- Medical Devices

- Cardiac Pacemaker Market

Cardiac Pacemaker Market Size, Share, and Growth Forecast, 2025 - 2032

Cardiac Pacemaker Market by Technology (Single-Chamber Pacemakers, Dual-Chamber Pacemakers, Others), Clinical Indication (Bradycardia, Arrhythmias, Congestive Heart Failure (CHF), Others), End-user (Hospitals & Cardiac Centers, Others), and Regional Analysis for 2025 - 2032

Cardiac Pacemaker Market Share and Trends Analysis

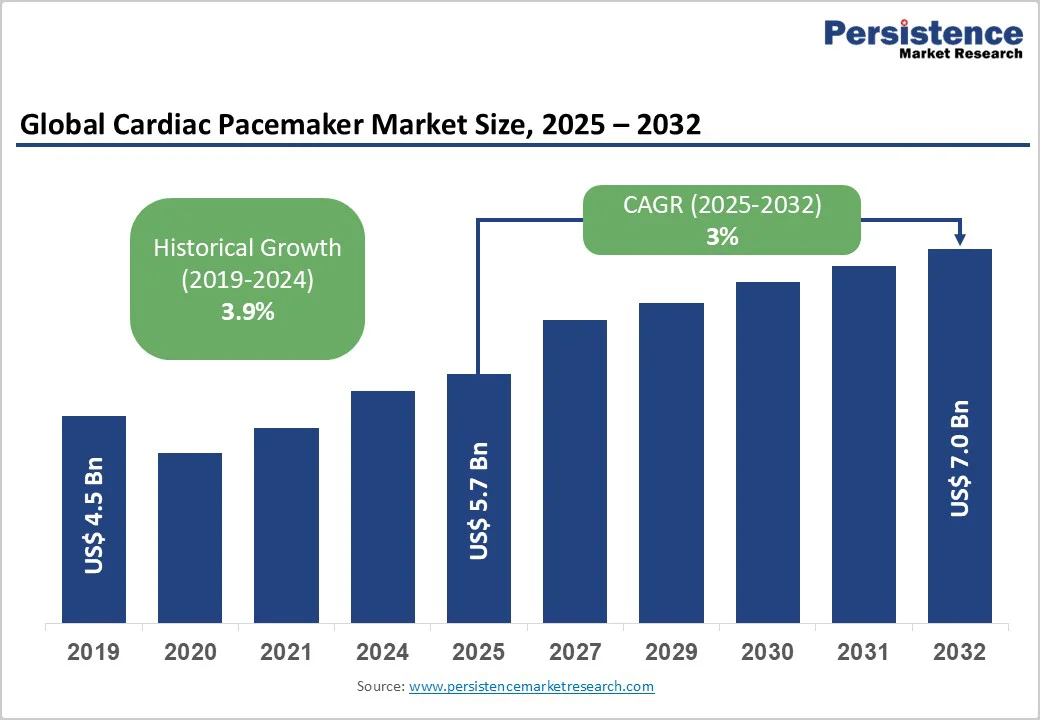

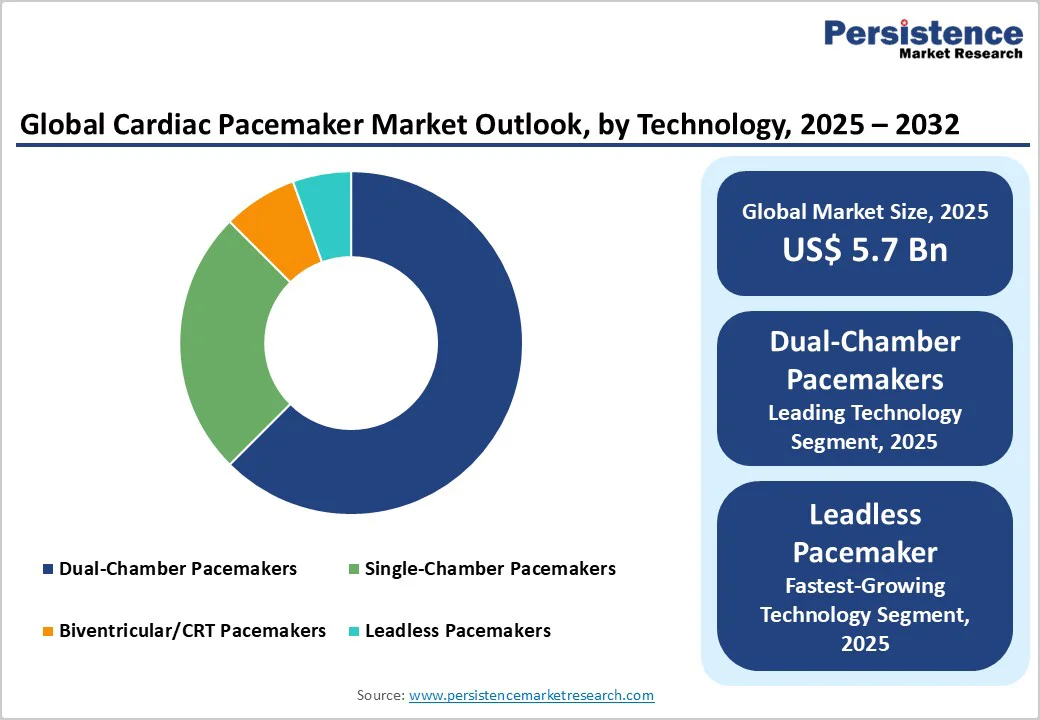

The global cardiac pacemaker market size is likely to be valued at US$5.7 Billion in 2025, and is estimated to reach US$7.0 Billion by 2032, growing at a CAGR of 3% during the forecast period 2025 - 2032, driven by the rising global prevalence of cardiovascular disorders (CVDs), such as arrhythmias and bradycardia, particularly in aging populations, alongside technological advancements such as leadless and MRI-compatible devices expanding therapeutic options.

Improving healthcare infrastructure and rising procedure volumes in emerging economies, offsetting saturation in mature regions, will drive market growth. Remote monitoring and minimally invasive procedures are redefining demand and supporting sustained expansion.

Key Industry Highlights

- Dominant Technology: Dual-chamber pacemakers dominate with an estimated 63% market share as of 2025, supported by advanced sensing and pacing features.

- Fastest-growing Technology: Leadless pacemakers are the fastest-growing technology segment, driven by safety and minimally invasive procedure benefits.

- Largest Clinical Indications: Bradycardia represents the largest clinical indication segment, with 26.1% market share, while arrhythmias are growing the fastest due to enhanced diagnostics and patient awareness.

- Leading End-users: Hospitals and cardiac centers are the main end-users, holding an estimated 70.3% market share in 2025, while ASCs are the fastest-growing segment through 2032, reflecting outpatient procedural shifts.

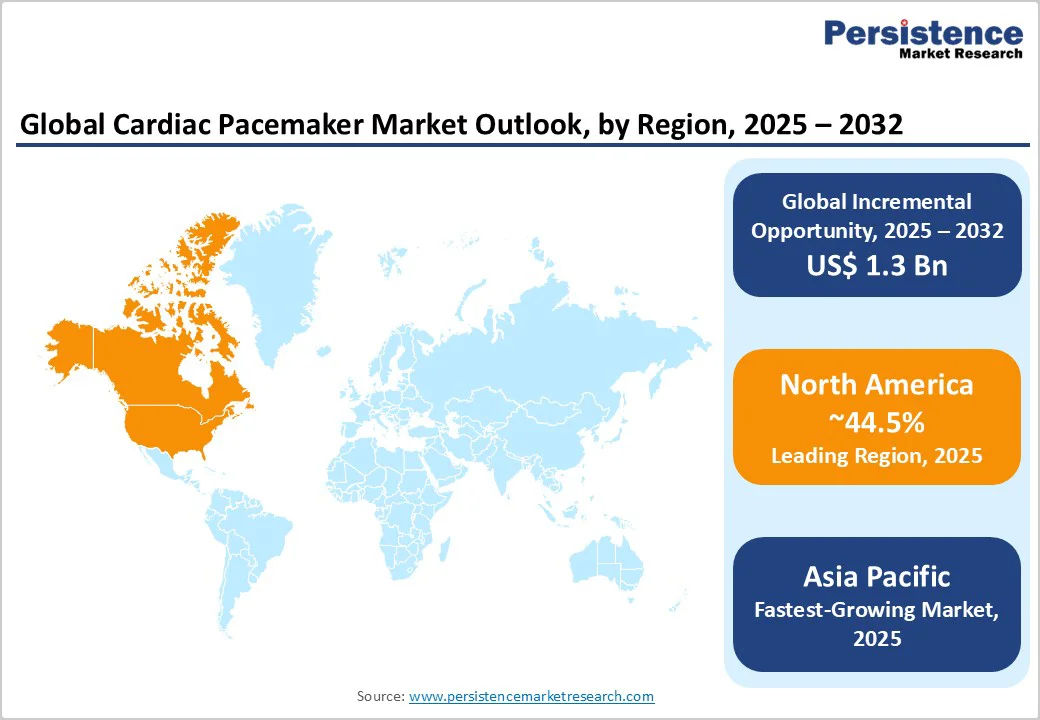

- Dominant Region: North America commands around 44.5% market share in 2025, leveraging a mature innovation environment and reimbursement structures.

- Regional Dynamics: Europe accounts for 37% market share, benefiting from regulatory harmonization and aging demographics, while Asia Pacific leads through 2032, supported by infrastructure investments and emerging market penetration.

- September 2025: Boston Scientific received CE-mark approval to expand the indications for its Ingevity+ pacing leads to include conduction system pacing (CSP) and sensing of the left bundle branch area (LBBA) when used with single- or dual-chamber pacemakers.

| Key Insights | Details |

|---|---|

| Cardiac Pacemaker Market Size (2025E) | US$5.7 Bn |

| Market Value Forecast (2032F) | US$7.0 Bn |

| Projected Growth (CAGR 2025 to 2032) | 3% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growing Incidence of Age-Related CVDs to Stoke Demand for Advanced Pacemaker Solutions

The escalating global demographic shift toward older populations is profoundly fueling demand for cardiac pacemakers. According to the World Health Organization (WHO), by 2030, one in six people worldwide will be aged 60 years or older, with cardiovascular disorders disproportionately affecting this age group.

Bradycardia and arrhythmias frequently require pacemaker implantation for symptomatic relief and mortality reduction. This demographic trend is complemented by increasing awareness and early diagnosis facilitated by advancements in cardiac diagnostics and continuous cardiac telemetry.

Technological advancements providing tailored pacing solutions, such as leadless pacemakers with fewer procedural complications and increased device longevity, are gaining traction, reinforcing adoption among older patients with comorbidities. Progressive reimbursement policies under Medicare and similar agencies globally are improving patient access to innovative pacing therapies, amplifying market traction.

The increasing adoption rate in emerging economies where aging populations are rapidly expanding is particularly notable, contributing significantly to the worldwide volume growth. This macroeconomic and demographic synergy is uplifting device demand, creating a durable foundation for market growth.

Regulatory Complexity and Cost Constraints Slowing Market Access and Uptake

Cardiac pacemaker manufacturers and healthcare providers are facing growing regulatory challenges that pose cost barriers and delay market penetration. The regulatory landscape governing implantable cardiac devices is stringent, with governing bodies such as the U.S. Food and Drug Administration (FDA), European Medicines Agency (EMA), and national health authorities requiring comprehensive clinical data for device safety and efficacy.

The recent introduction of enhanced post-market surveillance, unique device identification (UDI) requirements, and cybersecurity demands is increasing compliance costs substantially.

Smaller manufacturers, particularly in emerging regions, encounter hurdles in navigating these complex regulatory pathways, delaying product launches. The high upfront acquisition costs of advanced pacemakers, especially leadless and MRI-compatible models, strain hospital budgets and patient affordability, limiting adoption in price-sensitive markets.

For instance, the costs of leadless pacemakers can be up to three to five times higher than conventional devices, impacting reimbursement approvals and insurance coverage policies. Supply chain challenges, intensified by fluctuating raw material costs and geopolitical tensions affecting semiconductor availability, impose additional operational constraints.

Expanding Infrastructure and Rising Cardiac Care Capacity in Emerging Economies

Amidst global demand consolidation, the most lucrative growth potential lies in emerging markets, where healthcare infrastructure development and increasing cardiac disease burden are catalyzing pacemaker adoption. Countries such as China, India, Brazil, and Southeast Asian nations are witnessing accelerated investments in tertiary care and cardiac centers, supported by favorable government policies and international funding initiatives.

The unmet need remains substantial, as expanding access to cardiac centers, improving physician training, and growing telemedicine adoption collectively broaden procedural reach. The affordability gap is being progressively bridged by localized manufacturing and tailored device offerings.

This infrastructure momentum aligns with increasing insurance coverage and rising middle-class healthcare expenditure. Market players capable of effective localization, compliance with regional regulatory frameworks, and technology transfer stand to capitalize lucratively. The integration of remote monitoring platforms also addresses geographical healthcare service disparities, enhancing patient follow-up adherence and outcomes.

Category-wise Analysis

Technology Insights

The dual-chamber pacemakers segment is unequivocally the market leader in 2025, commanding an estimated 63% revenue share. These devices are preferred due to their sophisticated ability to manage complex cardiac conditions by synchronously pacing both the atrium and ventricle, thereby optimizing cardiac output and reducing symptoms in patients with bradyarrhythmias and conduction disorders.

The dual-chamber systems’ enhanced programmability and integration with sensor technologies improve patient outcomes, making them highly favored by electrophysiologists, especially in developed markets. Recent iterations also feature wireless remote monitoring capabilities and auto-adjusting pacing rates, which have scaled clinical preference and reimbursement inclusion globally.

On the other hand, the fastest-growing technology segment within the forecast period 2025 - 2032 is leadless pacemakers. Leadless pacemakers are revolutionizing the landscape by eliminating the need for transvenous leads, thus mitigating lead-associated complications such as infections, venous thrombosis, and lead fracture.

Their minimally invasive, catheter-based implantation procedures reduce hospitalization duration and procedural risk, particularly benefiting elderly and comorbid patient cohorts. Increased regulatory approvals alongside expanded clinical indications, especially for single-chamber use in resource-constrained and aging populations, are driving robust volume growth.

Clinical Indication Insights

Bradycardia continues to dominate as the prime clinical indication, capturing approximately 26.1% of the cardiac pacemaker market revenue share in 2025. Pacemaker therapy’s indication for symptomatic bradycardia, including sinus node dysfunction and atrioventricular blocks, is well-established in clinical guidelines, ensuring steady demand.

The aging global demographic surge intensifies this demand, as conduction abnormalities are prevalent in geriatric populations. Enhanced detection of asymptomatic bradycardia via wearable ECG devices is also broadening the clinical population eligible for pacing therapy.

Arrhythmias, encompassing atrial fibrillation and heart block variants, are likely to exhibit the most accelerated growth between 2025 and 2032. This dynamic expansion is propelled by heightened awareness, facilitated by advanced ambulatory cardiac monitoring devices enabling early diagnosis and timely intervention.

The expanding clinical scope comprises patients with concurrent tachy-brady syndromes and long QT syndrome, increasing the use case for dual-chamber and leadless pacemakers with sophisticated sensing modalities. Clinical trials validating pacing benefits in arrhythmia subpopulations further underpin expanding reimbursement and guideline recommendations worldwide, thereby accelerating market growth within this segment.

End-user Insights

Hospitals and cardiac centers remain the predominant end-user segment with an estimated 70.3% market share in 2025, anchored by their comprehensive cardiac surgery infrastructure and multidisciplinary healthcare teams.

These facilities are equipped to perform complex device implantations, follow-ups, and advanced pacing therapies requiring inpatient care, including device upgrades and revisions. Hospitals benefit from robust contracting power with suppliers, and established reimbursement pathways favoring advanced pacemaker therapy adoption, ensuring their market dominance.

Ambulatory surgical centers (ASCs) are emerging rapidly, registering the highest CAGR through 2032, signifying a substantial shift in healthcare delivery paradigms. This growth trajectory is supported by healthcare payers incentivizing outpatient care models due to lower costs and improved patient convenience.

Advances in pacemaker implantation techniques and shorter procedural times favor ASC adoption, especially for less complex cases such as single-chamber device insertions. ASCs are also increasingly integrating remote monitoring and telehealth follow-up protocols, further enhancing utilization rates.

Regional Insights

North America Cardiac Pacemaker Market Trends

North America, led by the U.S., is anticipated to command roughly 44.5% of the cardiac pacemaker market share by 2025. The region is characterized by an advanced regulatory environment, innovative healthcare infrastructure, and widespread insurance coverage, facilitating high device penetration rates.

The U.S. FDA’s streamlined device approval processes and support for expedited breakthrough device designations have accelerated the introduction of next-generation pacemakers, including leadless and MRI-compatible models. This innovation ecosystem is complemented by strong government funding and extensive clinical trial activity, ensuring continuous technology advancement.

The regional growth drivers include a high prevalence of aging populations with cardiovascular disorders, well-developed healthcare delivery systems, and rising physician awareness, accelerating pacemaker implantation rates.

Telemedicine integration and reimbursement expansions further boost the market size. Competitive dynamics reveal a balanced landscape with dominant incumbents investing heavily in R&D and emerging startups specializing in niche devices, shaping market evolution.

Europe Cardiac Pacemaker Market Trends

Europe represents approximately 37% of the global market in 2025, with Germany, the U.K., France, Spain, and Italy as pivotal markets. The region benefits from healthcare system harmonization under the European Union (EU)’s MDR, which standardizes clinical evaluation and post-market surveillance requirements, mitigating access delays. Germany’s advanced cardiac care infrastructure and the U.K.’s National Health Service (NHS), promoting cardiac interventions, drive significant pacemaker adoption volumes.

The Europe market is further propelled by demographic shifts toward older populations alongside increasing clinical guideline adoption endorsing pacemaker therapy in emerging indications beyond bradycardia, such as heart failure.

Significant investments in outpatient cardiac care models and specialized cardiac electrophysiology centers underline vertical growth aspects. Regional payer strategies are emphasizing cost containment to promote the adoption of minimally invasive and leadless devices. Strategic cross-border collaborations and clinical research consortia further facilitate technological diffusion.

Asia Pacific Cardiac Pacemaker Market Trends

Asia Pacific is the fastest-growing regional market for cardiac pacemakers, driven by burgeoning cardiovascular disease prevalence, expanding middle-class populations with increased healthcare access, and substantial investments in healthcare infrastructure spanning China, India, and ASEAN countries. Local governments are amplifying cardiac care capacity with initiatives supporting cardiac center development and physician training programs.

Efficiencies derived from local device manufacturing, lowered costs, and tailored distribution enable rapid pacemaker adoption in previously underpenetrated markets. Telecardiology and remote patient monitoring deployments are pioneering access in rural and semi-urban populations, enhancing follow-up care and therapy adherence.

Policy shifts enhancing health insurance penetration and medical tourism are additional growth catalysts. The Asia Pacific pacemaker market growth trajectory over the forecast period 2025 - 2032 is rooted in rising procedure volumes and market revenues, representing a critical focus for strategic commercial expansion.

Competitive Landscape

The global cardiac pacemaker market landscape maintains a moderately consolidated structure, with Medtronic, Abbott Laboratories, and Boston Scientific collectively controlling approximately 60% of the revenue share. These medical device giants dominate due to extensive R&D pipelines, broad portfolios across technology tiers, and robust global distribution and service networks, enabling superior customer engagement and rapid innovation adoption.

Following the leading trio, Tier 2 companies, including Biotronik SE & Co. KG, LivaNova PLC, and MicroPort Scientific Corporation, hold about 23% of the market. They compete through specialized innovations, niche clinical indications, and strategic localization in emerging markets.

The competitive positioning reflects a balance between technological sophistication and cost competitiveness, with market entrants aiming for differentiation through innovation, regulatory agility, and localized customer solutions.

Key Industry Developments

- In October 2025, Abbott launched a dual-chamber leadless pacemaker system using two tiny, wirelessly communicating devices placed in the right atrium and ventricle. Synchronizing beat-by-beat, it eliminates leads and surgical pockets and extends the AVEIR VR platform’s benefits to more patients, particularly those with bradycardia.

- In September 2025, Medtronic launched the global ELEVATE-HFpEF trial to study personalized conduction system pacing in up to 700 HFpEF patients using MRI-compatible pacemakers. The trial aims to assess whether tailored pacing improves symptoms and outcomes, marking a key step in expanding pacemaker use for broader cardiac conditions.

- In April 2025, Northwestern University engineers created the world’s smallest pacemaker, injectable via syringe for temporary use, especially in newborns with congenital heart defects. The dissolvable device, wirelessly controlled by light pulses from a wearable, regulates heart rhythm without leads, reducing complications of traditional temporary pacemakers and improving pediatric outcomes.

Companies Covered in Cardiac Pacemaker Market

- Medtronic PLC

- Abbott Laboratories (St. Jude Medical)

- Boston Scientific Corporation

- Biotronik SE & Co. KG

- LivaNova PLC

- MicroPort Scientific Corporation

- Lepu Medical Technology Co., Ltd.

- Shree Pacetronix Ltd.

- Osypka AG

- Oscor Inc.

- Medico S.p.A.

- EBR Systems Inc.

- Pacetronix

Frequently Asked Questions

The global cardiac pacemaker market is projected to reach US$5.7 Billion in 2025.

Rising global prevalence of cardiovascular disorders (CVDs), such as arrhythmias and bradycardia, particularly in aging populations, and expansion of therapeutic options due to technological advancements in leadless and MRI-compatible devices are driving the market.

The cardiac pacemaker market is poised to witness a CAGR of 3% from 2025 to 2032.

Increasing procedural volumes in emerging economies, integration of remote patient monitoring, and the shift toward minimally invasive procedures are key market opportunities.

Medtronic PLC, Abbott Laboratories (St. Jude Medical), and Boston Scientific Corporation are some of the key players in the market.