- Specialty & Fine Chemicals

- Cold Flow Improvers Market

Cold Flow Improvers Market Size, Share, and Growth Forecast 2026 - 2033

Cold Flow Improvers Market by Product Type (Ethylene-Vinyl Acetate (EVA) Based, Polymer-Based, Succinic Acid Ester Based, Acrylic Ester Based, Others), Fuel Type (Diesel Fuel, Biodiesel & Biofuel Blends, Heating Oil, Jet Fuel, Marine Fuel), End-user (Automotive, Aviation, Marine, Industrial, Residential & Commercial Heating, Agriculture), and Regional Analysis, 2026 - 2033

Cold Flow Improvers Market Size and Trend Analysis

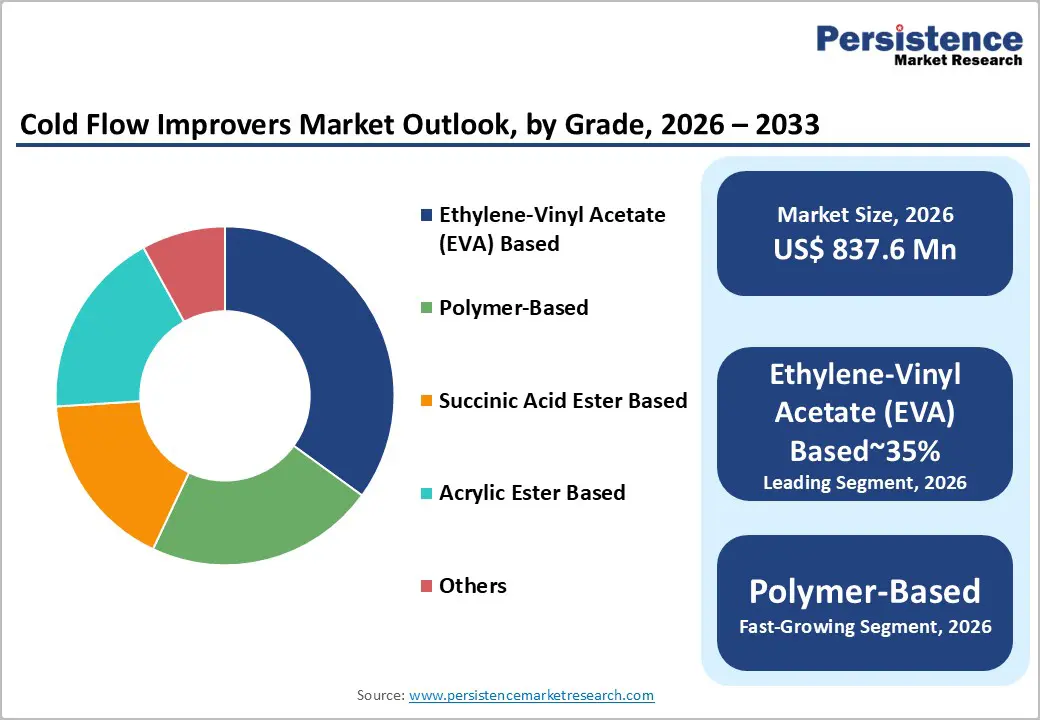

The global cold flow improvers market is projected to reach US$ 837.6 million in 2026 and US$ 1,242.9 million by 2033, growing at a CAGR of 5.8% over the forecast period. Market growth is driven by increasing demand for improved fuel performance in the automotive, aviation, and marine sectors operating in cold climates.

Key Industry Highlights:

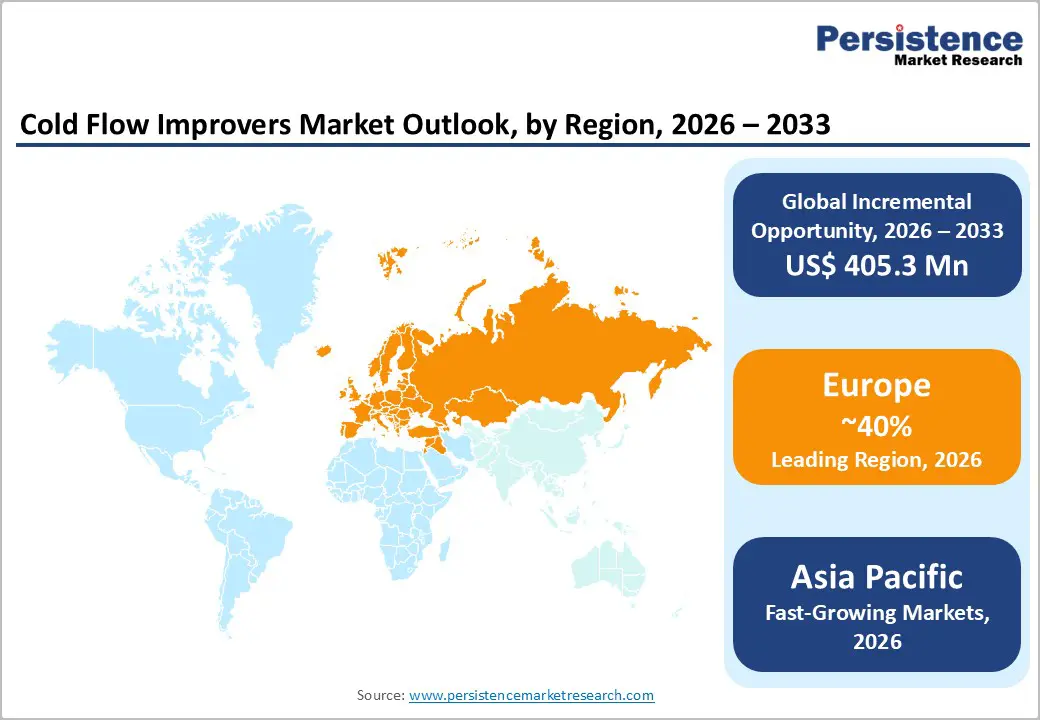

- Leading Region: Europe dominates the global cold flow improvers market, accounting for the largest share of revenue due to stringent EN 590 fuel quality standards, extensive geographic coverage of cold climates, and harmonized regulatory frameworks that sustain demand for premium additive solutions across diverse applications.

- Fastest Growing Region: Asia Pacific exhibits the highest growth trajectory, particularly driven by China's 63.5% East Asia market share, government renewable energy initiatives, rapid industrialization, and aggressive biodiesel expansion, creating substantial opportunities for regional and international manufacturers.

- Dominant Segment: Ethylene-Vinyl Acetate (EVA) based cold flow improvers command approximately 35% market share among polymer formulations, representing proven technology with established compatibility across fuel types and strong sales momentum increasing 33.5% versus the 2019 baseline.

- Fastest Growing Segment: Polymer-based cold flow improvers, particularly polymethacrylate formulations, demonstrate accelerating adoption rates reflecting performance advantages, improved thermal performance range, and regulatory compliance supporting premium positioning in competitive markets.

- Key Market Opportunity: Biodiesel cold-flow improver development for emerging Asia-Pacific markets, particularly customized formulations that optimize palm oil-based biodiesel performance and support Indonesia's 7.8% CAGR market growth through 2030, represents the highest-potential revenue opportunity.

| Key Insights | Details |

|---|---|

|

Cold Flow Improvers Market Size (2026E) |

US$ 837.6 Million |

|

Market Value Forecast (2033F) |

US$ 1,242.9 Million |

|

Projected Growth CAGR (2026-2033) |

5.8% |

|

Historical Market Growth (2020-2025) |

4.3% |

Market Dynamics

Drivers - Government-led Biodiesel Blending Mandates Globally Are Driving Sustained Demand for Cold Flow Improvers to Ensure Winter Fuel Operability

Government initiatives supporting renewable energy have significantly increased global biodiesel consumption, especially across North America and Europe, where mandatory fuel blending policies are actively enforced. The European Union’s renewable energy directives require the integration of biodiesel into transportation fuels, whereas the United States continues to implement the Renewable Fuel Standard, which mandates specific biodiesel blending volumes each year. However, biodiesel exhibits poor cold-flow performance due to its fatty acid structure. Its cloud point typically ranges between 0°C and +10°C, which is considerably higher than that of conventional diesel.

As a result, specialized cold-flow improvers are essential to ensure smooth fuel operation under winter conditions. These additives prevent fuel crystallization and operational failure in low temperatures. This regulatory-driven transition toward cleaner fuels has created long-term demand for cold-flow improver formulations. Leading manufacturers such as Evonik Industries AG and Clariant AG continue developing tailored additive solutions compatible with various biodiesel feedstocks, including soybean, palm oil, and waste cooking oil-based biodiesel.

Rising Heating Oil Consumption in Cold Regions Continues to Increase Reliance on Cold Flow Improvers for Uninterrupted Fuel Performance

Cold-climate regions across North America and Northern Europe continue to generate strong demand for heating oil and middle-distillate fuels that require cold-flow improvers for reliable winter performance. Areas such as the U.S. Midwest and Northeast experience recurring severe winter conditions, as reported by the National Weather Service, which lead to increased seasonal heating-oil consumption. Industrial facilities, residential heating systems, and commercial operations depend on an uninterrupted fuel supply during sub-zero temperatures, making cold flow improvers essential to prevent fuel gelling and filter blockage.

In addition, agricultural activities that rely on diesel-powered machinery during the winter months further strengthen additive demand. Recent severe winter conditions have pushed ultra-low sulfur diesel futures to approximately $2.39 per gallon, reflecting heightened volatility in demand. These conditions reinforce the importance of performance-enhancing fuel additives that ensure consistent operability, reduce equipment downtime, and maintain supply reliability across diverse cold-weather environments.

Restraints - High Additive Production Costs and Strong Price Sensitivity In Developing Economies Limit the Adoption Of Advanced Cold Flow Improver Technologies

Cold-flow improvers, particularly polymethacrylate and ethylene-vinyl acetate-based formulations, involve complex polymer chemistry and advanced synthetic processes. These technical requirements result in significantly higher production costs than those of conventional fuel additives. In emerging markets across Asia-Pacific and Latin America, where biodiesel output is expanding rapidly, fuel distributors often exhibit high price sensitivity. This limits the adoption of premium additive solutions, as cost reduction frequently takes priority over performance optimization. The economic gap between developed and developing regions creates barriers to adoption, particularly for high-end formulations.

Fluctuating prices of polymer feedstock and chemical raw materials introduce cost volatility for manufacturers. These fluctuations directly affect profit margins and restrict long-term investment in research and development. As a result, innovation cycles may slow, limiting the availability of advanced cold-flow technologies in cost-sensitive markets despite increasing fuel performance requirements.

Variations in Biodiesel Feedstocks and Fragmented Global Fuel Regulations Create Formulation Complexity and Increase Compliance Burdens for Manufacturers

The effectiveness of cold-flow improvers varies significantly with biodiesel feedstock composition, posing major formulation challenges for manufacturers. Biodiesel derived from palm oil, for example, exhibits markedly poorer cold-flow properties than soybean-based biodiesel, necessitating customized additive solutions. This variability increases research and development costs, as each formulation must be optimized for specific fatty acid profiles. Additionally, regulatory fragmentation across global markets adds complexity.

Standards such as Europe’s EN 590, ASTM fuel specifications in North America, and country-specific requirements in emerging regions require manufacturers to develop multiple product variants. Uncertainty surrounding future biodiesel blending mandates and evolving fuel quality regulations further complicates planning and investment decisions. These challenges are intensified by biodiesel impurities such as residual glycerides and saturated monoglycerides, which can interact unpredictably with additives. As a result, extensive compatibility testing is essential prior to commercial deployment.

Opportunities - Rapid Biodiesel Capacity Expansion Across Asia Pacific Presents Significant Growth Opportunities for Region-Specific Cold Flow Improver Formulations

Asia-Pacific represents the fastest-growing regional opportunity for cold-flow improvers, driven by large-scale biodiesel expansion in China, Indonesia, Malaysia, and India. China dominates East Asia’s biodiesel industry with approximately 63.5% regional share, supported by strong government initiatives focused on renewable energy adoption and air quality improvement. Indonesia’s biodiesel market is projected to grow at a CAGR of 7.8% through 2030, supported by abundant palm oil feedstock and rising domestic blending mandates.

These markets require cold-flow improvers specifically designed for tropical biodiesel feedstocks and that also support low-temperature performance in high-altitude and northern regions. Japan contributes expertise in advanced additive formulations, whereas Southeast Asian producers focus on cost-efficient solutions. The combination of regulatory support, expanding industrial activity, and local manufacturing capabilities creates significant revenue opportunities for additive suppliers that establish regional production and develop feedstock-specific technologies.

Growing environmental regulations are accelerating innovation in bio-based, sustainable cold flow improvers with improved performance efficiency

Rising environmental regulations are accelerating innovation toward bio-based and sustainable cold flow improver formulations. The European Union’s REACH directive has encouraged manufacturers to reduce toxicity and environmental impact across fuel additive portfolios. As a result, companies are increasingly developing additives derived from renewable sources, including bio-based polymers, ester compounds, and waste biomass materials. BASF SE has introduced bio-based cold-flow improvers that meet stringent safety requirements while maintaining performance comparable to conventional petroleum-based additives.

Refiners and fuel marketers are increasingly favoring such sustainable solutions to align with regulatory expectations and consumer environmental awareness. Advanced formulation techniques, including nanoemulsion technology and modified polymer chemistry, enable additives to function effectively at lower dosages. This improves fuel economics while enhancing compatibility with diverse fuel blends. Recent data indicate that bio-based additives have achieved approximately 33.5% higher sales growth than traditional formulations, highlighting strong differentiation potential.

Category-wise Analysis

Product Type Insights

Ethylene-vinyl acetate copolymers dominate the cold flow improvers market, commanding approximately 35% market share among all product type categories. The market leadership of EVA-based formulations reflects a compelling combination of technical performance and economic efficiency. EVA copolymers modify the crystalline morphology of paraffinic waxes precipitating from diesel fuel, preventing the formation of large crystal aggregates that obstruct fuel filtration systems and impair engine operability at low temperatures.

The cost efficiency of EVA synthesis relative to advanced polyacrylate alternatives, combined with its demonstrated compatibility across diverse fuel compositions, including petroleum diesel, biodiesel blends up to B20, heating oil, and marine distillates, ensures its continued dominance among fuel refiners and blenders operating under margin constraints. EVA additives typically reduce the pour point by 11-15°C and the cloud point by 3-8°C, making them suitable for regions with moderately severe winter conditions. The established manufacturing infrastructure, supply chain maturity, and proven performance profile position EVA-based products as the baseline technology against which competitive formulations are benchmarked.

Fuel Type Insights

Diesel fuel represents the largest and most mature application segment, accounting for 62% of the total cold-flow improvers market value in 2026 and maintaining this dominant position through 2033. The extraordinary scale of global diesel consumption, approximately 1.3 billion barrels annually across automotive, industrial, and power generation applications, creates the foundational demand base for cold flow improvers. However, the segment's growth trajectory has moderated from historical rates: the automotive diesel segment, which accounts for 78% of total diesel demand, faces headwinds from electric vehicle adoption in Western markets, particularly the European Union, where ICE vehicle sales have declined 25% since 2019.

Offsetting these headwinds, the expansion of biodiesel mandates in the United States (B11 nationwide, with state-level programs targeting B20-B50) and the European Union (increasing volumetric quotas annually) directly amplifies demand for cold flow improvers, as biodiesel's poor low-temperature properties necessitate aggressive additive treatment. Industrial diesel applications for stationary power generation, irrigation systems, and agricultural machinery in emerging markets, including India, Vietnam, and Indonesia, are expanding at 6-8% annually, partially offsetting headwinds in mature vehicle markets.

End-user Insights

Marine fuel and heating oil applications collectively account for approximately 22% of market demand, with marine fuel experiencing accelerated growth following the IMO 2020 sulfur reduction mandate. The marine fuel segment grew at an annual rate of 8% from 2020 to 2025, substantially exceeding overall market growth, as shipping operators and marine fuel suppliers across the Mediterranean, North Atlantic, and Asia-Pacific shipping corridors require specialized cold-flow improvers to maintain fuel fluidity during winter transits and high-latitude operations. Heating-oil applications, primarily in North America, Northern Europe, and Russia, account for approximately 10% of market value, with demand concentrated in regions that experience sub-zero temperatures during the winter months. Residential and commercial heating oil systems face particular challenges because inadequate cold-flow performance can lead to catastrophic system failures, creating a critical quality-control imperative for refiners and distributors. The nascent demand from Arctic shipping routes and the potential for expanded SAF adoption in aviation represent emerging opportunities to accelerate growth in the marine fuel segment toward a 12% market share by 2033.

Regional Insights

North America Cold Flow Improvers Trends

North America remains a key market for cold flow improvers due to severe winter conditions across the U.S. Midwest, Northeast, and Canada. Prolonged sub-zero temperatures consistently drive demand for additives that ensure fuel reliability during winter months. Recent cold seasons have significantly increased diesel and heating oil consumption, with ultra-low sulfur diesel futures rising between $2.33 and $2.39 per gallon. The region also benefits from strong regulatory support for biodiesel through the U.S. Renewable Fuel Standard, which mandates annual blending volumes. This creates dual demand drivers: traditional winter diesel operability and biodiesel-specific cold-flow challenges. Heavy-duty trucking, agricultural machinery, and commercial transport further strengthen additive consumption. Environmental regulations enforced by the EPA encourage the use of advanced, low-toxicity additives. Strategic collaborations between global manufacturers and regional fuel distributors enhance supply efficiency, while robust research infrastructure continues to support innovation in emerging fuels such as renewable diesel and synthetic blends.

Europe Cold Flow Improvers Trends

Europe is the largest global market for cold-flow improvers, supported by strict fuel-quality regulations, widespread cold-climate zones, and aggressive renewable energy mandates. The EN 590 diesel standard defines multiple climate grades, with Cold Filter Plugging Point requirements ranging from –5°C to –44°C depending on regional conditions. Northern European countries, including Germany, the UK, and the Scandinavian countries, experience sustained winter demand for heating oil and diesel additives. The Fuel Quality Directive mandates a minimum 7% biodiesel blending rate, increasing the need for cold flow solutions that address biodiesel limitations.

Europe also benefits from strong domestic chemical manufacturing capabilities, led by BASF SE, Clariant AG, and Evonik Industries AG. Environmental regulations under REACH promote innovation in bio-based and low-toxicity formulations. Industry collaborations, including renewable carbon supply initiatives, further support sustainability goals. The region’s mature infrastructure, regulatory clarity, and customer sophistication continue to reinforce Europe’s market leadership.

Asia Pacific Cold Flow Improvers Trends

Asia-Pacific is the fastest-growing regional market for cold-flow improvers, driven by rapid industrial expansion, rising vehicle ownership, and strong growth in biodiesel production. China leads regional demand with approximately 63.5% market share in East Asia, supported by infrastructure development and government-led emission reduction initiatives. Diesel-powered machinery in the construction, mining, and logistics sectors significantly contributes to additive consumption, particularly in northern regions with cold-season conditions.

Indonesia and Malaysia are expanding biodiesel capacity by leveraging abundant palm oil feedstocks, thereby creating demand for additives tailored to palm-based biodiesel. Japan remains the regional leader in advanced additive manufacturing technology, while ASEAN countries are strengthening their manufacturing and distribution capabilities. Growing mechanization in agriculture, expanding transportation networks, and evolving fuel standards continue to support long-term demand. Cost-efficient production advantages and increasing technical expertise position Asia-Pacific as both a major consumption hub and an increasingly important contributor to global cold-flow improver supply chains.

Competitive Landscape

The global cold flow improvers market is moderately consolidated, led by multinational chemical companies with strong research capabilities and global distribution networks. BASF SE and Clariant AG maintain competitive leadership through decades of fuel additive expertise, vertically integrated operations, and comprehensive technical support services. Evonik Industries AG has strengthened its market position through focused investments in advanced polymethacrylate chemistry and strategic capacity expansions. Competition is largely driven by innovation addressing evolving fuel specifications, sustainability requirements, and regional regulatory compliance.

Strategic collaborations, such as renewable carbon partnerships, highlight the industry’s shift toward environmentally responsible solutions. Regional players increasingly focus on niche markets by developing customized additives for specific biodiesel feedstocks and climate conditions. Key competitive differentiators include formulation flexibility, alignment with environmental compliance requirements, and strong technical service capabilities that support customers in dosage optimization and performance improvement. Supply chain resilience and sustainability innovation continue shaping long-term competitive positioning.

Key Market Developments

- In August 2023: Evonik Industries AG expanded production capacity for cold flow improvers at its German facility, reflecting strategic investment in high-performance diesel and biofuel additive manufacturing to support market growth and meet rising demand across automotive and industrial applications.

- In January 2024: BASF SE launched a new Keropur® gasoline additive formulation in Taiwan, enhancing engine cleanliness and performance for modern direct injection engines while supporting regional market expansion of advanced fuel additive technologies.

- In July 2024: Clariant AG and OMV entered a strategic partnership to advance renewable carbon integration in European ethylene supply chains, strengthening sustainable additive development and contributing to lower-carbon chemical value chains aligned with EU environmental policies.

Companies Covered in Cold Flow Improvers Market

- BASF SE

- Clariant AG

- Evonik Industries AG

- AkzoNobel N.V.

- Baker Hughes Inc.

- Afton Chemical

- Bell Performance, Inc.

- The Lubrizol Corporation

- Chevron Corporation

- Infineum International Limited

- Ecolab

- ADCO Global Inc.

- AICELLO CHEMICAL CO. LTD

- ACE Geosynthetics Enterprise Co., Ltd.

- International Fuel Technology, Inc.

- Innospec Inc.

- Croda International Plc

- Dorf Ketal Chemicals

- Chevron Oronite Company LLC

- LANXESS AG

Frequently Asked Questions

The global cold flow improvers market is expected to reach US$ 1,242.9 million by 2033, growing at a 5.8% CAGR driven by rising biodiesel use and cold-climate fuel requirements.

Demand is driven by biodiesel blending mandates, strict fuel quality regulations, harsh winter conditions, industrial expansion, and increasing diesel use in cold regions.

EVA-based cold flow improvers lead the market due to strong wax modification performance, wide fuel compatibility, cost efficiency, and well-established supply chains.

Europe dominates the market supported by strict EN 590 standards, mandatory biodiesel blending, cold climate exposure, and presence of major additive manufacturers.

Asia Pacific biodiesel expansion, particularly in China and Indonesia, represents the strongest opportunity driven by renewable fuel mandates and rising diesel consumption.

Key players include BASF SE, Clariant AG, Evonik Industries AG, Lubrizol, Afton Chemical, Infineum, and AkzoNobel, leading through innovation and global distribution strength.