- Medical Devices

- Cardiac Surgery Devices Market

Cardiac Surgery Devices Market Size, Share, and Growth Forecast 2026 - 2033

Cardiac Surgery Devices Market by Product Type (Cardiopulmonary Bypass (CPB) Equipment, Perfusion Disposables, Cardiac Ablation Devices, Beating Heart Surgery Systems (Off-Pump CABG Systems), Others), Application (Coronary Artery Bypass Grafting (CABG), Heart Valve Repair and Replacement, Congenital Heart Defect Repair, Cardiac Arrhythmia Surgery, Others), End-user (Hospitals and Cardiac Centers, Ambulatory Surgical Centers (ASCs), Specialty Clinics, Academic and Research Institutes), and Regional Analysis, 2026 - 2033

Cardiac Surgery Devices Market Size and Trend Analysis

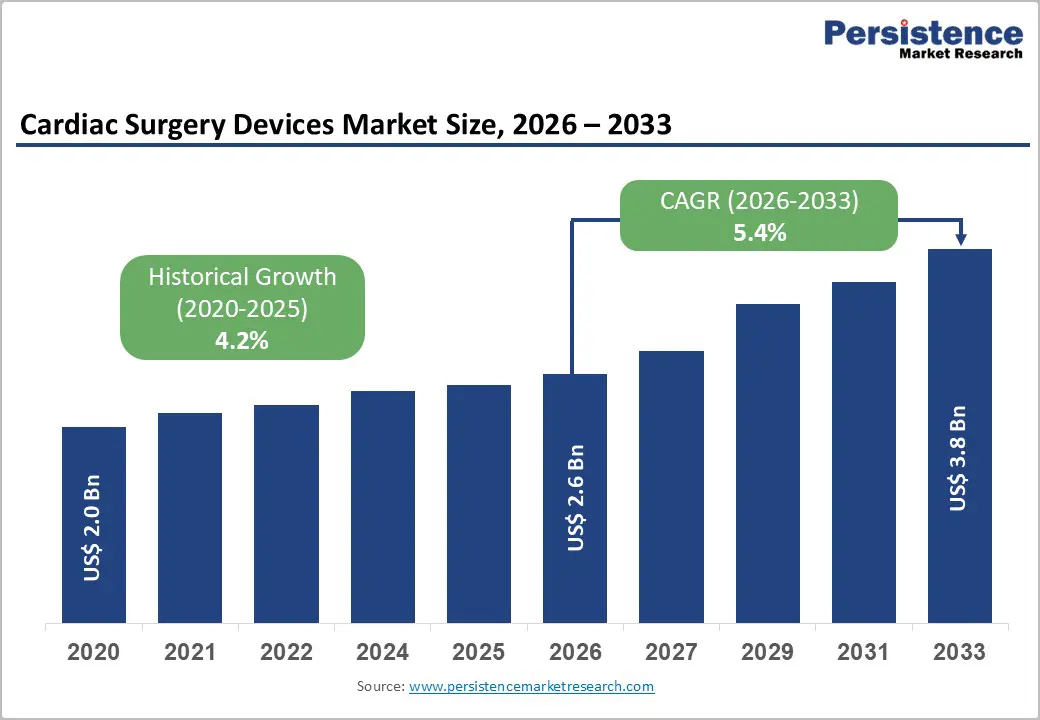

The global cardiac surgery devices market size is expected to be valued at US$ 2.6 billion in 2026 and projected to reach US$ 3.8 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033. This is driven by the rise in global burden of cardiovascular disease (CVD), the world's leading cause of death, combined with rapid innovation in minimally invasive cardiac surgery platforms, next-generation heart valve replacement systems, and advanced cardiopulmonary bypass (CPB) technology.

The World Health Organization (WHO) estimates that cardiovascular diseases account for approximately 17.9 million deaths annually, representing 32% of all global deaths. The American Heart Association (AHA) projects that by 2035, over 45% of the U.S. population will have some form of cardiovascular disease. These epidemiological trends, combined with aging global populations and expanding cardiac surgery infrastructure in the Asia Pacific, ensure sustained procedure volume growth and device market expansion by the forecast period.

Key Market Highlights

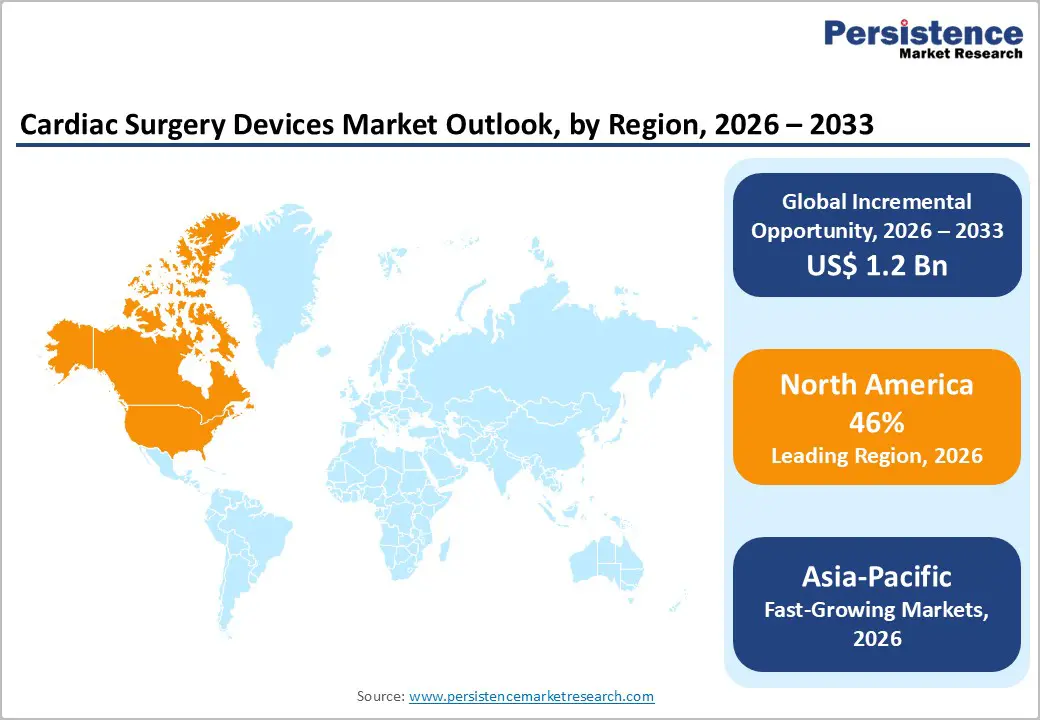

- Leading Region: North America leads the global Cardiac Surgery Devices market with approximately 46% revenue share in 2025, anchored by 200,000+ U.S. CABG procedures annually (STS database), AHA-backed guideline innovation, and headquarters concentration of global cardiac device leaders.

- Fastest Growing Region: Asia Pacific is the fastest growing cardiac surgery devices region during 2026 - 2033, led by China's 200,000+ annual open-heart surgeries (CSTCVS), India's growing private cardiac hospital network, and Healthy China 2030 cardiovascular care investments.

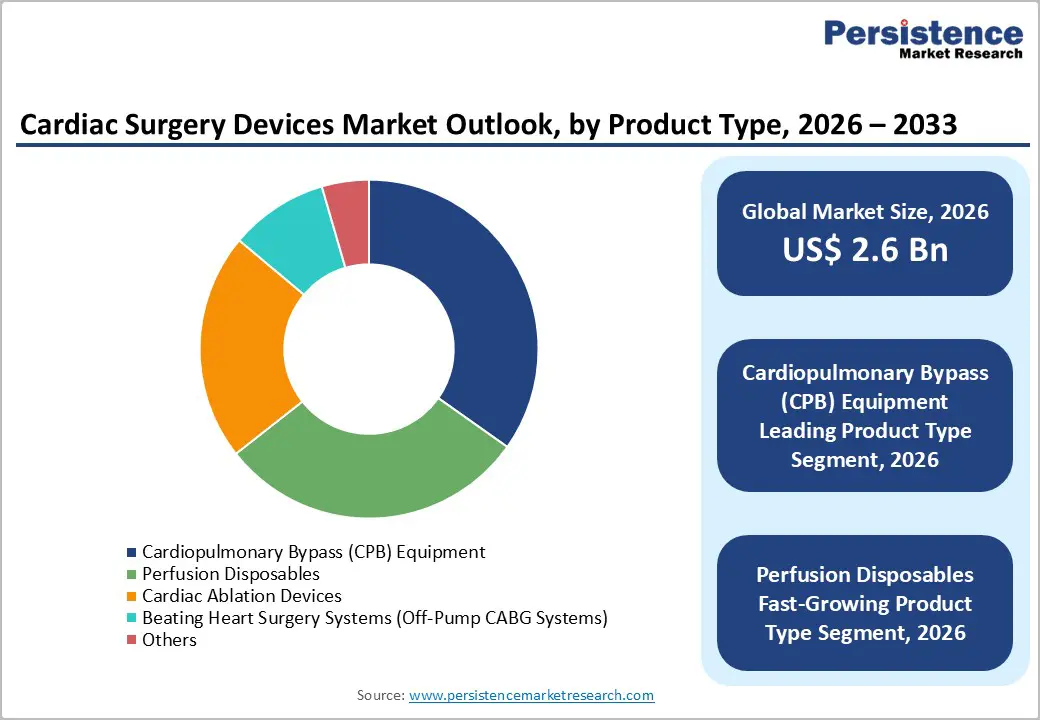

- Dominant Segment: Cardiopulmonary Bypass (CPB) Equipment leads with approximately 34% market share in 2025, driven by its non-substitutable role in all open-heart procedures and recurring per-case disposable demand across the 1 million+ global cardiac operations performed annually.

- Fastest Growing Segment: Cardiac Ablation Devices are the fastest growing product type during 2026 - 2033, fueled by AF affecting 37 million people globally (European Heart Journal) and ACC/AHA/HRS 2023 Guidelines expanding surgical ablation indications for concomitant cardiac procedures.

- Key Opportunity: Asia Pacific cardiac surgery expansion with India's 800,000+ annual cardiac procedures and China's CSTCVS-reported growth combined with Ayushman Bharat and Healthy China 2030 funding, offers high-volume device procurement opportunities for manufacturers with regionally adapted CPB and ablation portfolios.

Market Dynamics

Does The Rise in Global Cardiovascular Disease Burden and Surgical Intervention Volumes Fuel Growth?

Cardiovascular disease is the world's leading cause of death, with the WHO estimating 17.9 million CVD deaths annually. Coronary artery disease (CAD) and valvular heart disease the two most common indications for cardiac surgery are driven by aging populations, rising obesity, hypertension, and type 2 diabetes. The Society of Thoracic Surgeons (STS) database reports over 200,000 CABG procedures and approximately 100,000 heart valve procedures performed annually in the U.S. alone.

Globally, cardiac surgical procedure volumes are estimated at over 1 million operations per year, each requiring CPB equipment, perfusion disposables, and specialized surgical instruments directly driving per-procedure device and disposable revenue. The structural aging of populations in North America, Europe, and Asia Pacific ensures this procedure volume will grow steadily through 2033.

How Does the Innovation in Minimally Invasive Cardiac Surgery and Transcatheter Technologies Contribute?

The shift toward minimally invasive cardiac surgery (MICS) and hybrid surgical-interventional approaches is expanding the range of devices used per procedure and improving clinical outcomes that drive adoption. Medtronic's minimally invasive valve replacement platforms and Edwards Lifesciences' SAPIEN transcatheter heart valve system, which has achieved over 1 million implants globally demonstrate the commercial scale of this transition.

The AHA/ACC 2021 Valvular Heart Disease Guidelines broadened TAVR (Transcatheter Aortic Valve Replacement) indications to include intermediate- and low-surgical-risk patients, dramatically expanding the potential procedural volume. AtriCure Inc.'s surgical ablation systems for atrial fibrillation (AF) treatment during open-heart surgery represent another high-growth innovation vector, with FDA-cleared indications enabling concomitant cardiac ablation procedures.

How Does the High Cost of Cardiac Surgery Devices and Limited Reimbursement in Emerging Markets Affect Growth?

Advanced cardiac surgery platforms, including oxygenators, heart-lung machines, and minimally invasive CABG systems, carry substantial per-unit and per-procedure costs that constrain adoption in cost-sensitive healthcare systems. A complete CPB circuit costs approximately US$ 500-1,500 per case in disposables alone, while comprehensive cardiac surgery suites require millions in capital investment. In Asia Pacific, Latin America, and the Middle East & Africa, limited insurance coverage for cardiac surgery and reimbursement caps significantly restrict device adoption, preventing equitable access to evidence-based cardiac surgical care.

Competition from Catheter-Based Interventions Reducing Open Cardiac Surgery Volumes

The growing clinical effectiveness of percutaneous catheter-based cardiac interventions, including PCI (Percutaneous Coronary Intervention) and TAVR is structurally reducing the volume of traditional open cardiac surgery for certain indications. The EXCEL and NOBLE trials demonstrated comparable outcomes between PCI and CABG for multivessel CAD in selected patients, influencing cardiologists and patient preference away from surgery. This substitution effect creates a competitive ceiling on traditional cardiac surgery device volumes, particularly for CABG-related CPB and instrument segments.

How do the Cardiac Ablation Devices Pose as the Fastest Growing Segment, Driven by the Atrial Fibrillation Burden

Cardiac ablation devices represent the fastest growing product type in the cardiac surgery devices market, propelled by the rise in global prevalence of atrial fibrillation (AF) the most common sustained cardiac arrhythmia. The European Heart Journal estimates that AF affects approximately 37 million people globally, a number projected to double by 2060 due to population aging. AtriCure Inc.'s LARIAT and Enclose surgical ablation systems and Medtronic's CryoMaze are gaining clinical adoption as the 2023 ACC/AHA/ACCP/HRS AF Guidelines expand indications for surgical ablation in patients undergoing concomitant cardiac surgery.

As AF-related hospitalization costs exceed US$ 26 billion annually in the U.S., according to the AHA, the economic case for surgical cure is compelling, driving strong growth in surgical ablation device adoption through 2033.

Asia Pacific Cardiac Surgery Infrastructure Expansion: Region's Fastest Growing Market

Asia Pacific represents the fast-growing regional market for cardiac surgery devices, driven by rapidly expanding cardiac surgical capacity, rising cardiovascular disease incidence from lifestyle changes, and government healthcare investment programs. China performs over 200,000 open-heart surgeries annually, according to the Chinese Society for Thoracic and Cardiovascular Surgery (CSTCVS), with volumes growing as tertiary hospital infrastructure expands under Healthy China 2030.

India's cardiac surgery volumes are growing through both Ayushman Bharat-funded government hospital procedures and rapidly expanding private cardiac hospital networks, including Narayana Health, Apollo Hospitals, and Fortis Healthcare. Companies with locally adapted product portfolios, affordable CPB disposable lines, and trained clinical support teams in this region are positioned to capture substantial incremental device revenue.

Category-wise Analysis

Product Type Insights

The cardiopulmonary bypass (CPB) equipment segment leads the cardiac surgery devices market, accounting for approximately 34% of total product type revenue in 2026. CPB systems comprising heart-lung machines, oxygenators, arterial filters, and cardiotomy reservoirs are indispensable for virtually all open-heart procedures, creating a structurally recurring, high-volume consumable demand across every cardiac surgery globally.

The Society of Thoracic Surgeons (STS) database records over 200,000 CABG and 100,000 valve procedures annually in the U.S. alone, each requiring a complete CPB circuit. Leading system providers including LivaNova PLC (S5 Heart-Lung Machine), Medtronic, and Terumo (FX15 oxygenator) hold established market positions, and CPB's non-substitutable role in open cardiac surgery sustains this segment's revenue leadership through the forecast period.

Procedure Type Insights

The coronary artery bypass grafting (CABG) procedure type leads the cardiac surgery devices market, representing approximately 38% of procedure-based device revenue in 2025. CABG is the most commonly performed cardiac surgery globally and the definitive surgical revascularization procedure for multivessel coronary artery disease. The Society of Thoracic Surgeons (STS) reports it as the most performed cardiac surgical operation in its national database.

Despite competition from PCI for single- and some multivessel disease, AHA/ACC CABG Guidelines maintain surgical revascularization as the preferred approach for left main and complex three-vessel CAD. Each CABG procedure consumes CPB equipment, beating-heart systems, grafting instruments, and cardioplegia delivery products, generating the highest per-procedure device revenue in the cardiac surgery portfolio.

End-user Insights

The hospitals and cardiac centers segment leads the cardiac surgery devices market by end-user, accounting for approximately 72% of end-user revenue in 2025. The overwhelming dominance of hospitals reflects the complexity, acuity, and resource requirements of cardiac surgery, requiring cardiac anesthesia, perfusion teams, cardiac ICU facilities, and post-operative monitoring unavailable in outpatient settings. Joint Commission-certified comprehensive cardiac surgery programs and ACC Chest Pain Center-accredited hospitals in the U.S. concentrate the majority of national cardiac surgical volume.

Specialist cardiac surgery centers, including Cleveland Clinic, Texas Heart Institute, and the Mayo Clinic, are among the highest-volume cardiac device procurement institutions globally, sustaining the hospital channel's dominant end-user position throughout the forecast period.

Regional Insights

North America Cardiac Surgery Devices Market Trends and Insights

North America accounted for approximately 46.0% of the global cardiac surgery devices market in 2025, led by high surgical volumes, strong reimbursement systems, and rapid adoption of advanced perfusion and ablation technologies. The region benefits from the presence of major manufacturers such as Medtronic, Edwards Lifesciences, and Abbott. Robust FDA approvals and extensive hospital infrastructure continue to support premium device utilization across both adult and pediatric cardiac surgery.

U.S. Cardiac Surgery Devices Market Trends and Insights

The U.S. represented nearly 88.5% of the North American market in 2025. More than 800,000 myocardial infarctions occur annually, sustaining high demand for CABG, valve repair, and arrhythmia surgery. Favorable reimbursement from Medicare and private insurers, combined with strong innovation from domestic manufacturers, supports continued leadership in advanced cardiac surgery devices. High procedure volumes at leading institutions and rapid FDA approvals continue to accelerate adoption of next-generation perfusion systems, ablation technologies, and surgical consumables.

Canada Cardiac Surgery Devices Market Trends and Insights

Canada contributed around 8.7% of the North American market in 2025 and is projected to grow at a CAGR of 6.4% through 2033. Universal healthcare coverage and centralized cardiac surgery programs in provinces such as Ontario and Quebec ensure consistent procurement of cardiopulmonary bypass systems, oxygenators, and perfusion disposables. Ongoing investments in pediatric and adult cardiac centers are further supporting the adoption of advanced extracorporeal circulation technologies and surgical consumables across the country.

Europe Cardiac Surgery Devices Market Trends and Insights

Europe captured an estimated 27.8% of global market revenue in 2025, supported by universal healthcare systems, well-established cardiothoracic surgery centers, and standardized adoption under EU MDR regulations. Clinical practice guidelines from the European Association for Cardio-Thoracic Surgery promote uniform device utilization across the region. Demand is particularly strong in Western Europe, where aging populations are increasing the volume of valve and bypass procedures.

Germany Cardiac Surgery Devices Market Trends and Insights

Germany accounted for approximately 23.6% of the European market in 2025. The country performs over 100,000 cardiac surgeries annually and maintains one of Europe's most advanced hospital infrastructures. Comprehensive reimbursement through statutory health insurance supports widespread use of CPB equipment, cannulae, and ablation systems. Strong clinical adoption in high-volume university hospitals and heart centers continues to drive demand for technologically advanced perfusion systems and surgical consumables.

UK Cardiac Surgery Devices Market Trends and Insights

The UK represented about 16.9% of the regional market and is expected to grow at a CAGR of 6.1% through 2033. National Health Service funding and technology assessments by NICE continue to support adoption of advanced cardiac surgery devices in tertiary cardiac centers. The country is also witnessing increased utilization of minimally invasive valve repair, surgical ablation systems, and extracorporeal circulation technologies across leading institutions such as Royal Brompton and Harefield Hospitals and Guy's and St Thomas' NHS Foundation Trust.

Asia Pacific Cardiac Surgery Devices Market Trends and Insights

Asia Pacific is likely to account for approximately 20.9% of the global cardiac surgery devices market in 2026, driven by increasing cardiovascular disease prevalence, expansion of cardiac centers, and improving access to complex surgery. Multinational companies and domestic manufacturers are strengthening regional manufacturing and physician training to address rising procedural volumes.

China Cardiac Surgery Devices Market Trends and Insights

China is likely to account for nearly 41.8% share in 2026. More than 200,000 open-heart surgeries are performed annually, supported by government investment under Healthy China 2030 and the expansion of tertiary hospitals. Domestic manufacturers such as Lepu Medical Technology are increasing market penetration with competitively priced systems. Rising procurement by top cardiovascular centers and continued localization of high-value surgical devices are further strengthening China's position as the region's largest market.

India Cardiac Surgery Devices Market Trends and Insights

India represented around 18.6% of the Asia Pacific market in 2025 and is expected to reach a CAGR of 9.8% by 2033. Rapid expansion of private cardiac hospital networks, increasing insurance penetration, and growing affordability of bypass and valve surgery are accelerating adoption of advanced cardiac surgery devices. Leading hospital groups such as Narayana Health and Apollo Hospitals are expanding access to complex cardiac procedures, supporting higher utilization of perfusion disposables, ablation systems, and off-pump surgical technologies.

Competitive Landscape

The global cardiac surgery devices market is moderately consolidated, with Medtronic plc, Edwards Lifesciences Corporation, Abbott Laboratories, and LivaNova PLC commanding significant revenue positions across CPB, valve, and ablation device categories. Edwards Lifesciences dominates the transcatheter heart valve segment with SAPIEN, while AtriCure and Medtronic lead surgical ablation. Key differentiators include clinical evidence depth, FDA/CE clearance breadth, and hospital partnership programs.

Emerging competitive dynamics include Lepu Medical challenging international incumbents in China on cost, and the integration of AI-guided perfusion management into next-generation CPB platforms by LivaNova and Terumo.

Key Developments:

- In May 2026, Medtronic consolidated its Cardiac Surgery and Aortic business units to form a unified Cardiovascular Surgery business, aimed at streamlining operations and strengthening its surgical cardiovascular portfolio.

- In January 2025, Boston Scientific Corporation acquired Bolt Medical, Inc., the developer of an advanced laser-based intravascular lithotripsy (IVL) platform for the treatment of coronary and peripheral artery disease.

- In April 2024, Abbott Laboratories received U.S. FDA approval for its heart valve repair device for patients with a potentially fatal heart disease, just months after its rival, Edwards Lifesciences, had received the regulator's approval for its device.

Companies Covered in Cardiac Surgery Devices Market

- Medtronic plc

- Edwards Lifesciences Corporation

- Abbott Laboratories

- Boston Scientific Corporation

- LivaNova PLC

- Terumo Corporation

- Artivion, Inc.

- AtriCure, Inc.

- Teleflex Incorporated

- Stryker Corporation

- Johnson & Johnson Services, Inc.

- B. Braun SE

- Lepu Medical Technology Co., Ltd.

- BD (Becton, Dickinson and Company)

- Others

Frequently Asked Questions

The global cardiac surgery devices market is estimated to be valued at US$ 2.6 billion in 2026, growing from US$ 2.0 billion in 2020 at a historical CAGR of 4.2% (2020-2025). The market is projected to reach US$ 3.8 billion by 2033, growing at a forecast CAGR of 5.4% between 2026 and 2033.

The rise in global prevalence of coronary artery disease, valvular heart disorders, and congenital heart defects is increasing the volume of cardiac surgeries and demand for advanced surgical devices.

North America leads with approximately 46% of global cardiac surgery devices revenue in 2025. The U.S. is the dominant national market, driven by 805,000+ annual heart attacks (AHA), comprehensive Medicare cardiac surgery coverage, the world's highest concentration of cardiac surgery innovation leaders, and robust FDA regulatory infrastructure supporting rapid device approval.

Expanding adoption of minimally invasive and robotic-assisted cardiac surgery technologies in emerging markets is creating significant growth opportunities for device manufacturers.

The cardiac surgery devices market is led by Medtronic plc (CPB, valves, ablation), Edwards Lifesciences (SAPIEN transcatheter valves 1M+ implants), Abbott Laboratories, LivaNova PLC (Essenz CPB system), and AtriCure (surgical ablation). CPB specialists include Terumo, B. Braun SE, and Getinge AB. Artivion leads aortic surgery, Lepu Medical competes in China's domestic market, and Boston Scientific, Stryker, and Teleflex serve complementary cardiac surgery device segments.