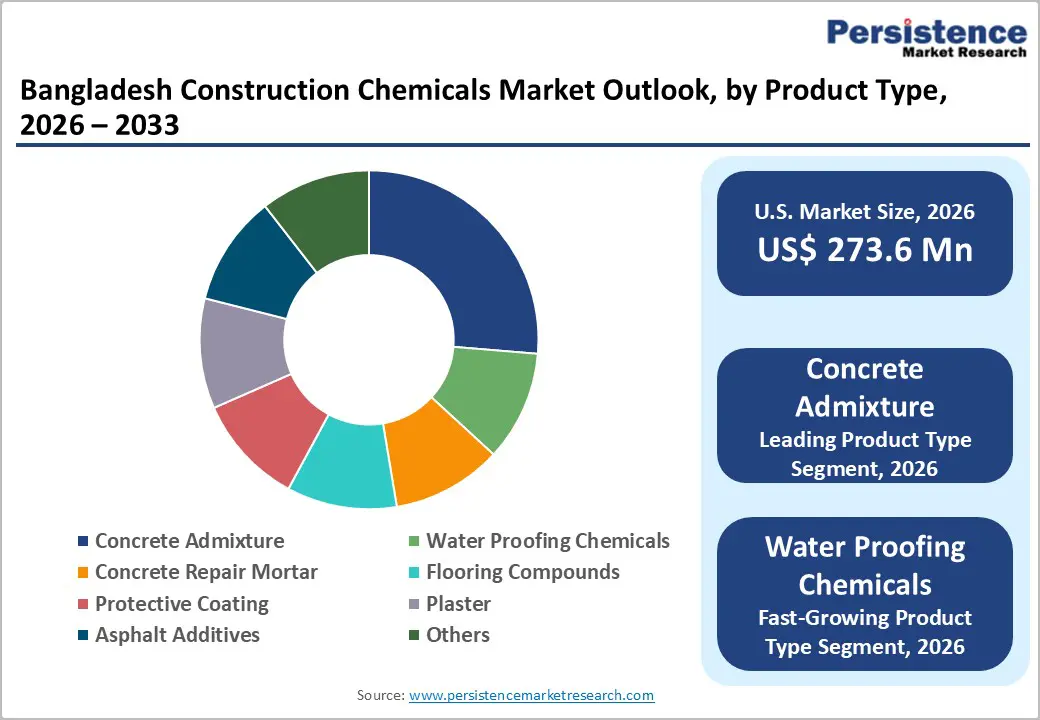

- Dominant Product Type: Concrete Admixtures dominate the Product Type segment with approximately 39% market share in Bangladesh in 2026, underpinned by mandatory use in government-specification concrete projects and the rapidly growing adoption of PCE-based high-range water reducers.

- Growing Product Type: Waterproofing Chemicals represent the fastest-growing product type segment in Bangladesh, driven by rising adoption of crystalline and polymer-modified waterproofing systems in flood-resilient residential and infrastructure construction.

- Dominant Application: Infrastructure is the leading and fastest-growing Application segment, commanding approximately 42% share in Bangladesh in 2026, driven by sustained ADP infrastructure allocations and high-profile national projects requiring certified, performance-grade chemical products.

- Growing Application: The Industrial application segment is the fastest-growing end-use category, propelled by rapid adoption of chemical-resistant protective coatings, heavy-duty flooring compounds, and industrial sealants across factory and warehouse construction within the Bangladesh Economic Zones Authority (BEZA).

- Key Market Opportunity: Green and sustainable construction chemicals represent the most significant market opportunity, as LEED, EDGE, and national climate adaptation mandates, supported by ADB and World Bank project funding, drive demand for eco-compliant, low-VOC formulations with premium margin potential.

| Key Insights | Details |

|---|---|

|

Bangladesh Construction Chemicals Market Size (2026E) |

US$ 273.6 Mn |

|

Market Value Forecast (2033F) |

US$ 487.5 Mn |

|

Projected Growth CAGR (2026-2033) |

8.6% |

|

Historical Market Growth (2020-2025) |

7.9% |

Market Dynamics

Drivers - Surge in Government-Led Infrastructure Development Across Bangladesh

Bangladesh has witnessed an unprecedented scale of public infrastructure investment over the past decade, creating durable and high-volume demand for specialty construction chemicals. The Roads and Highways Department (RHD) and the Bangladesh Bridge Authority have collectively overseen projects worth over BDT 1.2 trillion under successive national plans, encompassing road widening, bridge construction, and expressway development. Landmark projects, including the Dhaka Elevated Expressway, the Karnaphuli Tunnel, the Padma Multipurpose Bridge, and the ongoing Dhaka Metro Rail network, managed by Dhaka Mass Transit Company Limited (DMTCL), have generated vast requirements for concrete admixtures, structural waterproofing systems, and high-durability protective coatings.

According to the Annual Development Programme (ADP) for Fiscal Year 2023–24, the transport and infrastructure sector alone received an allocation of approximately BDT 580 billion, reflecting the government's continued prioritization of construction activity. These megaprojects mandate high-performance chemical specifications, making construction chemicals a non-negotiable component of project execution across all development phases.

Rapid Urbanization Driving Residential and Commercial Construction Activity

Bangladesh's accelerating urbanization is generating structural and sustained demand for construction chemicals throughout the residential and commercial building segments. The Bangladesh Bureau of Statistics (BBS) projects that over 40% of the national population will reside in urban areas by 2031, compared to approximately 36% in 2022. This demographic shift is driving intensive multi-storey residential construction in Dhaka, Chittagong, Sylhet, and Khulna, where the use of tile adhesives, waterproofing compounds, repair mortars, and flooring chemicals is most concentrated.

The Real Estate and Housing Association of Bangladesh (REHAB) estimates that Bangladesh requires approximately 3.8 million new dwelling units annually to meet existing and emerging demand, a scale of construction that inherently necessitates the deployment of advanced chemical products for structural integrity and longevity. The growing middle class and improving mortgage penetration under Bangladesh Bank's housing finance policy frameworks are further amplifying the consumption of quality construction chemicals in this segment.

Restraints - High Import Dependency and Raw Material Price Volatility

A fundamental structural constraint of Bangladesh's construction chemicals sector is its heavy reliance on imported raw materials. Key chemical inputs, including Polycarboxylate Ethers (PCE), Sulfonated Naphthalene Formaldehyde (SNF), and specialty polymers, are predominantly sourced from China, India, and Europe, with the Bangladesh Trade and Tariff Commission estimating that over 60% of critical chemical feedstocks are imported. This dependency exposes local manufacturers to significant volatility arising from global commodity price cycles, geopolitical supply disruptions, and currency depreciation.

During the post-pandemic inflationary period of 2022–2023, sharp increases in petrochemical input costs severely compressed margins for domestic formulators. The imposition of supplementary import duties on specific chemical categories further raises production costs, limiting price competitiveness and slowing adoption among cost-sensitive small and medium contractors across Bangladesh.

Limited Technical Awareness and Skilled Applicator Shortage

The effective adoption of advanced construction chemicals in Bangladesh is critically hampered by a widespread deficit in technical knowledge among construction contractors and applicators. A large proportion of small-to-mid-scale construction firms continue to rely on conventional methods and express reluctance toward specialty chemicals, primarily due to unfamiliarity with application protocols, dosage requirements, and curing procedures. Industry stakeholders, including the Bangladesh Institute of Construction Management (BICM) have acknowledged that formal technical training on chemical product application remains inadequate, especially outside major metropolitan centers.

Improper application of products such as epoxy protective coatings, crystalline waterproofing systems, or cementitious repair mortars can lead to premature product failure, reinforcing skepticism among end users and deterring repeat purchases. This knowledge gap acts as a persistent market penetration barrier, particularly in Tier-2 and Tier-3 towns and rural construction markets.

Opportunity - Green and Sustainable Construction Chemicals Aligned with National Climate Goals

Bangladesh's national climate commitments and green building ambitions are creating a compelling and expanding opportunity for sustainable construction chemical formulations. The country's National Adaptation Plan (NAP) and obligations under the Paris Agreement are driving increased uptake of environmentally responsible building practices, particularly in donor-funded and government-institutional projects. The Bangladesh Green Building Council (BGBC) has been actively promoting LEED and EDGE certification pathways for commercial and institutional construction, compelling architects and project developers to specify low-VOC adhesives, eco-formulated waterproofing membranes, and green admixtures.

International financing institutions, including the Asian Development Bank (ADB) and the World Bank, are channeling investments into climate-resilient infrastructure programs in Bangladesh, such as the Dhaka Environmentally Sustainable Water Supply Project, which specifies high-performance, eco-compliant chemical products. Manufacturers that proactively develop green product lines and pursue ISO 14001 environmental certification will gain a decisive competitive advantage in this growing premium market segment, which commands higher margins and stronger customer retention.

Rising Demand from Industrial and Special Economic Zone Construction

The Government of Bangladesh's ambitious industrial expansion strategy under the Special Economic Zones (SEZ) program, administered by the Bangladesh Economic Zones Authority (BEZA), presents a high-value and rapidly expanding demand source for construction chemicals. As of 2024, BEZA had operationalized over 12 economic zones across the country and was actively developing more than 80 additional zones, each requiring substantial industrial construction, including heavy-duty flooring compounds, chemical-resistant sealants, corrosion-resistant protective coatings, and industrial-grade adhesives.

The Bangladesh Export Processing Zones Authority (BEPZA) has similarly reported ongoing expansion of garment and light manufacturing facilities that depend on specialty flooring and moisture-barrier solutions. This industrial infrastructure wave is directly aligned with the Government of Bangladesh's Vision 2041 roadmap to transition to a developed-nation status, a vision that necessitates world-class industrial facilities built with internationally certified chemical products, a demand opportunity that premium construction chemical companies are uniquely positioned to capture.

Category-wise Analysis

Product Type Insights

Concrete Admixtures represent the dominant product segment in the Bangladesh construction chemicals market, capturing approximately 39% of total market revenue in 2026. This leadership position is firmly anchored in the segment's indispensable role across all scales of construction, from high-volume infrastructure concrete pours to precision residential formwork applications. Within the admixtures sub-category, Polycarboxylate Ether (PCE)-based plasticizers have emerged as the fastest-growing product type, owing to their superior water-reduction efficiency, workability enhancement, and compatibility with blended cements widely used in Bangladesh under the Bangladesh National Building Code (BNBC).

The government's mandate to upgrade over 30,000 kilometers of road network under successive Five Year Plans has institutionalized the use of high-performance concrete across public works, driving consistent and large-volume admixture procurement. Leading multinational players including SIKA AG, Master Builder Solutions, and Fosroc International have strategically broadened their Bangladesh admixture portfolios in response to this demand concentration, further reinforcing the segment's dominance.

Application Insights

The Infrastructure segment leads the Bangladesh construction chemicals market by application, accounting for approximately 42% of total market share in 2026. This dominance reflects the central role of government-financed infrastructure development in driving nationwide chemical product demand. Signature projects such as the Padma Multipurpose Bridge, the Karnaphuli Tunnel, the Matarbari Ultra-Super-Critical Coal Power Plant, the Hazrat Shahjalal International Airport expansion, and the ongoing Dhaka–Chittagong Highway widening have collectively consumed vast quantities of structural waterproofing compounds, high-performance admixtures, and durable protective coatings.

The Bangladesh Planning Commission has consistently allocated the largest share of Annual Development Programme budgets to the transport and energy infrastructure sectors, sustaining a predictable and large-scale chemical procurement pipeline. Infrastructure projects also serve as the primary entry point for multinational construction chemical companies seeking market foothold in Bangladesh, as government tender specifications typically mandate internationally certified and laboratory-tested chemical formulations, concentrating revenue in this segment.

Competitive Landscape

The Bangladesh construction chemicals market is moderately consolidated at the premium tier, with a cluster of multinational companies, including SIKA AG, Master Builder Solutions, MAPEI, and Pidilite Industries, commanding significant share through superior product certification, technical service capabilities, and established distribution networks. Regional players such as Chembond Chemicals Limited and CICO Technologies Limited compete competitively in mid-tier and value segments.

Key differentiators among market leaders include alignment with Bangladesh National Building Code (BNBC) standards, on-ground technical support teams, and contractor training programs. Companies are increasingly investing in local blending and packaging facilities to reduce logistics costs and buffer against import volatility. Co-specification with engineering consultants and project developer partnerships are emerging as decisive competitive business model trends.

Key Market Developments

- In January 2025, SIKA AG announced the strategic expansion of its Bangladesh distribution network through a new partnership with a leading Dhaka-based construction materials distributor, targeting enhanced penetration across public infrastructure project procurement channels and Tier-2 city markets.

- In March 2024, Pidilite Industries launched a new range of fiber-reinforced waterproofing membranes under the Dr. Fixit brand, specifically engineered for South Asian tropical climate conditions, with field validation trials conducted across active construction sites in Dhaka and Chittagong.

- In October 2023, MAPEI Construction Products India Pvt. Ltd. extended its Bangladesh product portfolio with the introduction of high-strength tile adhesives and grouts compliant with ISO 13007 standards, targeting the growing premium commercial flooring and facade renovation segment.

Companies Covered in Bangladesh Construction Chemicals Market

- Chembond Chemicals Limited

- Master Builder Solutions

- SIKA AG

- The Dow Chemical Company

- Pidilite Industries

- Fosroc International

- MAPEI Construction Products India Pvt. Ltd.

- Flowcrete India Ltd

- CICO Technologies Limited

- MYK LATICRETE India

- Ardex Endura

- KERAKOLL India Pvt. Ltd

- Akzo Nobel NV

- RPM International Inc.

- Saint-Gobain S.A.

Frequently Asked Questions

The Bangladesh Construction Chemicals market was valued at US$ 273.6 million in 2026 and is projected to reach US$ 487.5 million by 2032, expanding at a forecast CAGR of 8.6% over the period 2026 to 2033.

The primary growth drivers are the government's sustained public infrastructure investment under the Annual Development Programme (ADP), including projects like the Dhaka Metro Rail and Padma Bridge, rapid urbanization generating residential construction demand, and the ongoing expansion of Special Economic Zones under BEZA, each requiring high-performance chemical formulations.

Concrete Admixtures lead the product type segment with approximately 39% market share in 2026. Within this category, PCE-based plasticizers are the fastest-growing sub-segment, driven by mandatory high-performance concrete specifications in government infrastructure projects and growing compliance requirements under the Bangladesh National Building Code (BNBC).

The principal market opportunity lies in developing and supplying green and sustainable construction chemicals aligned with LEED, EDGE, and Bangladesh's national climate adaptation commitments. Multilateral funding from the Asian Development Bank and the World Bank for eco-compliant infrastructure in Bangladesh is creating structured demand for low-VOC, bio-based, and environmentally certified chemical products, offering higher margins and long-term contracts.

The leading companies include SIKA AG, Master Builder Solutions, Pidilite Industries, Fosroc International, MAPEI Construction Products India Pvt. Ltd., Chembond Chemicals Limited, CICO Technologies Limited, MYK LATICRETE India, Ardex Endura, Akzo Nobel NV, RPM International Inc., and Saint-Gobain S.A., among others operating across product and application segments.