- Specialty & Fine Chemicals

- Chemical Protective Clothing Market

Chemical Protective Clothing Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Chemical Protective Clothing Market by Type of Clothing (Durable Chemical Protective Clothing, Disposable Chemical Protective Clothing), Material Type (Polyvinyl Chloride (PVC), Polypropylene, Polyethylene, Rubber, PTFE (Polytetrafluoroethylene), and Other Materials), Industry (Pharmaceuticals, Oil & Gas, Construction & Manufacturing, Healthcare/Medical, Firefighting & Law Enforcement, Mining, Military, and Others), and Regional Analysis for 2026 - 2033

Chemical Protective Clothing Market Size and Trends Analysis

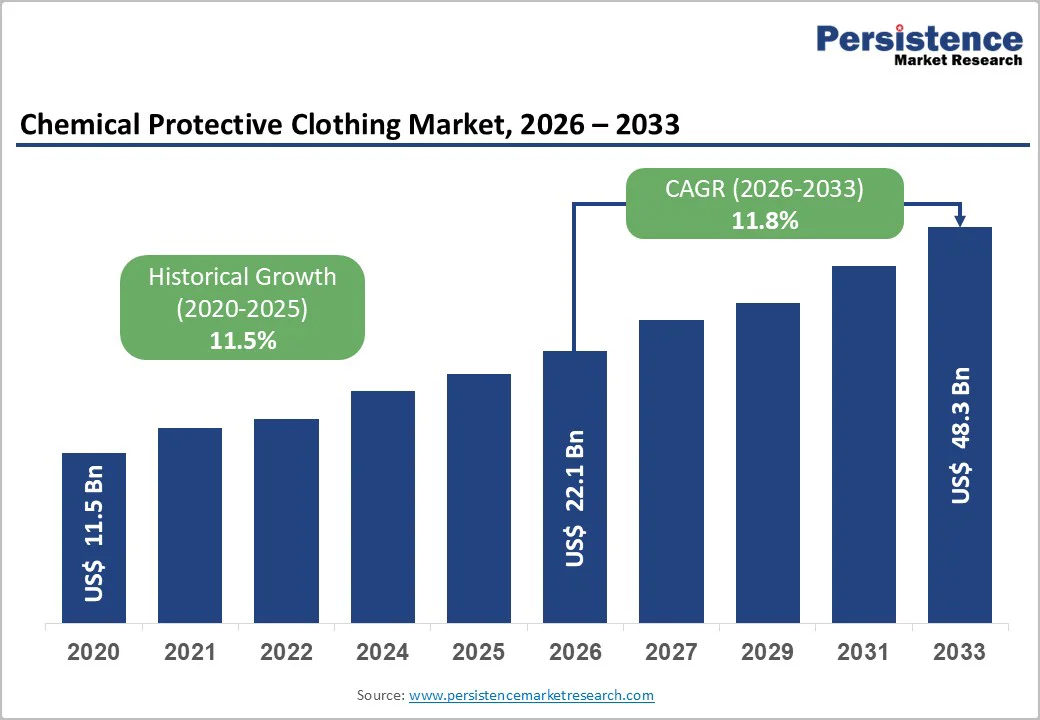

The global chemical protective clothing market size is likely to reach US$22.0 billion in 2026 and is expected to reach US$48.1 billion by 2033, registering a strong CAGR of 11.9% during the forecast period 2026 to 2033. The rise in stringent occupational safety regulations, rapid advancements in materials science, and incidents of chemical and biological hazard exposure in industrial environments underscore the need for chemical protective clothing. The demand is particularly strong in the pharmaceutical, oil & gas, and emergency response sectors.

Key Industry Highlights:

- Power Source Leadership: Diesel-powered grinders command 60%+ revenue share, while the electric-powered segment represents the fastest-growing category due to environmental regulations and operational cost advantages.

- Capacity Market Leader: 700-900 HP category dominates with 40%+ revenue share; 400-700 HP represents the fastest-growing segment aligned with specialized application expansion and distributed processing facility development.

- Application Dynamics: Wood recycling and processing maintains 20%+ revenue share; land clearing and forestry operations experience fastest growth at 6.8-7.4% CAGR driven by infrastructure development and climate-related land management requirements.

- Regional Market Performance: North America maintains 40% global market share (US$640 million); Asia Pacific represents the fastest-growing region at 6.1% CAGR in the forecast period.

- Strategic Developments: Product line expansion by CBI (2025), Bandit Industries market entry (2025), and electric technology commercialization by WSM indicate intensifying competition and technology-driven market differentiation strategies reshaping competitive positioning.

| Key Insights | Details |

|---|---|

|

Chemical Protective Clothing Market Size (2026E) |

US$22.1 Bn |

|

Market Value Forecast (2033F) |

US$48.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

11.8% |

|

Historical Market Growth (CAGR 2019 to 2025) |

11.5% |

Market Dynamics

Drivers - Key Regulatory, Industrial, and Technological Forces Driving Demand for Chemical Protective Clothing

Stringent occupational health and safety regulations have become one of the strongest demand catalysts for chemical protective clothing, as global authorities intensify compliance requirements. Agencies such as OSHA, ECHA, and the ILO have tightened enforcement of chemical exposure standards, mandating certified, high-performance protective apparel across industrial environments. OSHA’s 12% rise in hazardous-chemical-related citations in 2023 underscores the growing pressure on employers to prevent worker exposure and invest in compliant protective solutions. This regulatory momentum directly accelerates procurement, particularly in high-risk sectors where chemical, biological, or toxic hazards are prevalent.

Parallel to regulatory pressure, the expansion of high-risk industrial sectors—including pharmaceuticals, oil & gas, and emergency response—continues to fuel market growth. The IEA’s report of a 15% increase in global oil and gas exploration investment between 2022 and 2025 highlights the intensified handling of hazardous substances, while WHO projections show continued pharmaceutical manufacturing growth in emerging markets, reinforcing the need for stringent occupational safety controls.

Adding to these forces, rapid technological advancements in materials science are reshaping product performance. Innovations in polymer blends, breathable membrane systems, and next-generation PVC and PP fabrics now deliver up to 35% longer service life, improved comfort, and superior resistance properties. These breakthroughs not only address evolving end-user expectations but also support premiumization and long-term market expansion.

Restraint - High Cost of Advanced Protective Clothing

The adoption of advanced chemical protective clothing is significantly constrained by high costs and ongoing raw material volatility. Cutting-edge protective apparel designed with multilayer barrier technologies, specialty coatings, and high-performance finishes is priced 20% to 40% higher than traditional alternatives, according to U.S. Department of Labor (DOL) data. This elevated cost structure creates substantial pressure on procurement budgets, particularly for small and medium-sized enterprises that already operate within tight financial limits. As a result, the market sees uneven adoption, with advanced protective solutions remaining more accessible to heavily regulated industries, multinational corporations, or organizations with strong compliance-driven budgets.

Compounding the cost challenge are persistent supply chain disruptions and fluctuations in raw material prices. Specialty polymers and synthetic rubber—critical inputs for manufacturing chemical protective clothing—are highly vulnerable to geopolitical tensions, trade restrictions, and global logistics constraints. In 2022, supply interruptions contributed to a sharp 15% year-over-year increase in polyurethane prices, as reported by U.N. Comtrade, further heightening production costs and limiting availability in cost-sensitive markets. These combined factors hinder pricing stability and create barriers for widespread adoption, especially across developing regions where resource limitations and inconsistent supply networks make procurement more challenging.

Chemical Protective Clothing Market Trends and Opportunities

The COVID-19 pandemic fundamentally elevated organizational prioritization of worker safety, extending beyond pandemic-specific requirements to permanent systemic changes in occupational health practices. Healthcare systems globally recognize enhanced PPE deployment as essential infrastructure, with World Health Organization guidelines establishing minimum protective equipment stockpiles for hospitals and medical facilities. The healthcare sector expenditure on protective clothing increased 340% from 2019-2022, establishing higher baseline procurement levels expected to persist.

Developing countries are systematically upgrading healthcare worker protection standards to align with WHO guidelines, creating substantial procurement opportunities. Pharmaceutical manufacturing facilities have correspondingly expanded protective equipment investments, recognizing that worker illness and absenteeism directly impact production capacity. This structural shift toward elevated safety consciousness represents a permanent market demand increase, offering manufacturers sustained revenue expansion opportunities.

Category-wise Analysis

Type of Clothing Insights

Durable chemical protective clothing remains the leading segment, consistently holding over 60% of global revenue share throughout the forecast period. These reusable garments are engineered for repeated use in high-risk industrial environments such as pharmaceutical production units, chemical processing plants, and oil and gas operations where workers face continuous chemical exposure. Their reinforced construction, thicker materials, and advanced seam technologies deliver higher durability and performance reliability, justifying their premium price range of US$200–500 per suit.

For industries employing large workforces, durable protective clothing offers strong lifecycle cost advantages, as the cost per use declines significantly across 50–200 wearing cycles. Standardization by pharmaceutical companies and petrochemical refineries further drives demand, while replacement cycles averaging 18–36 months ensure a stable and recurring revenue flow for manufacturers.

In contrast, disposable chemical protective clothing is the fastest-growing category, rapidly expanding due to heightened healthcare activity and stringent single-use safety protocols designed to eliminate cross-contamination. Hospitals, diagnostic centers, and pharmaceutical labs increasingly rely on disposable suits for infection control, emergency chemical exposure handling, and contamination-free workflows. This segment is projected to grow at a robust CAGR of over 14.2% from 2026 to 2033, far surpassing the 10.1% growth rate of durable clothing.

The economies of scale have lowered disposable suit prices from US$35–45 in 2020 to US$15–25 by 2026, making them more accessible for budget-conscious organizations. With strong government healthcare investments in emerging markets, disposable protective clothing is expected to capture 38–42% market share by 2033, reflecting a clear shift toward convenience and infection-control-oriented safety practices.

Material Type Insights

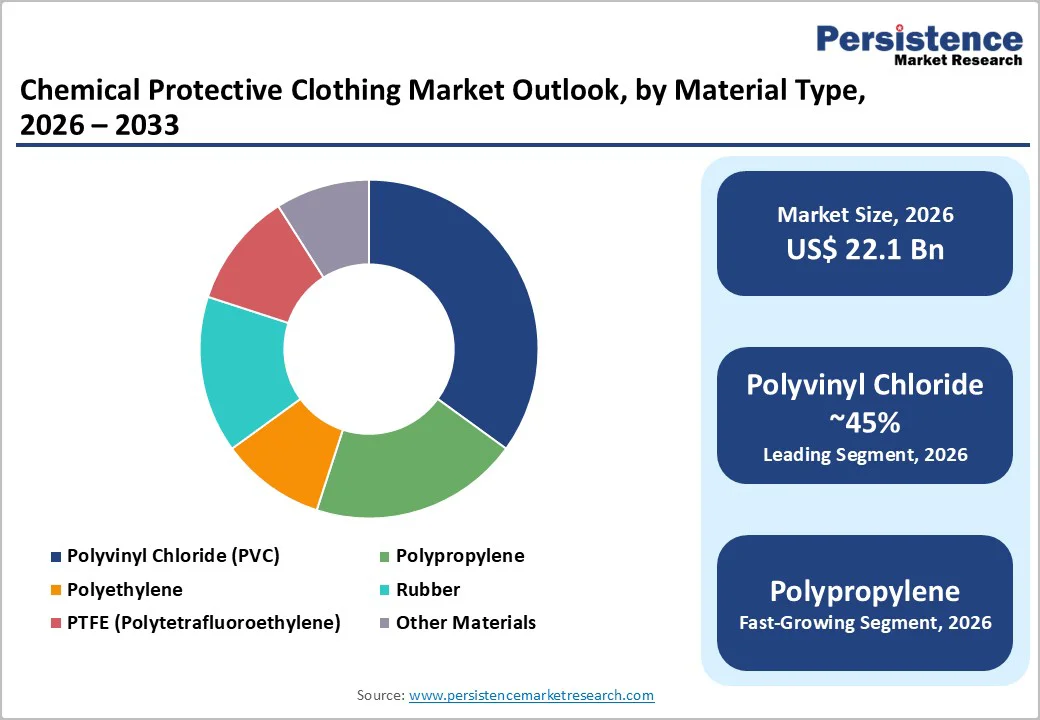

Polyvinyl Chloride (PVC) remains the leading material in the protective clothing market, consistently accounting for more than 45% of total revenue share throughout the forecast period. Its dominance is supported by mature global manufacturing infrastructure, cost-efficiency, and strong chemical resistance against inorganic acids, bases, and petroleum-derived substances—qualities that make PVC the preferred choice for pharmaceutical, industrial, and chemical processing applications. Extensive supplier networks ensure stable raw material availability and competitive pricing, while the material’s inherent flexibility allows manufacturers to design customized garments with reinforced seams, secure closures, and accessory integration. Additionally, PVC’s long-standing regulatory acceptance in North American and European industrial safety standards reinforces its position as the most reliable and widely adopted protective clothing material.

In contrast, polypropylene represents the fastest-growing material category, driven by increasing demand for breathable, lightweight, and comfort-enhancing protective garments. Its superior moisture management enables extended wear in high-temperature or physically demanding environments, significantly improving worker compliance and reducing fatigue. Polypropylene is particularly favored in the healthcare sector for its strong protection against biological hazards and comfort advantages over traditional materials.

Ongoing advancements, including multilayer polypropylene blends, integrated filtration layers, and next-generation nanofiber or electrospun polymer technologies, are expanding its applicability across high-performance industrial safety segments. As a result, polypropylene’s market share is projected to rise from 18% in 2020 to nearly 28–32% by 2033, supported by sustained healthcare demand and broader industrial adoption.

Material Type Insights

The pharmaceutical industry remains the leading end-use segment for protective clothing, consistently accounting for over 30% of total revenue share. Its dominance is driven by stringent regulatory oversight, including FDA and EMA Good Manufacturing Practice (GMP) requirements that mandate high levels of worker protection and contamination control. Facilities handling active pharmaceutical ingredients (APIs), potent compounds, and sensitizing materials rely heavily on certified protective clothing to ensure both employee safety and regulatory compliance. Expansion of pharmaceutical manufacturing hubs across Asia Pacific, alongside annual industry growth projections of 7–9% through 2033, reinforces steady and price-insensitive demand for high-performance protective garments.

Conversely, the oil and gas industry represents the fastest-growing segment, driven by rising petroleum consumption in emerging markets and increasingly rigorous safety protocols. Workers in extraction, refining, and distribution face chronic exposure to volatile organic compounds, hydrogen sulfide, and flammable chemicals, necessitating advanced protective clothing. Regulatory bodies such as OSHA and European safety authorities enforce mandatory equipment standards, while offshore operations demand premium-grade protection due to extreme environmental risks. Rapid industry expansion across Southeast Asia and the Eastern Mediterranean, coupled with deep-water and unconventional exploration activities, is propelling protective clothing demand at an exceptional CAGR of 13.8% between 2026 and 2033, outpacing all other end-use industries.

Regional Insights and Trends

North America Chemical Protective Clothing Market Trends

North America dominates the global protective clothing market with over 40% revenue share, driven primarily by the United States. The mature industrial ecosystem, stringent regulatory frameworks, and a deeply embedded organizational safety culture has designed sustainability in the U.S. OSHA compliance mandates, FDA protocols for pharmaceutical manufacturing, and EPA regulations for hazardous materials handling collectively ensure sustained institutional demand for certified protective apparel.

The U.S. pharmaceutical sector—valued at more than US$600 billion—requires continuous investment in protective garments to meet GMP standards, while the petrochemical hub along the Gulf Coast, producing over 400 million metric tons annually, relies heavily on high-performance protective equipment. Growth is further strengthened by increasing regulatory penalties for non-compliance, the rapid adoption of technologically advanced protective materials offering superior performance, and permanently elevated healthcare PPE procurement levels following pandemic-era infrastructure upgrades. The competitive landscape remains moderately concentrated, with leading manufacturers accounting for 45–55% market share and investing heavily in smart textiles, chemical-sensing fabrics, and material innovations. Strategic acquisitions and increased private equity funding between 2023 and 2026 continue to reinforce market consolidation and accelerate technological development.

Europe Chemical Protective Clothing Market Trends

Europe stands as the second-largest market, contributing over 20% of global revenue and projected to grow at a strong CAGR of 12.5%. This growth is supported by stringent occupational safety directives, mature manufacturing ecosystems, and a long-standing institutional emphasis on worker protection rooted in social partnership models. Germany remains the regional leader, backed by Europe’s largest industrial base and a robust chemical manufacturing sector employing more than 410,000 workers who require high-performance protective clothing.

The United Kingdom continues to generate steady demand through its established pharmaceutical and chemical industries, while France and Spain show consistent growth driven by industrial diversification and the expansion of pharmaceutical production capabilities. The regulatory landscape plays a pivotal role in shaping market dynamics, with the EU Personal Protective Equipment Regulation (EU 2016/425) enforcing strict conformity assessments, CE marking, and performance testing protocols that raise entry barriers and support premium product pricing. Additional directives, such as the EU Chemical Agents Directive (98/24/EC), reinforce institutional compliance obligations, further stimulating demand.

Market competition remains fragmented, with numerous regional and specialized manufacturers catering to country-specific regulations and application needs. Limited consolidation, strong sustainability mandates, and circular economy policies fuel innovation in recyclable materials, while German and Swiss manufacturers continue to dominate technological advancements in high-performance protective clothing design.

Competitive Landscape

The global chemical protective clothing market exhibits moderate consolidation, with the top five manufacturers holding nearly 52–58% of the total market share. These leading multinational corporations benefit from robust distribution networks, strong R&D capabilities, and deep regulatory compliance expertise, enabling them to maintain dominant positions. Competitive differentiation increasingly stems from advancements in material science, supporting the development of premium, high-performance protective clothing.

While global players strengthen their foothold through technology leadership, regional manufacturers remain competitive by offering cost-effective products tailored to local needs and leveraging strong customer relationships. The overall market structure reflects a mature yet steadily expanding industry, where consolidation trends favor established players. High entry barriers—such as stringent compliance norms, significant capital investments, and the need for extensive distribution networks—limit new entrants. Additionally, regional regulatory variations and localized performance requirements create fragmented demand patterns, sustaining regional strongholds for specialized manufacturers.

Key Industry Developments

- In November 2025 DuPont announced the launch of Tyvek® APX™, an advanced disposable chemical-protective garment fabric presented at A+A 2025 in Düsseldorf, Germany. Developed through extensive scientific research and close collaboration with end users, Tyvek® APX™ is described as the most advanced iteration of the Tyvek® material to date, offering significantly enhanced breathability while preserving high levels of durability and protection.

- In October 2025, Governor Jenniffer González Colón and DDEC Secretary Sebastián Negrón Reichard announced that Bethel Protective Systems, LLC, a U.S.-based textile manufacturer, would relocate part of its New Jersey operations to Barceloneta, Puerto Rico. The company is set to invest $8 million in establishing a facility at the Palmas Altas Industrial Park, a project expected to create 400 new jobs over two years.

- In September 2025, Lakeland Industries reported that it had completed the acquisitions of Arizona PPE Recon and California PPE Recon for a combined $9.5 million. The acquisitions expand Lakeland’s presence in the fire safety equipment maintenance market, despite the company experiencing a nearly 27% decline in its stock value over the previous six months, as noted by InvestingPro.

Companies Covered in Chemical Protective Clothing Market

- Honeywell International Inc.

- Lakeland Inc.

- W. L. Gore & Associates, Inc.

- PBI Performance Products, Inc.

- TenCate Protective Fabrics

- Kimberly-Clark Corporation

- Ansell Microgard Ltd.

- DuPont

- Bennett Safetywear Ltd.

- TEIJIN LIMITED

- Udyogi

- Sanctum Work Wear Pvt. Ltd.

- Derekduck Industries Corp.

- Protective Industrial Products

- Other Market Players

Frequently Asked Questions

The Chemical Protective Clothing market is estimated to be valued at US$ 1.6 Bn in 2026.

The primary demand driver for the chemical protective clothing market is the tightening of global occupational safety regulations, particularly across chemical manufacturing, pharmaceuticals, oil & gas, and industrial processing sectors.

In 2026, the North America region will dominate the market with an exceeding 30% revenue share in the global Chemical Protective Clothing market.

Among material types, polyvinyl chloride (PVC) has the highest preference, capturing beyond 45% of the market revenue share in 2026, surpassing other material types.

Honeywell International Inc., Lakeland Inc., W. L. Gore & Associates, Inc., Kimberly-Clark Corporation, DuPont, Bennett Safetywear Ltd., and TEIJIN LIMITED are a few leading players in the Chemical Protective Clothing market.