- Electrical Equipment & Services

- Centralized Control Cabinet Market

Centralized Control Cabinet Market Size, Share, and Growth Forecast, 2026 - 2033

Centralized Control Cabinet Market by Power (1-3 kW, 3-6 kW, 6-9 kW, 9-12 kW), Application (Water & Wastewater, Pulp & Paper, Oil & Gas, Petrochemical), Voltage Type (Low, Medium, High), and Regional Analysis for 2026-2033

Centralized Control Cabinet Market Share and Trends Analysis

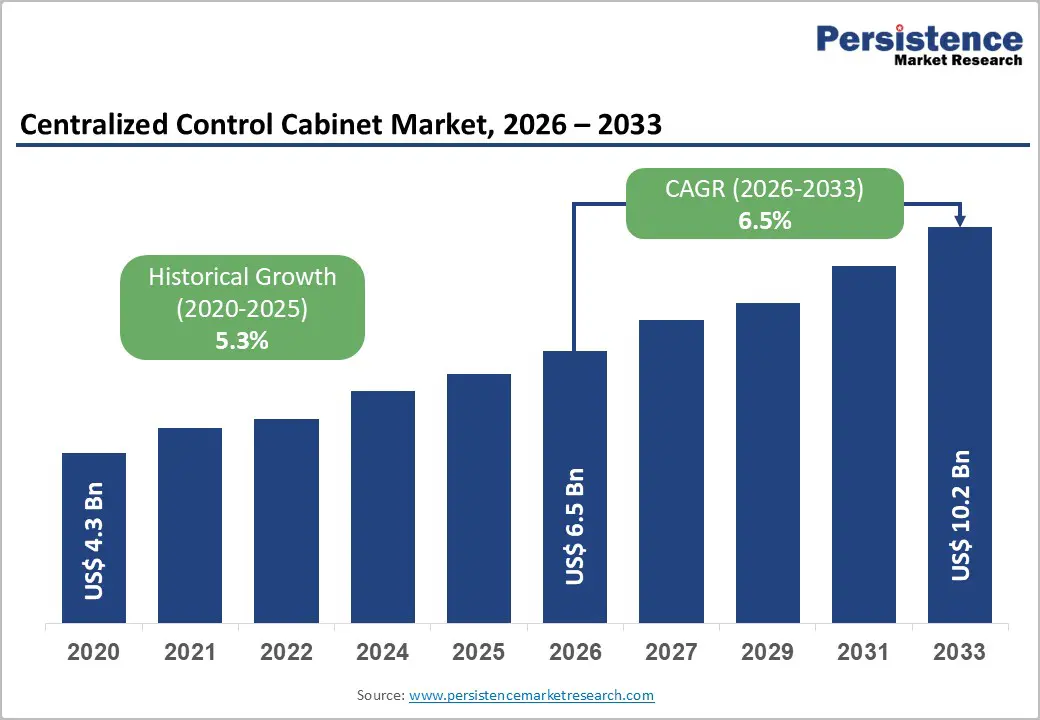

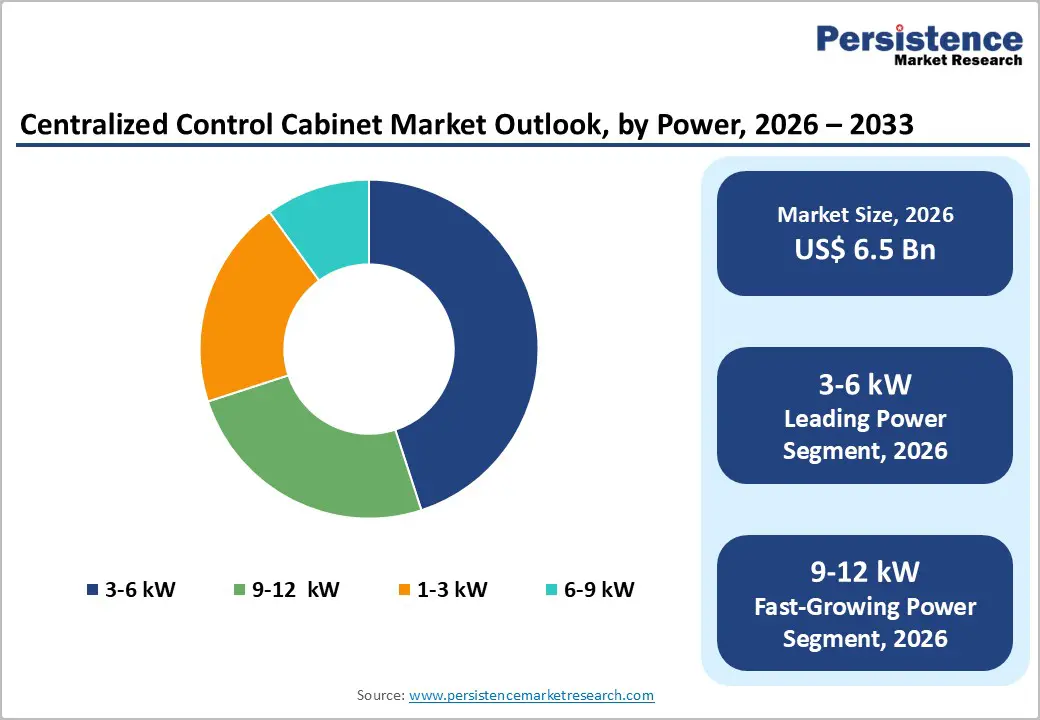

The global centralized control cabinet market size is likely to be valued at US$ 6.5 billion in 2026, and is projected to reach US$ 10.2 billion by 2033, growing at a CAGR of 6.5% during the forecast period 2026−2033.

Fueling the growth momentum of the market is the sustained investments in industrial automation across manufacturing, energy, utilities, and transportation infrastructure. Companies are deploying automated production lines to improve throughput and reduce manual intervention. Centralized control cabinets are enabling integration of programmable logic controllers, power distribution units, and monitoring interfaces within a unified system architecture. This consolidation is reducing operational downtime and improving process visibility. As industries are prioritizing efficiency and digital oversight, demand for reliable control enclosures is strengthening.

The adoption of Industry 4.0 frameworks is further reinforcing market expansion. Manufacturers are integrating sensors, real-time analytics platforms, and supervisory control and data acquisition systems, commonly referred to as supervisory control and data acquisition (SCADA), within centralized control structures. These systems are improving data consolidation, reducing signal loss, and enhancing predictive maintenance capabilities. Regulatory authorities are placing stronger emphasis on workplace safety and equipment compliance, and centralized cabinets are supporting standardized electrical protection and fault management. Energy and infrastructure operators are modernizing grid and facility control networks to ensure operational continuity.

Key Industry Highlights

- Application Leadership: Oil & gas is expected to hold roughly 30% revenue share in 2026, whereas water & wastewater applications are slated to be the fastest-growing during the 2026-2033 forecast period.

- Voltage Type Dynamics: The low voltage segment is likely to dominate with an approximate 65% market share in 2026, while the medium voltage segment is anticipated to be the fastest-growing between 2026 and 2033.

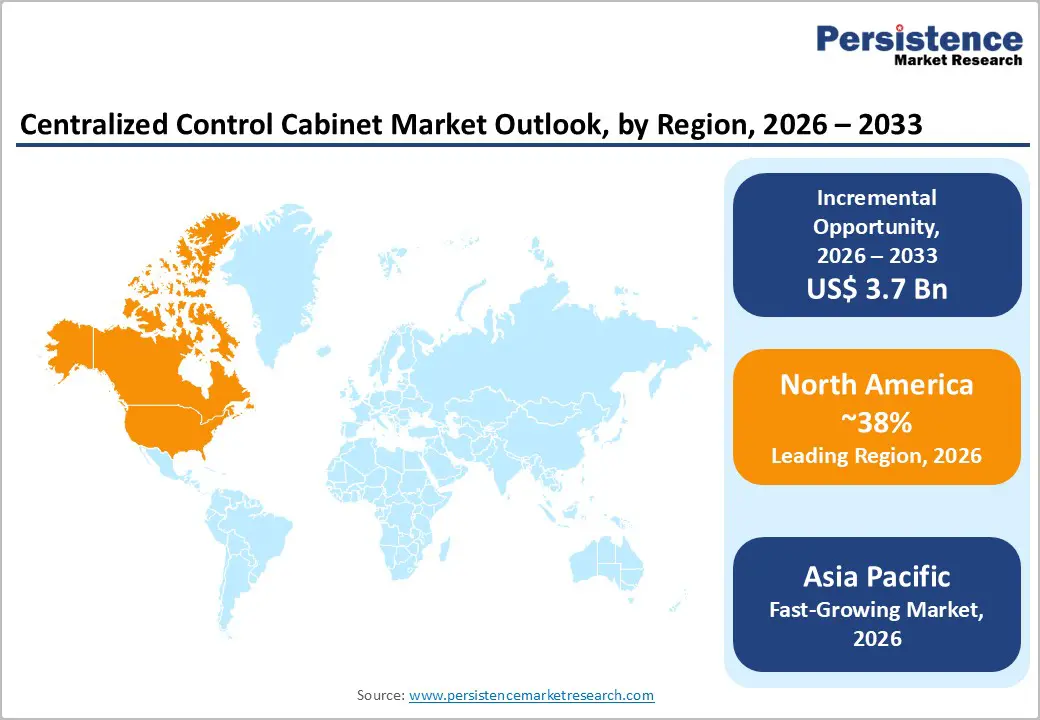

- Dominant Region: North America is expected to command about 38% market share in 2026, owing to a mature industrial base and widespread adoption of automation technologies.

- Fastest-growing Market: The Asia Pacific market is forecast to be the fastest-growing through 2033, powered by rapid industrialization and infrastructure transformation.

| Key Insights | Details |

|---|---|

| Centralized Control Cabinet Market Size (2026E) | US$ 6.5 Bn |

| Market Value Forecast (2033F) | US$ 10.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Industrial Automation and Smart Manufacturing Expansion

The centralized control cabinets market increasingly benefits from the growing focus on industrial automation and smart manufacturing. Companies across sectors now view automation as a strategic lever to improve operational efficiency, maintain consistent quality, and respond more quickly to market demands. Centralized control cabinets act as the core control point for production assets, coordinating machinery, conveyors, drives, and safety systems in a structured and manageable way. By standardizing control architectures across facilities, organizations can simplify maintenance, improve uptime, and create a more scalable platform for future upgrades and process enhancements.

The integration of advanced technologies such as the Internet of Things (IoT), artificial intelligence (AI), and machine learning (ML) is transforming these cabinets from basic hardware enclosures into intelligent decision-support hubs. Manufacturers can use connected control systems to monitor equipment conditions in real time, detect anomalies at an early stage, and schedule interventions before failures occur. Data captured at the cabinet level also supports continuous improvement programs, helping engineering and operations teams refine process parameters and eliminate bottlenecks. This evolution means centralized control cabinets are no longer a commodity purchase but a strategic asset that underpins digital transformation, supports predictive maintenance strategies, and aligns plant operations with broader business performance objectives.

System Complexity and Specialized Expertise Requirements

The complexity inherent in centralized control cabinets creates significant implementation hurdles for many organizations. These systems integrate multiple critical components such as programmable logic controllers (PLCs), variable frequency drives (VFDs), SCADA systems, and diverse communication protocols. Engineering teams must possess interdisciplinary expertise spanning electrical engineering, software programming, and network architecture to deploy these solutions successfully. Organizations without dedicated automation departments face prolonged vendor selection processes and extended commissioning periods. Procurement managers often underestimate the coordination required across multiple system integrators, which extends project timelines and elevates coordination costs.

The shortage of qualified automation professionals compounds these technical challenges and creates operational vulnerabilities. Installation teams require specialized training to configure safety interlocks, optimize drive parameters, and validate communication networks properly. Even minor configuration errors during commissioning can trigger cascading equipment failures and production interruptions. Maintenance requirements demand continuous access to skilled technicians familiar with specific vendor architectures and proprietary software platforms. Companies lacking robust service contracts with manufacturers face prolonged response times during critical failures. Legacy infrastructure integration presents additional obstacles, as older facilities struggle to accommodate modern control cabinet footprints, power requirements, and cybersecurity standards.

Ongoing Modernization of Industrial Infrastructure

Industrial infrastructure modernization in emerging economies represents a substantial growth opportunity for centralized control cabinet providers. Governments and private enterprises actively replace aging control systems with contemporary solutions that deliver superior reliability and operational performance. These upgrades address chronic reliability issues prevalent in legacy installations while establishing foundations for digital transformation initiatives. Forward-thinking manufacturers can target this window by developing control solutions specifically engineered for retrofit applications, featuring modular designs and backward compatibility with existing electrical infrastructure. Stakeholders can also accrue benefits from standardized footprints and simplified commissioning protocols that minimize disruption to ongoing operations.

Energy efficiency and sustainability imperatives create additional strategic openings within this modernization cycle. Industries increasingly seek control cabinets incorporating advanced power management features such as VFDs, harmonic mitigation systems, and intelligent load balancing capabilities. These technologies enable precise energy consumption optimization across production cycles while meeting stringent environmental regulations. Manufacturers distinguish themselves by offering comprehensive energy monitoring platforms integrated directly into control architectures, providing facility managers with actionable insights for continuous efficiency improvements.

Category-wise Analysis

Power Insights

The 3-6 kW segment is slated to maintain a dominant position in 2026 with an estimated 45% of the centralized control cabinet market revenue share. These configurations strike an optimal balance between cost-effectiveness and sufficient capacity for standard industrial applications such as manufacturing, water treatment facilities, and building automation systems. Their widespread adoption stems from versatility across diverse operational environments, eliminating the need for specialized electrical infrastructure modifications. Standardized designs also facilitate faster procurement cycles and simplified maintenance protocols, making them particularly attractive for mid-sized enterprises and retrofit projects where budget constraints and timeline pressures dominate decision-making criteria.

The 9-12 kW segment is likely to be the fastest-growing during the 2026-2033 forecast period. Growth drivers include large-scale industrial automation projects, heavy manufacturing applications, and energy sector deployments requiring robust control capacity. Oil and gas facilities, power generation plants, and large processing operations demand high-power systems capable of managing extensive equipment arrays. As industrial facilities scale operations and integrate additional automation components, power requirements increase correspondingly, driving adoption of higher-capacity control cabinet configurations.

Application Insights

Applications across the oil & gas sector are projected to account for approximately 30% of the centralized control cabinet market share in revenue terms in 2026. The sector heavily relies on these systems to manage critical functions such as drilling control, refining processes, and pipeline distribution networks. Operators are deploying centralized cabinets to maintain stable performance in environments characterized by extreme temperatures, corrosive exposure, and stringent safety requirements. Exploration and production projects are continuing across both offshore and unconventional resource fields, and facility modernization programs are upgrading legacy control infrastructure. Companies are replacing outdated panels with integrated automation cabinets that support improved monitoring, fault detection, and compliance with enhanced safety regulations. As production capacities are expanding and digitalization is progressing, demand for ruggedized and certified control systems is strengthening across upstream and downstream operations.

Water and wastewater treatment are likely to become the fastest-growing application segment between 2026 and 2033. Rapid urbanization, population growth, and stricter environmental discharge regulations are increasing global demand for advanced treatment capacity. Municipal authorities are investing in new infrastructure projects, particularly in developing economies that are constructing modern treatment facilities. In mature markets, aging infrastructure replacement initiatives are generating parallel procurement requirements. Industrial operators are facing tighter wastewater discharge standards, and they are upgrading control systems to ensure regulatory compliance and operational efficiency. Centralized control cabinets are enabling real-time monitoring, automated valve control, and integrated alarm systems within treatment plants.

Voltage Type Insights

The low voltage segment is forecasted to capture nearly 65% of the market revenues in 2026. These systems are primarily serving residential buildings and small commercial facilities where electrical operations are functioning below 1,000 volts. Demand is being supported by increasing adoption of smart home technologies and energy management systems. Residential developers are integrating standardized low voltage infrastructure into new housing complexes to enable lighting automation, climate control, and security monitoring. Commercial property managers are also deploying these cabinets to support scalable building management systems. As urban housing construction and mixed-use developments are expanding, installation of low voltage control cabinets is becoming a standard component of modern building design.

The medium voltage segment is expected to post the highest CAGR through 2033, as industrial expansion and infrastructure upgrades continue to accelerate. These control cabinets are supporting operations within the 1,000 to 35,000-volt range and are serving manufacturing plants, power distribution networks, and heavy industrial facilities. Operators are modernizing electrical systems to improve energy efficiency, reduce downtime, and meet updated safety codes. Infrastructure investment in utilities and large-scale production complexes is increasing the need for reliable power coordination and load management. Medium voltage cabinets are enabling stable electricity distribution while protecting equipment from overload and system faults. Companies that are prioritizing thermal management, arc flash protection, and compliance certification are positioning themselves to capture sustained demand in industrial and utility-driven applications.

Regional Insights

North America Centralized Control Cabinet Market Trends

North America is set to secure the largest portion of the centralized control cabinet market share of about 38% in 2026. The United States drives regional dominance through its mature industrial base and widespread adoption of automation technologies across manufacturing, energy, and infrastructure sectors. Operators prioritize advanced control solutions to support ongoing modernization of production facilities, utility networks, and critical infrastructure. Federal infrastructure programs channel significant resources toward smart grid development, water treatment upgrades, and manufacturing facility renewals, creating sustained demand for reliable control systems. Industry leaders such as Schneider Electric have regularly demonstrated confidence in this market through substantial investments in domestic production capacity and technology centers.

The region's competitive advantages stem from a well-established regulatory framework and thriving innovation ecosystem. Safety standards from the American Society of Heating, Refrigerating and Air-Conditioning Engineers (ASHRAE), National Fire Protection Association (NFPA), and National Electrical Code (NEC) mandate sophisticated control architectures that prioritize energy efficiency and cybersecurity protection. North America's automation ecosystem anchored by leading equipment manufacturers, research institutions, and system integrators accelerates development of next-generation solutions featuring advanced connectivity and embedded analytics capabilities. Mature supply chains and extensive service networks, enabling faster deployment cycles and comprehensive after-sales support, are the most attractive factors pulling global market players to this region.

Europe Centralized Control Cabinet Market Trends

Europe is expected to command a substantial share of the market for centralized control cabinets in 2026 and beyond, anchored by Germany's manufacturing leadership in automotive production and industrial machinery sectors. Operators across the region prioritize advanced control infrastructure to support precision manufacturing and complex production environments. The European Green Deal has established comprehensive carbon-reduction targets that integrate automation systems with real-time sustainability tracking and environmental performance monitoring. Regulatory harmonization across European Union (EU) member states creates consistent compliance frameworks, favoring manufacturers who deliver modern control solutions with embedded energy management capabilities. Facility managers benefit from standardized specifications that streamline procurement across multinational operations.

France sustains steady demand through its nuclear energy infrastructure and diversified industrial base, while the United Kingdom pursues industrial modernization despite post-Brexit regulatory adjustments. Spain's renewable energy expansion, particularly solar photovoltaic installations, accelerates adoption of medium voltage control cabinets for grid integration and power management applications. Competitive dynamics feature European automation leaders Siemens and Schneider Electric alongside ABB, creating a mature ecosystem of system integrators and service providers. Investment priorities center on sustainability-linked financing mechanisms, Industry 4.0 platform deployments, and building automation upgrades aligned with energy performance certificate requirements. Procurement teams gain strategic advantages through established supply chains and comprehensive after-sales support networks spanning the entire Europe market.

Asia Pacific Centralized Control Cabinet Market Trends

The Asia Pacific market is anticipated to emerge as the fastest-growing during the 2026-2033 forecast period, propelled by rapid industrialization and infrastructure transformation across multiple economies. China establishes regional dominance through massive manufacturing scale, aggressive smart factory deployments, and comprehensive infrastructure modernization programs. Operators prioritize advanced control infrastructure to support expanding production capacities and complex automation environments. Government industrial policies actively channel resources toward manufacturing hubs and urban development projects, creating sustained demand for reliable control solutions. Japan sustains leadership in precision manufacturing and robotics integration, while emerging markets pursue ambitious automation agendas to compete globally.

India accelerates growth through targeted initiatives such as Make in India and Smart Cities Mission, positioning the country as a high-potential market for control infrastructure investments. Major ASEAN economies of Thailand, Vietnam, Indonesia, and Malaysia are attracting significant manufacturing relocations, generating greenfield opportunities for new control installations. Regional advantages encompass competitive production costs, expanding middle-class consumption patterns, and strategic technology localization efforts that enhance supply chain resilience. Investment priorities emphasize automation platform upgrades, energy-efficient manufacturing systems, and smart infrastructure deployments, positioning Asia Pacific as the strategic growth engine for global control cabinet manufacturers seeking to balance mature market stability with emerging market expansion.

Competitive Landscape

The global centralized control cabinet market is exhibiting a moderately concentrated structure. Schneider Electric, Siemens AG, ABB, Rockwell Automation, and Mitsubishi Electric Corporation are the top market players that are collectively account for approximately 45-50% of total revenues in 2026. These multinational firms are leveraging broad product portfolios, strong engineering capabilities, and global service networks to maintain competitive advantage. Competition is intensifying as both global and regional manufacturers are investing in continuous product innovation, strategic alliances, and selective mergers and acquisitions. Market leaders are differentiating themselves through integrated automation solutions that address diverse requirements across manufacturing plants, power generation facilities, and infrastructure projects. Their scale enables efficient procurement, standardized quality control, and compliance with international certification standards.

Manufacturers are increasingly prioritizing advanced and energy-efficient control systems that align with industrial automation objectives and sustainability mandates. Integrated cabinet solutions are incorporating programmable logic controllers, energy monitoring modules, and digital communication interfaces to support modern production environments. Companies are emphasizing modular design, thermal optimization, and cybersecurity integration to meet evolving operational requirements. As industries are transitioning toward smart factories and digitalized utilities, centralized control cabinets are becoming critical infrastructure components.

Key Industry Developments

- In February 2026, Rolls-Royce SMR and Yokogawa Electric Corporation formed a strategic partnership to provide the data processing and control systems (DPCS) for the first units in Rolls-Royce’s planned global fleet of small modular reactors (SMRs), covering system design, hardware, testing, installation, and commissioning to support reactor automation and safety infrastructure.

- In January 2026, Delta Electronics showcased smart automation technologies for data center cooling distribution unit (CDU) infrastructure at AHR Expo 2026, highlighting its integrated approach to energy-efficient facility management and automated environmental control.

- In July 2025, ABB equipped a new eye care center in Central London with its smart power protection solutions to ensure reliable electricity supply and safeguard critical medical equipment, enhancing operational continuity and patient safety. The installation demonstrates ABB’s focus on intelligent power management in healthcare facilities.

Companies Covered in Centralized Control Cabinet Market

- Schneider Electric SE

- ABB Ltd

- Siemens AG

- Eaton Corporation

- Rockwell Automation Inc.

- Mitsubishi Electric Corporation

- Emerson Electric Co.

- Honeywell International Inc.

- General Electric

- Rittal GmbH & Co. KG

- Pentair plc

- Legrand SA

- nVent Electric plc

- Elmech Pneumatic Industries Pvt Ltd

Frequently Asked Questions

The global centralized control cabinet market is projected to reach US$ 6.5 billion in 2026.

Industrial automation, smart manufacturing, and Industry 4.0 adoption across manufacturing, energy, and infrastructure sectors are driving the market.

The market is poised to witness a CAGR of 6.5% from 2026 to 2033.

Infrastructure modernization in emerging economies and energy-efficient control solutions supporting sustainability mandates is unlocking massive growth opportunities.

Schneider Electric, Siemens AG, ABB Ltd., Rockwell Automation, and Mitsubishi Electric Corporation are some of the key players in the market.