- Biotechnology

- Infectious Diseases Diagnostics Market

Infectious Diseases Diagnostics Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Infectious Diseases Diagnostics Market by Product (Reagents, Kits & Consumables, Instruments, Software & Services), Technology (Immunodiagnostics, Molecular Diagnostics , Clinical Microbiology, Others), Disease Type (Respiratory Infections, HIV, Hepatitis, Hospital-Acquired Infections (HAIs), Sexually Transmitted Infections, Mosquito-Borne, Others), End User (Hospitals, Diagnostic Laboratories, Clinics / POC Settings , Research Institutes, Others), and Regional Analysis from 2026 to 2033

Infectious Diseases Diagnostics Market Size and Trend Analysis

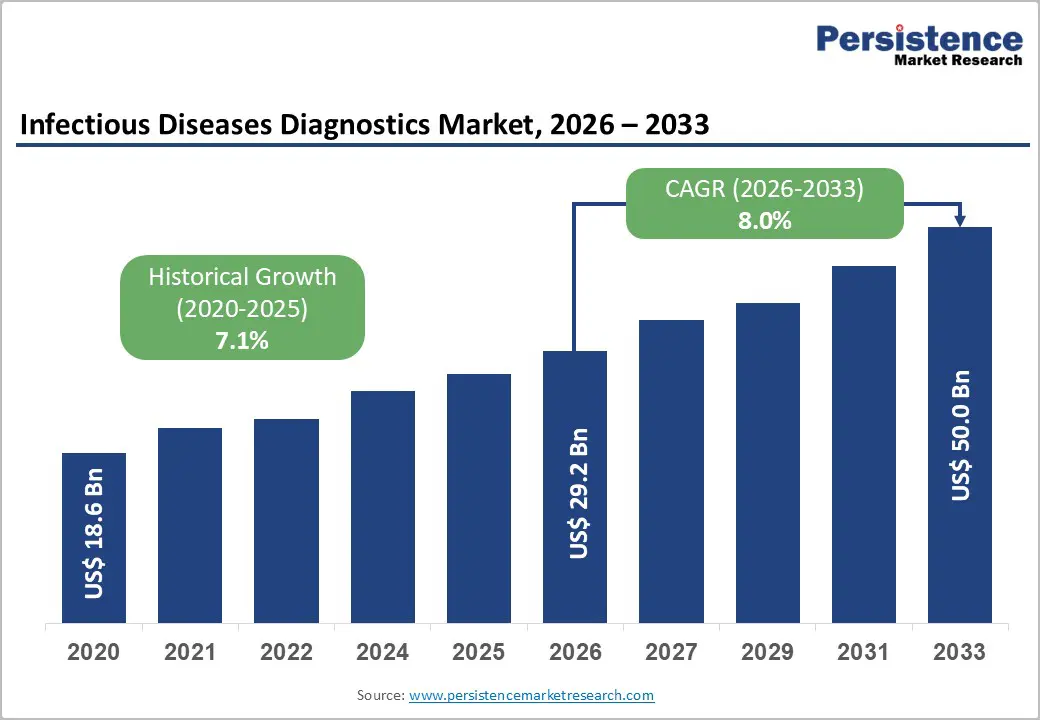

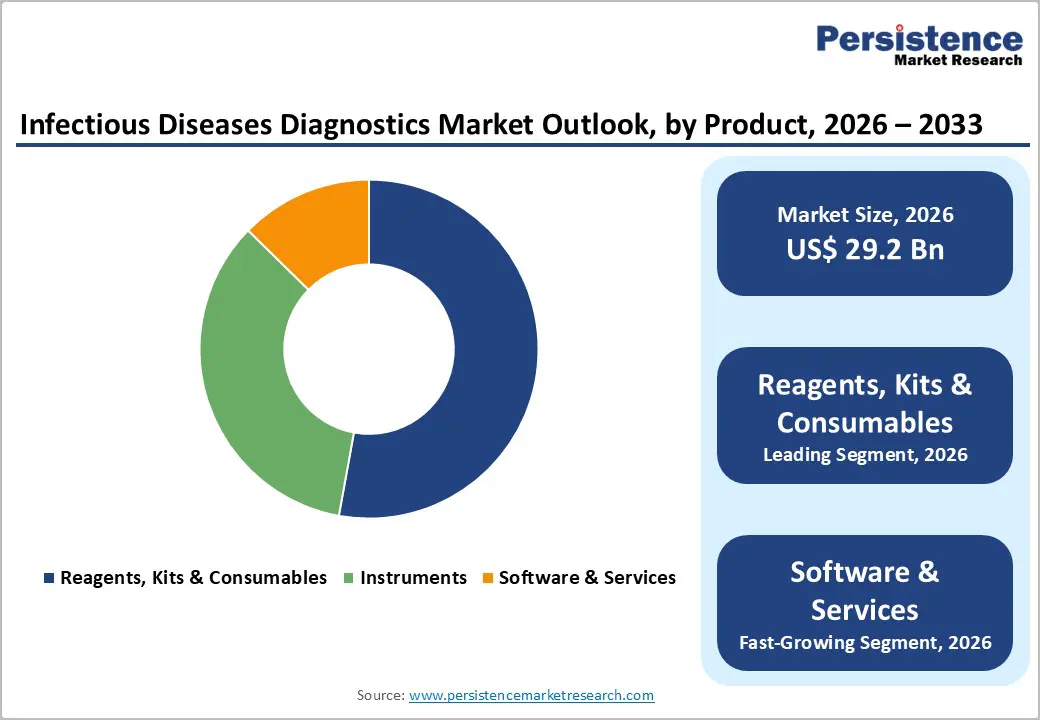

The global infectious diseases diagnostics market is estimated to grow from US$ 29.2 Bn in 2026 to US$ 50.0 Bn by 2033. The market is projected to record a CAGR of 8.0% during the forecast period from 2026 to 2033.

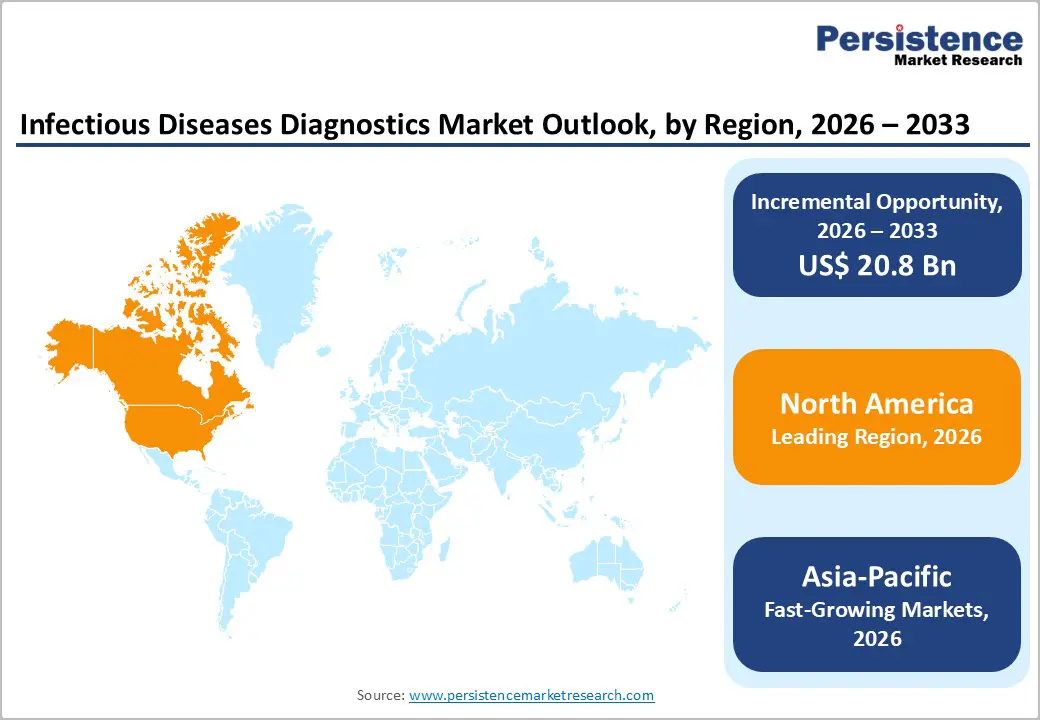

The global infectious diseases diagnostics market is growing steadily, fueled by rising disease prevalence, increasing demand for rapid and accurate testing, and expanding healthcare infrastructure. North America leads with advanced diagnostics infrastructure, strong regulations, and high R&D investment. Asia-Pacific is the fastest-growing region, driven by government initiatives, expanding laboratories, cost advantages, and rising patient awareness.

Size and Trend Analysis

- Dominant Segment: Reagents, Kits & Consumables dominated the Infectious Diseases Diagnostics Market with around 52.9% share in 2025, driven by high demand for rapid, accurate testing, routine laboratory use, recurring consumption, and integration with advanced molecular and immunodiagnostic platforms.

- Dominant Region: North America led due to advanced diagnostic infrastructure, strict regulatory compliance, and high R&D investment. Asia-Pacific was the fastest-growing region, supported by cost-effective laboratory expansion, government initiatives, rising healthcare access, and growing disease awareness.

- Market Drivers: Rising prevalence of infectious diseases, increasing demand for rapid diagnostics, government health programs, technological advancements, and adoption of point-of-care testing.

- Market Opportunity: Opportunities include growth in molecular diagnostics, AI-enabled diagnostic platforms, expansion of point-of-care testing, integration of multiplex panels, and increasing demand from emerging healthcare markets.

| Global Market Attributes | Key Insights |

|---|---|

| Global Infectious Diseases Diagnostics Market Size (2026E) | US$ 29.2 Bn |

| Market Value Forecast (2033F) | US$ 50.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.1% |

Market Dynamics

Driver: Growing demand for rapid and accurate diagnostics

Surgical site infections (SSIs) and other healthcare?associated infections remain persistent challenges worldwide, significantly driving demand for infectious disease diagnostics in surgical settings. A global meta?analysis found the pooled incidence of SSIs at approximately 2.5 percent among surgical patients, with some regions reporting rates as high as 7.2 percent, indicating substantial diagnostic needs for early detection and prevention. In the United States alone, hospital?acquired infections, including SSIs affect roughly 1.7 million patients annually, contributing to significant morbidity and mortality. Rapid, accurate diagnostics are therefore integral to surgical care pathways to mitigate complications and improve outcomes.

Heightened awareness of nosocomial infection burdens further amplifies diagnostic demand. Chronic and acute infectious risks underscore the need for reliable surveillance and pathogen identification, especially where infection control resources vary. For example, health?care settings in low? and middle?income countries report SSI rates as high as one?third of operated patients, far exceeding rates in high?income settings and underscoring inequities in infection prevention. This global infectious burden fuels investment in advanced surgical infectious disease diagnostics to support timely intervention, antimicrobial stewardship, and reduced postoperative complications.

Restraints: High cost of advanced diagnostic instruments and molecular tests

Advanced diagnostic instruments, especially molecular platforms used in surgical infection diagnostics, often carry high acquisition and operational costs that hinder widespread adoption. Credible market analysis notes that molecular point?of?care systems frequently require significant capital investment, with instrument costs ranging from $15,000 to $50,000, while individual test cartridges may cost $30–$100 each. These financial barriers are particularly impactful for smaller hospitals and clinics with constrained budgets, limiting the procurement of cutting?edge tools even where clinical need is high.

Beyond upfront costs, recurring expenses for consumables, maintenance, and calibration further strain healthcare facility resources, especially in resource?limited regions. Cost barriers also intersect with reimbursement limitations in many public health systems, where insurance coverage for advanced diagnostic testing is inadequate or restrictive. Consequently, facilities may defer adoption of higher?performance diagnostics in favor of cheaper, less accurate methods, slowing overall market penetration and innovation uptake within surgical infection diagnostics.

Opportunity: Expansion of point-of-care and home-based testing solutions

Expansion of point?of?care and at?home testing represents a significant opportunity within the surgical infectious diseases diagnostics landscape. The convergence of telemedicine, mobile health, and decentralized care has accelerated demand for rapid, accessible diagnostics that can be deployed outside centralized laboratories. For instance, point?of?care testing adoption has expanded notably in infectious disease screening and chronic care, with home?based solutions increasing accessibility and patient engagement. These technologies enable clinicians to identify postoperative infections earlier, potentially reducing readmissions and streamlining outpatient follow?up.

The growth of decentralized diagnostics also aligns with broader healthcare trends toward self?management and value?based care. With telehealth adoption rising and remote monitoring increasingly integrated into care pathways, there is a growing market for portable, user?friendly testing formats that support both clinical decision?making and patient?centric care delivery. Especially in regions where laboratory infrastructure is limited, point?of?care and home testing can bridge gaps in surgical infection surveillance, offering faster turnaround times and improved access to actionable results.

Category-wise Analysis

By Product, Reagents, Kits & Consumables Dominates the Infectious Diseases Diagnostics Market

Reagents, Kits & Consumables occupies 52.9% share of the global market in 2025, because they are essential for virtually every infectious disease test and are consumed repeatedly. These components account for a large portion of testing activity, with one sector analysis showing the reagents and consumables segment holding over 50 percent share due to constant usage in both laboratory and point?of?care settings. Unlike instruments that are one?time purchases, reagents and kits must be replenished for every test, sustaining demand as global testing volumes rise. Their compatibility with multiple technologies and cost?effective operation further reinforce their prevalence in daily diagnostic workflows.

By Technology, Molecular Diagnostics dominate due to high sensitivity, specificity, and rapid pathogen detection globally

Molecular diagnostics lead the market by technology because they provide superior sensitivity and specificity compared with conventional methods, detecting pathogen DNA or RNA even at very low levels. Techniques such as real?time PCR are now standard for many infectious diseases, enabling early and precise identification of viruses and bacteria, and supporting rapid clinical decisions. Global diagnostic practice has shifted markedly toward molecular methods; PCR is widely used in routine screening for conditions like HIV, tuberculosis, and COVID?19 due to its reliability and speed. Clinical adoption continues to grow as laboratories expand molecular testing capacity to meet increasing surveillance and outbreak response needs.

Regional Insights

North America Infectious Diseases Diagnostics Market Trends

North America dominates the infectious diseases diagnostics market with 38.0% share in 2025, due to its advanced healthcare infrastructure, high surgical volumes, and rigorous infection surveillance programs. In 2024, the region accounted for the largest share of the global market, supported by widespread adoption of cutting edge diagnostic technologies, including molecular and rapid tests, in hospitals and surgical centers. Robust regulatory oversight and infection prevention mandates facilitate consistent implementation of diagnostics to detect and manage surgical site and other healthcare?associated infections.

Furthermore, the United States reports high surgical activity and significant infection control efforts. For example, CDC data indicate that surgical site infections remain a key focus of national healthcare?associated infection reporting, with tens of thousands of cases monitored annually, underscoring the need for reliable diagnostics in surgical care pathways.

Europe Infectious Diseases Diagnostics Market Trends

Europe is an important region in the surgical infectious diseases diagnostics market because of its well established public healthcare systems, comprehensive infection control policies, and structured SSI surveillance programs. Across several EU member states, surgical site infection incidence data are regularly collected to inform clinical practices, with observed rates varying by procedure type and monitored through standardized reporting frameworks.

European healthcare facilities prioritize patient safety and evidence based infection prevention, which drives the adoption of diagnostic tools that support early detection and clinical decision making, particularly in pre and postoperative care. Strong regulatory environments and integration of diagnostic protocols in national health systems further bolster Europe’s role in shaping best practices for surgical infection diagnostics. Collectively, these factors sustain demand for advanced diagnostics across major European markets.

Asia-Pacific Infectious Diseases Diagnostics Market Trends

The Asia Pacific region is the fastest growing market for surgical infectious diseases diagnostics due to expanding healthcare infrastructure, rising healthcare expenditure, and increasing surgical procedure volumes in emerging economies such as China and India. Significant investments in hospital networks and modernization of diagnostic laboratories are improving access to advanced testing solutions, accelerating regional demand.

Population level factors also contribute: the region bears a substantial burden of healthcare associated infections and is intensifying infection surveillance and prevention efforts, encouraging wider adoption of surgical diagnostics. Additionally, rising medical tourism in parts of Asia Pacific increases demand for high quality surgical care and associated diagnostics. Together with supportive government policies and growing awareness of infection control practices, these trends underpin robust growth in surgical infectious diseases diagnostics across the region.

Market Competitive Landscape

Leading companies in the infectious diseases diagnostics market focus on scalable production, workflow optimization, and regulatory compliance. Investments in advanced diagnostic platforms, automation, and data analytics enhance accuracy, efficiency, and reliability. Strategic partnerships, integrated supply chains, and expanded laboratory capacity ensure consistent, high-quality testing solutions for hospitals, surgical centers, and public health programs worldwide.

Key Industry Developments:

- In October 2025, Sysmex Corporation signed an exclusive distribution and supply agreement with QIAGEN K.K., the Japanese subsidiary of QIAGEN N.V., for clinical diagnostic products in infectious diseases and oncology in Japan.

- In September 2025, QIAGEN received U.S. Food and Drug Administration (FDA) clearance for its higher throughput QIAstat Dx Rise syndromic testing system, expanding rapid infectious disease testing access in the United States.

Companies Covered in Infectious Diseases Diagnostics Market

- QIAGEN

- Bio-Rad Laboratories

- Roche Diagnostics

- Thermo Fisher Scientific

- Adaptive Biotechnologies

- Siemens Healthineers

- Grifols

- Beckton Dickinson (BD)

- PerkinElmer

- Abbott Laboratories

- Hologic

- MedMira

- Lucira Health

- Seegene

- Sherlock Biosciences

- Danaher (e.g., Cepheid, Beckman Coulter)

- Illumina

Frequently Asked Questions

The global infectious diseases diagnostics market is projected to be valued at US$ 29.2 Bn in 2026.

Rising infectious disease prevalence, demand for rapid testing, technological advances, and expanded healthcare infrastructure drive growth.

The global infectious diseases diagnostics market is poised to witness a CAGR of 8.0% between 2026 and 2033.

Opportunities include molecular diagnostics expansion, point-of-care testing, AI integration, multiplex panels, and emerging healthcare markets.

QIAGEN, Bio-Rad Laboratories, Roche Diagnostics, Thermo Fisher Scientific, Adaptive Biotechnologies, Siemens Healthineers.