- Medical Devices

- Global Cardiac Marker Analyzer Market

Global Cardiac Marker Analyzer Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Cardiac Marker Analyzer Market by Product Type (Immuno-Fluorescence Analyzers (IFA), Magnetic Immuno-Chromatographic Assay (MICA) Analyzers, Chemiluminiscenece Immunoassay (CLIA) Analyzers, Radioimmunoassay (RIA) Analyzers, Enzyme Immunoassay (EIA) Analyzers), Nature (Hospitals, Diagnostic Centers, Academic and Research institutes), and Regional Analysis from 2026 to 2033

Cardiac Marker Analyzer Market Size and Trends Analysis

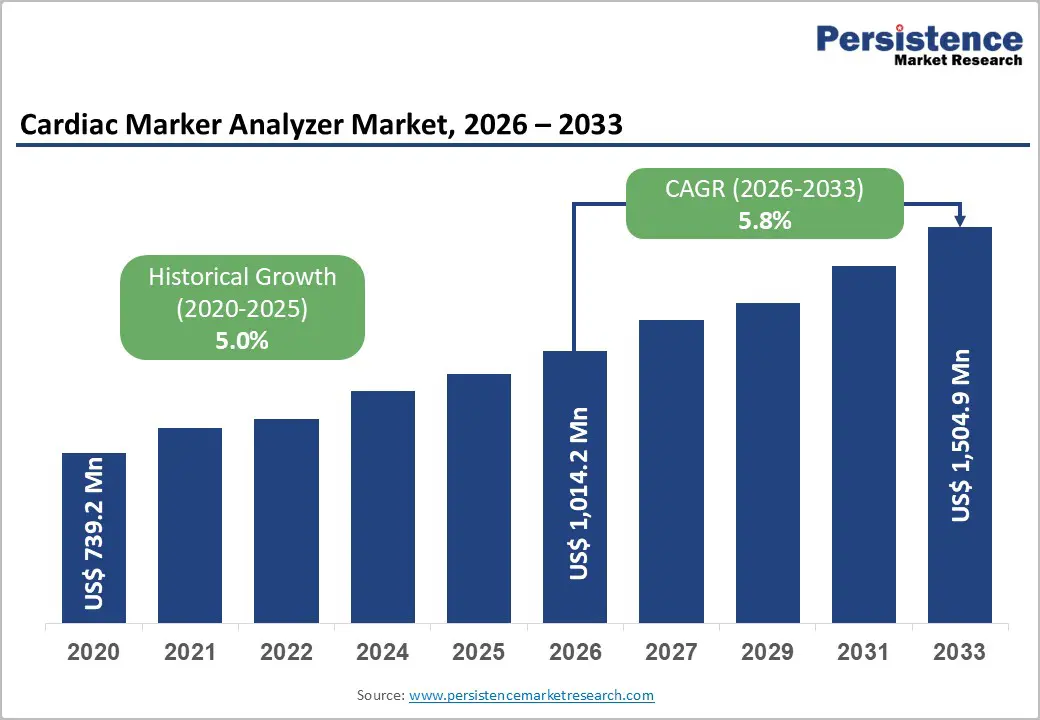

The global cardiac marker analyzer market is estimated to grow from US$ 1,014.2 Mn in 2026 to US$ 1,504.9 Mn by 2033. The market is projected to record a CAGR of 5.8% during the forecast period from 2026 to 2033.

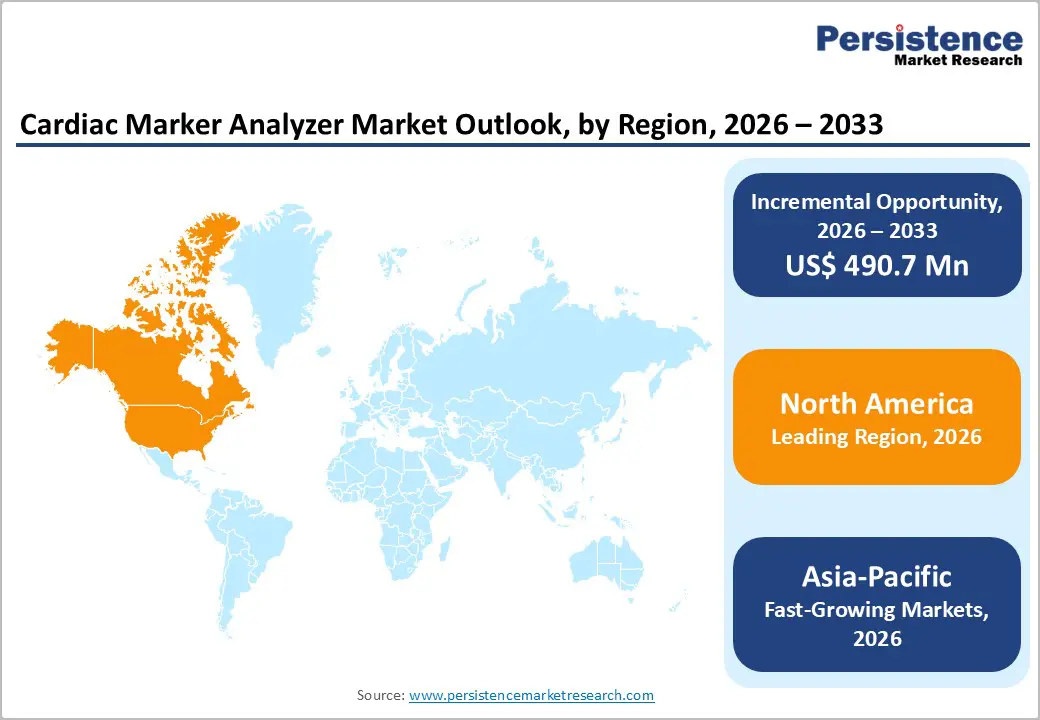

The global cardiac marker analyzer market is growing steadily, driven by rising cardiovascular disease prevalence, increasing emergency admissions, and demand for rapid diagnostics. North America holds the largest share due to advanced healthcare infrastructure, while Asia-Pacific is the fastest-growing region, supported by expanding laboratory networks, rising test volumes, improving healthcare access, and growing awareness of early cardiac diagnosis.

Key Industry Highlights

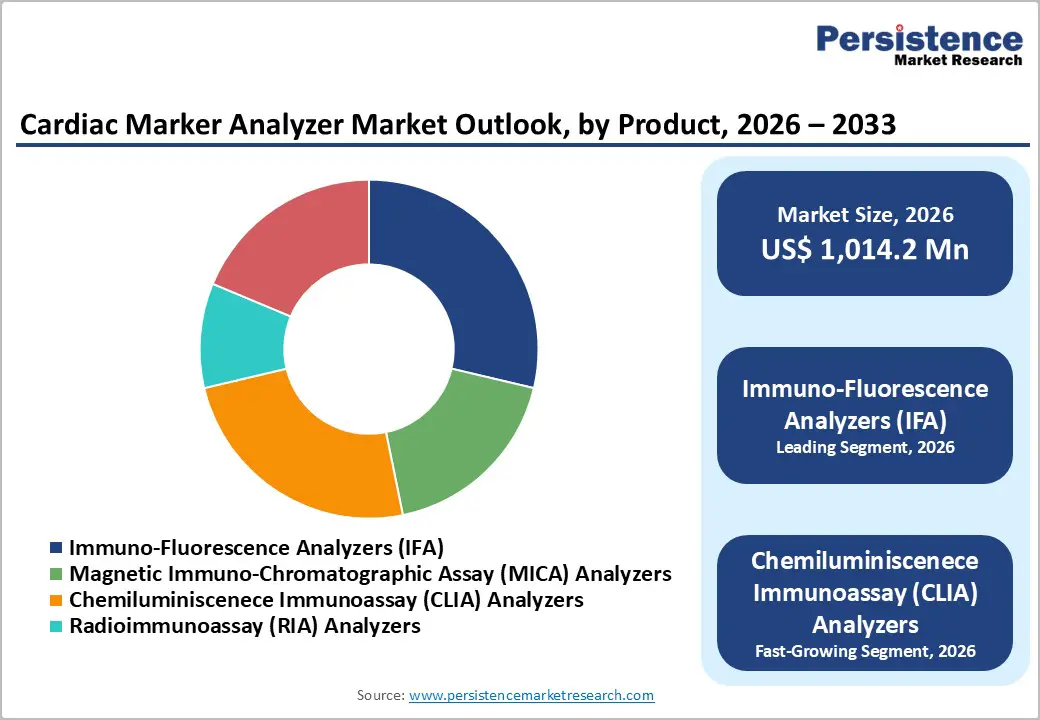

- Dominant Segment: Immuno-Fluorescence Analyzers (IFA) dominate a significant portion of the cardiac marker analyzer market in 2025 with 28.7% share, valued for high specificity and early cardiac biomarker detection. Automation, multiplex testing capability, and reliable performance in hospital and specialty laboratories drive their adoption. IFAs are also among the fastest-growing segments, supported by demand for rapid and accurate cardiac diagnostics.

- Dominant Region: North America holds the largest market share in 2025 with 43.6% share, supported by advanced diagnostic infrastructure, high cardiovascular disease burden, and favorable reimbursement. Asia-Pacific is the fastest-growing region, driven by expanding laboratory networks, rising cardiac testing volumes, and improving healthcare access.

- Market Drivers: Growth is driven by increasing prevalence of cardiovascular diseases, rising emergency admissions, demand for early and accurate diagnosis, technological advancements in immunoassay platforms, and growing adoption of point-of-care testing.

- Market Opportunity: Key opportunities include high-sensitivity troponin testing, point-of-care analyzers, automation and AI-enabled diagnostics, integration with hospital information systems, and rapid expansion in emerging economies with improving diagnostic infrastructure.

| Global Market Attributes | Key Insights |

|---|---|

| Global Cardiac Marker Analyzer Market Size (2026E) | US$ 1,014.2 Mn |

| Market Value Forecast (2033F) | US$ 1,504.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.0% |

Market Dynamics

Driver: Rising prevalence of cardiovascular diseases (CVDs) globally

Cardiovascular diseases (CVDs) remain the leading cause of death globally, claiming an estimated 17.9 million lives annually according to the World Health Organization, which is nearly one third of all global deaths. The burden of acute myocardial infarction and other cardiac events drives urgent demand for timely diagnosis and intervention. Cardiac marker analyzers are integral in emergency settings to detect biomarkers such as troponins, enabling clinicians to confirm or rule out heart attacks quickly and accurately. This increasing disease prevalence correlates with ageing populations, lifestyle changes, and expanding healthcare access, prompting hospitals and clinics worldwide to adopt advanced cardiac diagnostic platforms to improve outcomes.

The growing incidence of heart disease also translates into rising healthcare utilization and expenditures in both developed and emerging regions. In the United States, heart disease affects approximately one in every four deaths, reflecting persistent high demand for cardiac care. Early and precise biomarker detection not only reduces mortality risk but also shortens hospital stays and optimizes resource allocation, which is especially critical in emergency departments. As healthcare systems prioritize value based care and rapid clinical decision making, cardiac marker analyzers are increasingly deployed across diagnostic workflows, reinforcing their role as essential tools in modern cardiovascular care pathways.

Restraints: High cost of advanced analyzers and reagents limiting adoption in smaller labs

Advanced immunoassay and high sensitivity cardiac marker analyzers represent substantial capital investments for healthcare providers, with unit prices ranging from USD 150,000 to 500,000 for premium platforms. These upfront costs are compounded by ongoing operational expenses including reagents, calibration materials, and specialized maintenance plans, creating financial pressure on hospital budgets and smaller diagnostic centers. In cost sensitive healthcare environments, especially in low income countries or rural regions, such high expenditures can delay procurement decisions and restrict widespread deployment. Consequently, facilities may continue relying on older, less sensitive diagnostic methods or centralized laboratory testing, which hampers broader market penetration for cutting edge analyzers.

Reagent costs further elevate the cost burden, with individual cardiac biomarker tests ranging from USD 25 to 75 per patient depending on the assay panel and technology. Smaller laboratories often face reagent waste due to short shelf lives and minimum order quantities, reducing cost efficiency. These economic constraints are amplified where reimbursement frameworks do not fully cover advanced diagnostics, leading providers to absorb additional costs. As a result, the high total cost of ownership limits adoption rates in underfunded health systems and underscores the need for cost effective alternatives or supportive financing mechanisms to enable broader access to high performance cardiac diagnostic technologies.

Opportunity: Development and adoption of point-of-care (POC) cardiac marker analyzers

The continued growth of point of care (POC) diagnostics presents a major opportunity for the cardiac marker analyzer market, driven by the need for rapid, near-patient testing. POC cardiac marker tests enable clinicians to detect heart attacks and other acute cardiac events quickly, reducing delays in diagnosis and allowing timely treatment decisions. Hospitals, emergency rooms, and urgent care settings benefit from faster turnaround times compared with traditional central laboratories, improving patient outcomes and supporting efficient clinical workflows. The increasing focus on early intervention and preventive care further encourages the adoption of these rapid diagnostic solutions.

POC solutions also enhance accessibility in outpatient clinics, mobile health units, and remote regions, providing compact, user-friendly platforms that deliver actionable results within minutes. As healthcare systems prioritize patient-centered care and decentralization of services, portable cardiac marker analyzers are increasingly integrated into routine diagnostics. Advancements in miniaturized immunoassay technologies, digital connectivity, and automated testing further support this trend, making POC analyzers a practical tool for improving cardiac care delivery and expanding diagnostic reach across diverse healthcare settings.

Category-wise Analysis

By Product, Immuno-Fluorescence Analyzers (IFA) Dominates the Cardiac Marker Analyzer Market

Immuno-Fluorescence Analyzers (IFA) occupies 28.7% share of the global market in 2025, because they combine high analytical sensitivity with rapid turnaround, critical for diagnosing acute cardiac events. Immunofluorescence techniques detect minute concentrations of biomarkers such as troponin with superior sensitivity compared with older colorimetric methods, supporting early intervention in suspected myocardial infarction cases. Regulatory bodies like the U.S. Centers for Disease Control and Prevention note that high sensitivity cardiac biomarker testing improves risk stratification and patient outcomes in emergency settings. High dependency on accurate point of care diagnostics in emergency departments where every 30 minute delay in diagnosis increases morbidity drives preference for IFA systems that deliver results within 15–30 minutes, expanding their utilization in hospitals and urgent care facilities.

By End User, Hospitals dominates due to high acute cases, infrastructure, rapid diagnostics, and mortality reduction

Hospitals dominate the cardiac marker analyzer market because they manage the highest volume of acute cardiac cases, requiring rapid and accurate diagnostics. In the United States, for example, heart disease remains the leading cause of death, accounting for about 1 in every 5 deaths, and many of these patients first present through hospital emergency departments. Early and precise detection of cardiac biomarkers such as troponin is critical in hospitals to guide interventions that reduce mortality. Hospitals also have the infrastructure, staffing, and budget to support advanced analyzers, unlike smaller clinics. Additionally, the World Health Organization reports that over three quarters of CVD deaths occur in low and middle income countries, where hospital diagnostic capacity is growing, further reinforcing hospitals’ central role in cardiac marker testing.

Regional Insights

North America Cardiac Marker Analyzer Market Trends

North America dominates the cardiac marker analyzer market with 43.6% share in 2025, because of its high burden of cardiovascular disease and advanced healthcare infrastructure. In the United States alone, cardiovascular disease remains the leading cause of death, with approximately 805,000 heart attacks annually and heart disease accounting for a substantial share of mortality and healthcare utilization, driving demand for rapid and precise cardiac diagnostics. Additionally, the region conducts a significant proportion of global diagnostic tests supported by extensive hospital laboratory networks, automation adoption, and strong insurance coverage enabling broad deployment of advanced cardiac marker analyzers. These factors together sustain North America’s leadership in the global market.

Europe Cardiac Marker Analyzer Market Trends

Europe is an important region in the cardiac marker analyzer market because cardiovascular diseases (CVDs) exert a substantial health burden and drive significant demand for diagnostic testing. In the WHO European Region, CVDs cause approximately 4.2 million deaths annually, accounting for about 42.5% of all deaths, with heart attacks and strokes representing the majority of these fatalities, underscoring continual clinical need for early cardiac marker detection. Additionally, diseases of the circulatory system accounted for 32.4% of deaths in the EU in 2022, reflecting high prevalence across diverse populations and healthcare settings. Europe’s well developed healthcare infrastructure and widespread laboratory services further support adoption of advanced cardiac diagnostics, reinforcing its strategic importance in the global market.

Asia-Pacific Cardiac Marker Analyzer Market Trends

Asia Pacific is the fastest growing region in the cardiac marker analyzer market because cardiovascular disease (CVD) burden is rising sharply and healthcare capacity is expanding across diverse countries. In the Asia Pacific, CVDs account for a substantial share of deaths, with heart disease and stroke contributing to nearly 40% of total mortality in the Western Pacific and about a quarter in South East Asia, reflecting enormous clinical need for cardiac diagnostics. Rapid population ageing, urbanisation, and increases in risk factors such as hypertension and diabetes are driving more cardiac events, prompting hospitals and clinics to invest in marker analyzers to improve early detection and care pathways. Additionally, expanding healthcare infrastructure and government initiatives to strengthen primary care and diagnostic services support faster adoption of advanced analyzers, making the region a high growth market.

Market Competitive Landscape

Leading cardiac marker analyzer market companies focus on high-sensitivity, rapid, and automated diagnostic systems. Investments target advanced immunoassay technologies, point-of-care solutions, and integration with hospital information systems. R&D emphasizes accuracy, throughput, and clinical reliability, while collaborations with healthcare providers enhance adoption. These strategies drive innovation, expand cardiac diagnostic applications, and strengthen global market penetration.

Key Industry Developments:

- In December 2025, Siemens Healthineers advanced coronary artery disease management by launching its Syngo.CT Coronary Cockpit software. The solution aimed to streamline cardiac CT imaging workflows, enhance diagnostic accuracy, and support clinicians in evaluating coronary artery conditions more efficiently. This software provided integrated tools for analysis, visualization, and reporting, helping hospitals and cardiology centers improve patient care and decision-making in coronary artery disease management.

- In November 2025, Thermo Fisher Scientific announced the acquisition of Clario to strengthen its clinical insights capabilities and accelerate innovation. The acquisition aimed to expand Thermo Fisher’s offerings in clinical research and data analytics, enabling faster, more efficient development of diagnostics and treatments. This strategic move enhanced the company’s ability to provide integrated solutions for clinical trials and patient-centered healthcare.

Companies Covered in Global Cardiac Marker Analyzer Market

- Abbott Laboratories

- Siemens Healthineers AG

- Thermo Fisher Scientific

- F. Hoffmann-La Roche Ltd.

- Danaher (Beckman Coulter Inc.)

- Quidel Corporation

- Trinity Biotech PLC

- PHC Holdings Corporation (LSI Medience Corporation)

- Boditech Med Inc.

- Agappe Diagnostics Ltd

- Hangzhou Laihe Biotech Co. Ltd

- CardioGenics Holdings Inc.

- Others

Frequently Asked Questions

The global cardiac marker analyzer market is projected to be valued at US$ 1,014.2 Mn in 2026.The global cardiac marker analyzer market is projected to be valued at US$ 1,014.2 Mn in 2026.

Rising cardiovascular disease prevalence, emergency admissions, demand for rapid diagnostics, advanced immunoassay adoption, and awareness.

The global cardiac marker analyzer market is poised to witness a CAGR of 5.8% between 2026 and 2033.

Point-of-care analyzers, high-sensitivity troponin tests, automation, digital integration, emerging economies, and rapid cardiac diagnostics expansion.

Abbott Laboratories, Siemens Healthineers AG, Thermo Fisher Scientific, F. Hoffmann-La Roche Ltd., Danaher (Beckman Coulter Inc.), Quidel Corporation.