- Medical Devices

- Central Line Catheters Market

Central Line Catheters Market Size, Share, and Growth Forecast, 2025 - 2032

Central Line Catheters Market By Product Type (Peripherally Inserted Central Catheters (PICC), Non-Tunneled Short-Term Catheters, Others), Material Type (Polyurethane, Silicone, Other), End-user, and Regional Analysis for 2025 - 2032

Central Line Catheters Market Size and Trends Analysis

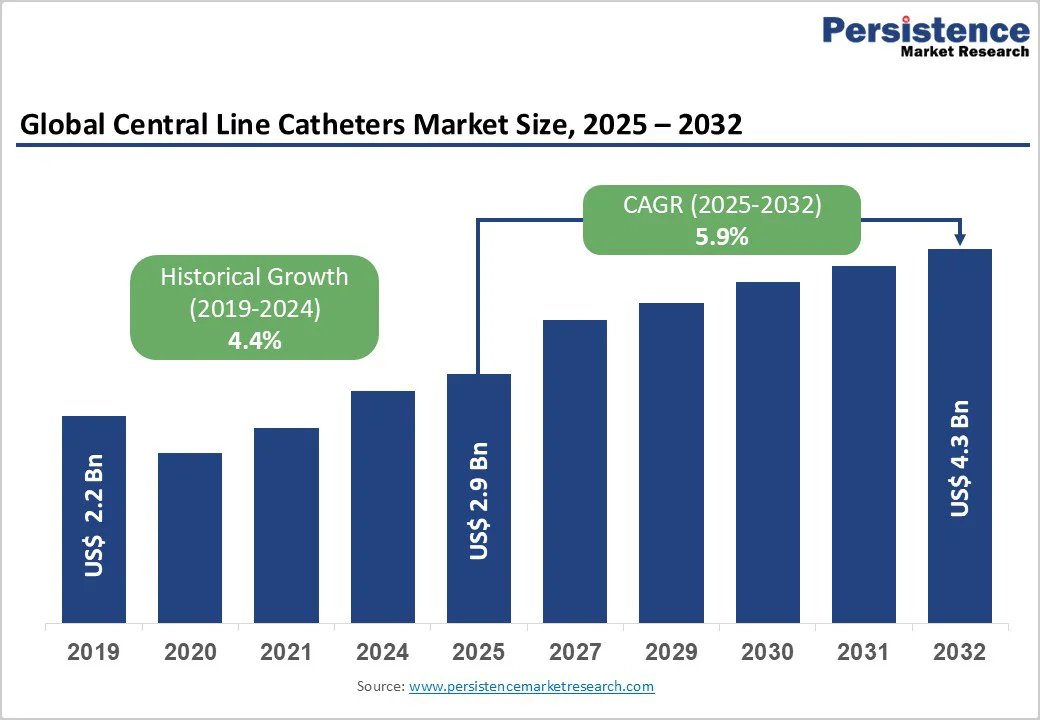

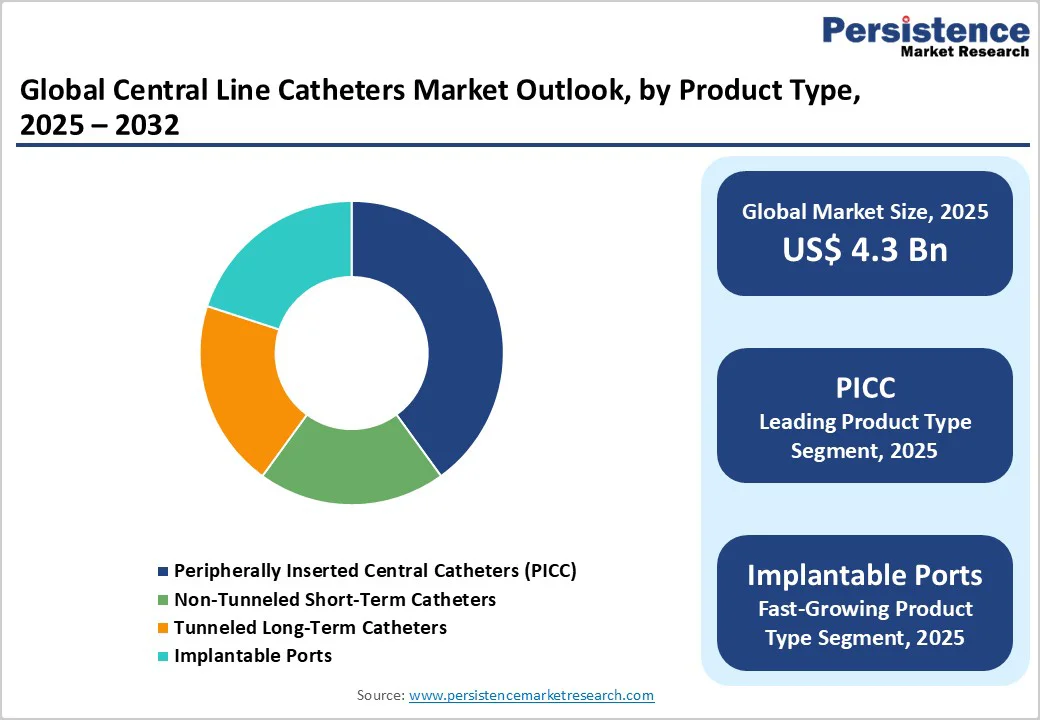

The global central line catheters market size is likely to be valued at US$2.9 billion in 2025 and is expected to reach US$4.3 billion by 2032, growing at a CAGR of 5.9% during the forecast period from 2025 to 2032, driven by the rising demand for reliable vascular access in oncology, critical care, and long-term infusion therapy.

The market is shaped by rising hospital demand for infection-prevention technologies, supported by new device designs such as antimicrobial coatings and integrated insertion systems. Growth is tempered by strict regulatory requirements and persistent concerns over CLABSI, underscoring the need for compliant, clinically proven solutions.

Key Industry Highlights

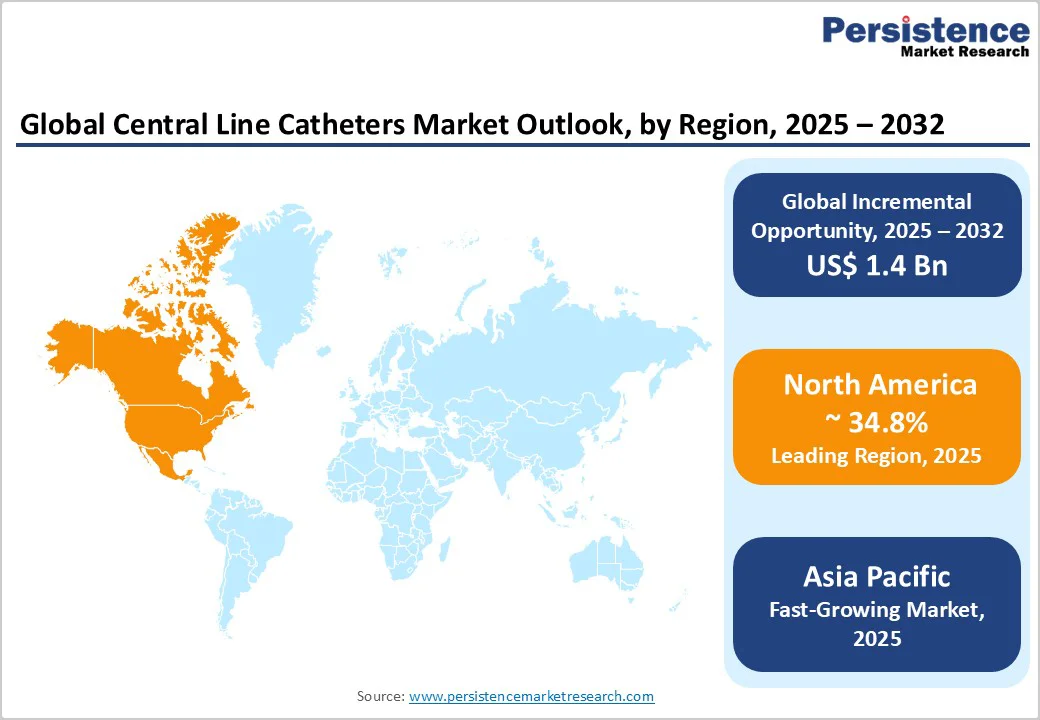

- Leading Region: North America holds the largest share of the global market, accounting for over 34.8% of total revenue due to high central line utilization rates, strong oncology procedure volumes, and established vascular access protocols.

- Fastest-growing Region: Asia Pacific is the fastest-expanding region, driven by rising cancer treatment capacity, hospital infrastructure upgrades, and expanded use of long-term vascular access devices.

- Investment Plans: Capital spending continues to rise in oncology infusion centers, vascular access teams, and catheter-associated infection-reduction programs, with several markets increasing long-term vascular access investments by 8–10% annually through expanded procurement of ports and antimicrobial-coated lines.

- Dominant Product Type: PICC lines remain the dominant product category and represent more than 40.7% of total central line placements due to their versatility across inpatient, outpatient, and home-based infusion pathways.

- Leading Material Type: Polyurethane leads material share with usage levels exceeding 56%, supported by its durability, structural stability, and compatibility with multi-lumen, high-flow designs commonly adopted in hospitals.

| Key Insights | Details |

|---|---|

|

Market Size (2025E) |

US$2.9 Bn |

|

Market Value Forecast (2032F) |

US$4.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Procedure Volumes and Chronic-Care Demand

The increase in global oncology treatments, ICU admissions, and long-term parenteral nutrition is expanding the need for central venous access. Hospitals account for substantial device usage due to high volumes of chemotherapy, hemodynamic monitoring, renal replacement therapy, and complex infusion therapies. Growing dependence on central venous access kits in both developed and emerging markets is expected to drive volume growth through 2032. Greater clinical emphasis on standardized insertion techniques and rising preference for multi-lumen configurations strengthen demand.

Infection-Control Technology and Product Innovation

Hospitals increasingly prioritize devices that minimize CLABSI risk. Manufacturers have responded with antimicrobial and antithrombogenic coatings, improved securement systems, advanced dressings, and closed connectors. The clinical and financial burden of bloodstream infections encourages procurement teams to adopt devices with proven infection-reduction benefits. As a result, premium catheter lines and integrated insertion platforms are gaining traction in critical care units and oncology wards. Continued reporting of preventable infections reinforces the shift toward advanced catheters, enabling suppliers to justify higher prices for technologies that reduce complication rates and support hospital quality benchmarks.

Ambulatory Care and Home Infusion Growth

Outpatient oncology, home infusion therapy, and decentralized care models are expanding faster than inpatient services. This transition boosts the need for long-term access solutions such as PICC lines and implantable ports. Payers and providers value devices that are easier to insert, maintain, and monitor outside the hospital setting. Demand for kits integrating securement technology, safety clamps, and user-friendly components is rising as home-care programs expand. PICCs and ports suitable for outpatient treatment cycles, particularly chemotherapy and antibiotic infusion, are experiencing strong growth.

Barrier Analysis - Regulatory and Compliance Burden

Increasingly stringent regulatory expectations across major regions are raising development and certification costs. Requirements for more robust clinical evidence, extended post-market surveillance, and detailed technical documentation lengthen time-to-market and heighten compliance expenditures. Smaller manufacturers face particular challenges due to the financial and administrative load. Updates to regulations in regions such as Europe and tighter review cycles in the U.S. create structural constraints that slow product introductions unless companies invest significantly in regulatory capacity.

Cost and Budget Pressures for Advanced Systems

Higher-cost advanced catheter systems sometimes face slower adoption in budget-restricted healthcare settings. Hospitals that prioritize short-term unit pricing over long-term savings may delay procurement of antimicrobial-coated catheters or integrated insertion platforms. Premium devices can cost 20–60 percent more than basic product lines, which limits near-term uptake in cost-sensitive units. In markets where reimbursement does not directly account for infection-prevention features, purchasing committees often opt for standard devices even when improved technologies offer clinical advantages.

Opportunity Analysis - Emerging Markets and Capacity Expansion

Rapid growth in healthcare investment across the Asia Pacific and parts of Latin America presents a significant opportunity for central line catheter manufacturers. Rising ICU capacity, expanding cancer centers, and increased hospital construction efforts directly increase demand for vascular access devices. Several high-growth markets in the region are projected to grow by double digits over the next five to seven years. Localized manufacturing and cost-competitive designs can accelerate penetration, especially in hospitals where budgets remain sensitive. Early movers that combine affordability with clear infection-control performance have strong potential for rapid market share gains.

Digital and Insertion-Assist Technologies

Integration of digital tools such as ultrasound-guided insertion support, RFID-enabled kit tracking, and automated checklists offers opportunities to reduce errors during catheter placement. Single-use insertion platforms that standardize steps and improve adherence to guidelines are gaining interest. Vendors coupling catheters with training programs and data-driven support tools create an attractive outcomes-focused value proposition. Devices and kits featuring digital elements represent a growing sub-segment with premium margins and recurring revenue from consumables and training.

Category-wise Analysis

Product Type Insights

PICC lines remain the leading segment, holding about 40.7% of the market, supported by high-volume use across inpatient wards, ambulatory infusion centers, and home-based care. Their bedside insertion capability allows rapid deployment without interventional radiology, a major advantage in high-throughput hospitals. PICCs are central to multi-week IV antibiotics, chemotherapy, parenteral nutrition, and complex infusion protocols. Large health systems often streamline procurement through bundled kits and standardized pathways, reinforcing PICC dominance. In many regions, they represent a significant share of long-term vascular access placements, aided by widespread ultrasound-guided insertion and dedicated vascular access teams.

Implantable ports and tunneled catheters are growing fastest as oncology and long-duration infusion needs rise. Their advantages, greater comfort, reduced dressing requirements, and low visibility, make them well-suited for multi-month chemotherapy. Many tertiary cancer centers increasingly standardize ports for breast cancer and hematologic malignancies due to reliable flow and lower maintenance. Longer dwell times also enhance cost efficiency.

Tunneled catheters such as Hickman lines are seeing greater uptake in bone marrow transplant and immunotherapy programs. As outpatient cancer care expands worldwide, port placements are increasing in parallel, supported by growing procedure volumes and higher average selling prices than those of short-term devices.

Material Type Insights

Polyurethane remains the leading material for central line catheters, accounting for roughly 56% of the market due to its durability, structural rigidity, and suitability for multi-lumen designs. Its thin-wall capability allows larger internal diameters, supporting rapid transfusions, power injection for contrast imaging, and complex multi-therapy infusions. Hospitals often standardize polyurethane devices as they resist kinking and breakage during long inpatient therapies or frequent manipulation. Critical-care and emergency units also favor polyurethane for its flow consistency and mechanical stability. Trauma centers, for example, routinely select polyurethane central lines to enable aggressive fluid resuscitation and high-flow medication delivery, reinforcing their status as the dominant material.

Silicone-based catheters, however, continue to gain momentum, especially in pediatric and neonatal care, where softness and flexibility help minimize vessel irritation. Their biocompatibility makes them well-suited for long-term use in patients requiring nutrition therapy, congenital cardiac support, or chronic disease management. Oncology teams also rely on silicone for tunneled catheters that must remain in place for extended periods.

Next-generation polymers and surface treatments further support growth. Hydrophilic, antimicrobial, and anti-thrombotic coatings are increasingly incorporated to reduce complications such as bloodstream infections or occlusions, especially in hospitals prioritizing infection-control pathways.

Regional Insights

North America Central Line Catheters Market Trends-High-Acuity Demand & Infection-Prevention Innovation

North America remains the largest market, accounting for over 34.8%, with substantial ICU capacity and widespread availability of specialized oncology and critical care services. The U.S. contributes the majority of regional revenue, driven by large hospital networks, strong reimbursement pathways, and early adoption of advanced catheter designs. Higher average selling prices support revenue growth as hospitals favor devices with proven infection-reduction features.

The region has some of the highest catheter use rates per 1,000 hospital admissions, supported by extensive oncology treatment pathways and advanced critical care protocols. Quality-reporting frameworks related to CLABSI reduction influence procurement across hospital systems, encouraging the transition toward antimicrobial-coated devices and integrated insertion systems. The regulatory environment is well-defined, with structured review pathways for catheter designs and modifications. Although innovation remains robust, expectations for clinical evidence continue to rise, encouraging manufacturers to prioritize data-driven differentiation.

The competitive landscape comprises major multinational firms with strong contracting power and significant installed-base advantages. Investment activity has been notable in vascular access kits, securement systems, and digital platforms that standardize insertion steps. North America remains a key launch region for new products, supported by its ability to generate early real-world clinical evidence and rapid adoption in high-acuity centers.

Europe Central Line Catheters Market Trends-Evidence-Driven Procurement & Regulatory-Shaped Adoption

Europe is the second-largest market, with Germany, the U.K., France, and Spain accounting for most regional demand. Hospitals in Western Europe maintain strong utilization of advanced vascular access devices, supported by structured clinical pathways and investment in infection-prevention programs.

Germany demonstrates high uptake due to its substantial ICU footprint, while the U.K. shows active development of outpatient oncology pathways that increase demand for implantable ports. Growth drivers include expanding ambulatory care, heightened attention to infection-prevention standards, and replacement of older catheter lines with improved coated and digitized systems. Procurement in Europe often operates through tenders and public purchasing frameworks, which favor solutions with strong evidence and cost-effectiveness.

The introduction of updated regulatory requirements has significantly influenced product strategies. Higher evidence and reporting thresholds have increased compliance costs, leading some smaller companies to rationalize portfolios. This shift subtly consolidates the market, giving larger firms a competitive edge. Investment opportunities continue to emerge in evidence generation, regional manufacturing assets, and strategic acquisitions that strengthen regulatory readiness. The region remains cautious but steady in its adoption of advanced catheter technologies.

Asia Pacific Central Line Catheters Market Trends - Rapid Expansion via Tertiary Care Growth & Localized Manufacturing

Asia Pacific is the fastest-growing regional market, driven by rising hospital construction, expanding oncology capacity, and increasing adoption of home infusion services. China and India are major contributors to volume growth, driven by greater access to tertiary care, expanding private hospital networks, and rising demand for long-term infusion therapies. Japan remains a mature market with a strong preference for high-specification devices. Primary growth factors include rising chronic disease prevalence, decentralization of care, and expanding ICU capacity.

Regulatory frameworks in the region continue to evolve, with many countries strengthening clinical data requirements while also enabling clearer pathways for domestic manufacturing. Companies investing in local partnerships or national distribution channels gain meaningful time-to-market advantages.

A mix of multinational and local players competes in this region. Pricing competition is high in public tenders, while premium devices are well placed in private urban hospitals. Home infusion programs and digital support tools represent emerging opportunities alongside growing demand for long-term access solutions.

Competitive Landscape

The global central line catheters market is moderately concentrated, led by multinational firms with strong portfolios in PICCs, tunneled catheters, and implantable ports. Advantages come from integrated kits, training, and long-term hospital contracts. High entry barriers include regulatory complexity, evidence requirements, and switching costs.

Smaller players target niche advances in coatings, securement, and digital insertion tools. Key strategies focus on infection-control innovation, expanded bundled kits, digital support, and Asia-Pacific growth. Suppliers prioritize clinical differentiation and service integration, while challengers compete through material innovation and cost-efficient access solutions for sustained global competitiveness.

Key Industry Developments

- In July 2025, Medtronic announced a digital-health platform for its central venous catheters, enabling remote monitoring of catheter status and patient data to optimize vascular access care.

- In August 2025, Bard introduced a next-generation line of central venous catheters with advanced antimicrobial coatings to reduce the risk of bloodstream infections, reinforcing its infection-prevention portfolio.

Companies Covered in Central Line Catheters Market

- BD

- Teleflex

- B. Braun

- AngioDynamics

- Smiths Medical

- Medtronic

- Cook Medical

- ICU Medical

- Vygon

- Fresenius Medical Care

- Merit Medical Systems

- Poly Medicure

- Lepu Medical

- Guangdong Baihe Medical

- Marvao Medical

- Argon Medical Devices

- Greiner Bio-One

- Cardinal Health

- Nexus Medical

- Medcomp

Frequently Asked Questions

The global central line catheters market size in 2025 is estimated at US$2.9 Billion.

By 2032, the central line catheters market is projected to reach US$4.3 Billion.

Key trends include broader use of long-term vascular access devices, growth of outpatient chemo programs, increased uptake of antimicrobial and advanced coatings, rising preference for implantable ports, and stronger investment in vascular access teams and infection-control pathways.

PICC lines are the leading product segment, accounting for the highest share due to versatility across inpatient, ambulatory, and home-care environments.

The central line catheters market is expected to grow at a 5.9% CAGR from 2025 to 2032, supported by higher oncology treatment volumes and increasing use of long-term and specialty access devices.

Major companies include BD (Becton Dickinson), Teleflex, B. Braun, AngioDynamics, and Smiths Medical.