- Specialty & Fine Chemicals

- Construction Chemicals Market

Construction Chemicals Market Size, Share, and Regional Forecast for 2026 - 2033

Construction Chemicals Market by Product Type (Concrete Admixture, Water Proofing Chemicals, Protective Coating, and Others), Application, and Regional Analysis for 2026 - 2033

Construction Chemicals Market Share and Trends Analysis

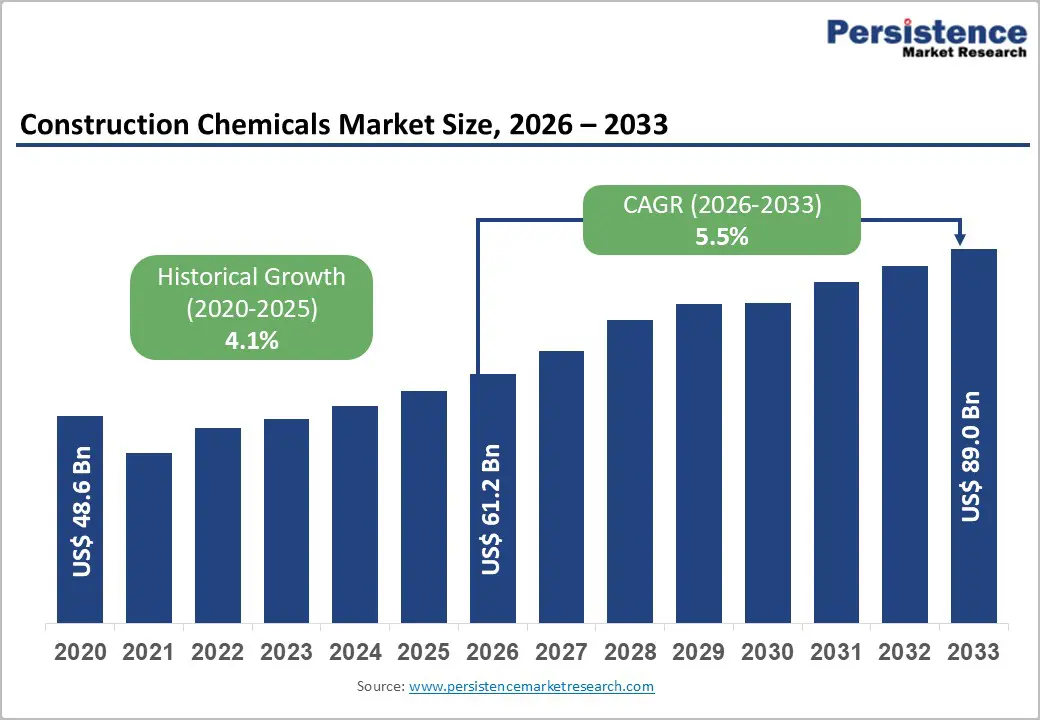

The global construction chemicals market size is projected to expand at a steady CAGR of 5.5% from 2026 to 2033, increasing from US$ 61.2 billion in 2026 to US$ 89.0 billion by 2033.

This growth is primarily driven by rising demand for high-performance, durable, and sustainable construction materials across residential, commercial, and infrastructure sectors. Robust infrastructure development and urbanization, increasing investment in smart city and infrastructure projects, and the growing adoption of precast and modular construction techniques are significantly contributing to market expansion.

Key Industry Highlights:

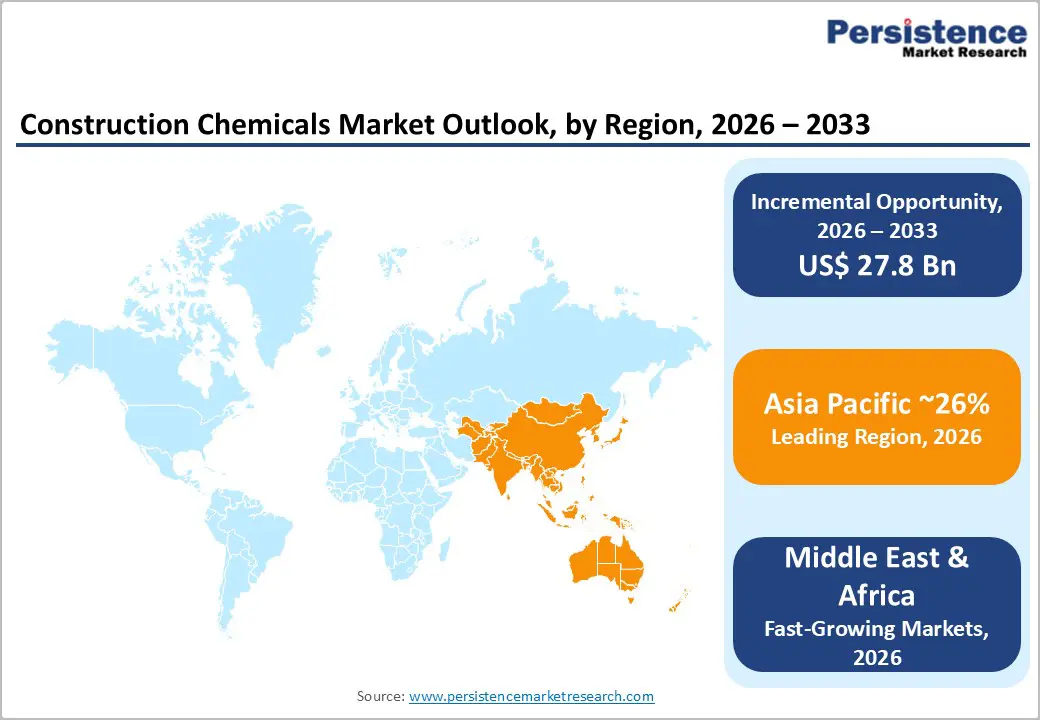

- Leading Region: Asia Pacific to account for 25% market share in 2026, amid robust urbanization and mega-infrastructure projects, driving market growth.

- Fastest Growing Region: Middle East and Africa are emerging as a fast-growing market driven by urbanization and infrastructure development.

- Leading Product Type: Waterproofing Chemicals to dominate, while concrete admixtures emerge as the fastest-growing product type

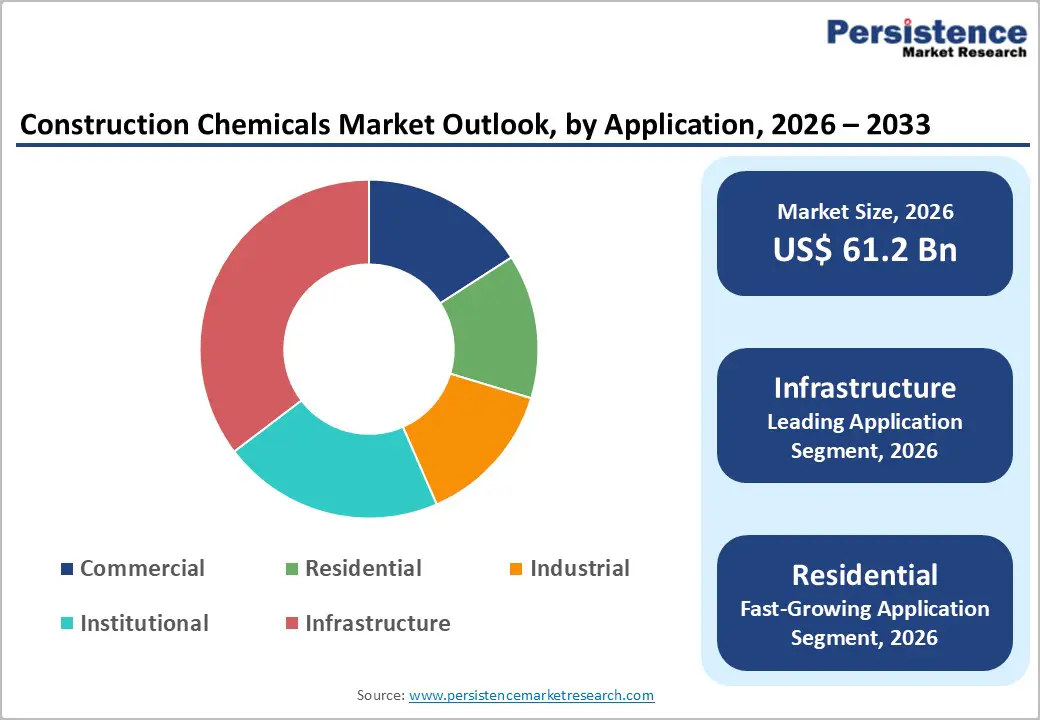

- Leading Application: Infrastructure segment is expected to dominate the global construction chemicals market, capturing an estimated 28% market share.

- Growth Indicator: Rapid urbanization and infrastructure development are driving demand for construction chemicals.

| Key Insights | Details |

|---|---|

| Construction Chemicals Market Size (2026E) | US$ 61.2 Bn |

| Projected Market Value (2033F) | US$ 89.0 Bn |

| Global Market Growth Rate (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth Rate (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Drivers - Rapid Urbanization and Infrastructure Mega-Projects Fueling Market Expansion

The global construction chemicals market is experiencing unprecedented growth driven by accelerating urbanization and massive infrastructure investments, particularly in the Asia-Pacific region where cities are projected to represent 60% of the world's urban population by 2050. Developing countries in Asia and the Pacific require infrastructure investments totaling $26 trillion from 2016 to 2030, equivalent to $1.7 trillion annually, to accommodate the projected addition of hundreds of millions of urban residents.

China's substantial commitment to infrastructure includes significant funding for transportation networks, renewable energy systems, water infrastructure, and smart urbanization initiatives, while prioritizing green building practices and energy efficiency in all construction activities. India's ambitious National Infrastructure Pipeline allocates funding for critical transport corridors, energy networks, and affordable housing programs targeting 20 million homes, creating sustained demand for high-performance admixtures, waterproofing compounds, and repair mortars.

Urban concentration in mega-cities like Tokyo, New Delhi, and Shanghai reinforces the region's position as a center of global growth and innovation, attracting cross-border investment into mixed-use developments, logistics hubs, and transit-oriented projects that require specialty construction chemicals capable of withstanding heavy loads and environmental exposure. Infrastructure spending has emerged as one of the strongest drivers of urban development across the Asia-Pacific, with governments actively incentivizing development through special economic zones, regional infrastructure corridors, and targeted tax incentives that stimulate construction activity in both primary and secondary cities.

Sustainability Mandates and Green Chemistry Innovation: Transforming Product Demand

The transition toward sustainable construction practices represents a transformative driver for the global construction chemicals market, propelled by stringent environmental regulations and green building certification standards such as LEED and BREEAM that mandate low-VOC and eco-certified construction materials. LEED certification programs have established concentration limits for formaldehyde, 4-phenylcyclohexene, and total volatile organic compounds based on pre-occupancy sampling, with updated 2013 standards expanding the regulated VOC list to 33 compounds to ensure improved indoor air quality and occupant health protection. New construction projects increasingly undergo VOC testing prior to occupancy to verify that materials qualify as "low-emitting," with green buildings designed to protect occupant health and comfort through strict adherence to air quality criteria.

South Korea is reinforcing its carbon neutrality goals by implementing stricter green construction standards that advance sustainable development, while China prioritizes green building practices and energy efficiency across all infrastructure projects. The regulatory landscape governing bio-based materials continues to evolve, with building codes being updated to incorporate performance-based standards that accommodate the unique characteristics of sustainable materials rather than rigidly adhering to prescriptive requirements designed for conventional products. Environmental compliance requirements now extend beyond VOC limits to encompass life cycle assessment reporting that verifies carbon footprint reduction, transparency in sourcing and manufacturing processes, and alignment with LEED certification points for bio-based construction materials.

Restraint Stringent Environmental Regulations and Compliance Challenges Hinder Market Growth

Stringent environmental regulations and compliance challenges are significantly affecting the global construction chemicals market. Key regulations, such as the European Union’s REACH and the U.S. Environmental Protection Agency’s VOC emission limits, require the reformulation of critical products like adhesives, sealants, and coatings to decrease harmful emissions. This often results in increased production costs, up to 25%, as low-VOC or bio-based chemicals demand expensive raw materials and advanced processing techniques. Non-compliance can lead to severe penalties or market bans, particularly in Europe and North America, where oversight is strict. In 2023, the EU heightened its chemical safety standards, requiring detailed environmental impact data, which strains smaller companies with limited resources.

While leading manufacturers like Fosroc and Saint-Gobain are making substantial investments in compliance, Fosroc introduced eco-friendly waterproofing solutions in 2023, and Saint-Gobain acquired Chryso in 2021; these measures can drive up product prices, hindering adoption in cost-sensitive markets. This regulatory burden stifles innovation and limits market expansion, particularly for small manufacturers that struggle to manage compliance costs, ultimately restraining overall market growth. Addressing these challenges is essential for fostering a sustainable and competitive industry.

Opportunity - Rising demand for green building certifications creates opportunities for eco-friendly construction chemicals

The increasing demand for green building certifications, such as LEED and BREEAM, is creating significant opportunities for the global construction chemicals market, as developers prioritize eco-friendly materials to meet sustainability goals. With the construction sector accounting for approximately 39% of global carbon emissions, according to the International Energy Agency, governments and consumers are pushing for low-carbon, energy-efficient buildings. Eco-friendly construction chemicals, including low-VOC adhesives, bio-based sealants, and sustainable concrete admixtures, are critical for achieving these certifications, which enhance property value and appeal.

Saint-Gobain’s acquisitions of FOSROC in June 2025 and Ovniver Group in August 2025 strengthen its portfolio of sustainable solutions, with FOSROC’s eco-friendly waterproofing systems gaining traction in India’s green residential projects. Thermax’s October 2025 acquisition of Buildtech Products India Private Limited bolsters its offerings in low-carbon admixtures for infrastructure, aligning with India’s sustainability mandates. These strategic initiatives reflect manufacturers’ focus on developing products that reduce environmental impact while meeting regulatory standards like the EU’s REACH framework. By expanding production of bio-based and recycled-content chemicals, companies can capture market share in regions with strong green building policies, such as Asia-Pacific and Europe, and cater to the growing consumer preference for sustainable construction, driving long-term growth and profitability.

Advancement of Smart and Self-Healing Construction Materials

The development and commercialization of smart construction materials, particularly self-healing concrete and nano-engineered formulations, presents a significant growth opportunity for construction chemicals manufacturers. Self-healing bio-concrete incorporates specialized bacterial strains such as Bacillus subtilis that remain dormant within the concrete mix until cracks form and moisture activates them, triggering consumption of nutrients and conversion into calcium carbonate that naturally fills and repairs fractures while restoring structural integrity. This microbial-induced carbonate precipitation (MICP) technology enables concrete to autonomously perceive and heal cracks through bio-mineralization processes, with bacteria encapsulated in expanded perlite particles that provide protective environments against high pH levels while enabling deeper crack healing compared to surface-level treatments.

Nanotechnology integration further enhances self-healing performance through graphite nanoplatelets that uniformly deliver curing agents and nanocomposite sensors using carbon fiber, multi-wall carbon nanotubes, and graphene as conductive fillers that convert applied strain into electrical resistance variations. Smart concrete embedded with piezoelectric sensors and fiber optic sensors enables real-time structural health monitoring by detecting and transmitting continuous data on strain, temperature, and crack formation, allowing early detection of structural failures, reducing maintenance costs, and extending infrastructure lifespan without compromising mechanical properties. The integration of 3D concrete printing technology creates additional opportunities, with researchers developing printable concrete mixes that use 30% less material compared to conventional construction while achieving compressive strengths exceeding 50 megapascals.

Category-wise Insights

Product Type Insights

Based on product type, waterproofing chemicals are expected to account for nearly 21% share of the global construction chemicals market in 2026, owing to their essential role in enhancing the durability, safety, and structural integrity of buildings and infrastructure. These chemicals are widely used in rooftops, basements, tunnels, water tanks, and other critical structures to prevent water ingress, which can lead to corrosion, weakening of concrete, and costly repairs. Their versatility, available in forms such as membranes, coatings, and crystalline compounds, makes them indispensable in modern construction practices.

The concrete admixtures segment is projected to be the fastest-growing product category and is expected to create a million-dollar absolute opportunity from 2026 to 2033. These admixtures, ranging from plasticizers and superplasticizers to accelerators and retarders, are designed to modify the properties of concrete during mixing, curing, and setting, resulting in improved strength, workability, and durability. Innovations in admixture formulations that support low-carbon and high-strength concrete are attracting significant market interest, especially in developed regions and environmentally conscious markets.

Application Insights

In 2026, the infrastructure segment is expected to dominate the global construction chemicals market, capturing an estimated 26% market share, driven by large-scale public and private sector investments in transportation, energy, and water management systems. Governments across developed and emerging economies are prioritizing infrastructure modernization, including roads, bridges, tunnels, railways, and airports, which require substantial volumes of construction chemicals such as concrete admixtures, waterproofing systems, sealants, and repair materials.

The residential segment is projected to experience the highest growth rate, with a compound annual growth rate (CAGR) of 6.6% from 2026 to 2033. This growth is attributable to rising urbanization, population growth, and increased housing demand, particularly in rapidly developing countries across the Asia-Pacific, Africa, and Latin America.

Country-wise Insights

Asia Pacific Construction Chemicals Market Trends

The Asia-Pacific region is expected to lead the construction chemicals market, driven by rapid urbanization, infrastructure expansion, and the development of industrial facilities. The region is expected to account for nearly a 25% share of the global market in 2026. Rising urban populations in countries such as China, India, and Southeast Asia are expected to increase the demand for roads, bridges, metro systems, utilities, and high-rise commercial buildings.

Major initiatives like China's Belt and Road projects, India's Smart Cities Mission, and ASEAN's smart infrastructure upgrades are key factors supporting the market growth. For example, India’s infrastructure spending is projected to reach approximately 3.3% of GDP in 2025 and continues to rise with ongoing projects in highways, metros, and affordable housing. These trends are positioning Asia-Pacific as a key market for the construction chemicals industry, with strong demand for products like concrete admixtures, waterproofing agents, and repair materials.

North America Construction Chemicals Market Trends

North America's construction chemicals market is experiencing steady growth, fueled by a well-established construction industry and increasing emphasis on sustainable and high-performance building practices. The ongoing wave of residential renovations and new home constructions continues to support demand for tile adhesives, sealants, waterproofing solutions, and concrete admixtures. In 2025, the total value of construction put in place in the United States reached an estimated US$ 2.1 trillion, marking a 6.5% increase over 2023.

The North American construction industry is significantly influenced by green building standards, such as LEED and Energy Star, which are encouraging contractors and developers to adopt eco-friendly construction chemicals that have low VOC emissions and improved durability. Robust increases in mega infrastructure projects, such as highway rehabilitation, airport upgrades, and smart city initiatives, are being driven by both federal funding (e.g., the U.S. Infrastructure Investment and Jobs Act) and private sector investment is also expected to drive the North American construction chemicals market.

Middle East and Africa Construction Chemicals Market Trends

The Middle East and Africa (MEA) region is projected to emerge as one of the most promising markets for construction chemicals, driven by increasing urbanization, population growth, and robust infrastructure investment. In 2025, the Gulf Cooperation Council (GCC) countries awarded construction contracts worth US$ 273 billion, marking a 9.6% increase from 2023 and signaling strong market recovery and investor confidence.

Saudi Arabia led this surge, accounting for 53.8% of the total GCC awards with US$ 146.8 billion in contracts, driven largely by its ambitious Vision 2030 agenda and transformative mega-projects such as NEOM, The Line, and Red Sea Global. With rising awareness of energy efficiency and environmental standards, there is growing traction for sustainable, energy-saving solutions, such as cool roof coatings and low-emission adhesives. While the market is still developing in parts of Africa, key manufacturers are expanding operations and forming local partnerships to tap into this high-potential region.

Competitive Landscape

The global construction chemicals market is moderately fragmented, with the presence of Tier I, Tier II, and Tier III players competing across various segments. Leading companies such as Sika AG, Saint-Gobain, Mapei, The 3M Company, and Pidilite Industries collectively hold around 30–35% of the global market share.

These key players are focused on strategic acquisitions, regional expansion, R&D investment, and sustainability to strengthen their market positions in emerging regions. Key trends among competitors include the development of eco-friendly and high-performance products, digitalization of technical services, and integrated solutions aimed at enhancing construction efficiency and long-term durability.

Recent Industry Developments

- In January 2026, Saint-Gobain has established a joint venture with a subsidiary of Indocement Tunggal Prakarsa, an Indonesia-based, publicly listed cement producer majority owned (53%) by Heidelberg Materials, to acquire Indocement’s mortars business in Indonesia. Under the agreement, Saint-Gobain will hold a 60% stake in the joint venture, while Indocement Tunggal Prakarsa will own the remaining 40%.

- In October 2025, Bigbloc Construction Limited announced its foray into the construction chemicals segment. The company currently offers block jointing mortar and ready mix plaster through white labeling under the brands Nxtfix and Nxtplast. With plans to introduce tile adhesives under the new brand Nxtgrip, Bigbloc is aiming to diversify its product portfolio and tap into the growing demand in India’s construction and renovation market.

- In September 2025, MBT Construction Chemicals, part of the Master Builders Solutions Group, has inaugurated a new state-of-the-art manufacturing facility in Taloja, Navi Mumbai, India. The plant offers an annual single-shift capacity of 25,000 metric tons and 300 tons of storage, producing admixtures, waterproofing solutions, grouts, flooring systems, repair mortars, and protective coatings.

Companies Covered in Construction Chemicals Market

- Sika AG

- Saint Gobain

- The 3M Company

- MAPEI S.p.A.

- Arkema Group

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Ashland Inc.

- Dow Chemical Company

- Pidilite Industries Limited

- SCG Chemicals

- RPM International Inc.

- Thermax Limited

- Evonik Industries

- LATICRETE International, Inc.

Frequently Asked Questions

The global construction chemicals market is projected to be valued at US$ 61.2 Bn in 2026.

Key growth drivers include rising demand for high-performance, durable, and sustainable construction materials across residential, commercial, and infrastructure sectors.

The construction chemicals market is poised to witness a CAGR of 5.5% from 2026 to 2033.

Rising Demand for green building certifications creates opportunities for eco-friendly construction chemicals.

Major players in the construction chemicals market include Sika AG, Saint Gobain, Mapei, The 3M Company, Arkema Group, and others.