- Transportation & Logistics

- Cold Chain Market

Cold Chain Market Size, Share, and Growth Forecast, 2025 - 2032

Cold Chain Market by Product Type (Storage [Facilities/Services {Refrigerated Warehouse (Private & Semi-Private, Public), Cold Room}, Equipment {Blast Freezer, Walk-in Cooler and Freezer, Deep Freezer, Others}], Transportation [By Mode {Road, Sea, Rail, Air}, By Offering {Refrigerated Vehicles, Refrigerated Container}]), Equipment, Application, and Regional Analysis for 2025 - 2032

Cold Chain Market Size and Trend Analysis

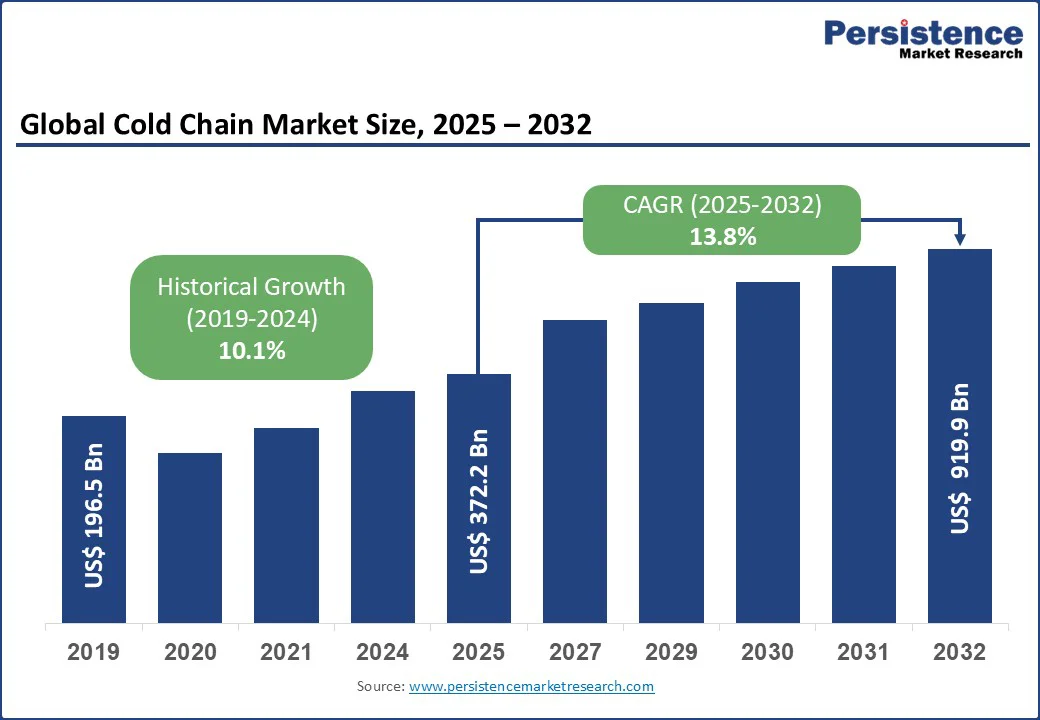

The global cold chain market size is likely to be valued at US$372.2 Bn in 2025. It is expected to reach US$919.9 Bn by 2032, growing at a CAGR of 13.8% during the forecast period from 2025 to 2032, driven by increasing demand for perishable goods, pharmaceuticals, and processed foods, where temperature-controlled logistics are critical.

Key Industry Highlights:

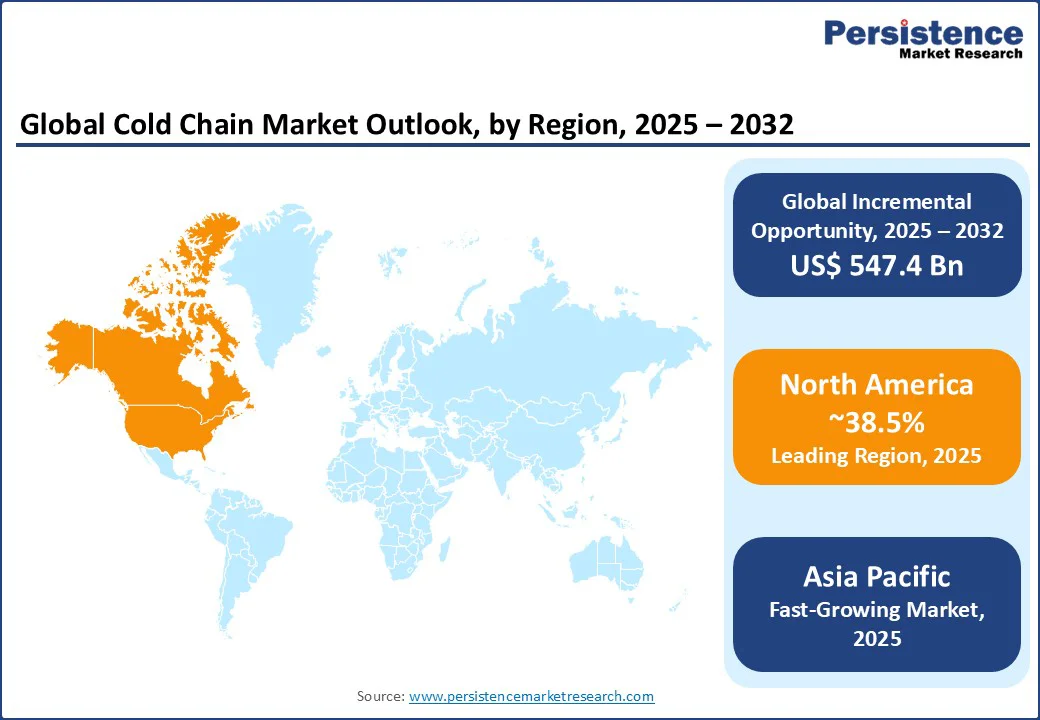

- Leading Region: North America is likely to hold a 38.5% share in 2025, propelled by advanced infrastructure, stringent regulations, and high demand for pharmaceuticals and processed foods in the U.S. and Canada.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by rapid urbanization, expanding food retail, and increasing healthcare investments in China and India.

- Investment Plans: China’s 14th Five-Year Plan (2021 - 2025) emphasizes cold chain infrastructure development, targeting 100 national cold chain logistics bases and creating a network that links production and sales areas.

- Dominant Product Type: Storage accounts for nearly 51.8% of the Cold chain market share, due to the critical role of refrigerated warehouses in food and pharmaceutical logistics.

| Key Insights | Details |

|---|---|

| Cold Chain Market Size (2025E) | US$ 372.2Bn |

| Market Value Forecast (2032F) | US$ 919.9Bn |

| Projected Growth (CAGR 2025 to 2032) | 13.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 10.1% |

Market Dynamics

Driver: Growing Demand for Perishable Goods and Pharmaceuticals Fuels Market Expansion

The global cold chain market is experiencing robust growth, driven by the rising demand for perishable food items and temperature-sensitive pharmaceuticals. Cold chain logistics play a crucial role in preserving the integrity and quality of products such as fresh produce, dairy, meat, and vaccines, all of which require precise temperature control and adherence to strict safety standards.

According to the Food and Agriculture Organization (FAO), global food trade reached $1.8 trillion in 2023, with a substantial portion involving perishable goods.

In North America, the pharmaceutical sector, particularly in the U.S., relies extensively on cold chain infrastructure for efficient vaccine storage and distribution. United States cold storage, for example, reported sales increases in 2024, reflecting this growing demand.

Government initiatives such as India’s National Cold Chain Development Program are bolstering infrastructure and capacity. Rising consumer preference for fresh and organic foods & beverages is further fueling demand, ensuring continued market expansion through 2032.

Restraint: High Operational Costs and Energy Consumption Challenges

The cold chain market, while growing, faces several significant challenges that can hinder its long-term expansion. One of the primary concerns is the high operational cost associated with maintaining temperature-controlled environments. Cold storage facilities rely on energy-intensive equipment, such as blast freezers, refrigerated warehouses, and temperature-controlled transport vehicles, which drive up electricity consumption and increase overhead expenses.

These costs can be particularly burdensome in regions with high energy prices or unreliable power supply. Moreover, the environmental impact of cold chain operations is a growing concern, as refrigeration systems contribute to greenhouse gas emissions, prompting scrutiny from regulators and sustainability-conscious stakeholders.

In developing regions such as parts of Africa and South Asia, limited infrastructure, inadequate investment, and logistical hurdles further restrict cold chain adoption. Additionally, competition from more flexible or cost-effective logistics options, such as air freight for durable goods, challenges the cold chain market's growth potential, especially in price-sensitive markets where cold chain investment may not yield immediate returns.

Opportunity: Rising Investments in Sustainable Cold Chain Technologies

The growing emphasis on sustainability and green technologies is unlocking substantial opportunities within the cold chain market. Energy-efficient refrigeration innovations, including solar-powered cold boxes and eco-friendly refrigerants, are increasingly being adopted to reduce carbon footprints and operational costs.

The International Energy Agency’s Renewables 2024 report projects that approximately 5,500 GW of new renewable energy capacity will be added globally between 2024 and 2030, creating a supportive environment for off-grid and hybrid cold chain solutions.

In the pharmaceutical sector, companies such as Sonoco ThermoSafe are pioneering sustainable packaging designed to maintain temperature integrity while minimizing environmental impact, aligning with stricter global regulations.

Furthermore, government initiatives such as the European Union’s Green Deal and India’s renewable energy programs are driving investments into green cold chain infrastructure, offering financial incentives and policy support. Together, these trends are encouraging manufacturers to innovate eco-friendly, cost-effective cold chain solutions, ensuring resilience and compliance in a rapidly evolving market through 2032.

Category-wise Insights

By Product Type

- Storage holds the largest market share, approximately 51.8% in 2025, due to the critical role of refrigerated warehouses and cold rooms in preserving perishable goods and pharmaceuticals. These facilities ensure product integrity across food and healthcare supply chains, with companies such as Americold Logistics and LINEAGE LOGISTICS HOLDING, LLC leading in advanced storage solutions for North America and Europe.

- Transportation is the fastest-growing segment, driven by the rising demand for refrigerated vehicles and containers to support global food trade and vaccine distribution. Companies such as A.P. Moller - Maersk are expanding refrigerated container offerings, particularly in the Asia Pacific, to meet the needs of cross-border perishable goods logistics.

By Equipment

- Transportation holds the largest market share, accounting for around 60.4% of the cold chain market in 2025, driven by the rising demand for refrigerated trucks, reefer containers, and solar-powered transport units to support global food trade and vaccine distribution. Companies such as A.P. Moller - Maersk are expanding their refrigerated container offerings, especially in the Asia Pacific region, to meet the growing needs of cross-border cold chain logistics and last-mile delivery of temperature-sensitive goods.

- Storage is the fastest-growing segment, due to the critical role of refrigerated warehouses, walk-in coolers, freezers, and cold rooms in preserving perishable goods and pharmaceuticals. These facilities ensure product integrity across food and healthcare supply chains, with companies such as United States Cold Storage and NewCold leading in advanced on-grid and off-grid storage solutions for North America, Europe, and developing regions.

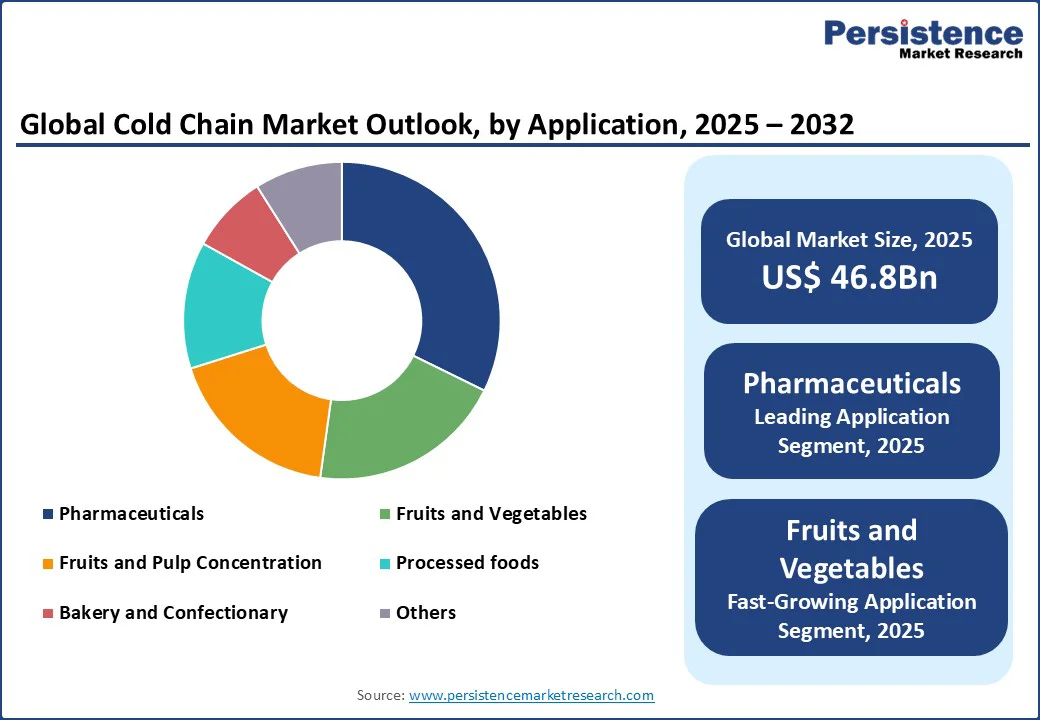

By Application

- Pharmaceuticals account for over 32.4% of market revenue in 2025, driven by the global demand for vaccines and biologics. Cold chain logistics ensure the safe storage and transportation of temperature-sensitive drugs, with companies such as United Parcel Service of America, Inc. leading in vaccine distribution across North America and Europe.

- Fruits and vegetables are the fastest-growing segment, propelled by increasing global food trade and consumer demand for fresh produce. The Asia Pacific region, particularly China and India, drives this growth, with players such as Burris Logistics expanding cold storage networks to support agricultural supply chains.

Regional Insights

North America Cold Chain Market Trends

North America leads the global cold chain market, holding a significant 38.5% share in 2025, primarily due to strong demand from the pharmaceutical and food retail sectors across the U.S. and Canada.

The region benefits from highly advanced cold chain infrastructure, including state-of-the-art refrigerated warehouses and transportation networks that are crucial for the safe distribution of vaccines, biologics, and perishable foods. In the U.S., the cold chain’s importance is underscored by its vital role in vaccine distribution, ensuring temperature-sensitive drugs reach their destinations without compromising efficacy.

Canada’s robust agriculture sector fuels demand for cold storage solutions, with the Canadian Food Inspection Agency emphasizing the need for stringent temperature controls to maintain food safety and quality.

Industry leaders such as Americold Logistics and United States Cold Storage dominate the cold chain market with expansive facilities and integrated logistics services. Additionally, evolving consumer preferences for fresh, high-quality foods and strict regulatory standards continue to bolster North America’s dominant position in the cold chain industry.

Asia Pacific Cold Chain Market Trends

The Asia Pacific region is emerging as the fastest-growing market in the global cold chain industry, driven by rapid urbanization, expanding food retail sectors, and increasing healthcare investments, particularly in China and India. China, recognized as the world’s largest food market by the Food and Agriculture Organization (FAO), plays a pivotal role in cold chain demand, fueled by a rising middle class and the surge in e-commerce food sales, which require reliable temperature-controlled logistics.

India’s cold chain sector is witnessing robust growth supported by government initiatives such as the National Cold Chain Development Program, which aims to reduce post-harvest losses and enhance refrigerated warehousing infrastructure.

The pharmaceutical industry in the region, coupled with a strong agricultural base, further amplifies demand for cold chain solutions. Leading companies such as NICHIREI CORPORATION are expanding their footprint to capitalize on these opportunities. Continuous consumer preference for fresh, safe foods and large-scale government infrastructure investments are expected to sustain the Asia Pacific’s rapid cold chain market growth through 2032.

Europe Cold Chain Market Trends

Europe stands as the second fastest-growing region in the global cold chain market, propelled by stringent regulatory frameworks, increasing demand in pharmaceuticals and food retail, and significant infrastructure investments, particularly in Germany and France.

The European cold chain industry plays a vital role in supporting refrigerated storage and transportation, ensuring product safety and quality across the supply chain. Germany’s robust pharmaceutical sector is a major driver of cold chain demand, with leading logistics providers such as A.P. Moller - Maersk offering specialized temperature-controlled solutions to meet the sector’s exacting standards.

The European Union’s Green Deal further accelerates growth by promoting sustainable cold chain technologies, encouraging the adoption of energy-efficient refrigeration systems and reducing carbon footprints.

Europe’s commitment to regulatory compliance, combined with a growing consumer preference for fresh, high-quality products, is pushing companies to innovate continuously. This focus on sustainability and compliance is expected to sustain Europe’s strong market growth trajectory through the coming decade.

Competitive Landscape

The global cold chain market is highly competitive, characterized by a fragmented landscape with numerous domestic and international players. Leading companies such as Americold Logistics, LINEAGE LOGISTICS HOLDING, LLC, and United States Cold Storage dominate through extensive storage networks and advanced technologies.

Regional players such as NICHIREI CORPORATION focus on localized offerings in the Asia Pacific. Companies are investing in energy-efficient systems and sustainable solutions to enhance market share, driven by demand for high-performance cold chain logistics in the food and pharmaceutical sectors.

Key Industry Developments

- March 2025: Americold Logistics announced the acquisition of a state-of-the-art automated refrigerated warehouse in Russellville, Arkansas. This facility, standing 140 feet tall and spanning 136,000 square feet, is equipped with advanced automation technologies, including an Automated Storage and Retrieval System (ASRS), ammonia refrigeration, and energy-efficient systems.

- September 2024: Maersk Container Industry (MCI) introduced the Star Cool 1.1, a triple refrigerant reefer cooling machine designed to promote sustainable global cold chains. This innovative unit offers adaptability to three alternative refrigerants, including the climate-friendly R1234yf, which boasts an ultra-low Global Warming Potential (GWP).

Companies Covered in Cold Chain Market

- Americold Logistics, Inc.

- LINEAGE LOGISTICS HOLDING, LLC

- United States Cold Storage

- Burris Logistics

- Wabash National Corporation

- NewCold

- Sonoco ThermoSafe (Sonoco Products Company)

- United Parcel Service of America, Inc.

- A.P. Moller - Maersk

- NICHIREI CORPORATION

- Tippmann Group

- Others

Frequently Asked Questions

The Cold Chain market is projected to reach US$372.16 Bn in 2025.

Growing demand for perishable goods and pharmaceuticals, and advancements in refrigeration technologies are the key market drivers.

The Cold Chain market is poised to witness a CAGR of 13.8% from 2025 to 2032.

The rising investments in sustainable cold chain technologies are the key market opportunity.

Americold Logistics, LINEAGE LOGISTICS HOLDING, LLC, United States Cold Storage, and A.P. Moller - Maersk are key market players.