- Specialty & Fine Chemicals

- Dechlorination Chemicals Market

Dechlorination Chemicals Market Size, Share, and Growth Forecast 2026 - 2033

Dechlorination Chemicals Market by Chemical Type (Sulphur Based Chemicals: Sodium Metabisulfite, Sodium Sulfite, Sodium Bisulfite; Activated Carbon Based Chemicals: Drinking Water Grade, Waste Water Grade; Others), Form (Liquid, Solid), End Use (Water Treatment, Food and Beverage, Textile, Miscellaneous), by Regional Analysis, 2026 - 2033

Dechlorination Chemicals Market Size and Trend Analysis

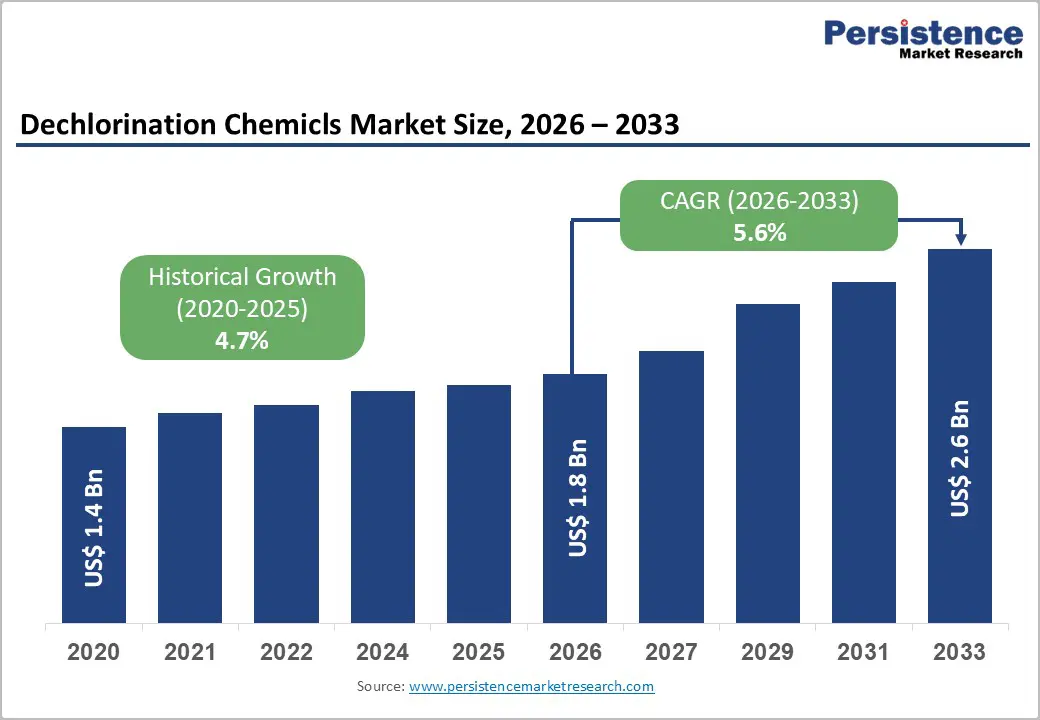

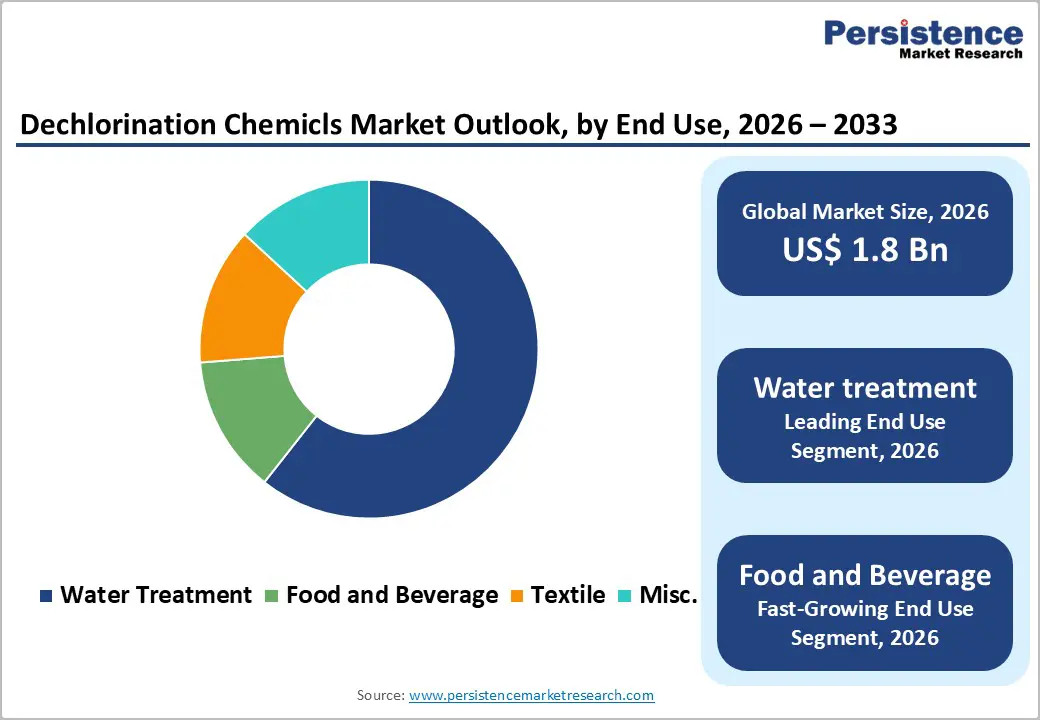

The global dechlorination chemicals market size is expected to be valued at US$ 1.8 billion in 2026 and projected to reach US$ 2.6 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

The dechlorination chemicals market is experiencing robust growth, primarily fueled by escalating global demand for safe potable water and increasingly stringent effluent discharge regulations enforced by environmental agencies worldwide. Regulatory mandates such as the U.S. Environmental Protection Agency (EPA) guidelines on chlorine discharge limits and the European Union (EU) Urban Wastewater Treatment Directive are compelling water utilities, municipalities, and industrial facilities to adopt reliable dechlorination solutions. Simultaneously, rapid urbanization and expanding industrial base across the Asia Pacific region are opening new high-volume consumption avenues for sodium metabisulfite, sodium sulfite, and activated carbon-based dechlorination chemicals.

Key Industry Highlights

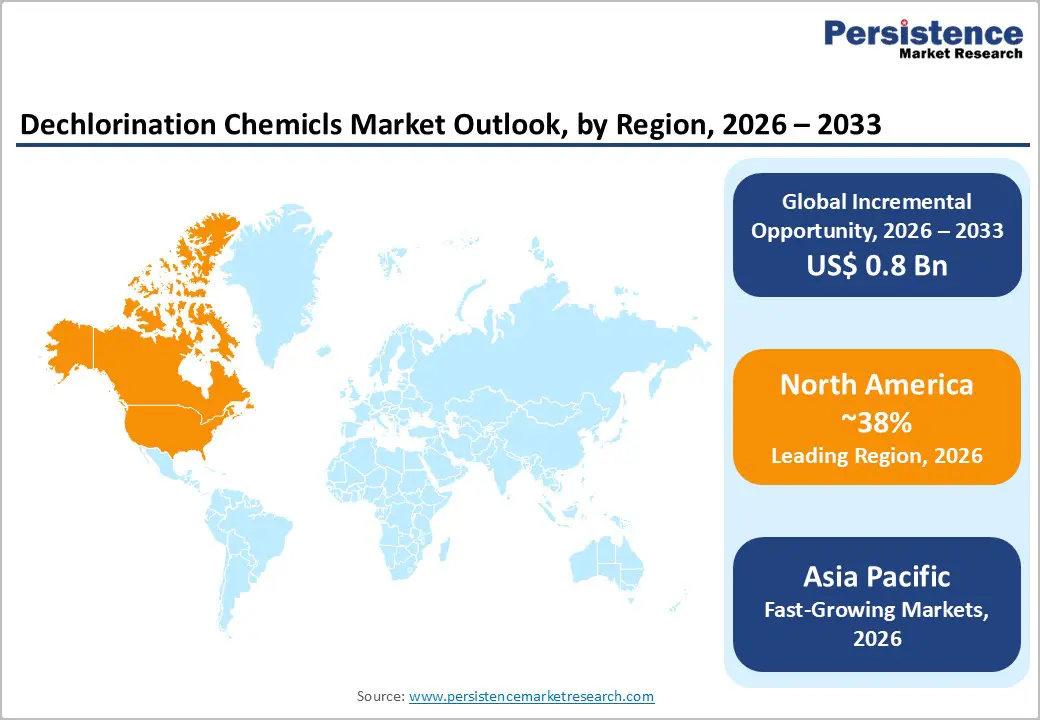

- Leading Region: North America dominates the global dechlorination chemicals market with approximately 38% share in 2025, driven by the U.S. EPA regulatory mandates, over 148,000 public water systems, and mature water treatment infrastructure.

- Fastest Growing Region: Asia Pacific is set to record the highest CAGR of 6.8% through 2033, fueled by China's wastewater infrastructure expansion, India's AMRUT 2.0 program, and rising industrial water treatment demand across ASEAN nations.

- Dominant Chemical Type Segment: Sulphur-based chemicals, led by sodium metabisulfite, command approximately 55% market share in 2025, owing to cost-effectiveness, regulatory acceptance, and compatibility with automated municipal water dosing systems endorsed by AWWA.

- Fastest Growing Chemical Type Segment: Activated carbon-based dechlorination chemicals are projected to grow at the fastest CAGR through 2033, driven by demand for simultaneous micropollutant removal and dechlorination in advanced water treatment facilities in Europe and North America.

- Key Opportunity: Expanding global food processing output and rapidly growing aquaculture production, surpassing 90 million metric tons in 2022 per FAO, represent high-growth white spaces for food-grade and aquaculture-grade dechlorination chemical specialties.

| Key Insights | Details |

|---|---|

| Dechlorination Chemicals Market Size (2026E) | US$ 1.8 Billion |

| Market Value Forecast (2033F) | US$ 2.6 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.6% |

| Historical Market Growth (2020 - 2025) | 4.7% |

Market Dynamics

Drivers - Rising Stringency of Water Quality Regulations and Discharge Norms

One of the most consequential drivers for the dechlorination chemicals market is the tightening of water quality regulations globally. The World Health Organization (WHO) recommends a maximum residual chlorine concentration of 5 mg/L in drinking water, while many national regulators set even more stringent thresholds. The U.S. EPA under the Safe Drinking Water Act and the Clean Water Act mandates dechlorination of effluents before discharge into receiving water bodies, particularly for municipal wastewater treatment plants. In the European Union, the revised Urban Wastewater Treatment Directive (2023/2184/EU) imposes stricter limits on micropollutants and residual disinfectants in treated effluent. These evolving regulatory frameworks are compelling water utilities and industrial plants in over 180 countries to scale up their dechlorination chemical procurement, directly reinforcing sustained market demand.

Rapid Expansion of Water and Wastewater Treatment Infrastructure

Global investment in water and wastewater treatment infrastructure is accelerating at an unprecedented pace, serving as a pivotal demand catalyst for dechlorination chemicals. According to the United Nations Environment Programme (UNEP), over 2.2 billion people still lack access to safe drinking water, prompting governments worldwide to commission large-scale water treatment projects. The Asian Development Bank (ADB) estimated that Asia alone requires water infrastructure investment of approximately US$ 800 billion by 2030 to meet sustainable development goals. In the United States, the Infrastructure Investment and Jobs Act (2021) allocated US$ 55 billion specifically for clean water and wastewater improvements. Each new treatment plant and upgrade project increases the baseline consumption of dechlorination agents such as sodium bisulfite and activated carbon, structurally expanding the addressable market for years to come.

Market Restraints

Volatile Raw Material Prices and Supply Chain Disruptions

The dechlorination chemicals market faces a persistent headwind from the volatility of key raw material prices, particularly sulfur derivatives used to manufacture sodium metabisulfite and sodium sulfite. Sulfur prices are intrinsically linked to oil and gas refining activity; the U.S. Energy Information Administration (EIA) reported significant price swings of over 30% in elemental sulfur during 2021-2023 owing to post-pandemic supply chain bottlenecks. These cost fluctuations squeeze manufacturer margins and can translate into unpredictable pricing for end users, especially smaller municipal operators with fixed procurement budgets. Supply concentration among a handful of global chemical suppliers further amplifies this vulnerability.

Environmental and Handling Concerns Associated with Chemical Dosing

Despite their efficacy, sulphur-based dechlorination chemicals pose inherent handling and storage challenges that can restrain adoption, particularly among smaller operators. Sodium metabisulfite and sodium bisulfite can decompose upon exposure to moisture and air, releasing sulfur dioxide, a toxic gas regulated by the U.S. Occupational Safety and Health Administration (OSHA) with a permissible exposure limit of 2 ppm. Improper dosing can also lead to dissolved oxygen depletion in receiving water bodies, causing ecological harm. These considerations necessitate investment in specialized storage, dosing equipment, and operator training, adding to total cost of ownership and presenting barriers to market penetration in cost-sensitive regions.

Opportunities - Growing Demand from the Food and Beverage Sector for Food-Grade Dechlorination

The food and beverage industry represents a rapidly expanding opportunity for dechlorination chemicals, particularly food-grade sodium metabisulfite and activated carbon solutions. Chlorinated municipal water used in food processing can adversely affect taste, color, and microbial quality of products, making pre-treatment with dechlorination chemicals a critical step in quality assurance. The Food and Agriculture Organization (FAO) and WHO Codex Alimentarius Commission recognize sodium metabisulfite as a permitted food additive (E223) with specific applications in dechlorination and preservation. Global food processing output is projected to increase by over 3% annually through 2030, according to the FAO, and the proliferation of bottled water, beverages, and packaged food manufacturing plants in emerging markets will proportionally drive uptake of specialized dechlorination chemical grades. Companies offering certified food-grade products with documented traceability will be best positioned to capture this segment.

Emerging Opportunities in Industrial Aquaculture and Environmental Restoration

The global aquaculture industry presents a high-growth, underserved opportunity for dechlorination chemical suppliers. Aquaculture facilities rely on dechlorinated water to protect fish, shrimp, and other aquatic organisms from chlorine toxicity at concentrations as low as 0.003 mg/L, far below municipal water standards. The Food and Agriculture Organization (FAO) estimates global aquaculture production surpassed 90 million metric tons in 2022, with the sector growing at approximately 5%-6% per year. Nations including China, India, Vietnam, and Norway are heavily investing in sustainable aquaculture, creating sustained demand for sodium thiosulfate and sodium bisulfite in fish hatcheries and grow-out facilities. Environmental restoration projects, including river dechlorination following industrial spills, additionally represent a niche but growing application for activated carbon-based chemicals in the coming years.

Category-wise Analysis

Chemical Type Insights

Sulphur-based dechlorination chemicals account for the leading share of approximately 55% of the global dechlorination chemicals market in 2025, with sodium metabisulfite being the dominant product. This chemical type's market leadership is attributable to its high dechlorination efficiency, cost-effectiveness, and broad regulatory acceptance across water treatment, food processing, and industrial applications. The American Water Works Association (AWWA) widely endorses sodium metabisulfite and sodium bisulfite as standard dechlorination agents for potable water systems. Their well-established supply chains, ease of storage in both solid and liquid forms, and compatibility with existing dosing equipment have entrenched sulphur-based chemicals as the default choice among municipal water utilities and large-scale industrial operators globally, reinforcing their market dominance over activated carbon alternatives.

Form Insights

Liquid dechlorination chemicals hold a commanding share of approximately 62% of the global market by form in 2025. Liquid formulations of sodium bisulfite and sodium metabisulfite are preferred by large-scale water treatment plants and industrial facilities due to their ease of handling, direct pump-and-dose applicability, and elimination of dissolution step required for solid forms. The Water Environment Federation (WEF) highlights that automated chemical dosing systems, now standard in over 70% of mid-to-large wastewater treatment plants in developed countries, are predominantly engineered around liquid chemical feeds. Liquid forms also reduce operator exposure during chemical transfer, aligning with workplace safety standards set by OSHA and equivalent bodies in Europe, making them the preferred commercial format for procurement in the water treatment end-use segment.

End-user Insights

Water treatment is the dominant end-use segment, representing approximately 60% of the global dechlorination chemicals market share in 2025. Municipal drinking water production and wastewater discharge operations are the largest consumers of dechlorination agents, driven by mandatory compliance with chlorine residual and effluent discharge standards enforced by regulatory bodies such as the U.S. EPA, the European Environment Agency (EEA), and national water boards across Asia and Latin America. According to the UN-Water Global Analysis and Assessment of Sanitation and Drinking-Water (GLAAS) 2023 report, over 5 billion people are served by managed drinking water services that employ chlorination-dechlorination cycles, underscoring the structural demand anchor this segment provides for the dechlorination chemicals market.

Regional Insights

North America Dechlorination Chemicals Market Trends and Insights

North America leads the global dechlorination chemicals market with approximately 38% market share, underpinned by a mature water infrastructure, robust regulatory enforcement, and high per-capita water treatment capacity. The United States, anchored by the Safe Drinking Water Act (SDWA) and Clean Water Act (CWA) compliance requirements enforced by the U.S. EPA, represents the single largest national market for dechlorination chemicals. The American Water Works Association (AWWA) estimates there are over 148,000 public water systems in the U.S. alone, a substantial proportion of which employ sodium metabisulfite or activated carbon for dechlorination in treatment trains.

The region is also home to a vibrant innovation ecosystem, with companies investing in advanced granular activated carbon (GAC) systems for simultaneous dechlorination and micropollutant removal. Canada's Wastewater Systems Effluent Regulations (WSER) under the Fisheries Act similarly mandate dechlorination of chlorinated effluents prior to discharge into natural water bodies. Growing adoption of smart dosing technologies and IoT-based chemical management systems is further elevating operational efficiency and supporting premium product demand in the North American market.

Europe Dechlorination Chemicals Market Trends and Insights

Europe represents the second-largest regional market for dechlorination chemicals, driven by harmonized environmental standards under the EU Water Framework Directive and revised Urban Wastewater Treatment Directive (2023/2184/EU). Germany, the U.K., France, and Spain are key consuming nations, with strong demand from municipal water utilities and food and beverage processors. Germany alone operates over 6,000 public water supply systems, with the German Technical and Scientific Association for Gas and Water (DVGW) actively guiding best practices for dechlorination chemical use in potable water production.

The U.K.'s Water Industry Act 1991 and updated Water Framework Regulations 2017 enforce strict effluent quality norms, sustaining steady demand for sodium bisulfite and activated carbon. France and Spain are intensifying investments in wastewater reuse infrastructure to address water scarcity, creating incremental dechlorination demand. EU REACH regulations govern the safe use and trade of dechlorination chemicals across member states, ensuring consistent product quality standards and acting as an indirect driver for premium, compliant chemical sourcing across the region.

Asia Pacific Dechlorination Chemicals Market Trends and Insights

Asia Pacific is the fastest-growing regional market with a projected CAGR of 6.8% between 2026 and 2033 for dechlorination chemicals, propelled by rapid urbanization, expanding industrial activity, and significant government investment in water infrastructure. China, the region's largest market, is implementing its 14th Five-Year Plan (2021-2025) with ambitious targets for upgrading urban water supply and wastewater treatment capacity. The Ministry of Housing and Urban-Rural Development (MOHURD) of China reported that sewage treatment capacity reached over 210 million m³/day in 2022, requiring substantial volumes of dechlorination agents for effluent compliance.

India's National Mission for Clean Ganga (NMCG) and AMRUT 2.0 urban infrastructure scheme are channeling significant public funds into sewage treatment plant (STP) upgrades, creating recurring dechlorination chemical demand. Japan's mature treatment market prioritizes high-purity, specialty-grade dechlorination products aligned with JIS (Japanese Industrial Standards) requirements. ASEAN nations such as Vietnam, Indonesia, and Thailand are building new treatment capacity at pace, while benefiting from competitive local manufacturing of sulphur-based chemicals, making Asia Pacific the most dynamic regional growth frontier for dechlorination chemical suppliers through 2033.

Competitive Landscape

The global dechlorination chemicals market exhibits a moderately fragmented structure, characterized by the presence of multinational chemical producers, specialized water treatment solution providers, and regional manufacturers serving localized demand. Competitive intensity is shaped by pricing pressures, regulatory compliance requirements, and the need for reliable supply chains. Large integrated players benefit from economies of scale and backward integration into key raw materials, supporting cost efficiency and margin stability.

Strategically, companies are focusing on capacity expansion, portfolio diversification, and geographic penetration into high-growth emerging markets. Product differentiation is increasingly centered on certified food-grade and aquaculture-grade formulations, enhanced performance chemistries, and value-added technical services that strengthen customer retention. Firms are also investing in application expertise, distribution partnerships, and localized manufacturing to improve responsiveness. Mergers and acquisitions continue to play a critical role in expanding regional footprint, strengthening distribution networks, and achieving operational scale advantages in a competitive global environment.

Key Developments:

- December 2025: Hawkins, Inc. completed the acquisition of Redbird Chemical, Inc. assets in eastern Texas, expanding its water treatment and industrial chemicals footprint while integrating Redbird’s distribution network and local team to accelerate regional growth.

- September 2025: Arxada’s Enviro Tech division launched Peragreen® 26WW, a smart peracetic acid microbial control solution for medium- to large-scale municipal wastewater systems, offering cost-effective, environmentally friendly treatment and reduced reliance on chlorine-based disinfection.

- June 2025: Osmonix expanded into Mexico by launching Osmonix S.A. de C.V., establishing a regional office to deliver its high-performance membranes, specialty chemicals, and water treatment solutions locally while supporting industrial clients in mining, automotive, steel, and manufacturing sectors.

Companies Covered in Dechlorination Chemicals Market

- Solvay SA

- One Equity Partners

- Lenntech B.V.

- Jay Dinesh Chemicals

- INEOS CALABRIAN

- Hydrite Chemical Co.

- Hawkins, Inc.

- Grasim Industries Limited (Aditya Birla Group)

- ESSECO USA LLC

- Carbotecnia

- BASF SE

- Airedale Group

- Univar Solutions

- Thatcher Company

- Kanto Chemical Co., Inc.

- Holland Company

- Toray Industries, Inc.

- Accepta Water Treatment

Frequently Asked Questions

The dechlorination chemicals market is estimated at US$ 1.8 billion in 2026.

Stringent water regulations and expanding water treatment infrastructure drive demand.

North America leads with around 38% share in 2025.

Food processing and aquaculture sectors offer strong growth opportunities.

Major players include BASF SE, Solvay SA, Grasim Industries, INEOS CALABRIAN, and Hawkins Inc.