- Transportation & Logistics

- Refrigerated Transport Market

Refrigerated Transport Market Size, Share, and Growth Forecast 2026 - 2033

Refrigerated Transport Market by Technology (Air-blown Evaporators, Eutectic, Hybrid, Fully Electrified), Application (Food & Beverages, Pharmaceuticals, Chemicals; Others), Temperature Range (Deep Frozen Below -25°C, Frozen -18°C to -25°C, Chilled 0°C to 8°C, Ambient Controlled 8°C to 25°C), Mode of Transport (Road, Rail, Sea, Air), and Regional Analysis, 2026 - 2033

Refrigerated Transport Market Size and Trend Analysis

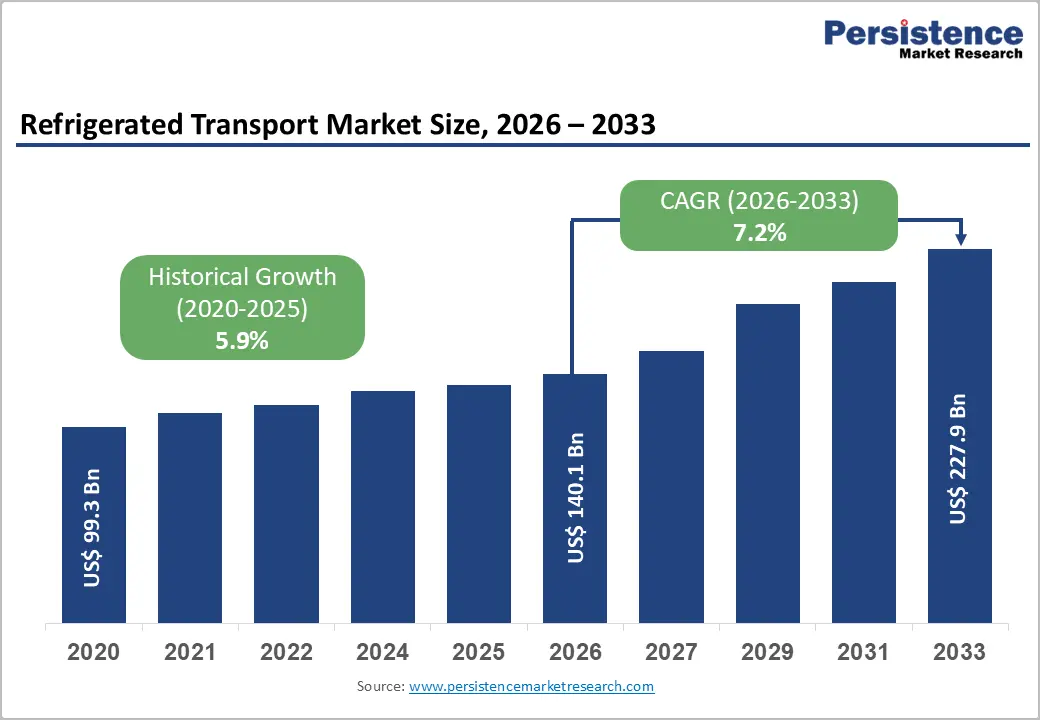

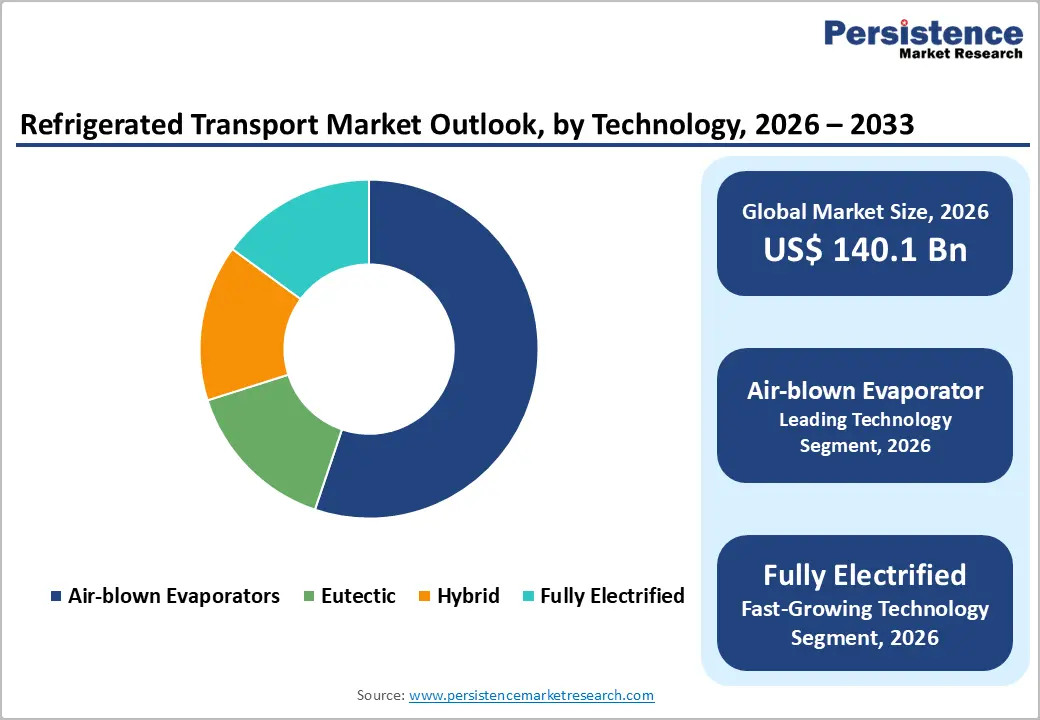

The global refrigerated transport market size is expected to be valued at US$ 140.1 billion in 2026 and projected to reach US$ 227.9 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

The expansion of global food trade and organized retail requiring reliable cold chain coverage, the COVID-19 accelerated buildout of pharmaceutical cold chain infrastructure for vaccine and biologic distribution, and the rapid development of cold chain logistics networks in the Asia Pacific and the Middle East supported by stricter food safety regulations and rising urban delivery demand.

Key Industry Highlights

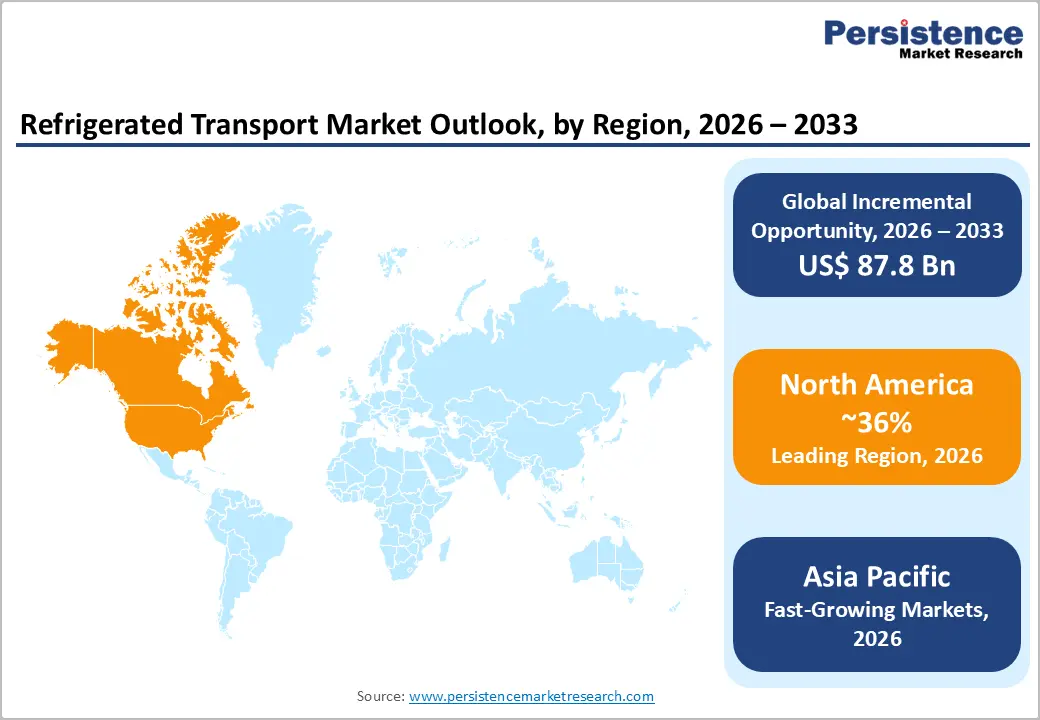

- Leading Region: North America commands 36% global refrigerated transport share in 2025, anchored by the world's most extensive organized grocery cold chain, C.R. England and J.B. Hunt's high-utilization reefer fleets, and USDA-documented consistent growth in refrigerated truck-miles driven by e-grocery and pharmaceutical cold chain expansion.

- Fastest Growing Region: Asia Pacific is the fastest growing market poised at 9.0% CAGR through 2033, driven by India's FAO-documented 25-35% food loss rate requiring structural cold chain investment, China's 14th Five-Year Plan cold chain expansion, and Southeast Asia's organized retail and food safety regulation formalization.

- Dominant Mode: Road commands 72% mode market share in 2025, driven by IRU-documented 80% of European perishable freight moving exclusively by road and the universal requirement for door-to-door cold chain delivery that only refrigerated trucking can fulfill as the mandatory first and last mile.

- Fastest Growing Technology: Fully electrified transport refrigeration units are the fastest growing technology, driven by EU zero-emission delivery zone mandates, Daikin's EU-certified E-powered TRU, and F-Gas Regulation phase-down of HFC refrigerants forcing fleet upgrades to electric and CO2-based refrigeration systems.

- Key Market Opportunity: Kuehne + Nagel's KN PharmaChain expansion to 15 Asian markets signals that WHO GDP-compliant pharmaceutical refrigerated transport is the highest-margin segment, and Asia Pacific's structural cold chain gap creates the largest greenfield volume opportunity for operators with certified networks through 2033.

Market Dynamics

Drivers - Pharmaceutical Cold Chain Mandates Driving Non-Negotiable Infrastructure Investment

The pharmaceutical industry’s rising reliance on biologics, mRNA vaccines, and temperature-sensitive specialty drugs is turning cold chain logistics into a strategic requirement, pushing carriers and 3PLs to invest in GDP-compliant refrigerated transport infrastructure. WHO Good Distribution Practice guidelines and EU GDP regulations mandate strict temperature-controlled handling, with non-compliance risking recalls and loss of market authorization. The COVID-19 vaccine rollout highlighted this need, requiring ultra-cold chain capabilities and triggering long-term upgrades in pharmaceutical transport systems.

Leading logistics providers are expanding GDP-certified capacity to serve this high-value segment, which is emerging as one of the fastest-growing and highest-margin areas in the refrigerated transport market through 2033.

Organized Retail Expansion and Food Safety Regulation Enforcement Expanding Cold Chain Demand

The expansion of modern organized retail formats, supermarkets, hypermarkets, and online grocery platforms across Asia Pacific, Latin America, and the Middle East is structurally requiring cold chain infrastructure that did not previously exist at national scale, creating the single largest volume demand expansion opportunity in refrigerated transport.

The Food and Agriculture Organization (FAO) estimates that approximately 14% of global food production is lost between harvest and retail, losses that cold chain infrastructure directly reduces, creating powerful policy and commercial incentives for cold chain investment. India's Food Safety and Standards Authority (FSSAI) food safety regulations and China's National Food Safety Standards enforcement are progressively mandating refrigerated transport for temperature-sensitive food categories that previously moved at ambient temperatures.

Each new organized retail store requiring replenishment from a refrigerated distribution center extends the cold chain network and generates recurring refrigerated trucking demand, sustaining above-average refrigerated transport demand growth in these markets through the forecast period.

Restraints - High Capital and Operating Costs of Reefer Fleet Limiting Small Operator Participation

Refrigerated transport requires capital investment and operating cost structures 2-3 times higher than equivalent dry freight transport, encompassing reefer unit procurement, diesel fuel for refrigeration, maintenance of cryogenic sealing, and compliance certification, creating a structural barrier that concentrates market participation among well-capitalized operators and limits competition. Thermo King and Carrier Transicold refrigeration unit prices can add US$ 25,000-US$ 60,000 per trailer, with annual maintenance and fuel costs further elevating total cost of ownership.

For new entrants in developing markets where refrigerated transport is earliest-stage, this capital intensity restricts rapid supply expansion to meet demand growth, creating capacity bottlenecks that in turn compress service quality and limit cold chain coverage to economically justifiable urban corridors.

Refrigerant Phase-Down Regulations Forcing Equipment Replacement and Technology Transition

The international phase-down of hydrofluorocarbon (HFC) refrigerants under the Kigali Amendment to the Montreal Protocol, ratified by 148 parties as of 2024, is forcing refrigerated transport operators to accelerate equipment replacement and transition to next-generation refrigerants including CO2 (R-744), R-452A, and HFO-1234yf, incurring significant capital expenditure that was not anticipated in existing fleet depreciation schedules.

The EU F-Gas Regulation banning high-GWP refrigerants in mobile refrigeration from 2025 is the most immediate compliance driver for European operators, imposing retrofit or replacement costs on refrigerated trailers and rigid vehicles using R-404A or R-410A. Operators unable to absorb these transition costs, particularly smaller regional carriers, face competitive disadvantage versus well-capitalized fleets that proactively upgraded to low-GWP refrigerant systems.

Opportunities - Fully Electrified Refrigerated Transport: The Highest-Growth Technology Segment

Fully electrified transport refrigeration units (e-TRUs), powered by electric drives rather than diesel gensets, represent the fastest growing technology segment in refrigerated transport, and companies that invest in electric reefer fleets now are positioned to capture both regulatory tailwinds and operational cost advantages as electricity displaces diesel across urban freight corridors. The EU's Clean Vehicles Directive and zero-emission urban delivery zone mandates in cities including London, Paris, and Amsterdam are creating hard regulatory deadlines for zero-emission last-mile delivery, including refrigerated last-mile, that make e-TRU investment a compliance necessity rather than a sustainability option

Daikin Industries has launched electric TRUs specifically targeting urban zero-emission delivery programs. SolarFreeze and Fenagy are pioneering solar-powered and hybrid-electric cold storage mobility platforms for emerging markets where grid access is unreliable. Carriers that build electric reefer capability early will enjoy first-mover advantage in urban routes where e-TRU becomes the only regulatory-compliant option.

Asia Pacific Pharmaceutical and Food Cold Chain Buildout: Highest-Volume Greenfield Opportunity

Asia Pacific represents the single largest greenfield opportunity in refrigerated transport, a region where cold chain coverage gaps are structural rather than cyclical, meaning demand creation from regulatory enforcement and organized retail expansion will generate new refrigerated transport volumes rather than merely displacing existing operators. India's National Cold Chain Fund and government-backed Integrated Cold Chain Infrastructure Scheme under the Ministry of Food Processing Industries (MoFPI) are channeling public and private capital into refrigerated transport infrastructure to reduce the 25-35%) food loss rate that the FAO attributes to inadequate cold chain coverage.

China's 14th Five-Year Plan targets significant expansion of refrigerated logistics capacity to support food safety enforcement and pharmaceutical distribution. For logistics operators, including C.H. Robinson, Kuehne + Nagel, and Schneider National establishing refrigerated transport capabilities and partnerships in Asia Pacific now positions them to capture the highest-volume single regional demand expansion in cold chain logistics through 2033.

Category-wise Analysis

Technology Insights

Air-blown Evaporator refrigeration systems command the leading Technology segment position with approximately 58% market share in 2025, a dominance rooted in the technology's universal compatibility with the global installed base of refrigerated trailers and its flexibility across the temperature ranges required by the dominant food and beverage application segment.

Air-blown evaporators circulate refrigerated air throughout the cargo space through a heat exchanger coil powered by a diesel or electric compressor, making them the standard design specification for road reefer trailers from manufacturers including Great Dane and Wabash National. Their established global service network, from Thermo King and Carrier Transicold dealer networks, provides the maintenance infrastructure that sustains operator preference. Fully electrified e-TRUs are the fastest growing technology, gaining traction in urban zero-emission delivery programs across Europe.

Application Analysis

Food and Beverages commands the leading application segment at approximately 67% market share in 2025, driven by the universal requirement for temperature-controlled distribution across fresh produce, dairy, meat, seafood, and processed food categories that collectively constitute the world's highest-volume refrigerated commodity flows.

The World Trade Organization (WTO)) documents global agricultural trade exceeding US$ 2 trillion) annually, with temperature-sensitive food categories representing a growing proportion of total food trade as organized retail formats requiring consistent cold chain penetrate new geographies. Within food and beverages, fish, meat, and seafood represent the highest per-shipment value density, while fruits and vegetables generate the highest volume. The pharmaceutical application segment is the fastest growing, expanding well above the overall CAGR as biologic drug and vaccine distribution mandates proliferate.

Temperature Range Insights

Chilled transport (0°C to 8°C) commands the leading temperature range segment at approximately 42% market share in 2025, reflecting the dominant position of fresh food, dairy products, fresh produce, beverages, and chilled ready meals in the overall refrigerated transport commodity mix. Chilled transport is structurally the most commercially active temperature band because it serves the broadest range of everyday consumer food categories that require consistent near-0°C management without the deep-freeze infrastructure costs associated with frozen and deep-frozen applications.

The Global Cold Chain Alliance (GCCA)) documents chilled storage and transport as the fastest-growing cold chain service category globally, outpacing frozen, driven by consumer preference for fresh versus frozen food across developed and developing markets alike. Deep-frozen transport is growing fastest among the temperature segments, driven by expanding frozen food trade and vaccine ultra-cold chain requirements.

Mode of Transport Insights

Road refrigerated transport commands the dominant position at approximately 72% market share in 2025, reflecting the fundamental operational requirement for door-to-door delivery that only road transport can fulfill as the first and last mile of virtually every cold chain movement. The International Road Transport Union (IRU) estimates that 80% of European perishable food freight travels exclusively by road, a pattern replicated across North America, Asia, and Latin America where refrigerated truck networks serve both long-haul origin-to-distribution-center and short-haul last-mile delivery roles. Refrigerated sea freight is the second-largest mode by revenue, critical for inter-continental fresh and frozen food trade, while air freight commands the highest per-shipment value density through its dominance in pharmaceutical and high-value perishable shipments.

Regional Insights

North America Refrigerated Transport Market Trends and Insights

North America leads the global refrigerated transport market through its mature, high-utilization refrigerated fleet, dominated by C.R. England, J.B. Hunt, and Swift Transportation, combined with a highly developed food and beverage cold chain infrastructure serving the world's largest organized retail and grocery sector. The USDA documents consistent growth in refrigerated truck-miles traveled, underpinned by expanding e-grocery and meal kit delivery requiring temperature-controlled last-mile execution. The region's forward trajectory points toward electrification of urban reefer delivery, pharmaceutical cold chain expansion driven by specialty drug distribution growth, and carrier consolidation as scale economies increasingly favor national versus regional operators.

U.S. Refrigerated Transport Market Size

The United States accounts for approximately 84% of North American refrigerated transport revenue in 2025, underpinned by USDA-documented consistent growth in temperature-sensitive food shipments and the world's largest pharmaceutical distribution network requiring GDP-compliant cold chain. C.R. England and J.B. Hunt's refrigerated divisions serve national food distribution. U.S. CAGR is projected at approximately 6.8% through 2033, driven by pharmaceutical cold chain and e-grocery expansion.

Europe Refrigerated Transport Market Trends and Insights

Europe's refrigerated transport market is defined by the world's most stringent regulatory environment, encompassing EU GDP Directive pharmaceutical requirements, F-Gas Regulation refrigerant phase-down mandates, and urban zero-emission delivery zone proliferation, that simultaneously constrains conventional reefer operations and creates premium opportunity for operators with compliant, next-generation fleets. Kuehne + Nagel) and European 3PLs dominate pharmaceutical cold chain, while food distribution giants serve pan-European chilled freight networks. The region is transitioning toward electric and hybrid reefer vehicles faster than any other geography, making technology investment a core competitive differentiator.

Germany Refrigerated Transport Market Size

Germany holds approximately 23% of European refrigerated transport revenue in 2025, anchored by Europe's largest food processing industry and pharmaceutical manufacturing base requiring consistent refrigerated distribution. German logistics operators are leaders in adopting CO2 refrigeration and electric TRUs under F-Gas Regulation compliance. Germany is projected at approximately 7.0% CAGR through 2033, with pharmaceutical cold chain the fastest growing sub-segment.

U.K. Refrigerated Transport Market Size

The United Kingdom represents approximately 14% of European refrigerated transport revenue in 2025. The UK's mature grocery cold chain, dominated by Tesco, Sainsbury's, and Ocado's automated cold fulfilment network, sustains consistent chilled and frozen transport demand. London's zero-emission delivery zone requirements are accelerating electric reefer van adoption. UK CAGR is projected at approximately 6.9% through 2033.

France Refrigerated Transport Market Size

France accounts for approximately 12% of European refrigerated transport revenue in 2025. France's premium food and dairy exports, including cheese, wines, and fresh produce requiring consistent temperature management, generate high-value refrigerated freight, while Sanofi)'s and other pharmaceutical manufacturers' distribution networks sustain pharmaceutical cold chain demand. Paris' zero-emission urban logistics zones are driving electric reefer van deployment. France is projected at approximately 6.8% CAGR through 2033.

Asia Pacific Refrigerated Transport Market Trends and Insights

Asia Pacific is the fastest growing refrigerated transport region globally, driven by the structural convergence of cold chain infrastructure gaps, food safety regulatory enforcement, and organized retail expansion across the world's most populous markets. China, which accounts for approximately 38% of Asia Pacific refrigerated transport demand, is investing massively in domestic cold chain infrastructure under its 14th Five-Year Plan, while India, Southeast Asia, and South Korea are experiencing rapid cold chain formalization from both food safety regulation and pharmaceutical distribution requirements. Companies scaling refrigerated transport capabilities in Asia Pacific now will build first-mover advantages in markets where cold chain coverage gaps are structural and demand creation from regulatory enforcement will be sustained for at least a decade.

India Refrigerated Transport Market Size

India represents approximately 14% of Asia Pacific refrigerated transport revenue in 2025. India's 25-35% FAO-documented food loss rate from inadequate cold chain, combined with FSSAI food safety regulation enforcement and MoFPI cold chain scheme incentives, are driving structural refrigerated transport demand growth. India is projected at approximately 10.5% CAGR through 2033, the fastest among major markets, as first-time cold chain infrastructure buildout generates structurally additive demand.

Japan Refrigerated Transport Market Size

Japan contributes approximately 11% of Asia Pacific refrigerated transport revenue in 2025. Japan's sophisticated food culture, extensive convenience store distribution network, with 7-Eleven), FamilyMart, and Lawson requiring multi-temperature daily replenishment, and advanced pharmaceutical logistics sustain high utilization of Japan's mature reefer fleet. Japan is projected at approximately 6.5% CAGR through 2033, with electric reefer vehicles gaining adoption.

Southeast Asia Refrigerated Transport Market Size

Southeast Asia collectively accounts for approximately 13%) of Asia Pacific refrigerated transport revenue in 2025. Thailand, Vietnam, Indonesia, and the Philippines are experiencing rapid cold chain formalization as expanding organized retail, growing seafood exports, and tightening food safety regulations drive refrigerated transport investment. SolarFreeze’s solar-powered cold storage and Fenagy's hybrid cold chain platforms are pioneering off-grid-capable solutions specifically for Southeast Asian market constraints. Southeast Asia is projected at approximately 9.8% CAGR through 2033.

Competitive Landscape

The refrigerated transport market is moderately fragmented at the carrier level, with numerous regional operators serving food and pharmaceutical supply chains, while scale and network integration increasingly define competitiveness at the 3PL level. Large operators benefit from extensive fleets, long-term shipper relationships, and optimized route networks, whereas smaller players compete through regional specialization and flexibility.

Strategically, the market is shifting toward technology-driven differentiation, with investments in electric refrigeration units, low-emission refrigerants, and GDP-compliant cold chain infrastructure becoming critical. Vertical specialization, particularly in high-value pharmaceutical logistics versus volume-driven food distribution, is shaping service offerings and margins. Additionally, digital platforms providing real-time temperature monitoring, tracking, and compliance reporting are emerging as key value-added services. New entrants are leveraging asset-light, technology-enabled models to penetrate emerging markets, offering cost-efficient and scalable solutions where traditional refrigerated transport economics remain challenging.

Key Developments

- April 2026: Carrier Transicold announced it will showcase electric and low-emission transport refrigeration solutions at Transport 2026, highlighting hybrid and zero-emission systems designed to reduce fleet emissions, improve energy efficiency, and support sustainable cold chain operations.

- August 2025: TIP Group partnered with Sunswap to launch EU trials of a zero-emission transport refrigeration unit with Daily Logistics Group, testing battery and solar-powered cooling technology on long-haul routes to reduce emissions and improve cold chain efficiency.

- June 2024: Mitsubishi Heavy Industries announced development of next-generation aviation and mobility technologies, focusing on advanced aerospace systems, low-emission propulsion solutions, and integrated transport innovation to strengthen its long-term position in global industrial and mobility markets.

Refrigerated Transport Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 99.3 Billion |

| Current Market Value (2026) | US$ 140.1 Billion |

| Projected Market Value (2033) | US$ 227.9 Billion |

| CAGR (2026 - 2033) | 7.2% |

| Leading Region | North America, 36% market share (2025) |

| Dominant Technology | Air-blown Evaporators, 58% share (2025) |

| Top-Ranking Application | Food & Beverages, 67% share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 87.8 Billion |

Companies Covered in Refrigerated Transport Market

- C.R. England Inc.

- J.B. Hunt Transport Services, Inc.

- Swift Transportation Co.

- Schneider National, Inc.

- Great Dane LLC

- C.H. Robinson Worldwide, Inc.

- Fenagy

- Kuehne + Nagel International AG

- SolarFreeze

- Wabash National Corporation

- Daikin Industries, Ltd.

- Thermo King Corporation (Trane Technologies)

- Carrier Transicold

- DB Schenker

- DSV A/S

Frequently Asked Questions

The market is projected to reach US$ 140.1 billion in 2026.

Demand is driven by pharmaceutical cold chain expansion, food safety needs, and retail cold chain growth.

North America leads, accounting for around 36% of the market share.

The key opportunity lies in pharmaceutical cold chain logistics and electric reefer technologies.

Leading players include C.R. England Inc., J.B. Hunt Transport Services, Kuehne + Nagel, C.H. Robinson, Swift Transportation, Schneider National, Great Dane, Wabash National, Daikin Industries, Thermo King, Carrier Transicold, SolarFreeze, Fenagy, DB Schenker, and DSV A/S.