- Medical Devices

- Cardiac Arrhythmia Monitoring Devices Market

Cardiac Arrhythmia Monitoring Devices Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Cardiac Arrhythmia Monitoring Devices Market by Device {Holter Monitors, Electrocardiogram (ECG) Monitors, Mobile Cardiac Telemetry (MCT), Event Monitors, Implantable Cardiac Monitors (ICMs), Others}, Application (Atrial Fibrillation (AFib), Tachycardia, Bradycardia, Premature Cardiac Contraction, Others), End-user (Hospitals and Clinics, Diagnostic Centers, Ambulatory Surgical Centers, Homecare Settings, Others), and Regional Analysis from 2026 to 2033

Cardiac Arrhythmia Monitoring Devices Market Share and Trends Analysis

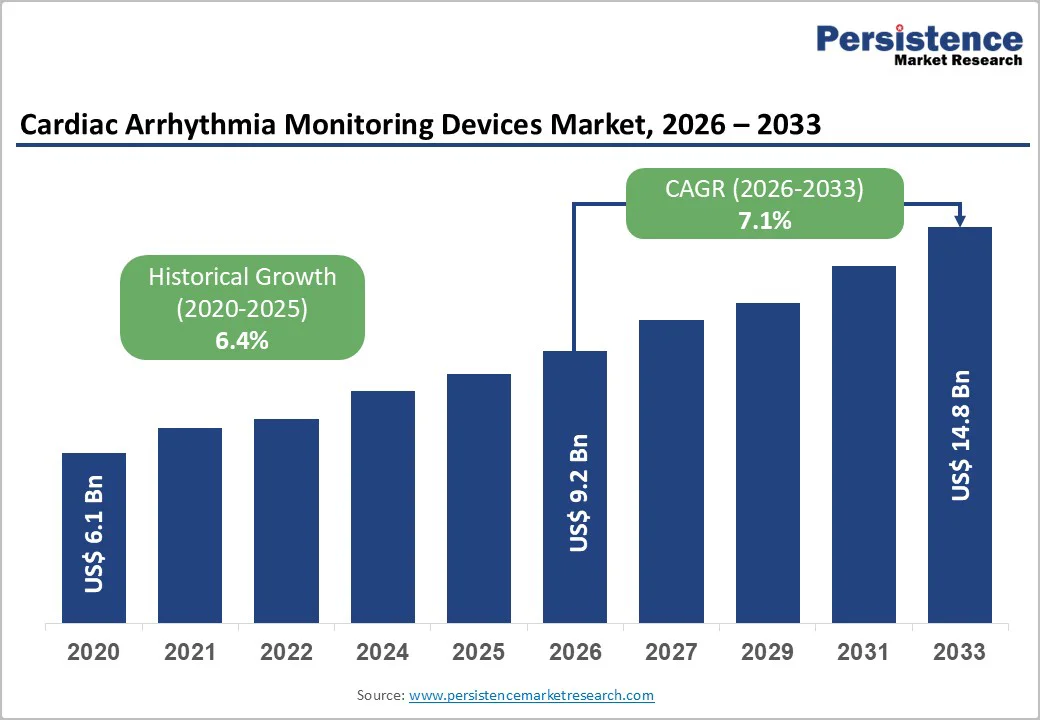

The global cardiac arrhythmia monitoring devices market size is estimated to grow from US$ 9.2 billion in 2026 to reach US$ 14.8 billion by 2033, growing at a CAGR of 7.1% during the forecast period from 2026 to 2033.

The cardiac arrhythmia monitoring devices market is growing rapidly, fueled by rising bradycardia cases, demand for minimally invasive therapies, and fewer lead-related complications. North America leads with high device adoption, strong reimbursement, and advanced electrophysiology centers. Asia Pacific is the fastest-growing region, driven by increasing cardiac procedures, improved healthcare access, and adoption of next-generation leadless devices.

Key Industry Highlights:

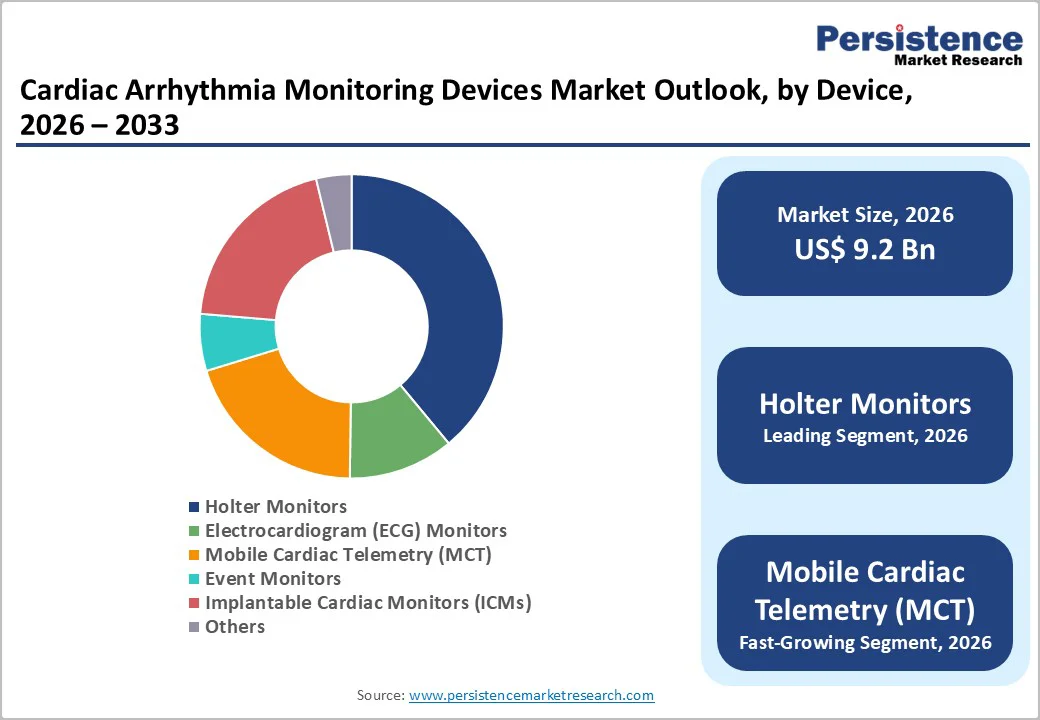

- Dominant Segment: Holter monitors lead with 39.0% share due to wide clinical adoption, affordability, and accuracy. MCT grows fastest for remote monitoring; implantable monitors remain niche.

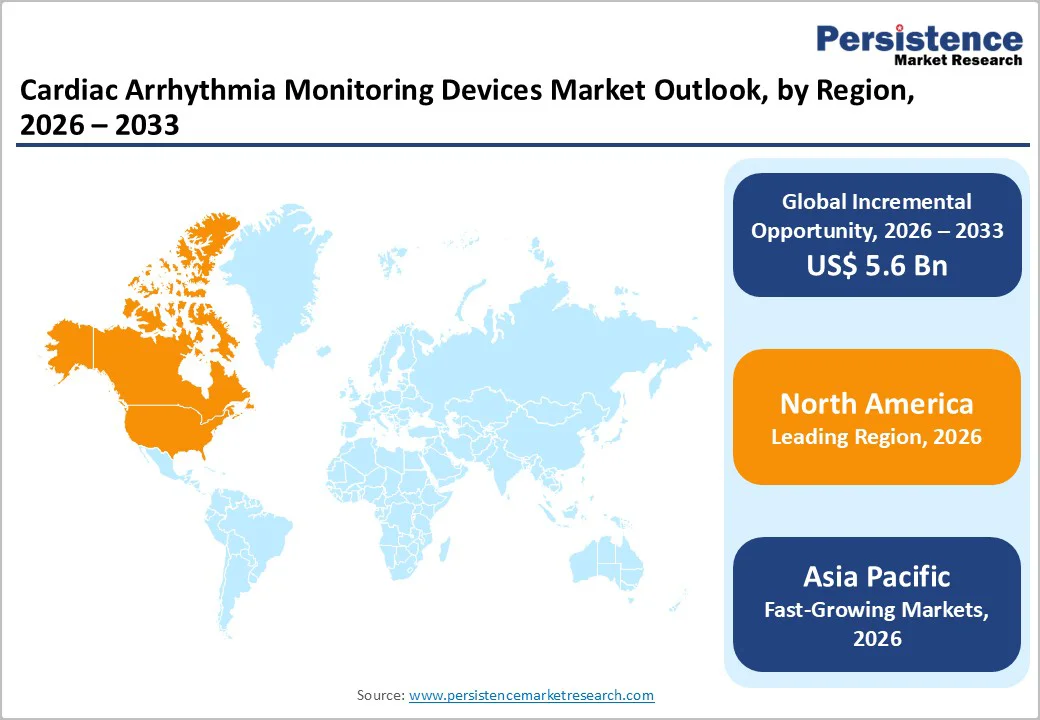

- Dominant Region: North America takes 44.1% share in 2025, with high adoption, advanced EP labs, and reimbursement. Europe follows; Asia Pacific grows fastest due to rising cardiovascular cases and hospital infrastructure expansion.

- Growth Indicator: Rising AFib, tachycardia, prevalence of bradycardia, demand for remote and continuous monitoring, wearable technology, minimally invasive solutions, elderly population growth, and telehealth integration drive market expansion.

- Market Opportunity: Growth opportunities include MCT and wearable adoption, AI-enabled detection, long-term implantable monitors, telehealth platforms, value-tier devices, and partnerships targeting AFib, tachycardia, bradycardia, and premature contractions.

| Key Insights | Details |

|---|---|

| Global Cardiac Arrhythmia Monitoring Devices Market Size (2026E) | US$ 9.2 Bn |

| Market Value Forecast (2033F) | US$ 14.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

Market Dynamics

Driver - Growing Preference for Remote and Wearable Monitoring

These technologies enable continuous, real-time heart rhythm tracking outside hospital settings. This is particularly valuable for detecting intermittent or asymptomatic arrhythmias and for long-term patient follow-up. Adoption of connected health devices has grown sharply in recent years, reflecting greater patient and provider comfort with remote monitoring.

Wearable ECG devices, including patches, smart textiles, and wrist-worn monitors, allow passive or active surveillance and transmit data to clinicians via cloud-based systems, improving diagnosis and management efficiency. These devices are especially useful for elderly patients and those with chronic cardiovascular conditions, reducing the need for frequent hospital visits.

Advances in sensor technology, battery life, and wireless connectivity have made monitoring more accurate and convenient. Rising prevalence of cardiovascular diseases, coupled with increasing patient preference for non-invasive and user-friendly monitoring solutions, continues to accelerate adoption and transform arrhythmia management.

Restraints - Reimbursement & Insurance Limitations

Reimbursement and insurance limitations are major restraints for the cardiac arrhythmia monitoring devices market, restricting patient access to advanced monitoring technologies. In countries like India, only about 3-5% of the population has health insurance, forcing the majority to pay out-of-pocket for devices such as Holter monitors, wearable ECG patches, and long-term implantable monitors.

Even in high-income regions, reimbursement for extended-duration or remote monitoring devices is often limited to specific clinical indications, leaving patients responsible for 20-35% of the device cost. High out-of-pocket expenses discourage use, particularly among middle- and low-income patients, reducing overall adoption rates.

Partial or inconsistent coverage also affects hospitals and clinics, as they may hesitate to invest in advanced monitoring infrastructure without guaranteed reimbursement. Consequently, financial and insurance barriers slow the uptake of newer, more capable arrhythmia-monitoring solutions, limiting the market’s expansion despite growing cardiovascular disease prevalence and technological advancements in wearable and remote monitoring devices.

Opportunity - Long-Term Implantable Monitoring Solutions

Long-term implantable monitoring solutions present a significant opportunity in the cardiac arrhythmia monitoring devices market by enabling the detection of arrhythmias that short-term monitoring often misses.

Studies show that nearly 46% of patients with implantable cardiac monitors (ICMs) received a clinically significant arrhythmia diagnosis within months, many of whom were asymptomatic, highlighting the superiority of long-term monitoring over 24-hour Holter or periodic external devices.

In patients with cryptogenic stroke, continuous ICM monitoring detected atrial fibrillation in about 21.5% of cases over two years, identifying arrhythmias that would likely have been missed with conventional monitoring. These devices allow early diagnosis and timely interventions, such as anticoagulation therapy, pacemaker implantation, or defibrillator use, improving patient outcomes.

With the global burden of cardiovascular disease rising and increasing awareness of asymptomatic arrhythmias, the adoption of long-term implantable monitoring solutions is expanding. Their ability to provide continuous, reliable, and minimally invasive monitoring positions them as a key growth driver in the arrhythmia monitoring market.

Category-wise Analysis

By Device, Holter Monitors Dominates the Cardiac Arrhythmia Monitoring Devices Market

Holter Monitors occupies 39.0% share of the global market in 2025, because they provide continuous 24-48 hour heart rhythm recording, capturing cardiac activity during normal daily life, unlike standard ECGs that offer only brief snapshots.

Studies show that in a seven-day monitoring period, only 35% of arrhythmias were detected in the first 24 hours, while 65% were identified afterward, demonstrating the advantage of continuous monitoring for detecting intermittent arrhythmias.

Holter monitors are non-invasive, relatively low-cost, and widely available in hospitals and clinics, making them accessible for routine cardiac assessment. Their ease of use, reliability, and ability to detect a wide range of arrhythmias, including asymptomatic events, ensure that they remain the preferred choice for clinicians, sustaining their dominance in the global arrhythmia monitoring market.

By Application, Atrial Fibrillation (AFib) is gaining traction due to high prevalence, asymptomatic cases, and elevated stroke risk, driving monitoring demand

Atrial fibrillation (AFib) dominates the cardiac arrhythmia monitoring devices market because it is the most common cardiac rhythm disorder, affecting about 1-3% of the general population and up to 9% of individuals over 65. Many cases are intermittent or asymptomatic, with approximately 62% of patients unaware of their condition before diagnosis.

AFib significantly increases stroke risk, roughly fivefold compared with normal heart rhythm, and contributes to about one in seven strokes. Due to its high prevalence, serious complications, and often silent presentation, continuous and long-term cardiac monitoring is critical for early detection and management.

These factors drive clinicians to rely heavily on monitoring devices, making AFib the largest application segment and sustaining its dominance in the cardiac arrhythmia monitoring market.

Regional Insights

North America Cardiac Arrhythmia Monitoring Devices Market Trends

North America dominates the cardiac arrhythmia monitoring devices market with 44.1% share in 2025, because it carries a very high burden of cardiovascular disease and arrhythmias. In the U.S., nearly half of adults had cardiovascular disease in 2020. Continuously rising arrhythmia and heart-disease prevalence creates a large pool of patients needing monitoring.

The region also has a well-developed healthcare infrastructure, with widespread electrophysiology labs and hospitals capable of delivering advanced cardiac monitoring and follow-up care. Favorable reimbursement policies and insurance coverage make device-based monitoring more accessible.

Combined with high clinical awareness and strong adoption of innovations, these factors ensure sustained demand and lead to North America’s leadership in arrhythmia-monitoring device adoption.

Europe Cardiac Arrhythmia Monitoring Devices Market Trends

Europe is an important region in the cardiac arrhythmia monitoring devices market due to its high cardiovascular disease burden. In the WHO European Region, cardiovascular diseases account for approximately 42-45% of all deaths, representing the highest proportion globally. Arrhythmias, particularly atrial fibrillation, are prevalent, affecting around 15.7?million people across member countries.

Strong public healthcare infrastructure and statutory health coverage in countries like Germany and France support widespread adoption of diagnostic monitoring, including ambulatory ECGs, Holter monitors, and implantable devices. The aging population further increases demand for continuous and long-term arrhythmia monitoring.

Combined with high clinical awareness and robust cardiology networks, Europe remains a key and stable market for arrhythmia monitoring devices, sustaining consistent adoption of advanced wearable, implantable, and remote monitoring technologies.

Asia Pacific Cardiac Arrhythmia Monitoring Devices Market Trends

Asia Pacific is the fastest-growing region in the market due to a rapidly increasing cardiovascular disease (CVD) burden. In 2021, Asia accounted for approximately 61% of global CVD deaths. Cardiovascular diseases caused around 9.85?million deaths in WHO South-East Asia and Western Pacific countries, representing 45-50% of non-communicable disease-related mortality.

Rising arrhythmia prevalence, hypertension, and metabolic disorders, combined with an aging population, are increasing the need for continuous cardiac monitoring. Limited hospital-based diagnostic infrastructure in many areas drives adoption of ambulatory ECGs, wearable devices, and long-term implantable monitors.

Growing awareness of heart disease, improving healthcare access, and the demand for convenient, remote, and cost-effective monitoring solutions further accelerate market growth, making Asia Pacific the fastest-expanding region for arrhythmia monitoring devices globally.

Competitive Landscape

Leading companies in the cardiac arrhythmia monitoring devices market focus on reliable, innovative, and patient-friendly solutions. They invest in wearable, implantable, and remote monitoring technologies, enhance device accuracy and battery life, and collaborate with healthcare providers. R&D emphasizes simplicity, safety, and cost-effectiveness, supporting broader adoption across atrial fibrillation, tachycardia, bradycardia, and other arrhythmia management globally.

Key Industry Developments:

- In November 2025, iRhythm Technologies announced that a large-scale study had been published in Heart Rhythm, and new data were presented at the 2025 American Heart Association (AHA) Scientific Sessions. The study provided insights into the effectiveness and clinical impact of iRhythm’s cardiac monitoring solutions, reinforcing the role of wearable and remote arrhythmia monitoring in improving patient diagnosis and management.

- In April s2025, Medtronic expanded its Acute Care & Monitoring portfolio by signing a new distribution agreement for the Argos™ cardiac output monitor. This agreement enabled broader access to Medtronic’s advanced hemodynamic monitoring technology, supporting hospitals and clinicians in delivering precise cardiac output measurements for critically ill patients and enhancing patient care in acute care settings.

- In September 2024, iRhythm Technologies announced that it had received regulatory approval in Japan for its Zio® ECG Monitoring System, marking it as the first product in the country to provide arrhythmia monitoring services using artificial intelligence.

Companies Covered in Cardiac Arrhythmia Monitoring Devices Market

- iRhythm Technologies

- Medtronic plc

- AliveCor

- Biotronik

- Koninklijke Philips N.V

- GE Healthcare

- St. Jude Medical (Abbott Laboratories)

- Biotricity

- Nihon Kohden Corporation

- Spacelabs Healthcare (OSI Systems, Inc.)

- Welch Allyn (Hillrom Services, Inc.)

- Others

Frequently Asked Questions

The global cardiac arrhythmia monitoring devices market is projected to be valued at US$ 9.2 Bn in 2026.

Rising arrhythmia prevalence, aging population, demand for remote and wearable monitoring, technological advancements, and preference for minimally invasive, continuous cardiac monitoring.

The global cardiac arrhythmia monitoring devices market is poised to witness a CAGR of 7.1% between 2026 and 2033.

Expansion of wearable, mobile, and implantable monitors, AI integration, telehealth platforms, long-term monitoring solutions, and growth in emerging Asia Pacific and value-tier markets.

iRhythm Technologies, Medtronic plc, AliveCor, Biotronik, Koninklijke Philips N.V, GE Healthcare.