- Medical Devices

- Cardiac Biomarker Diagnostic Test Kits Market

Cardiac Biomarker Diagnostic Test Kits Market Size, Share, and Growth Forecast 2026 - 2033

Cardiac Biomarker Diagnostic Test Kits Market by Product Type (Brain Natriuretic Peptide (BNPs) Test Kits, Creatine Kinase MB (CK-MB) Test Kits, Troponin (I&T) Tests Kits, Myoglobin Test Kits, Others), by Indication (Angina Pectoris, Acute Myocardial Infarction, Congestive Heart Failure, Others), by End Use (Hospitals, Diagnostic Laboratories, Outpatient Clinics, Academic & Research Institutes), by Regional Analysis, 2026 - 2033

Cardiac Biomarker Diagnostic Test Kits Market Share and Trends Analysis

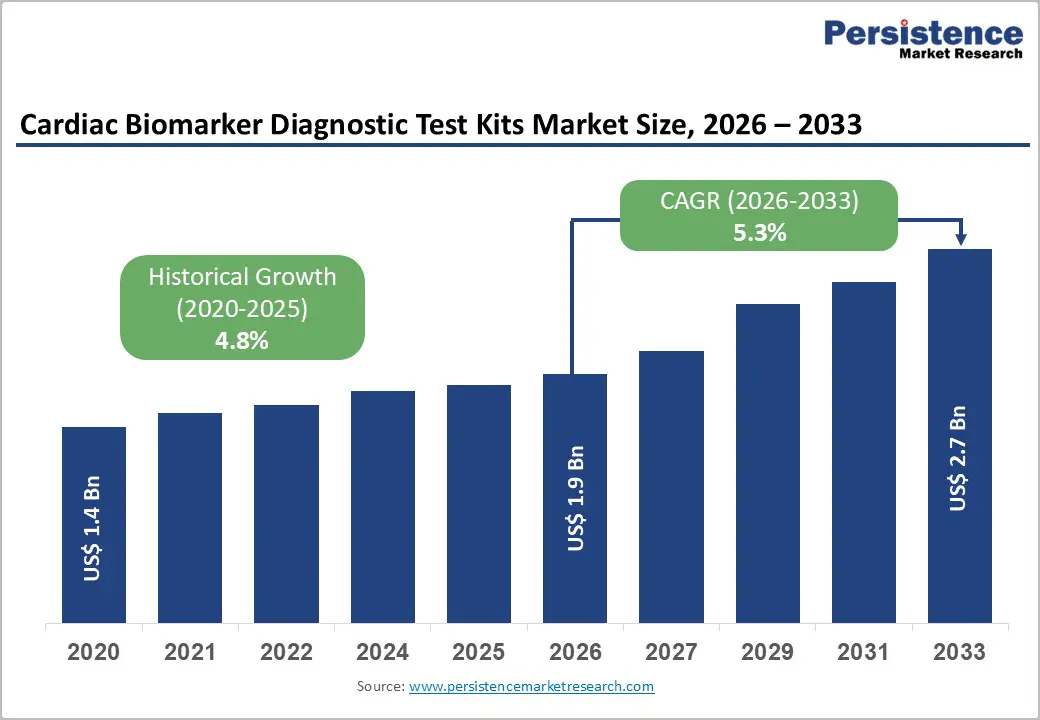

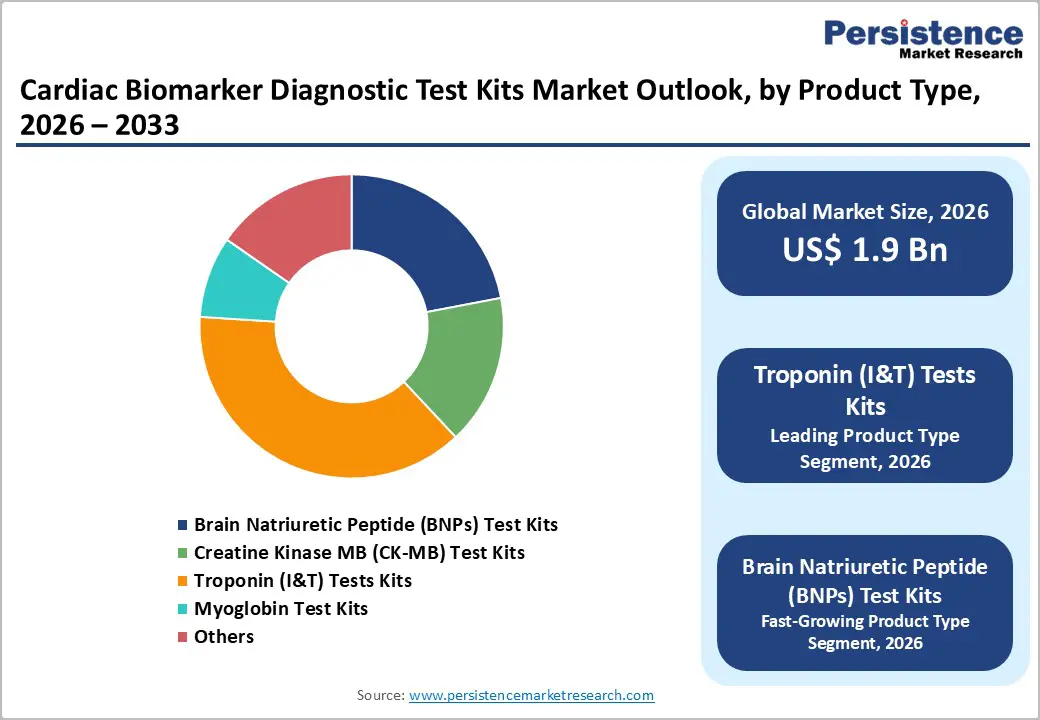

The global cardiac biomarker diagnostic test kits market size is expected to be valued at US$ 1.9 billion in 2026 and projected to reach US$ 2.7 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033. Growing cardiovascular disease burden, rapid adoption of high-sensitivity assays for early detection, and the shift toward point-of-care cardiac testing in emergency settings are the primary forces shaping this trajectory.

The rising incidence of acute myocardial infarction and heart failure, combined with aging populations in both developed and emerging economies, is expanding test volumes. Parallelly, hospitals and diagnostic laboratories are increasingly standardizing protocols around cardiac biomarkers such as troponins, BNP/NT proBNP, and CK MB in line with international cardiology guidelines, reinforcing recurring demand for high-performance diagnostic kits.

Key Industry Highlights:

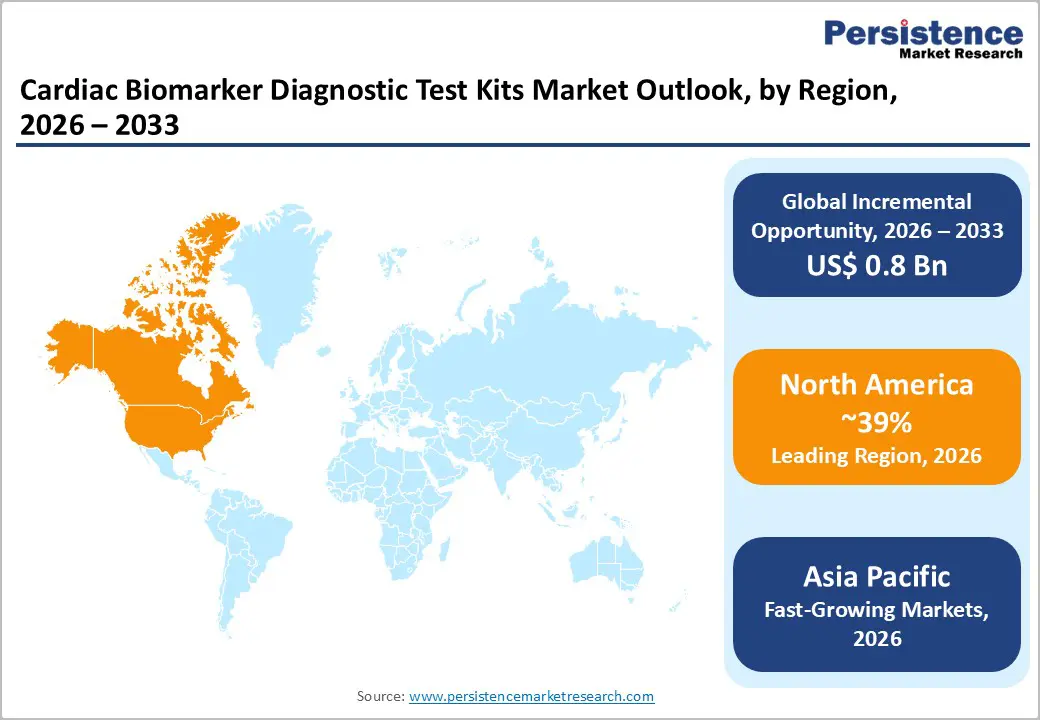

- North America remains the leading region for cardiac biomarker diagnostic test kits with about 39% share, driven by high cardiovascular disease prevalence, guideline-driven use of high-sensitivity troponin and BNP/NT proBNP, and strong presence of major diagnostic companies and advanced hospital networks.

- Asia Pacific is the fastest-growing regional market, expected to expand at CAGRs above 6–7% through 2032, supported by rising cardiovascular disease burdens, rapid hospital infrastructure development in China and India, and improving access to high-sensitivity assays in emerging healthcare systems.

- Troponin (I & T) test kits form the dominant product segment with roughly 38% share, reflecting their status as the gold-standard biomarker for myocardial infarction diagnosis and their central role in accelerated chest pain pathways recommended by international cardiology societies.

- BNP/NT proBNP test kits represent the fastest-growing segment, benefiting from their integration into heart failure diagnostic and management algorithms, rising heart failure prevalence, and the adoption of biomarker-guided chronic disease management programs aimed at reducing hospital readmissions.

- The key opportunity landscape centers on heart failure and chronic cardiovascular care, where expansion of natriuretic peptide testing, multi-marker risk stratification strategies, and point-of-care platforms can improve outcomes and support value-based care models in both developed and emerging markets.

| Key Insights | Details |

|---|---|

|

Cardiac Biomarker Diagnostic Test Kits Size (2026E) |

US$ 1.9 Bn |

|

Market Value Forecast (2033F) |

US$ 2.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.8% |

Market Dynamics

Drivers - Rising Global Burden of Cardiovascular Disease and Acute Coronary Syndromes

Cardiovascular diseases (CVDs) remain the leading cause of death worldwide, responsible for an estimated 17.9 million deaths annually according to the World Health Organization (WHO). A substantial share of these deaths are due to acute coronary syndromes, including myocardial infarction and unstable angina, where rapid diagnostic triage is critical. Emergency departments globally are seeing increasing chest pain admissions, and international guidelines from bodies such as the European Society of Cardiology (ESC) and the American Heart Association (AHA) recommend serial measurement of cardiac biomarkers, particularly high-sensitivity troponin, for diagnosis and risk stratification. With aging populations and rising prevalence of risk factors such as diabetes, hypertension, and obesity, especially in regions such as North America, Europe, and rapidly urbanizing parts of Asia Pacific, hospitals and diagnostic labs are expanding their use of standardized cardiac biomarker testing algorithms. This structural rise in testing volume directly supports sustained growth for cardiac biomarker diagnostic test kits across central labs, near-patient settings, and integrated health systems.

Advances in High-Sensitivity Assays and Point-of-Care Testing Integration

The rapid evolution of high-sensitivity assays, particularly high-sensitivity cardiac troponin (hs-cTnI and hs-cTnT) is a significant growth catalyst, as these assays enable earlier rule-in and rule-out of myocardial infarction, often within 1–3 hours of presentation. Their adoption has been supported by clinical evidence demonstrating improved diagnostic accuracy and reduced time to decision-making, which in turn shortens emergency department stays and can reduce healthcare costs. In parallel, the development of robust point-of-care testing (POCT) platforms for cardiac biomarkers, led by companies such as Abbott Laboratories Siemens Healthineers, and Roche is enabling the deployment of troponin and BNP testing in emergency rooms, ambulances, urgent care centers, and smaller hospitals lacking full central lab capacity. Integration of POCT with electronic medical records and hospital information systems is enhancing workflow efficiency and data traceability. As healthcare systems prioritize rapid triage and decentralized care models, demand for high-sensitivity and point-of-care cardiac biomarker diagnostic test kits is expected to expand steadily across both developed and emerging markets.

Restraints - Reimbursement and Cost-Containment Pressures in Key Healthcare Systems

Despite strong clinical need, adoption and utilization patterns of cardiac biomarker test kits are influenced by reimbursement policies and cost containment measures, particularly in publicly funded healthcare systems. Hospitals face budget constraints and must balance the clinical value of high-sensitivity assays with their per-test cost, leading some facilities to limit repeat testing or delay adoption of the latest assay generations. In certain markets, reimbursement rates for laboratory tests have been subject to downward revisions or bundling into diagnosis-related group (DRG) payments, constraining laboratory budgets. These pressures can slow replacement of legacy assays and limit uptake of more expensive multi-marker panels, especially in smaller hospitals and resource-constrained regions.

Variability in Clinical Practice and Limited Awareness in Low-Resource Settings

Another barrier arises from heterogeneity in clinical practice and limited awareness or training regarding optimal use of cardiac biomarkers in some regions. While guidelines from organizations such as the ESC and AHA/ACC strongly recommend high-sensitivity troponin-based diagnostic algorithms, implementation is uneven, particularly in low- and middle-income countries where access to high-quality assays, standardized protocols, and trained staff may be limited. In some settings, clinicians continue to rely heavily on electrocardiograms and clinical assessment alone, under-utilizing biomarker-guided strategies. Limited laboratory infrastructure, intermittent supply chains, and lack of quality assurance programs can further restrict the widespread use of advanced cardiac biomarker test kits, slowing market penetration despite a significant underlying disease burden.

Opportunities - Expansion of Heart Failure Management and BNP/NT-proBNP Testing

One of the most promising opportunities lies in the expanding use of Brain Natriuretic Peptide (BNP) and NT-proBNP testing for heart failure diagnosis and management. Heart failure affects more than 64 million people globally by some epidemiological estimates, with incidence rising alongside population aging and improved survival after myocardial infarction. Clinical guidelines from the ESC and AHA endorse natriuretic peptide testing as a core component of heart failure workup and prognostic assessment. BNP/NT-proBNP levels aid in distinguishing cardiac from non-cardiac causes of dyspnea and in monitoring response to therapy. As hospitals and outpatient clinics increasingly adopt guideline-driven heart failure pathways, often embedded in chronic disease management and telehealth programs the use of natriuretic peptide test kits is expected to outpace overall market growth. This positions BNP test kits as the fastest-growing product segment, particularly where payers incentivize reduced readmission rates and better chronic heart failure control through biomarker-guided care.

Growing Adoption of Multi-Marker Strategies and Personalized Risk Stratification

The shift toward precision cardiology and personalized risk stratification is creating opportunities for expanded use of multi-marker test panels that combine troponin, CK-MB, myoglobin, and natriuretic peptides, as well as emerging biomarkers such as high-sensitivity C-reactive protein (hs-CRP) and copeptin. Multi-marker approaches can improve differentiation between unstable angina, type 1 and type 2 myocardial infarction, and non-ischemic cardiac conditions. Health systems are increasingly interested in algorithms that combine biomarker profiles with clinical and imaging data to refine risk prediction, shorten length of stay, and optimize use of invasive procedures. Diagnostic companies are responding by developing integrated panels and algorithms, sometimes supported by digital decision-support tools and artificial intelligence platforms embedded in analyzers or laboratory middleware. Laboratories that adopt such advanced panels may shift test utilization toward higher-value cardiac biomarker kits, offering vendors opportunities to differentiate through clinical evidence, outcomes data, and integrated software solutions that go beyond single-analyte testing.

Category-wise Analysis

Product Type Insights

Troponin (I & T) test kits form the leading product segment, accounting for approximately 38% of the global cardiac biomarker diagnostic test kits market in 2025. Cardiac troponins are considered the gold-standard biomarkers for myocardial injury, and high-sensitivity assays are now entrenched in diagnostic pathways for acute coronary syndromes worldwide. Clinical guidelines from the ESC, AHA, and ACC explicitly recommend troponin as the primary biomarker for myocardial infarction diagnosis, making troponin testing nearly universal in emergency departments managing chest pain. The widespread transition from conventional to high-sensitivity troponin assays further solidifies this segment’s dominance, as hospitals standardize protocols and invest in compatible analyzers. Meanwhile, BNP/NT-proBNP test kits represent the fastest-growing product subsegment, supported by their expanding use in heart failure screening, risk stratification, and chronic disease management programs run by hospitals and outpatient clinics.

Indication Insights

Among indications, acute myocardial infarction (AMI) is expected to be the leading segment in terms of test utilization, with an estimated market share around 40% in 2025. AMI requires rapid, accurate differentiation from non-cardiac chest pain, and current clinical algorithms rely heavily on serial troponin measurements in combination with ECG findings. Increasing use of accelerated diagnostic protocols—such as 0/1 hour or 0/2 hour high-sensitivity troponin algorithms has increased the number of tests performed per patient encounter, reinforcing test kit consumption. At the same time, congestive heart failure is anticipated to be the fastest-growing indication segment, with test demand driven by natriuretic peptide use in emergency departments, inpatient wards, and ambulatory heart failure clinics. The rising prevalence of heart failure, frequent hospitalizations, and emphasis on reducing readmissions through biomarker-guided therapy adjustments are encouraging more routine BNP/NT-proBNP testing, especially in older populations and those with multiple comorbidities.

End-user Insights

Hospitals constitute the largest end-use segment for cardiac biomarker diagnostic test kits, likely accounting for around 55–60% of the total market share in 2025. Emergency departments, intensive care units, and cardiology wards rely extensively on cardiac biomarker testing to triage chest pain, monitor post-intervention patients, and manage decompensated heart failure. Large tertiary and quaternary care hospitals often run high-throughput analyzers capable of processing thousands of troponin and BNP tests daily, supporting both inpatients and referred cases. Diagnostic laboratories including independent reference labs and integrated health system labs represent the second major end-use segment and are expected to be the fastest-growing, driven by outsourcing trends, consolidation of lab services, and expansion of specialized cardiology testing services. Outpatient clinics and academic & research institutes contribute smaller but growing shares; outpatient centers are increasingly integrating point-of-care or near-patient biomarker testing for rapid decision-making, while research institutes use advanced assays for clinical trials and biomarker discovery studies in cardiology.

Regional Insights

North America Cardiac Biomarker Diagnostic Test Kits Market Trends and Insights

North America is the leading regional market, with an estimated 39% share in 2025, underpinned by high cardiovascular disease prevalence, strong guideline adoption, and advanced diagnostic infrastructure. The United States accounts for the majority of regional demand, with emergency departments routinely implementing high-sensitivity troponin protocols and heart failure programs incorporating BNP/NT proBNP testing in line with AHA/ACC and Heart Failure Society of America (HFSA) guidelines. High healthcare expenditure per capita and widespread health insurance coverage support broad access to biomarker testing in hospital and outpatient settings.

Asia Pacific Cardiac Biomarker Diagnostic Test Kits Market Trends and Insights

Asia Pacific is the fastest-growing regional market, with projected CAGRs higher than 6–7% between 2025 and 2032. The region is characterized by a high and rising burden of cardiovascular disease, rapidly expanding healthcare infrastructure, and increasing adoption of Western-style clinical guidelines. Countries such as China, Japan, India, and South Korea are at the forefront of market growth. In China, urbanization, lifestyle changes, and improved access to hospital care drive high rates of diagnosis for acute coronary syndromes and heart failure, which in turn boosts demand for troponin and BNP testing. Government initiatives to strengthen emergency medical services and regional chest pain centers are supporting broader deployment of high-sensitivity assays.

Japan, with its advanced healthcare system and aging population, has long used cardiac biomarkers in hospital settings, while manufacturers including Siemens AG, F. Hoffmann-La Roche Ltd., and regional players support a diverse installed base of analyzers. In India and ASEAN countries, the build-out of tertiary care hospitals, specialty cardiac centers, and private diagnostic laboratory chains is creating new opportunities for cardiac biomarker test kits despite ongoing affordability and access challenges. Manufacturing advantages and lower operating costs in parts of Asia Pacific are also encouraging leading diagnostic companies to expand production and assembly operations in the region, improving supply availability and enabling tailored offerings for local markets.

Competitive Landscape

The cardiac biomarker diagnostic test kits market is highly competitive and moderately consolidated, with major diagnostics firms and agile niche innovators continually refining their offerings and strategies to gain advantages. Competition centers on assay accuracy, turnaround time, platform interoperability, and integration with digital health tools, as companies invest in automation, high-sensitivity tests, and connected analytics to differentiate products. Strategic collaborations, mergers, and R&D investments are common as firms expand geographic reach and broaden portfolios to address both centralized lab and point-of-care needs. Price competition and regional players introducing cost-effective alternatives further intensify rivalry in this dynamic landscape.

Key Developments

- In November 2025, the Heart Foundation’s Lubdub initiative launched clinical studies to evaluate next-generation cardiac diagnostic tools. Researchers trialled a wearable ECG patch and a saliva-based biomarker test across metropolitan health centres, comparing them with standard hospital diagnostics to assess accuracy and comfort. Following this, the research expanded into community health settings to explore use in regional and remote populations. An additional study tested the saliva device in emergency departments for rapid triage of patients with chest pain.

Companies Covered in Cardiac Biomarker Diagnostic Test Kits Market

- Abbott Laboratories

- Danaher Corporation

- Bio-Rad Laboratories

- Thermo Fisher Scientific, Inc.

- Becton, Dickinson and Company

- F. Hoffmann-La Roche Ltd.

- Siemens AG

- BioMérieux SA

- Randox Laboratories Ltd.

- Siemens Healthineers

- Beckman Coulter

- Ortho Clinical Diagnostics

- QuidelOrtho Corporation

- PerkinElmer

- Sysmex Corporation

Frequently Asked Questions

The global cardiac biomarker diagnostic test kits market is expected to be valued at approximately US$ 1.9 billion in 2026, supported by growing cardiovascular disease burden, widespread adoption of high-sensitivity troponin assays, and expanded BNP/NT‑proBNP testing across hospitals and diagnostic laboratories worldwide.

Demand is driven by rising incidence of acute coronary syndromes and heart failure, guideline-driven use of high-sensitivity troponin and natriuretic peptides recommended by bodies like the ESC and AHA/ACC, the need for rapid triage in emergency departments, and growing deployment of point-of-care cardiac biomarker platforms in hospitals and outpatient settings.

North America is the leading regional market, with an estimated 39% share in 2025, reflecting high cardiovascular disease prevalence, strong adoption of evidence-based diagnostic pathways, advanced laboratory and hospital infrastructure, and the presence of major global diagnostics manufacturers supplying troponin and BNP/NT proBNP assays.

A major growth opportunity lies in the expansion of heart failure management and chronic cardiovascular care programs that use BNP/NT proBNP and multi-marker strategies for diagnosis, risk stratification, and therapy monitoring, particularly in rapidly developing healthcare systems across Asia Pacific and other emerging regions aiming to reduce hospitalizations and improve long-term outcomes.

Key players include Abbott Laboratories, F. Hoffmann-La Roche Ltd., Siemens AG and Siemens Healthineers, Danaher Corporation (including Beckman Coulter), BioMérieux SA, Thermo Fisher Scientific, Inc., Bio-Rad Laboratories, Becton, Dickinson and Company, and Randox Laboratories Ltd., all of which offer comprehensive cardiac biomarker assay portfolios and maintain strong clinical and regulatory footprints globally.