- Specialty & Fine Chemicals

- U.S. Perfume Ingredient Chemicals Market

U.S. Perfume Ingredient Chemicals Market Size, Share, and Growth Forecast 2026 - 2033

U.S. Perfume Ingredient Chemicals Market by Product Type (Essential Oils, Synthetic Aroma Chemicals), Source (Natural, Synthetic, Other), Application (Fine Fragrance, Soaps and Detergents, Personal Care & Cosmetics, Other), and Regional Analysis for 2026 - 2033

U.S. Perfume Ingredient Chemicals Market Size and Trend Analysis

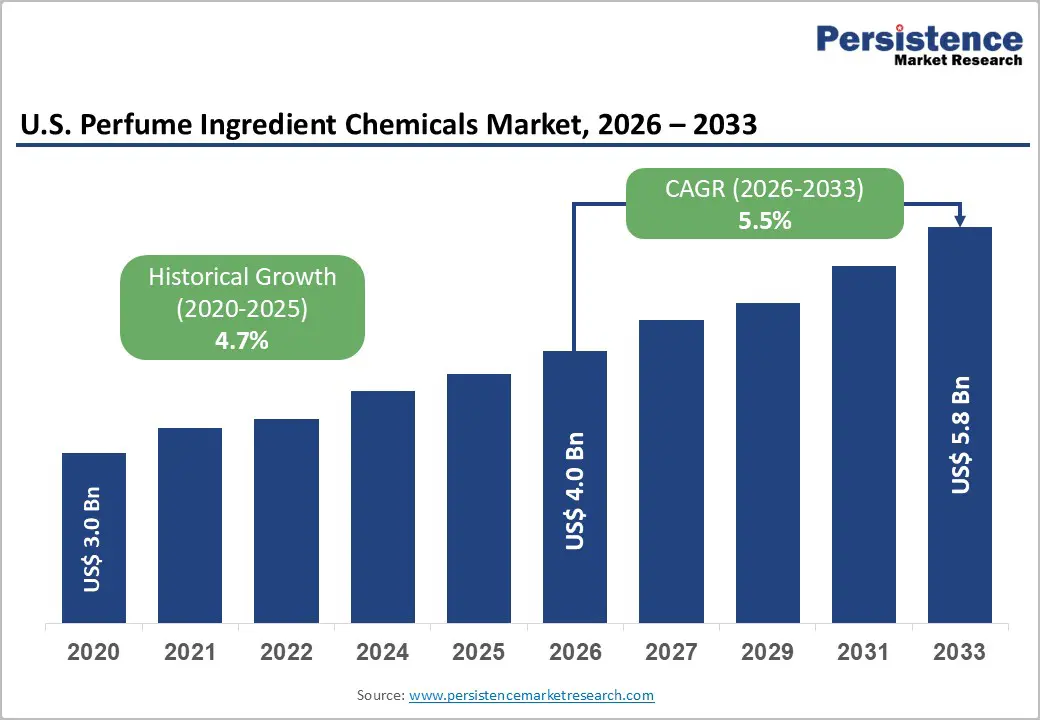

The U.S. perfume ingredient chemicals market is valued at US$ 4.0 Bn in 2026 and is projected to reach US$ 5.8 Bn by 2033, growing at a CAGR of 5.5% between 2026 and 2033.

The market is experiencing robust growth, driven primarily by surging consumer demand for premium, long-lasting fragrances, rising adoption of natural and sustainable aroma chemicals, and expanding personal care and cosmetics sectors across the U.S. The growing shift toward clean-label and eco-certified formulations has accelerated the integration of essential oils and bio-derived aroma chemicals. According to the International Fragrance Association (IFRA), the global fragrance industry registered consistent annual expansion supported by increased premiumization in consumer goods. Additionally, breakthroughs in biotechnology and AI-assisted fragrance formulation are enabling manufacturers to innovate faster, reducing cycle times and improving product performance across fine fragrance, soaps, detergents, and personal care applications.

Key Industry Highlights:

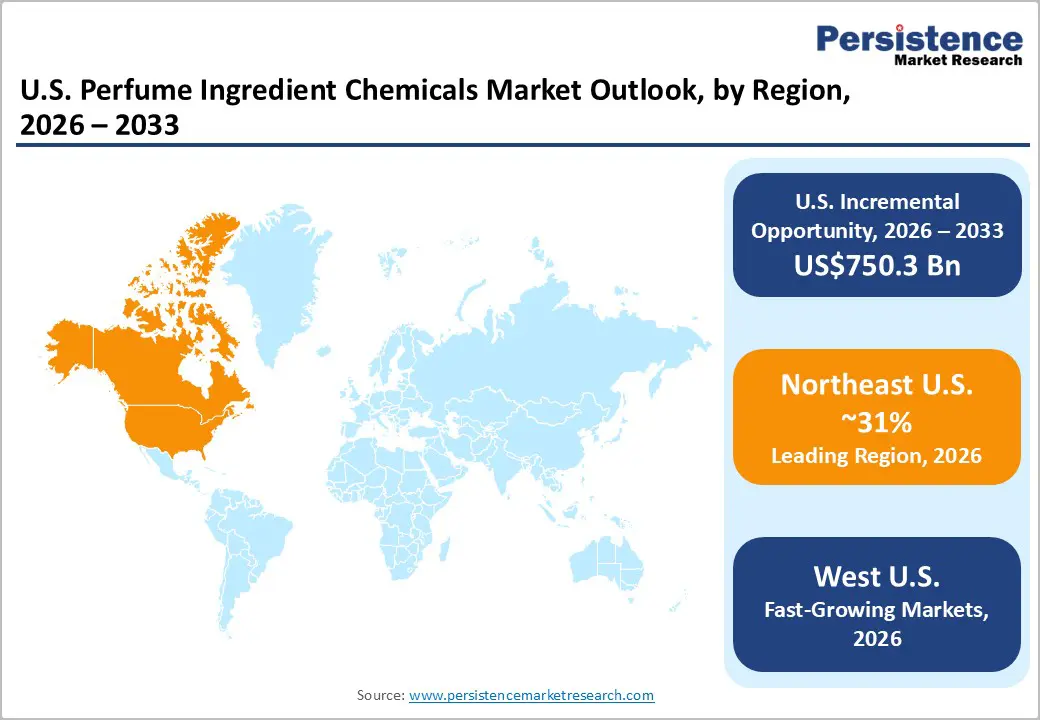

- Leading Region: The Northeast U.S. leads the market, with 31% market share, anchored by IFF's New York headquarters, dense luxury fragrance retail, and strong alignment with FDA cosmetic safety frameworks, driving demand for premium aroma chemicals and essential oils.

- Fastest Growing Region: The West U.S. is the fastest growing region, driven by California's stringent ingredient disclosure mandates, a vibrant wellness culture, and surging demand for certified natural and sustainable fragrance ingredients in clean-label personal care.

- Dominant Segment: Essential oils hold approximately 60% of the product type segment, led by orange, peppermint, and eucalyptus, driven by consumer preference for natural-origin fragrance materials aligned with clean beauty trends.

- Fastest Growing Segment: Fine fragrance is the fastest growing application segment, projected at a CAGR of 7.3%, fueled by premiumization trends, niche perfumery growth, and luxury brand investment in complex multi-note aroma chemical formulations.

- Key Market Opportunity: The development of EPA Safer Choice-certified, biodegradable aroma chemicals using biotechnology presents the market's most significant opportunity, unlocking demand from sustainability-mandated consumer goods companies and eco-conscious fine fragrance brands.

| Key Insights | Details |

|---|---|

| U.S. Perfume Ingredient Chemicals Market Size (2026E) | US$ 4.0 Bn |

| Market Value Forecast (2033F) | US$ 5.8 Bn |

| Projected Growth CAGR (2026 - 2033) | 5.5% |

| Historical Market Growth (2020 - 2025) | 4.7% |

Market Dynamics

Drivers - Rising Consumer Demand for Natural and Premium Fragrances

One of the most compelling growth drivers for the U.S. Perfume Ingredient Chemicals Market is the accelerating consumer preference for natural, premium, and sustainable fragrance formulations. According to the U.S. Personal Care Products Council, the natural personal care segment in the U.S. has grown at a compounded pace well above the overall market average, reflecting a structural shift in consumer behavior. The Natural Perfumers Guild has reported a rise of over 20 million units in demand for perfumes containing natural extracts and essential oils over the past five years.

Rising disposable incomes, growing awareness about synthetic chemical allergies, and the proliferation of clean-beauty movements such as "EWG Verified" and "COSMOS Organic" certifications are compelling fragrance manufacturers to reformulate with high-purity essential oils, including orange, eucalyptus, and peppermint. Leading brands are rapidly expanding their natural aroma chemical portfolios to capitalize on this demand, directly fueling ingredient procurement and market expansion.

Technological Advancements in Fragrance Formulation and Biotechnology

Technological innovation is reshaping the U.S. Perfume Ingredient Chemicals landscape at an unprecedented rate. The integration of artificial intelligence (AI) into scent creation, exemplified by Givaudan's Carto platform and Symrise's Philyra system (co-developed with IBM), is reducing formulation cycles and enabling hyper-personalized scent experiences.

Simultaneously, biotechnology-driven synthesis is producing high-quality aromatic compounds from renewable feedstocks. BASF SE launched Isobionics® Natural beta-Caryophyllene 80 in March 2024, produced entirely from renewable sources using proprietary fermentation technology. Furthermore, nanotechnology applications for encapsulated fragrance delivery are extending ingredient longevity across consumer goods. According to U.S. Patent and Trademark Office (USPTO) filings, fragrance biotechnology patents have seen notable year-on-year growth, underscoring the innovation momentum benefiting ingredient manufacturers and driving market expansion.

Restraints - Volatility in Raw Material Prices and Supply Chain Disruptions

A significant restraint weighing on the U.S. Perfume Ingredient Chemicals Market is the inherent price volatility of natural raw materials. According to the U.S. Department of Agriculture (USDA), prices of certain essential oil feedstocks can fluctuate by up to 50% depending on harvest seasons, climatic disruptions, and geopolitical conditions. Critical natural inputs such as rose, jasmine, and sandalwood are particularly susceptible to supply shocks, with sandalwood scarcity in key production zones inflating procurement costs substantially.

The high cost of natural essences has led approximately 95% of perfume makers to blend synthetic ingredients with essential oils. Such instability compresses manufacturer margins and limits the ability of smaller market participants to sustain consistent product quality.

Stringent Regulatory Compliance and Safety Standards

Increasing regulatory scrutiny presents a persistent barrier for fragrance ingredient manufacturers. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the International Fragrance Association (IFRA) continue to update safety standards for aroma chemicals, restricting or banning certain synthetic compounds linked to allergic reactions and environmental harm. IFRA's 49th Amendment introduced restrictive concentration limits on widely used fragrance molecules, compelling formulators to undertake expensive reformulation exercises.

Compliance processes are resource-intensive and time-consuming, creating a disproportionate burden on mid-sized manufacturers and new entrants. The Research Institute for Fragrance Materials (RIFM) maintains an extensive database that fragrance ingredient manufacturers must continuously reference, adding to regulatory compliance costs and delaying product commercialization timelines.

Opportunities - Growing Demand for Sustainable and Biodegradable Fragrance Ingredients

A transformative opportunity is emerging around the development and commercialization of sustainable, biodegradable fragrance ingredients. As ESG criteria gain traction among U.S. corporate procurement teams and sustainability-focused consumers, ingredient manufacturers that offer certified eco-friendly solutions stand to capture significant market share. DSM-Firmenich AG's EcoScent Compass utilizes AI to evaluate the environmental footprint of each fragrance ingredient, enabling brand partners to align with sustainability targets.

The U.S. Environmental Protection Agency's (EPA) Safer Choice program certifies fragrance components meeting stringent environmental and health safety criteria, creating a powerful commercial incentive for manufacturers offering qualifying ingredients. With Givaudan having launched PlanetCaps™, a biodegradable fragrance capsule, and BASF advancing biomass-balanced production, this opportunity is rapidly transitioning from niche to mainstream across fine fragrance and household care categories.

Accelerating Demand from the Fine Fragrance and Luxury Segment

The fine fragrance segment represents one of the fastest-growing and highest-value opportunities within the U.S. perfume ingredient chemicals market. According to the Fragrance Foundation USA, the U.S. prestige fragrance market experienced strong consecutive years of growth, underpinned by a post-pandemic renaissance in personal luxury spending. The luxury fragrance category is witnessing elevated demand for artisanal, bespoke, and niche perfumes, which require rare and high-quality aroma chemicals and essential oils, significantly higher-value inputs compared to mass-market formulations.

The proliferation of direct-to-consumer (DTC) fragrance brands and the expansion of specialty fragrance retail in the U.S. are amplifying demand for differentiated ingredients. Furthermore, the rise of personalized and custom-blended fragrances, supported by AI-enabled scent design tools, is opening entirely new product development avenues for ingredient suppliers, creating sustained demand momentum through the forecast period.

Category-wise Analysis

Product Type Insights

Essential Oils hold the leading position in the U.S. perfume ingredient chemicals market, commanding approximately 60% of the market share. This dominant position is attributed to the strong and growing consumer preference for natural, botanical, and plant-derived fragrance ingredients, which align with broader clean beauty and wellness trends in the U.S. Essential oils such as Orange, Citronella, Peppermint, and Eucalyptus are extensively utilized across fine fragrances, personal care, aromatherapy, and home care formulations, owing to their diverse and authentic aromatic profiles. Their therapeutic and multi-functional properties further enhance their appeal across both premium and mass-market segments.

The U.S. organic essential oils market has witnessed accelerated growth, supported by the USDA National Organic Program (NOP) certification framework, which has strengthened consumer trust in certified natural fragrance ingredients. Meanwhile, synthetic aroma chemicals, including alcohols, esters, ethers, and ketones, maintain a strong presence, valued for their cost-efficiency, consistency, and formulation versatility across industrial-scale fragrance manufacturing.

Source Insights

In terms of source, Natural aroma chemicals constitute the dominant segment, holding approximately 68% of the market share. This leadership is reinforced by the sustained shift in U.S. consumer sentiment toward eco-conscious, cruelty-free, and sustainably sourced fragrance products. Natural aroma chemicals derived from flowers, plants, and fruits offer intricate and authentic scent profiles that are highly valued in premium fragrance formulations, particularly in fine fragrances and prestige personal care. Regulatory momentum, including evolving FDA cosmetic ingredient disclosure mandates under MoCRA 2022, is further compelling brands to prioritize ingredient transparency, boosting demand for natural-sourced, traceable aroma materials.

The Synthetic segment, while commanding a smaller value share, remains indispensable for large-scale fragrance manufacturing due to its superior cost-efficiency, reproducibility, and supply chain stability, particularly in mass-market soaps, detergents, and household care applications, where consistent scent performance at high volumes is essential.

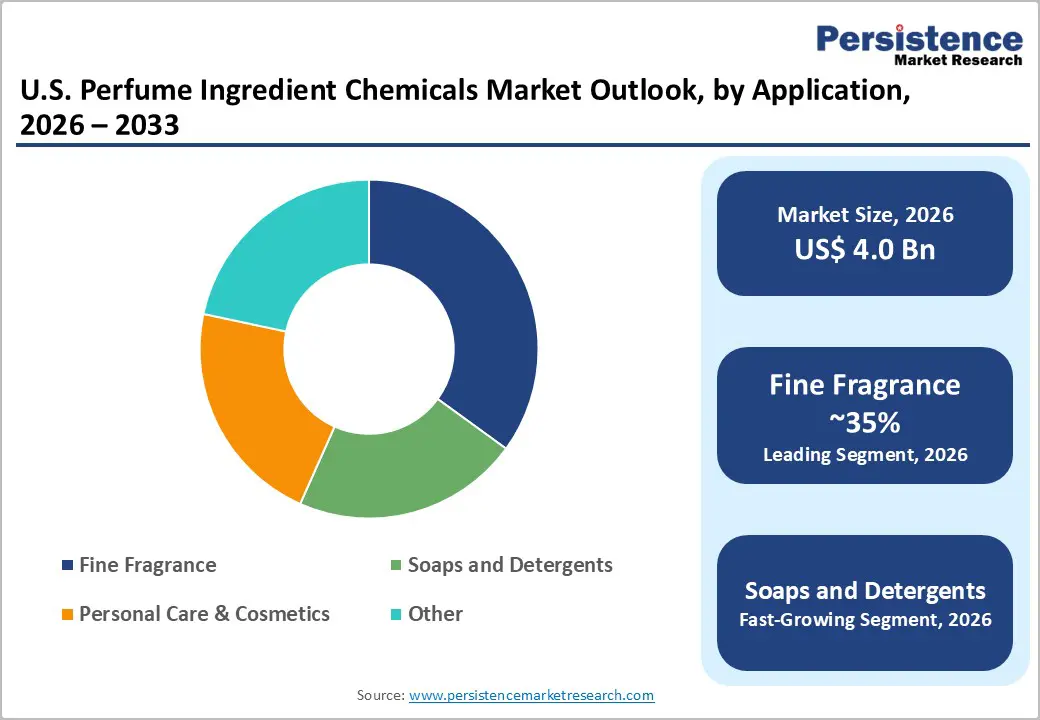

Application Insights

Across application segments, fine fragrance leads the U.S. perfume ingredient chemicals market with an estimated share of approximately 35%, driven by the strong and growing demand for premium, luxury, and artisanal perfumes in the U.S. consumer market. Fine fragrances typically incorporate complex blends of high-quality essential oils, rare aroma chemicals, and advanced fixatives, making this segment the highest-value consumer of premium perfume ingredients. The Fragrance Foundation USA reported continued expansion of the prestige perfume category in the U.S., supported by the resurgence of personal luxury spending and the rapid proliferation of niche and indie fragrance houses.

The Soaps and Detergents segment represents the second-largest application, leveraging synthetic aroma chemicals and cost-effective essential oils to deliver consistent, consumer-pleasing scent experiences at high manufacturing volumes. Personal Care & Cosmetics is the fastest-growing application segment, driven by the rapid expansion of scented skincare, haircare, and body care product lines, particularly among millennial and Gen Z consumers who place high value on multisensory product experiences.

Regional Insights

Northeast U.S. Perfume Ingredient Chemicals Trends

The Northeast U.S. leads the U.S. Perfume Ingredient Chemicals Market, with 31% market share, driven by its dense concentration of fine fragrance houses, prestige cosmetic brands, and world-class research institutions. New York City, in particular, serves as the creative and commercial epicenter for premium perfumery in North America, hosting the U.S. offices of global leaders, including International Flavors & Fragrances Inc. (IFF), headquartered in New York City. The region's robust retail infrastructure for luxury goods further amplifies ingredient consumption volumes.

From a regulatory perspective, the Northeast benefits from strong alignment with U.S. FDA cosmetic safety frameworks, and state-level sustainability mandates are accelerating the shift toward safer and greener fragrance ingredients. The region's innovation ecosystem, anchored by collaborations between fragrance companies and leading universities, continues to produce breakthrough research in natural extraction technologies, biotechnology, and AI-driven scent formulation, reinforcing the Northeast's position as the market's innovation and consumption leader.

West U.S. Perfume Ingredient Chemicals Trends

The West U.S., encompassing California, Oregon, and Washington, represents the fastest growing region for the U.S. Perfume Ingredient Chemicals Market, driven by the Pacific Coast's vibrant wellness culture, booming natural beauty industry, and a high density of clean-label consumer goods startups. California alone accounts for the largest share of certified organic and natural personal care product launches in the U.S., according to the Organic Trade Association (OTA), fueling elevated demand for essential oils and bio-derived aroma chemicals.

Regulatory harmonization is a key trend in this region, as California's Cleaning Product Right to Know Act and the California Safe Cosmetics Program mandate full fragrance ingredient disclosure, creating incentives for brands and their ingredient suppliers to transition to compliant, traceable materials. This regulatory environment is attracting investment from global fragrance ingredient suppliers seeking to position their IFRA-compliant and EPA Safer Choice-certified ingredient portfolios for the premium West Coast market, making the region a key growth frontier through 2033.

Competitive Landscape

The U.S. Perfume Ingredient Chemicals Market exhibits a moderately consolidated competitive structure, with a tiered hierarchy of global majors, regional specialists, and niche innovators. Leading players, Givaudan SA, IFF, DSM-Firmenich AG, Symrise AG, and BASF SE, collectively hold approximately 65% of the global fragrance ingredients market. Key competitive strategies include strategic M&A activity to broaden natural ingredient portfolios, heavy investment in R&D for biotechnology-derived molecules, and deployment of AI-powered formulation tools. Emerging business models increasingly center on ingredient traceability, carbon footprint labeling, and sustainability certifications as differentiating factors. Regional players such as Agilex Fragrances, Alpha Aromatics®, and Vigon International, LLC. are leveraging agility and customization capabilities to compete in the mid-market segment.

Key Market Developments

- March 2024: BASF SE expanded its Isobionics® portfolio by launching Isobionics® Natural beta-Caryophyllene 80, a natural aroma ingredient produced from renewable resources via proprietary fermentation biotechnology, reinforcing its commitment to sustainable ingredient innovation.

- July 2024: Givaudan SA announced the acquisition of b.kolormakeup & skincare (b.kolor), an innovative Italian cosmetic firm, strategically expanding its Fragrance & Beauty portfolio and strengthening its position in the premium consumer-packaged goods segment.

- May 2025: International Flavors & Fragrances Inc. (IFF) completed the strategic divestiture of its Pharma Solutions business to Roquette, allowing IFF to sharpen its strategic focus on high-growth fragrance and scent ingredient segments aligned with consumer beauty and wellness trends.

Top Companies in the U.S. Perfume Ingredient Chemicals Market

- Givaudan SA (Vernier, Switzerland) is the global leader in fragrance and beauty creation. The company's proprietary AI tools, Carto, Myrissi, and Well&Be, integrate neuroscience and consumer intelligence to craft personalized fragrance solutions. Givaudan's wide-ranging essential oils and aroma chemical portfolio, combined with its robust U.S. presence and continuous sustainability investments, cements its dominant market position.

- International Flavors & Fragrances Inc. (New York, U.S.) recorded full-year 2024 net sales of US$ 11.48 billion, with its Scent division achieving double-digit growth. A key player in the U.S. market, IFF commands deep expertise in synthetic aroma chemicals, essential oil extraction, and AI-based scent design. Its Science of Wellness program and partnerships with institutions such as Florida Polytechnic University continue to drive innovation in citrus and natural fragrance ingredients.

- DSM-Firmenich AG (Kaiseraugst, Switzerland), formed through the merger of Royal DSM and Firmenich in May 2023. The company's Perfumery & Beauty (P&B) division is a major market contributor, leveraging proprietary EcoScent Compass AI and green chemistry initiatives, including Clearwood® and Firgood®, to offer next-generation sustainable fragrance ingredients at scale.

Companies Covered in U.S. Perfume Ingredient Chemicals Market

- Givaudan SA

- International Flavors & Fragrances Inc. (IFF)

- DSM-Firmenich AG

- Symrise AG

- BASF SE

- MANE SA

- Fine Fragrances

- Agilex Fragrances

- Alpha Aromatics®

- Tropical Products

- Vigon International, LLC.

- Royal Aroma

- Henkel AG & Co. KGaA

- Sensient Technologies Corporation

- Takasago International Corporation

Frequently Asked Questions

The U.S. Perfume Ingredient Chemicals Market is estimated at US$ 4.0 Bn in 2026 and is projected to reach US$ 5.8 Bn by 2033, expanding at a CAGR of 5.5% during the forecast period 2026-2033, supported by growing demand for natural ingredients, premium fragrances, and biotechnology-driven aroma chemicals.

The market is driven by rising consumer preference for natural and sustainable fragrance ingredients, growth in premium personal care and fine fragrance products, increasing adoption of AI and biotechnology in scent formulation, and expanding regulatory frameworks supporting EPA Safer Choice and IFRA-compliant ingredient innovation.

The Essential Oils segment leads the market, holding approximately 60% of the product type share in 2024, driven by strong consumer demand for natural-origin aromatic materials, including orange, peppermint, eucalyptus, and citronella across fine fragrance and personal care formulations.

The Northeast U.S. is the leading regional market, powered by the headquarters of IFF, a dense ecosystem of luxury fragrance brands and prestige cosmetic retailers, and a robust regulatory compliance culture, making it the primary hub for fragrance ingredient consumption and innovation in the U.S.

The most significant market opportunity lies in the development and scaling of sustainable, biodegradable fragrance ingredients certified under programs such as the EPA Safer Choice initiative and COSMOS Organic standards.

The leading companies include Givaudan SA, International Flavors & Fragrances Inc. (IFF), DSM-Firmenich AG, Symrise AG, BASF SE, MANE SA, Agilex Fragrances, Alpha Aromatics®, Vigon International, LLC., and Henkel AG & Co. KGaA, among others, competing through innovation, sustainability, and portfolio differentiation.